Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

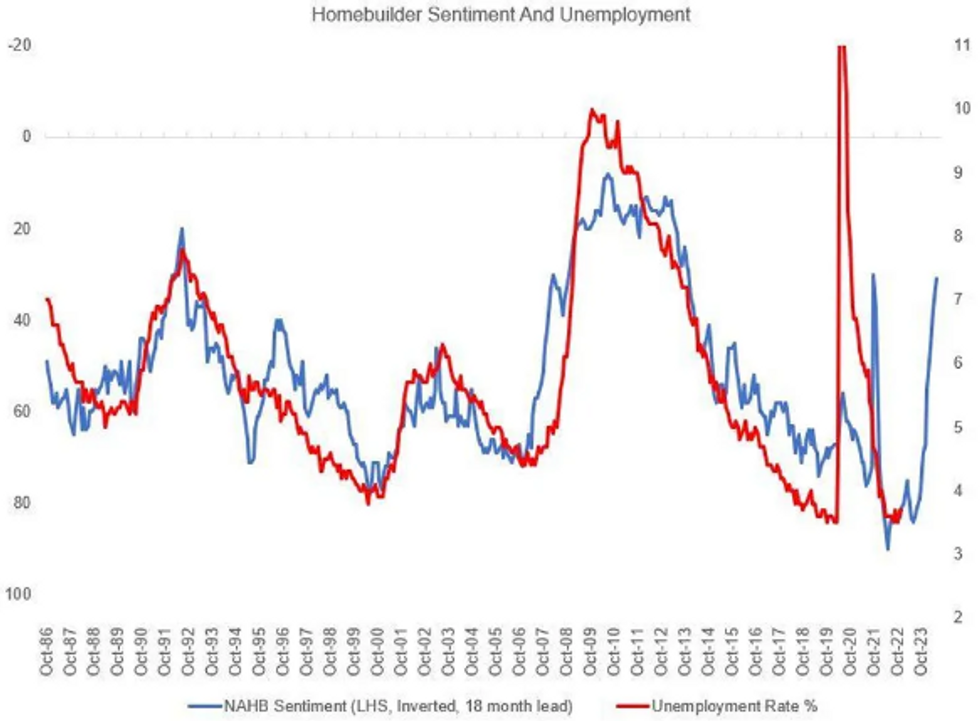

US DATA: Further Deterioration In Homebuilder Sentiment Points To Weaker Economy: Today's December NAHB reading of 31 (vs an uptick to 34 expected, from 33 prior) was a fresh decade low outside of the brief pandemic-related collapse in 2020.

- We continue to flag that homebuilder sentiment tends to lead a variety of indicators well in advance. That includes building permits, construction, and the unemployment rate (see chart).

- The current sentiment level is more consistent with an unemployment rate jump to 6-7% than with the current prevailing levels below 4%.

- Tuesday brings Building Permits and Housing Starts data for November. Each look set to record a further M/M % decline.

US

FED: Falling inflationary pressures as supply shocks ease and fiscal stimulus is reduced should allow the Federal Reserve to conclude its tightening cycle before it prompts a recession and any big spike in unemployment, former St. Louis Fed economist David Andolfatto told MNI.

- “You take a look at the most recent inflation prints, on a monthly basis they’ve come down quite a bit. Year-over-year it looks like you’re getting a nice hump-shaped pattern,” he said in an interview following the Fed’s decision to raise interest rates by another half percentage point last week.

- “The Fed can bring inflation down more rapidly than it otherwise would fall, but the reason it’s falling is that fiscal policy has gotten its act together. Why do we need the Fed to spur a recession to bring inflation down more rapidly at the expense of unemployment? Just let inflation come down gradually without the social cost of putting a bunch of people out of work.” For more see MNI Policy main wire at 1211ET.

FED: The lowest pay Americans would accept for a new job increased to a record USD73,667 according to a New York Fed survey as soaring prices change the calculus for workers.

- The self-reported "reservation wage" climbed fastest among those employed without a college degree according to a survey conducted three times a year that dates back to 2014. The measure grew 19% between March 2020 and November 2022 for employed respondents and 12% for non-employed respondents. Job holders without a college degree pushed up their reservation wage 27%.

- "The respondents’ increase in satisfaction with non-wage amenities in their current jobs are the main drivers of the rise in reservations wages since the onset of the pandemic, keeping everything else constant," a New York Fed blog said.

EUROPE

ECB: Ahead of the December ECB meeting we argued that while there was a strong case in favour of hiking policy rates by 75bp for a third time, gauging whether the GC would in fact hike by 75bp or 50bp was too close to call. In the end, the ECB opted for a 50bp hike combined with significantly hawkish messaging, as well as announcing a start date and initial run-off pace for the APP portfolio.

US TSYS: Tsys Reverse Friday's Optimism

Tsy futures broadly weaker after the close but off midday lows when 30YY tapped 3.6553% high. Light holiday volumes w/ TYH just over 700k after the close. Yield curves steeper (2s10s +2.604 at-67.630 vs. -64.130 high) but off early session highs amid orderly selling across the board.

- No real catalyst to the move, Tsys initially followed Bunds and Gilts lower early in the first half. Underlying weakness most likely unwinds of last Fri's rally despite the hawkish Fed speak from SF Fed Daly and Cleveland Fed Mester.

- Large 10Y Block sale (-10,120 TYH3 at 114-00, was well through the session low of 114-02.5 at the time (1105:00ET).

- No scheduled Fed speakers today, no react to slightly better than expexted NAHB Housing Market Index (36 vs. 34 est).

- Data picks up Tuesday w/ Building Permits (1.512M rev, 1.499M); MoM (-3.3% rev, -0.9%) and Housing Starts (1.425M, 1.404M); MoM (-4.2%, -1.5%) at 0830ET.

- Christmas holiday hours update:

- Trading floor closes at 1300ET while Globex close runs to 1600ET. Monday, Dec 26 is a full close w/ Globex reopening 1700ET

- Link to CME for reference

OVERNIGHT DATA

- US NAHB HOUSING MARKET INDEX 31 IN DEC

- US NAHB DEC SINGLE FAMILY SALES INDEX 36; NEXT 6-MO 35

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 328.33 points (-1%) at 32647.08

- S&P E-Mini Future down 50.25 points (-1.3%) at 3836

- Nasdaq down 183.6 points (-1.7%) at 10541.79

- US 10-Yr yield is up 9.9 bps at 3.5809%

- US Mar 10-Yr futures are down 21.5/32 at 114-4.5

- EURUSD up 0.0016 (0.15%) at 1.0606

- USDJPY up 0.35 (0.26%) at 136.94

- WTI Crude Oil (front-month) up $0.9 (1.21%) at $75.13

- Gold is down $6.39 (-0.36%) at $1786.95

- EuroStoxx 50 up 7.22 points (0.19%) at 3811.24

- FTSE 100 up 29.19 points (0.4%) at 7361.31

- German DAX up 49.8 points (0.36%) at 13942.87

- French CAC 40 up 20.66 points (0.32%) at 6473.29

US TSY FUTURES CLOSE

- 3M10Y +11.473, -71.281 (L: -85.8 / H: -69.698)

- 2Y10Y +2.523, -67.711 (L: -71.142 / H: -64.13)

- 2Y30Y +0.279, -63.671 (L: -66.892 / H: -57.204)

- 5Y30Y -0.573, -8.835 (L: -10.118 / H: -4.571)

- Current futures levels:

- Mar 2-Yr futures down 4.625/32 at 102-30.125 (L: 102-29.875 / H: 103-03)

- Mar 5-Yr futures down 14.25/32 at 109-2.25 (L: 109-00.5 / H: 109-15)

- Mar 10-Yr futures down 22/32 at 114-4 (L: 114-00.5 / H: 114-23)

- Mar 30-Yr futures down 46/32 at 129-23 (L: 129-09 / H: 131-01)

- Mar Ultra futures down 74/32 at 141-17 (L: 140-20 / H: 143-16)

US 10YR FUTURE TECHS: (H3) Fades Through London Close

- RES 4: 116-25 2.0% 10-dma envelope

- RES 3: 115-26 2.00 proj of the Oct 21 - 27 - Nov 3 price swing

- RES 2: 115-14 50% Aug - Oct Downleg

- RES 1: 115-11+ High Dec 13

- PRICE: 114-07 @ 1400ET Dec 19

- SUP 1: 113-22+/113-14 Low Dec 12 / 50-day EMA

- SUP 2: 112-11+ Low Nov 21 and a key short-term support

- SUP 3: 112-05+ Low Nov 14

- SUP 4: 110-22 Low Nov 10

Treasury futures continue to trade below the Dec 13 high. Last week’s print above resistance at 115-06+, Dec 7 high and a bull trigger, is a positive development. A clear break of this hurdle would confirm a resumption of the current uptrend and pave the way for a climb towards 115-26, a Fibonacci projection. Key short-term support has been defined at 113-22+, Dec 12 low. A reversal lower and a break of this level would threaten bullish conditions.

US EURODOLLAR FUTURES CLOSE

- Dec 22 +0.004 at 95.262

- Mar 23 -0.025 at 94.930

- Jun 23 -0.035 at 94.915

- Sep 23 -0.060 at 95.085

- Red Pack (Dec 23-Sep 24) -0.09 to -0.065

- Green Pack (Dec 24-Sep 25) -0.095 to -0.085

- Blue Pack (Dec 25-Sep 26) -0.095 to -0.085

- Gold Pack (Dec 26-Sep 27) -0.095 to -0.09

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00329 to 4.32029% (+0.49900 total last wk)

- 1M +0.00100 to 4.35386% (+0.08257 total last wk)

- 3M -0.00757 to 4.73829% (+0.01372 total last wk)*/**

- 6M -0.03700 to 5.14986% (+0.04715 total last wk)

- 12M -0.05115 to 5.42771% (-0.02057 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.77857% on 11/30/22

- Daily Effective Fed Funds Rate: 4.33% volume: $99B

- Daily Overnight Bank Funding Rate: 4.32% volume: $267B

- Secured Overnight Financing Rate (SOFR): 4.32%, $1.091T

- Broad General Collateral Rate (BGCR): 4.28%, $414B

- Tri-Party General Collateral Rate (TGCR): 4.28%, $391B

- (rate, volume levels reflect prior session)

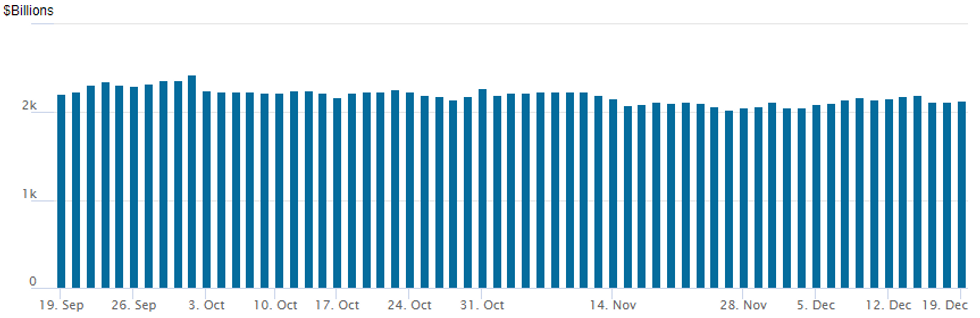

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,134.765B w/ 95 counterparties vs. $2,126.540B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EGBs-GILTS CASH CLOSE: Gilts Lead Broad Decline

European core FI sold off Monday, led by Gilts, with periphery EGBs putting in a mixed performance.

- Gilt yields soared following late Friday's BoE bond sale announcement and reports of potential energy cap pledges for businesses through 2024 The curve bear flattened sharply.

- The German curve bear steepened. Stronger-than-expected German IFO data contributed to the weak tone, with ECB speakers including de Guindos repeating last week's meeting message that 50bp hikes would be ongoing.

- On the EU level, we got supply plans from for H1 2023 (E80bln) and agreement on a gas price cap of E180/MWh. We also got EFSF / ESM 2023 funding plans.

- BTPs underperformed, with spreads widening once again in tandem with higher ECB terminal rate expectations.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.5bps at 2.44%, 5-Yr is up 1.9bps at 2.239%, 10-Yr is up 5.1bps at 2.203%, and 30-Yr is up 7.6bps at 2.063%.

- UK: The 2-Yr yield is up 20bps at 3.687%, 5-Yr is up 18.3bps at 3.491%, 10-Yr is up 17.3bps at 3.502%, and 30-Yr is up 15.2bps at 3.824%.

- Italian BTP spread up 3.4bps at 217.9bps / Spanish down 0.9bps at 108.8bps

FOREX: US Yields the Key Driver, as Stocks Extend Post-Fed Weakness

- The greenback pulled lower to begin the pre-holiday trading week, with the USD Index shedding 0.2% to the benefit of CAD, AUD and EUR. JPY was the poorest performer, however, prompting EUR/JPY to add well over 1% off the overnight Asia-Pac lows.

- The primary driver for markets Monday were Treasury yields playing catch-up, with the 10y yield adding 11bps to touch the best levels since last week's Fed decision.

- Yield gains worked against spot gold, which inched to session lows alongside the closing bell in London. Volumes across gold futures ticked higher on the move, but thin volumes and low liquidity were evident, with activity running at 40% below average.

- Stock markets extended their post-Fed decline, with the e-mini S&P pushing to a fresh December low of 3848.75. This makes for a clean break of the 50-dma at 3906.6, opening November's 3735.00 as the next major support.

- Focus Tuesday turns to RBA minutes and the Bank of Japan decision slated for release during the Asia-Pac trading day, while US housing starts and building permits make for the focus of the European/US trading day. ECB's Kazimir and Muller make up the speaker slate.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/12/2022 | 0115/0915 |  | CN | PBOC LPR announcement | |

| 20/12/2022 | 0700/0800 | ** |  | DE | PPI |

| 20/12/2022 | 1000/1000 | ** |  | UK | Gilt Outright Auction Result |

| 20/12/2022 | 1000/1100 | ** |  | EU | EZ Current Account |

| 20/12/2022 | - | *** |  | JP | BOJ policy announcement |

| 20/12/2022 | 1330/0830 | ** |  | CA | Retail Trade |

| 20/12/2022 | 1330/0830 | *** |  | US | Housing Starts |

| 20/12/2022 | 1330/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 20/12/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 20/12/2022 | 1500/1600 | ** | | EU | Consumer Confidence Indicator (p) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.