Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- US FED (BBG): I Changed My Mind. The Fed Needs to Cut Rates Now: Bill Dudley

- MNI US: Tumultuous Political Period Means Time Needed For Polls To Stabilise

- MNI BOC: BOC (MNI): BOC Cuts Rates Again, Says More Could Be Justified

- MNI US DATA: New Home Sales Activity And Prices Continue To Cool

- MNI US DATA: Services PMI Gains Continue To Diverge From Soft Manufacturing

US

US FED (BBG): I Changed My Mind. The Fed Needs to Cut Rates Now: Bill Dudley

- Waiting until September unnecessarily increases the risk of a recession. I’ve long been in the “higher for longer” camp, insisting that the US Federal Reserve must hold short-term interest rates at the current level or higher to get inflation under control.

CANADA

BOC (MNI): BOC Cuts Rates Again, Says More Could Be Justified

The Bank of Canada cut interest rates for a second time by 25 bps to +4.5% and said more cuts could be justified if inflation slows as expected. Governor Macklem said while risks to the outlook are balanced "the downside risks are taking on increased weight in our monetary policy deliberations."

- "If inflation continues to ease broadly in line with our forecast, it is reasonable to expect further cuts in our policy interest rate. The timing will depend on how we see these opposing forces playing out."

- Macklem said that progress back to target will likely be uneven. Base effects from gasoline are expected to pull inflation down in the second half of this year before edging up again.

- BoC revised down the 2024 growth forecast from +1.5% to +1.2%, and expects excess supply to counter shelter inflation and other service price increases.

- BoC sees signs wage growth is easing, but noted that the rate is still elevated.

- The press release said the Canadian dollar has been relatively stable. Economists have been forecasting the extent to which the BoC can diverge from the Fed before CAD weakness emerges.

NEWS

US (MNI): Tumultuous Political Period Means Time Needed For Polls To Stabilise

There is significant focus on the new opinion polls coming out after President Joe Biden's withdrawal from the race. There are two polls from well-known outlets (Ipsos and YouGov) carried out following Biden's withdrawal with VP Kamala Harris as the (overwhelmingly likely) Democrat nominee.

- The latest from YouGov has Republican Donald Trump on 44%, ahead of Harris on 41%. Meanwhile, the Ipsos poll for Reuters has Harris leading Trump by 44% to 42%. Both of these results are within the margin of error.

- Given the tumultuous nature of the news cycle - the debate that set off the chain reaction for Biden's withdrawal occured under a month ago and it is only 11 days since the attempted assassination of Trump - it is likely that opinion polling will remain volatile in the short term.

US (MNI): MSNBC-Harris Campaign Also Considering Buttigieg For VP

Kyle Griffin as MSNBC posts on X: "The Harris campaign is ALSO considering Transportation Secretary Pete Buttigieg as a possible running mate." On the afternoon of 23 July, Griffin posted that the Harris campaign had requested vetting materials from the following Democratic politicians: NC Gov. Roy Cooper, PA Gov. Josh Shapiro, AZ Sen. Mark Kelly, MI Gov. Gretchen Whitmer, and MN Gov. Tim Walz. Around 9 hours later, Griffin posts that the Harris campaign is also considering Kentucky Gov. Andy Beshear.

US (MNI): US: Next Week's House Votes Cancelled; Recess From 25 July Amid GOP Divisions:

The House of Representatives' Republican leadership has confirmed that no votes will take place the week starting 29 July, meaning the last vote will take place on 25 July at 1045ET. The House will then enter summer recess, returning on 9 September. This will leave around three weeks of sitting before the November election.

US TSYS Curves Twist to Least Inverted Levels Since Oct'23

- Treasury futures look to finish near late session lows Wednesday, curves twisting to the least inverted levels since October 2023 (2s10s tapped -13.040 high). After the bell, Sep'24 10Y futures traded -7 at 110-21 just below initial technical support of 110-21+ (20D EMA).

- Short end rates well bid after former NY Fed Pres Dudley suggested rate cuts warranted now, not later in the year. In turn: projected rate cut pricing into year end are gained vs. this morning's levels (*): July'24 at -5.5% w/ cumulative at -1.4bp at 5.315%, Sep'24 cumulative -27.3bp (-25bp), Nov'24 cumulative -42.8bp (-40.1bp), Dec'24 -65.3bp (-62.8bp).

- Treasury futures holding near early session highs, drawing modest sell interest after mixed Wholesale/Retail Inventories data, Advanced Goods Trade Balance slightly lower than expected.

- Futures remain mixed after lower than expected New Home Sales for June. Curves remain steeper with intermediates to long end underperforming since the mixed flash PMI data came out.

- Tsy futures pare gains slightly after the $70B 5Y note auction (91282CLC3) tail: drawing 4.121% high yield vs. 4.111% WI; 2.40x bid-to-cover vs. 2.36x for the prior auction.

- Focus turns to Thursday's GDP, Core PCE Weekly Claims and 7Y Note Sale.

OVERNIGHT DATA

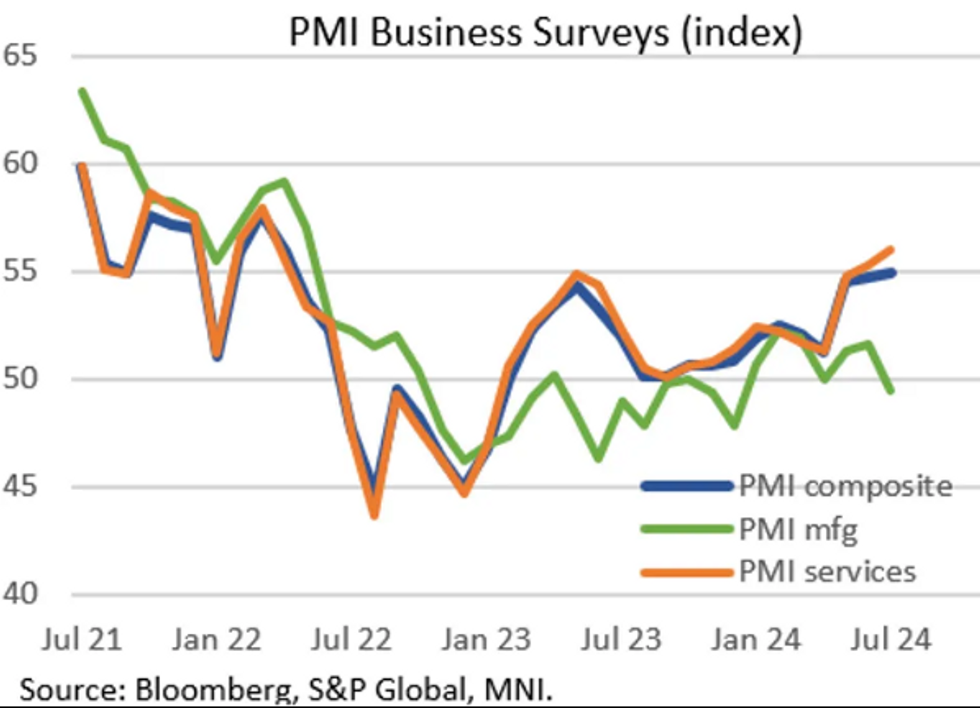

US DATA (MNI): Services PMI Gains Continue To Diverge From Soft Manufacturing

US PMI readings continued to diverge in July's flash report: the Manufacturing reading unexpectedly fell into contractionary territory at 49.5 (51.6 expected and prior), with Services unexpectedly rising to 56.0 (54.9 expected, 55.3 prior).

- The Services reading was the highest since March 2022, maintaining the upward momentum seen in the sector since 3Q 2023, while Manufacturing was the weakest (and first contractionary) reading since December 2023.

- The S&P Global report noted that the data is consistent with GDP growth of 2.5% annualized (vs 2.0% signaled by PMIs for 2Q - we get national accounts data Thursday), while the prices charged gauges are consistent with the Fed's 2% target.

US DATA (MNI): New Home Sales Activity And Prices Continue To Cool

New home sales totaled 617k in June, below the 640k expected and 621k prior (+2k upward revision), amid a soft report overall.

- June's sales marked the lowest seasonally-adjusted annual rate since November 2022, and came alongside a 0.1% Y/Y decline in median prices ($417.3k), the 6th in 7 months. While selling prices were the highest since March, those figures are not seasonally-adjusted.

- The flat price growth in new homes contrasts with modest positive existing home price readings (+4.1% Y/Y in June), with both inventory and lingering high mortgage rates weighing.

- With 476k new homes for sale at the end of the month - the most since 2008 - there is now 9.3 months of supply on the market, up from 9.1 prior. While that is lower than the 10.6 month peak in July 2022, it's up from 7.7 a year earlier and is clearly trending higher again.

US DATA (MNI): Mixed Mortgage Undercurrents And Signs Of Tighter Lending Conditions

MBA mortgage applications fell a seasonally adjusted 2.2% last week as they chipped away at the 3.9% increase in the week prior.

- Purchase applications fell further (-4.0% after -2.7%) whilst refinance applications consolidated a particularly firm increase (0.3% after 15.2%) for highs since Aug 2022.

- Purchase applications have seen little relief from a further decline in the 30Y mortgage rate, down another 5bps to 6.82% for technically the lowest since February.

- This easing hasn’t been reflected in jumbo loans though, where the rate actually ticked up 2bps to 7.09%.

- It leaves a regular-jumbo spread of -27bps at one of the most negative readings since late 2020/early 2021. That can be a sign of a tightening in lending conditions but would need to be repeated for what can be volatile data.

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 430.61 points (-1.07%) at 39929.54

- S&P E-Mini Future down 121 points (-2.16%) at 5478.25

- Nasdaq down 624.5 points (-3.5%) at 17374.17

- US 10-Yr yield is up 2.7 bps at 4.2779%

- US Sep 10-Yr futures are down 6.5/32 at 110-21.5

- EURUSD down 0.0015 (-0.14%) at 1.0839

- USDJPY down 1.58 (-1.02%) at 154.01

- #VALUE!

- Gold is down $1.74 (-0.07%) at $2407.96

- European bourses closing levels:

- EuroStoxx 50 down 54.93 points (-1.12%) at 4861.87

- FTSE 100 down 13.68 points (-0.17%) at 8153.69

- German DAX down 170.24 points (-0.92%) at 18387.46

- French CAC 40 down 84.9 points (-1.12%) at 7513.73

US TREASURY FUTURES CLOSE

- 3M10Y +1.771, -103.852 (L: -111.009 / H: -102.612)

- 2Y10Y +9.837, -14.453 (L: -24.715 / H: -13.04)

- 2Y30Y +12.398, 11.566 (L: -1.727 / H: 13.344)

- 5Y30Y +5.655, 37.71 (L: 31.397 / H: 38.701)

- Current futures levels:

- Sep 2-Yr futures up 1.25/32 at 102-17.5 (L: 102-15.125 / H: 102-20.5)

- Sep 5-Yr futures down 1/32 at 107-9.25 (L: 107-07.25 / H: 107-18)

- Sep 10-Yr futures down 6.5/32 at 110-21.5 (L: 110-20 / H: 111-04.5)

- Sep 30-Yr futures down 29/32 at 118-4 (L: 117-29 / H: 119-09)

- Sep Ultra futures down 1-15/32 at 124-8 (L: 124-00 / H: 125-30)

US 10YR FUTURE TECHS: (U4) Builds Base at Weekly Low

- RES 4: 112-25 High Mar 8

- RES 3: 112-10 1.50 proj of the Apr 25 - May 16 - 29 price swing

- RES 2: 111-31 1.382 proj of the Apr 25 - May 16 - 29 price swing

- RES 1: 111-13+/17+ High Jul 16 / 1.382 of Apr 25-May 16-29 swing

- PRICE: 111-04+ @ 16:05 BST Jul 24

- SUP 1: 110-21+/110-08 20- and 50-day EMA values

- SUP 2: 109-02+/109-00+ Low Jul 1 / Low Jun 10 and key support

- SUP 3: 108-27+ Low Jun 3

- SUP 4: 108-25+ Trendline drawn from the Apr 25 low

A bull theme in Treasuries remains intact, with markets seemingly building a base at the weekly low of 110-18+. This goes someway to correcting the pullback off last week’s high, but further progress higher is needed before historic resistance at 111-10+ gives way again. Clearance here would confirm a resumption of the bull cycle and open 111-17+ and 111-31, the 1.236 and 1.382 projection of the Apr 25 - May 16 - 29 price swing. Initial support is 110-21+, the 20-day EMA.

SOFR FUTURES CLOSE

- Sep 24 +0.020 at 94.945

- Dec 24 +0.025 at 95.345

- Mar 25 +0.030 at 95.725

- Jun 25 +0.030 at 96.015

- Red Pack (Sep 25-Jun 26) +0.010 to +0.030

- Green Pack (Sep 26-Jun 27) -0.01 to +0.005

- Blue Pack (Sep 27-Jun 28) -0.04 to -0.015

- Gold Pack (Sep 28-Jun 29) -0.055 to -0.045

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00008 to 5.34958 (+0.00283/wk)

- 3M +0.00124 to 5.28460 (+0.00161/wk)

- 6M +0.00485 to 5.14408 (+0.00940/wk)

- 12M +0.01590 to 4.83735 (+0.03709/wk)

- Secured Overnight Financing Rate (SOFR): 5.34% (+0.01), volume: $2.011T

- Broad General Collateral Rate (BGCR): 5.32% (+0.00), volume: $796B

- Tri-Party General Collateral Rate (TGCR): 5.32% (+0.00), volume: $773B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $85B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $225B

FED Reverse Repo Operation

NY Federal Reserve/MNI

RRP usage rebounds to $399.121B from $389.837B on Tuesday. Number of counterparties climbs to 75 from 64 prior. Today's usage compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

PIPELINE: $5.45B Corporate Debt Roundup

- Date $MM Issuer (Priced *, Launch #)

- 7/24 $2B #Capital One 6NC5 $1B +130, $1B 11NC10 +160

- 7/24 $1.85B #Whistler Pipeline $400M $5Y +125, $500M 7Y +150, $825M 10Y +170

- 7/24 $1B #Export Development Canada 4Y SOFR+33

- 7/24 $600M #Empresa Del Petroleo 10Y +187

- 7/24 $500M Wilsonart 8NC3

- Expected Thursday:

- 7/25 $Benchmark IADB 5Y SOFR+37a

EGBs-GILTS CASH CLOSE: Curves Twist Steepen In Risk-Off Session

Short-end core EGBs and Gilts strengthened Wednesday, and periphery spreads widened for a 2nd consecutive session, amid a broader global risk-off move.

- The UK and German curves twist steepened on the day. An early rally at the long end following softer-than-expected Euro area PMI data eventually faded. Longer-end Gilts traded weakly throughout the morning (solid/mixed UK PMIs) with losses extending in the afternoon.

- In contrast, short-dated yields fell sharply as implied global central bank easing ticked up.

- This drove the UK 2s10s spread to the most positive since March 2023, and Germany's the least negative since Nov 2023.

- With equities pulling back amid an apparent unwind in the Japanese yen carry trade and soft earnings reports by major US corporates, periphery EGB spreads widened again, with high-beta BTPs and GGBs underperforming.

- German IFO is the highlight of Thursday morning's docket, in addition to other European confidence indicators and UK CBI Trends, and appearances by ECB's Nagel and Lagarde.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 5.9bps at 2.655%, 5-Yr is down 2.7bps at 2.37%, 10-Yr is up 0.5bps at 2.444%, and 30-Yr is up 2.7bps at 2.661%.

- UK: The 2-Yr yield is down 3.6bps at 3.989%, 5-Yr is up 0.2bps at 3.942%, 10-Yr is up 3.2bps at 4.156%, and 30-Yr is up 3.7bps at 4.673%.

- Italian BTP spread up 4.2bps at 135bps / Greek up 3.5bps at 103.4bps

FOREX USD/JPY Slippage Triggers Oversold Condition For First Time in 18 Months

- JPY surged against all others in G10 Wednesday, as the short-covering triggered rally persisted to put USD/JPY through the 100-dma support and to the lowest levels since early May. This extends the gap with the cycle high posted pre-intervention to over 850 pips, and aids the JPY spot TWI's bounce to 5% off the cycle low.

- A poor showing from global equities worked in favour of haven currencies, and against growth proxies. Poorly received earnings reports from the likes of Alphabet and Tesla prompted sharp reversals in their share price, dragging the tech-heavy NASDAQ index lower by near 2.5% at some points of the session. As such, CHF rallied in tandem with JPY, adding more evidence to the argument that carry trade dynamics that dominated much of this year's currency trade are start to reverse.

- Antipodean currencies extends their recent spell of weakness, with added losses for industrial metals weighing further. AUD/USD's brief break below the 0.6587 200-dma was only saved by a turnaround for the greenback, as a bull-steepening of the US curve and outperformance in the short-end weighed on the dollar.

- Focus Thursday turns to Germany's IFO print for July, weekly jobless claims data from the US and the advanced Q2 GDP release. Both ECB's Nagel and ECB's Lagarde are set to speak.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/07/2024 | 0600/0800 | ** |  | SE | PPI |

| 25/07/2024 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 25/07/2024 | 0800/1000 | ** |  | EU | M3 |

| 25/07/2024 | 0800/1000 | *** |  | DE | IFO Business Climate Index |

| 25/07/2024 | 1000/1100 | ** |  | UK | CBI Industrial Trends |

| 25/07/2024 | - | | EU | ECB's Cipollone at Rio de Janeiro G20 Fin min/central bank meeting | |

| 25/07/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 25/07/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 25/07/2024 | 1230/0830 | *** | | US | GDP |

| 25/07/2024 | 1230/0830 | * |  | CA | Payroll employment |

| 25/07/2024 | 1230/0830 | ** | | US | Durable Goods New Orders |

| 25/07/2024 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 25/07/2024 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 25/07/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 25/07/2024 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 25/07/2024 | 1500/1700 | | EU | ECB's Lagarde attends Paris Summit | |

| 25/07/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 25/07/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 25/07/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.