Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI US Treasury Expects To Borrow $1.859T By Yearend

- MNI POLICY: BOE To Speed Up QT, Detail Likely In Sept

- Lending Standards Tightened At A Similar Or Faster Pace To Q1

- MNI Regional Fed Surveys and Chicago PMI Point To Small ISM Mfg Increase

- MNI Chicago Business Barometer™ - Rises to 42.8 in July

us

US TSYS: The U.S. Treasury Department on Monday announced it expects to borrow USD1.007 trillion in privately-held net marketable debt in the third quarter and an additional USD852 billion in the fourth quarter.

- Treasury's third quarter estimate is USD274 billion more than previously announced in May, primarily due to a low cash balance at the start of the quarter. Adjusted for changing cash balance levels, third quarter borrowing is expected to be the greatest quarterly borrowing on record. The U.S. agency also raised its previous assumption for the end-of-September cash balance by USD50 billion to USD650 billion, while assuming an end-of-December balance of USD750 billion.

- During the second quarter, the U.S. borrowed USD657 billion and ended the quarter with a USD402 billion cash balance. The Treasury's quarterly refunding, which is expected to show coupon increases, will be released at 8:30 a.m. August 2.

US: Lending standards saw another quarter of tightening across the board through Q2, for the most part either at a accelerated pace than was the case with the April release or showing a similar trend.

- Lending standards for commercial & industrial loans saw an intensification of tightening for firms of all sizes, pushing higher to

- CRE lending saw a similar paced net tightening for another quarter at roughly similar levels to the height of the pandemic.

- Residential real estate loans saw a mostly similar rate of tightening or a slight acceleration, barring the limited number of those loaning subprime mortgages where there was an easing.

- Consumer loans are most mixed meanwhile, with credit card lending standards tightened further but at a slower pace for both auto and other loans.

UK

BOE: The Bank of England is set to decide on an accelerated gilt sales programme which could marginally push up costs for the public finances, with the detail probably coming in September.

- While details of the first year of sales were unveiled last August for the Monetary Policy Committee to vote on it in September for an October commencement, markets and the Bank are now familiar with the process, so both the detailed announcement and the vote are likely to come next month rather than at this week’s meeting.

- This time round the target will likely be higher than year’s GBP80 billion stock reduction target, half of which was to be achieved through active sales, but the effect of that acceleration on the public finances, which the Office for Budget Responsibility will estimate for Budget arithmetic, looks set to be marginal. Deputy Governor Dave Ramsden, responsible for the Bank's balance sheet, said in a July 19 speech that he favored faster gilt sales for the second year of the programme. For more see MNI Policy main wire at 0845ET.

US TSYS Tsy Borrowing Est's Larger Than Expected

- Treasury futures remain in positive territory, well off mid-session highs after the Tsy anncd larger than expected Q3 issuance of $1.007 trillion in privately-held net marketable debt in the third quarter and an additional USD852 billion in the fourth quarter.

- Treasury's third quarter estimate is USD274 billion more than previously announced in May, primarily due to a low cash balance at the start of the quarter. Adjusted for changing cash balance levels, third quarter borrowing is expected to be the greatest quarterly borrowing on record.

- Reminder, the Treasury's quarterly refunding, which is expected to show coupon increases, will be released at 8:30 a.m. August 2.

- Meanwhile, lending standards saw another quarter of tightening across the board through Q2, for the most part either at a accelerated pace than was the case with the April release or showing a similar trend.

- Earlier data: The Chicago Business Barometer™, produced with MNI, ticked up by 1.3 points to 42.8 in July, the second consecutive monthly increase. However, with the exception of Prices Paid, all of the sub-indices remain in contractive territory (sub-50).

- Focus turns to ISMs on Tue (Mfg 46.98 est, prices paid 44.0 est), ADP on Wednesday (+188k est vs. 497k prior), and July employment data next Friday, current estimate of +200k job gains vs. +209k in June.

US DATA: The Chicago Business Barometer™, produced with MNI, ticked up by 1.3 points to 42.8 in July, the second consecutive monthly increase. However, with the exception of Prices Paid, all of the sub-indices remain in contractive territory (sub-50).

- New Orders, Production and Order Backlogs all moved higher in July while Employment and Supplier Deliveries deteriorated further in contractive territory.

- The biggest contributor to the increase in the headline index was New Orders, which rose 3.4 points. However, this masked the fact that the proportion of respondents reporting an increase in new orders in June was actually the lowest of the year. For more see MNI Policy main wire at 0845ET.

US DATA: The Dallas Fed activity index completed the July round of regional Fed manufacturing surveys (rising to -20 from -23.2), with the average of the five near unchanged at -10.5 after -10.1 in a mild improvement from levels earlier in the year including a low of -16.5.

- There was unusually little change on the month across each region, with the largest drop in the Empire survey from +6.6 to +1.1 as it held most of its prior surprise jump.

- The average remains at a level implying a small improvement in tomorrow’s ISM mfg survey, and indeed consensus looks for 46.9 from 46.0.

- A similar increase was supported by today’s MNI Chicago PMI despite a small miss, rising to 42.8 (cons 43.4) from 41.5, whilst the S&P Global PMI equivalent saw a sharper increase from 46.3 to 49.0.

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 8.22 points (0.02%) at 35466.93

- S&P E-Mini Future down 2 points (-0.04%) at 4604.25

- Nasdaq up 4 points (0%) at 14320.71

- US 10-Yr yield is down 0.2 bps at 3.9488%

- US Sep 10-Yr futures are up 4/32 at 111-15

- EURUSD down 0.0016 (-0.15%) at 1.1001

- USDJPY up 1.08 (0.77%) at 142.24

- WTI Crude Oil (front-month) up $1.31 (1.63%) at $81.90

- Gold is up $7.55 (0.39%) at $1967.03

- EuroStoxx 50 up 4.81 points (0.11%) at 4471.31

- FTSE 100 up 5.14 points (0.07%) at 7699.41

- German DAX down 22.92 points (-0.14%) at 16446.83

- French CAC 40 up 21.31 points (0.29%) at 7497.78

US TREASURY FUTURES CLOSE

- 3M10Y +1.459, -147.475 (L: -152.041 / H: -144.94)

- 2Y10Y +0.845, -92.362 (L: -93.619 / H: -90.63)

- 2Y30Y +0.938, -86.283 (L: -88.117 / H: -84.999)

- 5Y30Y +0.607, -16.259 (L: -18.841 / H: -15.498)

- Current futures levels:

- Sep 2-Yr futures up 1.125/32 at 101-16.625 (L: 101-14.25 / H: 101-18.5)

- Sep 5-Yr futures up 2.75/32 at 106-27 (L: 106-19.5 / H: 106-30.75)

- Sep 10-Yr futures up 3.5/32 at 111-14.5 (L: 111-02 / H: 111-20)

- Sep 30-Yr futures up 9/32 at 124-17 (L: 123-26 / H: 124-28)

- Sep Ultra futures up 14/32 at 132-12 (L: 131-15 / H: 132-26)

US 10Y FUTURE TECHS: (U3) Trading Closer To Its Recent Lows

- RES 4: 113-08 High Jul 18 and a bull trigger

- RES 3: 112-29 50-day EMA

- RES 2: 112-17+ High Jul 24

- RES 1: 112-07 High Jul 27

- PRICE: 111-08 @ 12:43 BST Jul 31

- SUP 1: 110-25+ Low Jul 28

- SUP 2: 110-13 Low Jul 7

- SUP 3: 110-05 Low Jul 6 and the bear trigger

- SUP 4: 109-14 Low Nov 8 2022 (cont)

Treasuries are trading closer to their recent lows. For now, the latest bear leg appears to be a correction. However, price has traded through all relevant short-term retracement points. A resumption of weakness would expose the key support at 110-05, the Jul 6 low. Clearance of this support point would confirm a continuation of the medium-term downtrend. Key resistance has been defined at 113-08, the Jul 18 high.

SOFR FUTURES CLOSE

Sep 23 steady at 94.590

Dec 23 +0.005 at 94.625

Mar 24 +0.025 at 94.845

Jun 24 +0.035 at 95.165

Red Pack (Sep 24-Jun 25) +0.040 to +0.045

Green Pack (Sep 25-Jun 26) +0.025 to +0.045

Blue Pack (Sep 26-Jun 27) +0.005 to +0.015

Gold Pack (Sep 27-Jun 28) steady to +0.010

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00026 to 5.31784 (+.02011 total last wk)

- 3M -0.00659 to 5.36532 (+.02070 total last wk)

- 6M -0.01487 to 5.43313 (+.01957 total last wk)

- 12M -0.02476 to 5.38312 (+.04638 total last wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $106B

- Daily Overnight Bank Funding Rate: 5.32% volume: $258B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.419T

- Broad General Collateral Rate (BGCR): 5.28%, $597B

- Tri-Party General Collateral Rate (TGCR): 5.28%, $574B

- (rate, volume levels reflect prior session)

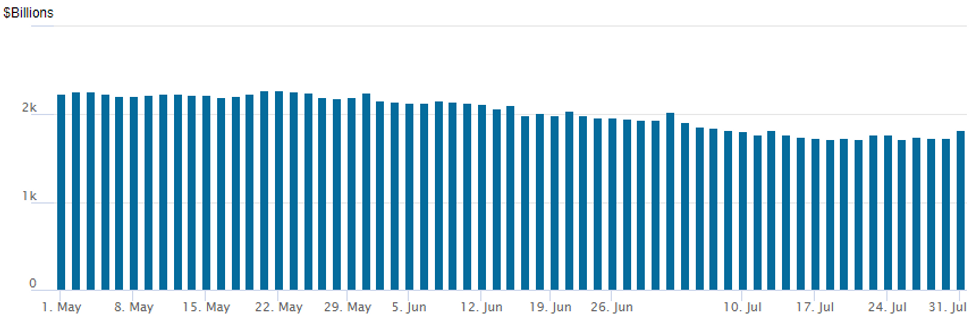

FED Reverse Repo Operation

NY Federal Reserve/MNI

The latest operation rebounds to $1,821.124B, w/105 counterparties, compared to $1,730.227B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE: CORPORATE DEBT FINISHING JULY STRONG

At least $17.7B to price Monday, still waiting for State St 3Y fixed/SOFR to launch

- Date $MM Issuer (Priced *, Launch #)

- 07/31 $5B #BAT $1B 5.5Y +175, $1B 7Y +225, $1.25B 10Y +245, $750M 20Y +285, $1B 30Y +305

- 07/31 $3.5B #Mercedes Benz $700M 2Y +52, $400M 2Y SOFR+57, $750M 3Y +72, $900M 5Y +95, $750M 10Y +115

- 07/31 $3.5B #Santander $1.5B 5Y +140, $2B 10Y +295

- 07/31 $2B #Lloyds $1.5B 4NC3 +148, $500M 4NC3 SOFR+156

- 07/31 $1.6B #Norfolk Southern $600M 7Y +102, $1B 30Y +137

- 07/31 $800M #Invitation Homes $450M 7Y +158, $350M 10Y +173

- 07/31 $800M #Xcel Energy 10Y +153

- 07/31 $500M #Consumers Energy +5Y +75

- 07/31 $Benchmark State St 3Y +75, +3Y SOFR

EGBs-GILTS CASH CLOSE: Shrugging Off Sticky Eurozone Core Inflation

The German curve twist steepened while the UK's twist flattened Monday.

- Eurozone flash July inflation reading was the highlight of the European schedule, and showed a slight upside surprise on core vs survey - but were largely in-line based on national-level prints and had little lasting impact.

- Afternoon trade proved slightly more constructive, as US Treasuries gained (in part after softer-than-expected MNI Chicago PMI data).

- Schatz yields closed slightly lower, in contrast to UK 2Y yields ticking higher (note that ECB terminal hike expectations rose 1bp on the day, but BoE was up 6bp ahead of Thursday's MPC decision).

- Further down the curve, 10Y Bund yields closed unchanged, with its UK counterpart seeing a 2bp dip in yields.

- Greece outperformed on the periphery, potentially on the prospective achievement of investment grade status with Scope Ratings on Friday following Japan's R&I move today (although neither impacts ECB purchase/bond index inclusion).

- Tuesday morning brings final manufacturing PMIs and German labour market data.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.3bps at 3.038%, 5-Yr is down 0.9bps at 2.536%, 10-Yr is unchanged at 2.492%, and 30-Yr is up 0.1bps at 2.57%.

- UK: The 2-Yr yield is up 1.2bps at 5%, 5-Yr is down 1.8bps at 4.394%, 10-Yr is down 1.7bps at 4.309%, and 30-Yr is down 1.9bps at 4.462%.

- Italian BTP spread down 1.2bps at 161bps / Greek down 6.6bps at 126.9bps

FOREX AUDJPY Rises 1.8% Amid BOJ Bond Purchase Operation, Focus Turns To RBA

- The Japanese Yen remains softer against all others in G10 on Monday, falling on the back of an unexpected BoJ operation to curb a rise in local bond yields. The Bank's operation was the first of its kind since February, intervening by buying as much as $2bln in JGBs at market rates.

- USDJPY (+0.78%) spiked in response and eventually traded to a high of 142.68 before consolidating just north of 142.00 for the majority of the US session. Price action leaves the pair at the highest since early July, narrowing the gap with the key bull trigger and medium-term resistance at 145.07.

- More impressive was the move in AUDJPY and NZDJPY, rising by 1.8% and 1.6% respectively. Antipodean currency strength comes ahead of Tuesday’s RBA rate decision, at which the bank is seen raising rates by 25bps to 4.35%. The moves also follow the mixed China PMI releases overnight. The official PMIs, in aggregate, suggest China's economy lost momentum in July, with the composite index slipping to 51.1 (from 52.3). However, the manufacturing reading beat expectations, with some positive details as well. The market may also be looking through the weaker services read, given efforts in recent weeks to boost consumption growth and potentially easier housing market restrictions.

- In similar vein, the Canadian dollar has also rallied around half a percent, alongside similar advances for both SEK and NOK, amid constructive price action for crude futures. Both the Euro and the USD index have had traded in tight ranges on Monday, with little impact from month-end rebalancing.

- Elsewhere in emerging markets, it is worth noting the Chilean Peso is 1.35% lower against the dollar following a more aggressive-than-expected 100bp rate cut late Friday.

- Aside from the RBA decision, Tuesday’s docket is highlighted by US July ISM Manufacturing PMI and JOLTS Job Openings.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/08/2023 | 2300/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

| 01/08/2023 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 01/08/2023 | 2350/0850 | * |  | JP | labor forcer survey |

| 01/08/2023 | 0030/0930 | ** | | JP | IHS Markit Final Japan Manufacturing PMI |

| 01/08/2023 | 0130/1130 | * | | AU | Building Approvals |

| 01/08/2023 | 0130/1130 | ** | | AU | Lending Finance Details |

| 01/08/2023 | 0145/0945 | ** |  | CN | IHS Markit Final China Manufacturing PMI |

| 01/08/2023 | 0430/1430 | *** | | AU | RBA Rate Decision |

| 01/08/2023 | 0715/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 01/08/2023 | 0745/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 01/08/2023 | 0750/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 01/08/2023 | 0755/0955 | ** |  | DE | Unemployment |

| 01/08/2023 | 0755/0955 | ** | | DE | IHS Markit Manufacturing PMI (f) |

| 01/08/2023 | 0800/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 01/08/2023 | 0830/0930 | ** | | UK | S&P Global Manufacturing PMI (Final) |

| 01/08/2023 | 0900/1100 | ** | | EU | Unemployment |

| 01/08/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 01/08/2023 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 01/08/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 01/08/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/08/2023 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 01/08/2023 | 1400/1000 | * | | US | Construction Spending |

| 01/08/2023 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 01/08/2023 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 01/08/2023 | 1400/1000 | | US | Chicago Fed's Austan Goolsbee | |

| 01/08/2023 | 1430/1030 | ** | | US | Dallas Fed Services Survey |

| 01/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 02/08/2023 | 2245/1045 | *** |  | NZ | Quarterly Labor market data |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.