Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI US-RUSSIA: Biden: "Too Early To Say Where Russia Situation Is Going"

- MNI POLITICAL RISK - Long-Term Risk To Putin Increases

- MNI Dallas Fed Mfg Sees Weaker Labor And Price Measures In June

US

US: US President Joe Biden has given his first public remarks on the insurrection by Yevgeny Prigozhin's Wagner Group.

- Biden says he directed his national security team to "monitor closely and report" to him "hour by hour," and prepare for a "range of scenarios." Biden says he agreed with allies to "give Putin no excuse to blame this on the West or NATO."

- Biden: "We made clear we were not involved. We had nothing to do with it. This was part of a struggle within the Russian system." Biden says he told Ukrainian President Volodymyr Zelensky that "no matter what happened in Russia," the US would continue to support Ukraine.

- Biden says "it is still to early to reach a definitive conclusion about where this is going. The ultimate outcome of all this remains to be seen." US Secretary of State Antony Blinken told CBS yesterday that the insurrection "...was a direct challenge to Putin’s authority... We do know that Putin has a lot more to answer for in the weeks and months ahead.” For more see the MNI Political Risk team's analysis of events: LINK

EUROPE

RUSSIA: With Yevgeny Prigozhin’s two-day Wagner Group rebellion against the Russian military establishment halted, there remains a lack of clarity on short-term implications for the war in Ukraine and the long-term implications for the regime of Russian President Vladimir Putin.

- The prevailing view is that the event has, to some extent, extinguished the idea that Putin has singular control over the Russia’s military apparatus, and the various proxies, like Prigozhin, he uses to diffuse power.

- It is unlikely that Prigozhin’s insurrection has fundamentally impacted the structures keeping Putin in power but the new reality that Putin does not control a monopoly of power within his own borders has raised the risk of further armed challenges to Putin's Kremlin.

- A significant shift in battlefield dynamics in Ukraine appears unlikely. Prigozhin’s Wagner Group was consistently touted as one of the most effective fighting forces of Russian military operation but Wagner's power within the Russian military ecosystem had been on the wane since a Pyrrhic victory at Bakhmut.

US TSYS: Firmer Ahead Tuesday Data, ECB CB Forum in Sintra, Portugal

- Treasury futures holding modestly firmer after the bell, near the lower half of a narrow session range - no particular headline driver for futures reversal off early session highs, however.

- Some factors at play. however, included incoming Treasury auctions ($65B 13W, $58B 26W bill auctions, $42B 2Y Note auction -- trades through: 4.670% high yield vs. 4.680% WI), while a pick-up in high-grade corporate debt issuance could be a factor for the dip in Treasury futures amid rate lock-hedge sales.

- Early month/quarter-end positioning also mentioned, with nascent asset allocation from Treasury futures to stocks. Underscoring this morning's retreat, the Sep'23 10Y contract trend outlook remains bearish. Recently, support at 112-29+, the May 26 / 30 low.

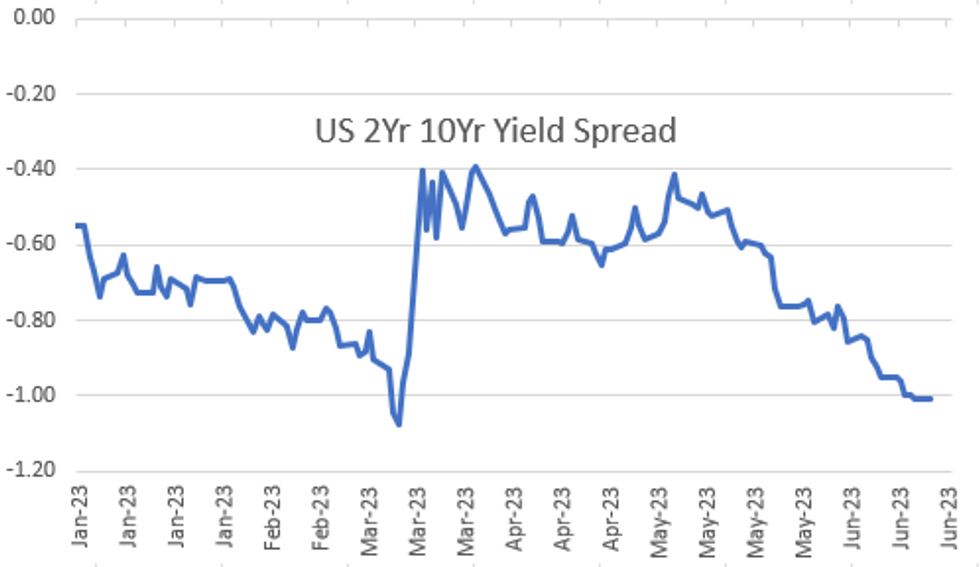

- Treasury curves extend inversion this morning, 2s10s taps -104.521 low, nearing March 40+ low around -111.0. “Although the cash curves are closing in on recent troughs," Goldman Sachs analysts write the "OIS and SOFR swap curves are still some distance away. Some of this weakness is likely the result of an anticipation of heavy front-end supply, but we expect it will not remain contained to front-end swap spreads as the full extent of supply increases becomes clear.”

- Economic data picks Tuesday: Durable Goods, Housing Metrics, Cons Confidence. While there is a dearth of scheduled Fed speakers Tuesday, attention will be on the ECB's forum on central banking in Sintra, Portugal that kicks off tonight with ECB Pres Lagarde. LINK.

OVERNIGHT DATA

- US JUNE DALLAS FED GENERAL BUSINESS ACTIVITY AT -23.2

- US JUNE DALLAS FED MANUFACTURING INDEX -23.2; EST. -21.8

US: The Dallas Fed manufacturing index came in close to expectations in June as it only recovered to -23.2 (cons -21.8) from -29.1 for its general business activity metric. The press releases notes some weaker internal points: Labor market measures suggest weaker employment growth and declining work hours. The employment index retreated 7pts to 2.2, falling below its average reading of 7.8. 17% of firms noted net hiring, while 15% noted net layoffs.

- “Price pressures evaporated, while wage pressures remained elevated. The raw materials prices index dropped 12pts to 1.4, indicative of little change in input costs from May. The finished goods prices index slipped from 0.4 to -1.9, suggesting selling prices edged down in June. The wages and benefits index held at 25.3, still slightly above its average of 21.1.”

- It continues a particularly mixed June for regional Fed mfg surveys, with Empire beating with a surprise jump to +6.6, Philly in line at -13.7 and Kansas missing at -12. The Richmond Fed survey lands tomorrow but Friday’s MNI Chicago PMI could provide a clearer indication of how risks are skewed for ISM Mfg to be released next week.

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 67.14 points (0.2%) at 33794.51

- S&P E-Mini Future down 5.5 points (-0.13%) at 4383.25

- Nasdaq down 89.1 points (-0.7%) at 13403.88

- US 10-Yr yield is down 1.4 bps at 3.7212%

- US Sep 10-Yr futures are up 4.5/32 at 113-7

- EURUSD up 0.0016 (0.15%) at 1.091

- USDJPY down 0.2 (-0.14%) at 143.5

- WTI Crude Oil (front-month) up $0.34 (0.49%) at $69.51

- Gold is up $2.13 (0.11%) at $1923.36

- EuroStoxx 50 up 8.96 points (0.21%) at 4280.57

- FTSE 100 down 8.29 points (-0.11%) at 7453.58

- German DAX down 16.88 points (-0.11%) at 15813.06

- French CAC 40 up 20.93 points (0.29%) at 7184.35

US TREASURY FUTURES CLOSE

- 3M10Y -3.162, -160.071 (L: -165.239 / H: -158.715)

- 2Y10Y +0.294, -101.202 (L: -104.521 / H: -100.762)

- 2Y30Y +2.746, -91.271 (L: -95.41 / H: -91.09)

- 5Y30Y +3.91, -14.395 (L: -17.97 / H: -14.127)

- Current futures levels:

- Sep 2-Yr futures up 0.875/32 at 102-3.125 (L: 102-01.75 / H: 102-05.625)

- Sep 5-Yr futures up 3.75/32 at 107-28.5 (L: 107-25.25 / H: 108-02.25)

- Sep 10-Yr futures up 4.5/32 at 113-7 (L: 113-03 / H: 113-16.5)

- Sep 30-Yr futures up 4/32 at 128-1 (L: 127-27 / H: 128-26)

- Sep Ultra futures steady at at 137-8 (L: 137-01 / H: 138-16)

US 10YR FUTURE TECHS: (U3) Trend Signals Remain Bearish

- RES 4: 115-00 High Jun 1 and a key resistance

- RES 3: 114-06+/10+ High Jun 6 / 50-day EMA

- RES 2: 114-00 High Jun 13

- RES 1: 113.18 High Jun 15

- PRICE: 113-07+ @ 1400ET Jun 26

- SUP 1: 112-12+ Low Jun 14 and the bear trigger

- SUP 2: 112-00 Low Mar 10

- SUP 3: 111-14+ Low Mar 9

- SUP 4: 110-27+ Low Mar 2 and key support

Treasury futures continue to trade inside the recent range. The trend outlook is unchanged and the outlook remains bearish. Recently, support at 112-29+, the May 26 / 30 low was cleared. This signals scope for 112-00, the Mar 10 low. Further out, potential is seen for a move towards 110-27+, the Mar 2 low and a key support. Short-term gains are considered corrective. Initial firm resistance is at 114-00, the Jun 13 high.

SOFR FUTURES CLOSE

- Sep 23 -0.005 at 94.660

- Dec 23 -0.015 at 94.770

- Mar 24 -0.015 at 95.080

- Jun 24 -0.005 at 95.495

- Red Pack (Sep 24-Jun 25) +0.015 to +0.060

- Green Pack (Sep 25-Jun 26) +0.035 to +0.055

- Blue Pack (Sep 26-Jun 27) +0.030 to +0.035

- Gold Pack (Sep 27-Jun 28) +0.025 to +0.035

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00364 to 5.08731 (+.00738 total last wk)

- 3M -0.00399 to 5.23471 (+.03186 total last wk)

- 6M -0.00867 to 5.32042 (+.03971 total last wk)

- 12M -0.02591 to 5.25769 (+.05398 total last wk)

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00457 to 5.06300%

- 1M +0.02943 to 5.17786%

- 3M -0.02314 to 5.52100% */**

- 6M -0.01672 to 5.67357%

- 12M -0.04058 to 5.88471%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.55743% on 6/12/23

- Daily Effective Fed Funds Rate: 5.07% volume: $135B

- Daily Overnight Bank Funding Rate: 5.06% volume: $284B

- Secured Overnight Financing Rate (SOFR): 5.05%, $1.389T

- Broad General Collateral Rate (BGCR): 5.03%, $605B

- Tri-Party General Collateral Rate (TGCR): 5.03%, $592B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

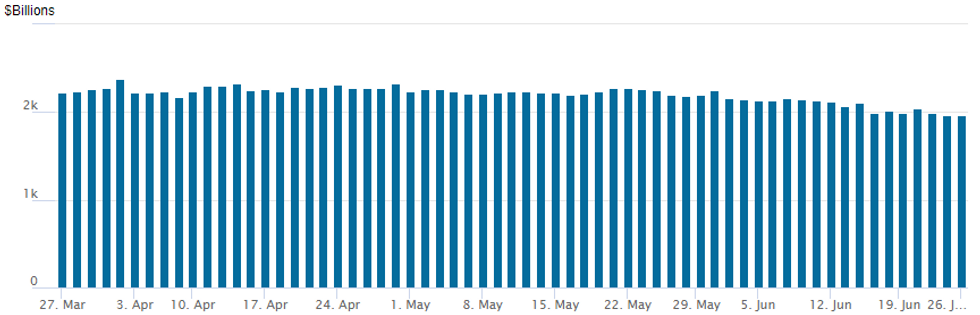

NY Federal Reserve/MNI

NY Fed reverse repo usage falls to $1,961.027B w/ 102 counterparties, compared to $1,969.380B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE: $2B Prologis 3Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 06/26 $2B #Prologis $750M 5Y +105, $750M +10Y +145, $500M 30Y tap +160

- 06/26 $1.5B #ANZ $1B 2Y +65, $500M 2Y SOFR+75

- 06/26 $1.25B #Petrobras Global Finance 10Y 6.625%

- 06/26 $600M *NongHyup Bank 5Y +98

- 06/26 $720M Viking Cruises 8NC3 9.25%a

- 06/26 $600M #Hyatt 3.5Y +145

- 06/26 $Benchmark Mitsubishi 5Y notes investor calls

EGBs-GILTS CASH CLOSE: Greece Outperforms Post-Election

European core FI had a constructive if quiet start to a busy week Monday, with some modest flattening in both the German and UK curves.

- The German belly outperformed as a weaker-than-expected IFO reading added another piece of evidence pointing toward renewed economic deceleration.

- Bunds held those morning gains, with focus turning to the ECB's Sintra event, and of course national (starting with Italy on Wednesday) and Eurozone flash inflation prints.

- UK yields fell, led by a sharp drop at the 30Y segment as the Gilt market took a bit of a breather from last week's surprise 50bp BoE hike. Appearances by Pill and Bailey on Wednesday are the focus, with GDP on Friday.

- GGBs outperformed in the European space, with the 10Y spread vs Germany touching a post-2021 low following the ND's attainment of a parliamentary majority over the weekend as expected.

- Up next: ECB Pres Lagarde makes remarks after hours, and early Tuesday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.9bps at 3.087%, 5-Yr is down 4.6bps at 2.449%, 10-Yr is down 4.4bps at 2.309%, and 30-Yr is down 3bps at 2.374%.

- UK: The 2-Yr yield is down 1.7bps at 5.16%, 5-Yr is down 1.4bps at 4.557%, 10-Yr is down 1.9bps at 4.301%, and 30-Yr is down 6.5bps at 4.385%.

- Italian BTP spread up 1.5bps at 164.1bps / Greek down 1.4bps at 123.6bps

FOREX: Japanese Yen Unable To Sustain Early Rally, USDCNH Extends Uptrend

- Despite an overall subdued session for global currency markets, the Norwegian krone stands out as the best performer, rising a little under 1%, whereas the Chinese Yuan has been the notable laggard.

- Initial price action on Monday saw the Japanese Yen outperform all others, receiving an early boost on the back of comments from the Japanese Chief Cabinet Secretary Matsuno, who added to recent rhetoric and stressed that "it's important for FX to move stably" and that "Japanese authorities are closely watching FX moves with a high sense of urgency".

- While USDJPY did come under pressure amid the headlines, the pair spent little time below the 143 handle before recovering well across the US open, and briefly trading back to unchanged around 143.70. The pair has edged slightly lower ahead of the APAC crossover, however, remains close to multi-month highs - last intervention phase was November 10th - as USDJPY traded around 146.50.

- USD/CNH {+0.40%) showed above 7.2300 for the first time this year, with the rally extending to highs of around 7.2450, Bulls are focused on the 28 Nov ’22 high (7.2592) after last week’s break and close above the well-defined uptrend channel resistance. Softer than pre-COVID level spending surrounding the Dragon Boat Festival holiday provided the latest batch of negative Chinese economic news. Markets will look to China’s official PMI data, due Friday, with continued focus on the need for deeper stimulus.

- Tuesday sees Canadian CPI as well as US durable goods and consumer confidence data. Later in the week, CPI data for Australia and the Eurozone will receive attention. Likely the market focus will be on the ECB Forum in Sintra, where on Wednesday Fed’s Powell, ECB’s Lagarde, BOJ’s Ueda and BoE’s Bailey all have a joint event.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 27/06/2023 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 27/06/2023 | 0600/0800 | ** |  | SE | PPI |

| 27/06/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 27/06/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 27/06/2023 | 0800/1000 |  | EU | ECB Lagarde Intro at ECB Forum | |

| 27/06/2023 | 0830/0930 | | UK | BOE Tenreyro Panels ECB Forum | |

| 27/06/2023 | 0830/1030 | | EU | ECB Panetta Panels ECB Forum | |

| 27/06/2023 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 27/06/2023 | 0930/1130 | | EU | ECB Elderson Panels ECB Forum | |

| 27/06/2023 | 1200/1400 | | EU | ECB Schnabel Panels ECB Forum | |

| 27/06/2023 | 1230/0830 | *** |  | CA | CPI |

| 27/06/2023 | 1230/0830 | ** |  | US | Durable Goods New Orders |

| 27/06/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 27/06/2023 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 27/06/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 27/06/2023 | 1400/1000 | *** | | US | New Home Sales |

| 27/06/2023 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 27/06/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 27/06/2023 | 1430/1030 | ** | | US | Dallas Fed Services Survey |

| 27/06/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 27/06/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.