Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

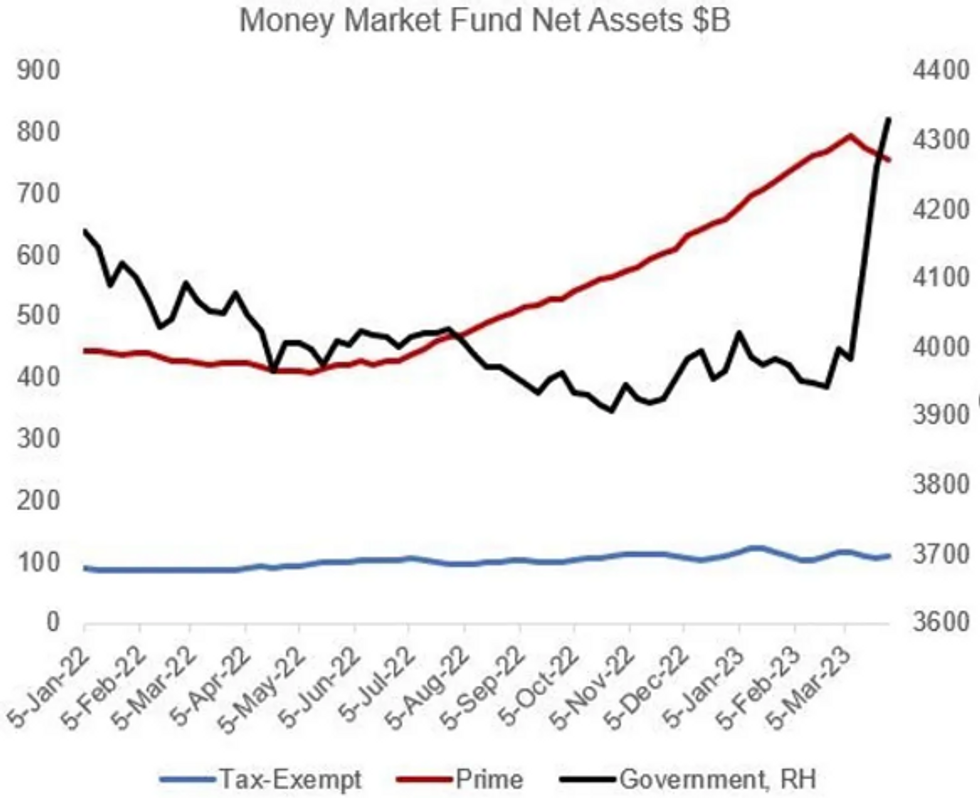

Gov't Money Market Fund Increase Points To Flight To Safety (Not Returns)

ICI/MNI

The $304B increase in money market fund assets since the start of March amid the turmoil triggered by Silicon Valley Bank and other institutions is thought to have come largely from a movement out of bank deposits into higher-yielding assets.

- That's certainly a large part of the story, with a slower pace of deposit outflows in late March mirroring the pace of MMF growth slowing (+$65B in the week to to Mar 29, vs around $120B in each of the prior two weeks - more detail in our latest US Commercial Banking Update).

- But a look within MMF asset composition shows that it's clearly been safety that has been sought rather than returns: Government-invested funds have seen assets explode, up $348B since the week of Mar 8, vs a drop of $37B in Prime funds (MMF AUM is up $304B on net).

- Prime MMFs offer higher yields but bear relatively higher risk to investors.

- It will be telling whether both MMF inflows as a whole, and their composition, shift in the weeks ahead as it appears the most acute fears over the banking system have abated but bank depositors are also recognizing the potential for higher returns elsewhere.

US

FED: St. Louis Fed President James Bullard said Thursday he doesn’t think the recent banking turmoil is enough to generate a recessionary tightening in U.S. credit conditions.

- “I’m less enamored with the story that credit conditions will tighten appreciably. I just don’t think it’s big enough by itself to send the U.S. economy into recession,” Bullard told reporters in a telephone briefing, arguing that only a small part of U.S. credit markets rely directly on the banking sector.

- “It’s not that clear to me that there will be much of a pullback on lending by these types of banks because they say loan demand remains relatively robust.” (See MNI INTERVIEW: Small, Midsize Credit Seizing Up, Says Kaplan)

- Bullard says the apparent easing of financial turbulence gives the Fed room to keep fighting against inflation that remains too high. "We need to stay at it and make sure we get the disinflationary process in place so you don’t get a repeat of the 1970s,” he said. “It’s a good moment to continue to fight inflation and get on that disinflationary path.”

US: U.S. home prices are on track for a double digit fall as the drop-off in construction and sales will likely help push the economy into recession, former head of the Federal Housing Finance Agency Mark Calabria told MNI.

- “Things can get pretty bad. I think we’re going to see pretty significant price declines, certainly in real terms in the double digits,” he said in an interview. “It’s kind of unprecedented to go through a big contraction in the housing market and to go through a fairly tough interest rate environment and not see a pullback.”

- Calabria, also former chief economist for the U.S. Vice President, said how bad things get for housing also depends on the resilience of a job market that has held up but could fray under restrictive monetary policy. “It’s hard to see jobs numbers continuing the way they have,” he said.

- “We are probably in the second, third inning of a housing correction. We’ve seen volumes in sales and construction fall off a cliff but prices really truly haven’t adjusted yet,” said Calabria, now at the CATO Institute. “The wild card will be the labor market, if we start to see construction job losses in a big way.” For more see MNI Policy main wire at 1105ET.

EUROPE

IMF: IMF Managing Director Kristalina Georgieva on Thursday said central banks must keep attacking inflation with interest rates and use other tools to stay on top of recent financial turmoil, crediting reforms since 2008 with limiting damage from distressed banks.

- “So long as financial pressures remain limited, we expect central banks to stay the course in the fight against inflation—holding a tight stance to prevent a de-anchoring of inflation expectations,” she said in the text of a speech previewing next week’s IMF meetings in Washington. (See: MNI INTERVIEW: Fed Not Done Hiking Despite Bank Pain-Cecchetti)

- Failure to curb inflation threatens global growth already cut in half to less than 3% this year amid geopolitical tensions such as the Ukraine war, she said. The IMF sees that growth rate persisting over the next five years, the worst such projection since 1990 and below the average 3.8% over the past two decades.

CANADA

CANADA: Canada kept adding more jobs than economists predicted in March, keeping unemployment near a record low and wage gains running above the 5% pace the central bank says will frustrate its efforts to bring inflation back to target.

- Employment rose by 34,700 in March to beat the consensus for a 7,500 gain. Statistics Canada also reported Friday the jobless rate held at 5%, close to last year's record low 4.9% in a month where economists predicted an increase to 5.1%.

- Wages climbed 5.3% from a year ago and hours worked by 1.6%, at a time when many economists and the Bank of Canada say the economy is stalling out or tipping into a mild recession. The composition of job gains was also favorable as private-sector hiring took over from recent gains led by governments, and there were slightly more new full-time positions than lower-paid part-time ones. For more see MNI Policy main wire at 0831ET.

US TSYS: Short End Extends Lows Ahead Fri's March Employment Data

- Front month Jun'23 Treasury futures trading mildly weaker after quickly reversing the knee-jerk bid anticipated in the event of a large claims up-revision.

- Tsy futures initially gapped higher (10s 116-30 high) following weekly claims: 18k drop to 228k vs. 200k est, prior revision to 246k, but quickly retraced to opening levels: 10s 116-23.5 (+5), 10Y yield 3.2662%.

- Yield curves have traded in a wide range today, well off early "highs" (2s10s -42.798 high), curves reversed course as the short end extended lows in the second half: 2s10s -52.850 at the moment (-4.710).

- Implied rate hikes gained slightly while rate cuts through year end have subsequently pared back from this morning's "highs".

- Fed funds implied hike for May'23 is currently at 12.6bp vs. 11.1bp, Jun'23 +8.1bp vs. 5.6bp cumulative at 4.893%.

- Projected rate cuts later in the year continue to recede from Wednesday's post-ADP levels: Sep'23 cumulative -33.3bp vs -36.6bp earlier to 4.490%, to -69.9bp vs. -75.5bp for Dec'23 (-84.9bp Wed) at 4.119.

- Focus turns to Friday's employment data for March at 0830ET. Reminder: Early close tomorrow in observance of Good Friday: 1100ET, Globex close at 1115ET. Full session on Monday. Side note: UK markets closed Friday and Monday.

OVERNIGHT DATA

- US JOBLESS CLAIMS -18K TO 228K IN APR 01 WK

- US PREV JOBLESS CLAIMS REVISED TO 246K IN MAR 25 WK

- US CONTINUING CLAIMS +0.006M to 1.823M IN MAR 25 WK

- Initial claims now see a notably different trajectory after seasonal adjustment revisions, with a trend rise in recent weeks more in keeping with higher non-seasonally adjusted data compared to more typical non-pandemic years (previous SA data had looked to be biased down as they overlapped with very high pandemic readings).

- It left a 4-week average of 238k (vs a little under 200k prior to the revisions), shifting higher from the prior payrolls reference week, although it has started to plateau more recently and the latest single week stepped down from 246k to 228k for the lowest in a month for the revised series.

- There still remains a reasonable disconnect with Challenger job cuts though, with this level of claims only slightly higher than the 2019 average of 218k compared to a sharper increase in layoffs.

- CANADA MARCH JOBS +34.7K VS FORECAST +7.5K, PRIOR +21.8K

- MARCH JOBLESS RATE HELD STEADY AT 5% VS FORECAST 5.1%

- CANADA HOURLY WAGES 5.3% YEAR-OVER-YEAR VS PRIOR 5.4%

- JOB GAIN LED BY TRANSPORTATION AND WAREHOUSING WORKERS

- CANADA FULL-TIME JOBS +18.8K, PART-TIME +15.9K

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 12.84 points (-0.04%) at 33469.45

- S&P E-Mini Future up 13.25 points (0.32%) at 4130.5

- Nasdaq up 85 points (0.7%) at 12081.63

- US 10-Yr yield is down 2.6 bps at 3.2847%

- US Jun 10-Yr futures are down 1/32 at 116-17.5

- EURUSD up 0.0027 (0.25%) at 1.0931

- USDJPY up 0.45 (0.34%) at 131.77

- WTI Crude Oil (front-month) up $0.02 (0.02%) at $80.63

- Gold is down $11.33 (-0.56%) at $2009.39

- EuroStoxx 50 up 11.09 points (0.26%) at 4309.45

- FTSE 100 up 78.62 points (1.03%) at 7741.56

- German DAX up 77.72 points (0.5%) at 15597.89

- French CAC 40 up 8.45 points (0.12%) at 7324.75

US TREASURY FUTURES CLOSE

- 3M10Y -13.845, -166.063 (L: -168.285 / H: -154.353)

- 2Y10Y -5.058, -53.198 (L: -54.072 / H: -42.798)

- 2Y30Y -6.016, -28.224 (L: -29.338 / H: -12.755)

- 5Y30Y -1.791, 17.958 (L: 16.84 / H: 26.89)

- Current futures levels:

- Jun 2-Yr futures down 3.75/32 at 103-22.5 (L: 103-21.125 / H: 103-31.875)

- Jun 5-Yr futures down 2.25/32 at 110-21.75 (L: 110-19 / H: 111-02.75)

- Jun 10-Yr futures down 1/32 at 116-17.5 (L: 116-11 / H: 116-30)

- Jun 30-Yr futures up 1/32 at 134-3 (L: 133-21 / H: 134-14)

- Jun Ultra futures up 11/32 at 144-28 (L: 144-01 / H: 145-08)

Key Resistance Remains Exposed

- RES 4: 117-29+ High Aug 26 2022 (cont)

- RES 3: 117-14+ High Aug 29 / 30 2022 (cont)

- RES 2: 117-01+ High Mar 24 and bull trigger

- RES 1: 116-30 High Apr 5 / 6

- PRICE: 116-15 @ 1440ET Apr 6

- SUP 1: 115-29/115-02+ Low Apr 5 / Low Apr 4

- SUP 2: 114-24+/07 20-day EMA / Low Mar 29 and 30

- SUP 3: 114-03+ 50-day EMA

- SUP 4: 113-26 Low Mar 22

Treasury futures traded higher this week as the contract extended the recovery from last week’s low. The strong bounce undermines recent bearish signals and price has cleared resistance at 116-06+, the Mar 27 high. The continuation higher exposes 117-01+, the Mar 24 high and a key short-term resistance. A break would strengthen bullish conditions and open 117-14+, the Aug 29/30 2022 high (cont). Key support is at 114-07, the Mar 29/30 low.

EURODOLLAR FUTURES CLOSE

- Jun 23 -0.045 at 94.845

- Sep 23 -0.10 at 95.275

- Dec 23 -0.115 at 95.645

- Mar 24 -0.120 at 96.095

- Red Pack (Jun 24-Mar 25) -0.09 to -0.05

- Green Pack (Jun 25-Mar 26) -0.03 to +0.005

- Blue Pack (Jun 26-Mar 27) -0.005 to +0.015

- Gold Pack (Jun 27-Mar 28) -0.015 to +0.010

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00042 to 4.80971% (+0.00885/wk)

- 1M +0.01015 to 4.90029% (+0.04258/wk)

- 3M -0.01314 to 5.19786% (+0.00515/wk)*/**

- 6M -0.05471 to 5.23743% (-0.07557/wk)

- 12M -0.07386 to 5.12571% (-0.17958/wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.22257% on 4/3/23

- Daily Effective Fed Funds Rate: 4.83% volume: $102B

- Daily Overnight Bank Funding Rate: 4.82% volume: $255B

- Secured Overnight Financing Rate (SOFR): 4.81%, $1.427T

- Broad General Collateral Rate (BGCR): 4.79%, $524B

- Tri-Party General Collateral Rate (TGCR): 4.79%, $510B

- (rate, volume levels reflect prior session)

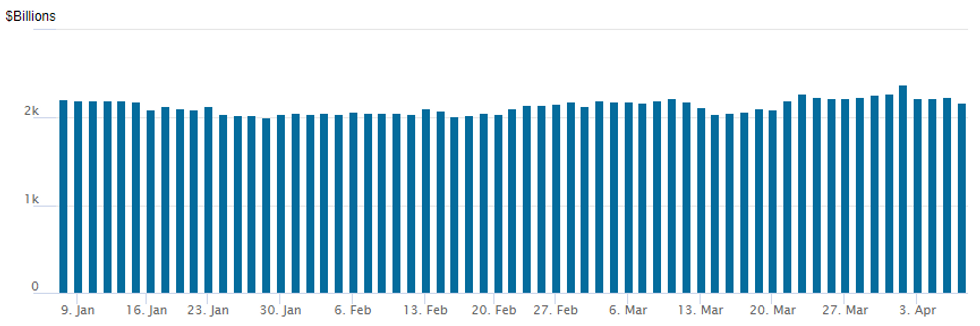

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage falls to $2,173.663B w/ 105 counterparties, compares to yesterday's $2,243.011B. All-time record high of $2,553.716B reached December 30, 2022; high usage for 2023: $2,375.171B on Friday March 31, 2023

PIPELINE: Bahrain 2Pt US$ Issuance on Tap

More supra-sovereign interest driving US$ issuance Thursday:

- Date $MM Issuer (Priced *, Launch #)

- 04/06 $Benchmark Bahrain 7Y 6.875%a, 12Y 8%a

- $11.75B Priced Wednesday, $35.35B/wk

- 04/05 $3.5B *Quebec 5Y SOFR+58a

- 04/05 $3.25B *Brazil 10Y 6.15%

- 04/05 $2.5B *Turkey +7Y 9.3%

- 04/05 1.5B *Micron $600M 5Y +205, $900M 10Y +265

- 04/05 $1B *Realty Income $400M 5Y +155, $600M 10Y +185

EGBs-GILTS CASH CLOSE: Busy Week Finishes On Flatter Pre-Holiday Note

The UK and German curves bear flattened Thursday to end an otherwise strong holiday-shortened week, with early strength at the short end reversing toward the close.

- The session was characterised by limited volumes and few event catalysts of note.

- Softer-than-expected US data has been the driving force in markets all week, and a jobless claims reading to the high side of expectations pushed Bund and Gilt yields to session lows in a knee-jerk move in the early European afternoon.

- But the move quickly faded, in large part due to seasonal adjustment revisions at play, and global core FI retreated ahead of the long weekend - with the US nonfarm payrolls reading Friday also on traders' minds.

- Equities rallied into the close, weighing on safe havens too. Periphery spreads were fairly steady throughout the session though, widening only mildly.

- BoE terminal rate hike pricing was little changed (4.63% for Sept); ECB terminal rose 5.6bp (to 3.52%, also for Sept). Little reaction to ECB Lane's reiteration that a May hike is the baseline case (futures continued to price in 22bp, unchanged).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3bps at 2.554%, 5-Yr is up 0.2bps at 2.18%, 10-Yr is up 0.1bps at 2.183%, and 30-Yr is up 1.6bps at 2.282%.

- UK: The 2-Yr yield is up 3.1bps at 3.372%, 5-Yr is up 1.5bps at 3.271%, 10-Yr is up 0.4bps at 3.432%, and 30-Yr is down 0.1bps at 3.771%.

- Italian BTP spread up 1.6bps at 184.9bps / Spanish up 1.8bps at 104.5bps

FOREX: NZD Remains Poorest Performer, DXY Unchanged Ahead Of NFP

- Despite the firmer sentiment across equity markets through the US session on Thursday, antipodean currencies have consolidated earlier losses. This sees NZD as the weakest in G10, declining 1% against the greenback amid a slightly weaker commodity complex. Despite the sharp drop, price remains around 50 pips shy of the weekly lows at 0.6208.

- In similar vein, AUDUSD is 0.6% lower as iron ore prices continue their slide to around 6% on the week.

- Overall, the USD index remains just south of unchanged as we approach tomorrow’s non-farm payrolls. The single currency has outperformed and has prompted EURUSD to regain some ground back above the 1.09 handle.

- With 1.0930 marking a key short-term hurdle for EURUSD bulls a sustained break would reinstate the recent bull theme and signal scope for a move to 1.1033, the Feb 2 high.

- USDJPY maintained an upward bias, edging around 1% higher from the overnight 130.78 lows but remains comfortably below the pre-JOLTS data levels of 132.70.

- For tomorrow’s data, Bloomberg consensus looks for still solid nonfarm payrolls growth of 230k in March as it falls back to closer to December’s pace with a return of more typical weather. However, actual expectations might be a little lower now after a recent string of weak data labour indicators.

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/04/2023 | 0645/0845 | * |  | FR | Foreign Trade |

| 07/04/2023 | 1230/0830 | *** |  | US | Employment Report |

| 07/04/2023 | 1900/1500 | * | | US | Consumer Credit |

| 10/04/2023 | - |  | EU | ECB Lagarde at IMF/World Bank Spring Meetings | |

| 10/04/2023 | 1400/1000 | ** | | US | Wholesale Trade |

| 10/04/2023 | 2015/1615 | | US | New York Fed's John Williams | |

| 11/04/2023 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 11/04/2023 | 0600/0800 | * |  | NO | CPI Norway |

| 11/04/2023 | 0900/1100 | ** | | EU | Retail Sales |

| 11/04/2023 | 1000/0600 | ** | | US | NFIB Small Business Optimism Index |

| 11/04/2023 | - | | EU | ECB Lagarde and Panetta in IMF/World Bank Spring Meetings | |

| 11/04/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 11/04/2023 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 11/04/2023 | 1730/1330 | | US | Chicago Fed's Austan Goolsbee | |

| 11/04/2023 | 2200/1800 | | US | Philadelphia Fed's Patrick Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.