Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: US Treasury Expects To Borrow $1.592T By End Q1

- MNI INTERVIEW: No BOC Cuts In View, More Hikes Possible-Tapp

- MNI INTERVIEW: ECB Rates Course Hinges On '25 Growth-BoG Deputy

- MNI Regional Fed Mfg Surveys Don’t Move The ISM Needle

US

US TSYS: The U.S. Treasury on Monday announced it expects to borrow USD1.592 trillion in privately-held net marketable debt over the next two quarters combined, on the high end of the range of market expectations.

- Treasury expects to borrow USD776 billion in the fourth quarter and an an additional USD816 billion in the first quarter of next year. Both estimates would represent records for each respective quarter. The fourth quarter estimate is USD76 billion less than previously announced in July, due to projections of higher receipts. The U.S. agency is assuming an end-of-December and end-of-March cash balance of USD750 billion.

- During the third quarter, the U.S. borrowed USD1.010 trillion and finished out with a USD657 billion cash balance. The Treasury's quarterly refunding, which is expected to show coupon increases, will be released at 8:30 a.m. ET on November 1.

CANADA

BOC: Investors are too dovish about the Bank of Canada's outlook given that policymakers are still leaving the door open to additional rate increases and are nowhere near considering cuts, Chamber of Commerce chief economist and former government researcher Stephen Tapp told MNI.

- The Chamber's third-quarter survey of executives also found 25% of them plan to raise prices in the next few months, about double the share consistent with inflation running at the Bank's 2% target, Tapp said in an interview. The central bank's own forecasts show inflation around 3.5% through the middle of next year and sluggish growth rather than a deep recession that would require monetary easing, he said.

- “Will rates go up? Should rates go up? I wouldn’t be surprised. I think people are underestimating the persistence and how broad-based inflation pressures are," said Tapp, a former researcher at the BOC, federal trade finance bank, parliamentary budget office and finance department. "We are not really close to winning the war on inflation." (See: MNI INTERVIEW: BOC Could Hike Once Or Twice More, Dodge Says) For more see MNI Policy main wire at 1505ET.

EUROPE

GREECE/ECB: The length of time during which the European Central Bank keeps interest rates at elevated levels will depend on economic growth, with the outlook for 2025 key, the deputy governor of the Central Bank of Greece told MNI.

- “The answer to the question for the interest rates ‘how long is long?’ lies on the level of economic activity, particularly in 2025, when inflation is projected to de-escalate to around 2%,” Theodore Pelagidis said. “To respond one has to predict whether stagnation and weak growth will insist, or are we going to have a full and robust recovery?”

- While the ECB says that its 4% deposit rate if “maintained for a sufficiently long duration” will make a “substantial contribution” to reaching its 2% inflation target, and President Christine Lagarde at last week’s Governing Council meeting refused to rule out further hikes, the eurozone’s growth outlook is highly uncertain, Pelagidis noted. For more see MNI Policy main wire at 1215ET.

US TSYS Inside Lower, Narrow Range, Tsy Borrow Ests Lower Than Expected

- Treasury futures holding modestly, see-sawing near the middle of the session range by the bell. Several exogenous factors at play.

- Tsy futures had been climbing off morning lows after lower than expected German CPI spurred shorts to unwind. That was until midmorning Nikkei headlines posited the Bank of Japan will consider tweaking yield curve control framework at tomorrow's policy meeting.

- Stocks regained positive momentum by midmorning as some desks suggest (unconfirmed) month-end asset allocation from FI into stocks may be at play.

- The pendulum swung higher on the bell after the US Tsy announced borrowing estimates for Q4 and Q1'24.

- Treasury expects to borrow USD776 billion in the fourth quarter and an an additional USD816 billion in the first quarter of next year. Both estimates would represent records for each respective quarter. The fourth quarter estimate is USD76 billion less than previously announced in July, due to projections of higher receipts. The U.S. agency is assuming an end-of-December and end-of-March cash balance of USD750 billion.

- Tuesday focus turns to ECI, Chicago PMI and Consumer Confidence data ahead ADP and TBAC refunding Wednesday morning followed by the FOMC policy announcement Wednesday afternoon.

OVERNIGHT DATA

US DATA: The Dallas Fed manufacturing survey came in a little weaker than expected as it slipped to -19.2 in October (cons -16.0) after -18.1.

- It sees general business activity at its lowest reading since -20 in July but is still off a recent low of -29.1 from May.

- Tallying up the five regional Fed manufacturing surveys suggests little bias for Wednesday’s ISM mfg release, and indeed consensus is currently for no change from the 49.0 in September having lifted from 46 readings back in May-July.

- Tomorrow’s MNI Chicago PMI will be watched to see if it provides a steer before then.

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA up 570.81 points (1.76%) at 32988.09

- S&P E-Mini Future up 55.75 points (1.35%) at 4193

- Nasdaq up 168.1 points (1.3%) at 12810.97

- US 10-Yr yield is up 3 bps at 4.8645%

- US Dec 10-Yr futures are down 5/32 at 106-8.5

- EURUSD up 0.0054 (0.51%) at 1.0619

- USDJPY down 0.6 (-0.4%) at 149.05

- WTI Crude Oil (front-month) down $3.11 (-3.64%) at $82.42

- Gold is down $8.66 (-0.43%) at $1997.75

- European bourses closing levels:

- EuroStoxx 50 up 13.96 points (0.35%) at 4028.32

- FTSE 100 up 36.11 points (0.5%) at 7327.39

- German DAX up 29.13 points (0.2%) at 14716.54

- French CAC 40 up 29.69 points (0.44%) at 6825.07

US TREASURY FUTURES CLOSE

- 3M10Y +2.598, -60.098 (L: -64.509 / H: -54.873)

- 2Y10Y -0.34, -17.297 (L: -19.368 / H: -13.84)

- 2Y30Y -2.661, -1.636 (L: -3.043 / H: 3.605)

- 5Y30Y -2.732, 22.21 (L: 21.404 / H: 25.814)

- Current futures levels:

- Dec 2-Yr futures down 1.5/32 at 101-9.125 (L: 101-06.875 / H: 101-11)

- Dec 5-Yr futures down 3.25/32 at 104-18.75 (L: 104-12.5 / H: 104-23)

- Dec 10-Yr futures down 5/32 at 106-8.5 (L: 105-30 / H: 106-14.5)

- Dec 30-Yr futures down 1/32 at 109-15 (L: 108-16 / H: 109-26)

- Dec Ultra futures up 2/32 at 112-19 (L: 111-08 / H: 113-01)

US 10Y FUTURE TECHS: (Z3) Trend Direction Remains Down

- RES 4: 109-20 High Sep 19

- RES 3: 108-08+/16 50-day EMA / High Oct 12 and key resistance

- RES 2: 107-22+ High Oct 16

- RES 1: 106-27+ 20-day EMA

- PRICE: 106-06 @ 10:32 BST Oct 30

- SUP 1: 105-10+ Low Oct 19 and the bear trigger

- SUP 2: 104-26 2.00 proj of the Jul 18 - Aug 4 - Aug 10 price swing

- SUP 3: 104-02+ 2.0% 10-dma envelope

- SUP 4: 103-20+ Low Jun’07

The trend condition in Treasuries is unchanged and the direction remains down. The recent breach of 106-03+, the Oct 4 low, confirmed a resumption of the downtrend and an extension of the price sequence of lower lows and lower highs. The move down has exposed 104-26, a Fibonacci projection. Key short-term trend resistance is at 108-16, the Oct 12 high. Initial firm resistance is at 106-27+, the 20-day EMA.

SOFR FUTURES CLOSE

- Dec 23 -0.015 at 94.570

- Mar 24 -0.015 at 94.660

- Jun 24 -0.020 at 94.880

- Sep 24 -0.025 at 95.145

- Red Pack (Dec 24-Sep 25) -0.025 to -0.015

- Green Pack (Dec 25-Sep 26) -0.015 to -0.005

- Blue Pack (Dec 26-Sep 27) -0.005 to -0.005

- Gold Pack (Dec 27-Sep 28) steady

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00404 to 5.32008 (-0.00274 total last wk)

- 3M -0.00609 to 5.37712 (-0.00677 total last wk)

- 6M -0.00614 to 5.43449 (-0.01628 total last wk)

- 12M -0.01373 to 5.35922 (-0.03054 total last wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $94B

- Daily Overnight Bank Funding Rate: 5.32% volume: $238B

- Secured Overnight Financing Rate (SOFR): 5.31%, $1.496T

- Broad General Collateral Rate (BGCR): 5.30%, $564B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $556B

- (rate, volume levels reflect prior session)

FED REVERSE REPO OPERATION

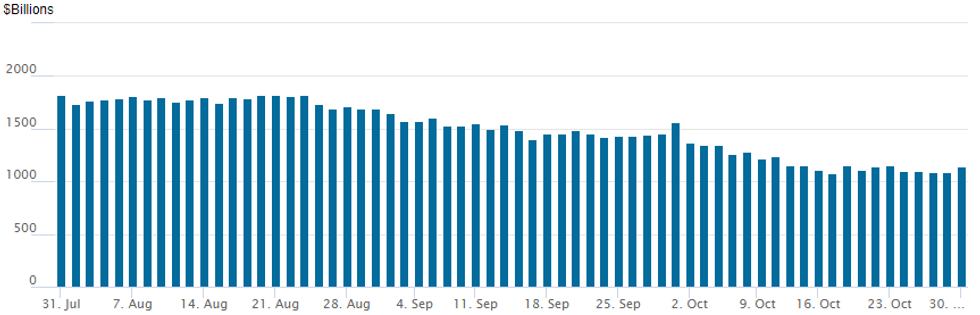

NY Federal Reserve/MNI

The NY Fed Reverse Repo operation usage inches up to $1,138.035B w/101 counterparties vs. $1,091.858B in the prior session -- just above October 17 level of $1,082.399B - the lowest level since mid-September 2021. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

$18.5B Corporate Debt Issued Monday, More to Follow

Multiple corporate issuers over the last half hour, running total at $18.5B with more to follow:

- Date $MM Issuer (Priced *, Launch #)

- 10/30 $6B #Morgan Stanley $1.65B 3Y +100, $350M 3Y SOFR+116.5, $2B 6NC5 +160, $2B 11NC10 +175

- 10/30 $4.5B #Bristol-Myers $1B 7Y +90, $1B 10Y +105, $1.25B 30Y +122, $1.25B 40Y +135

- 10/30 $3.75B #Santander $1B 4NC3 +165, $1.25B 5Y +180, $1.5B 10Y +205

- 10/30 $1.5B #Hyundai 2Y +125, $300M 2Y SOFR+132, $700M +5Y +178

- 10/30 $1B #Arthur Gallagher $400M +10Y +163, $600M +30Y +178

- 10/30 $1B #Discover Financial 11NC10 +310

- 10/30 $750M #Quest Diagnostics 10Y +153

- 10/30 $Benchmark Altria Grp 5Y +145, 10y +205

- 10/30 $Benchmark Bimbo Bakeries US +5Y +125, +10Y +155

- 10/30 $Benchmark Canadian National 10Y +125a, 30Y +140a

- 10/30 $Benchmark Ryder 5Y +150, 10Y +175

EGBs-GILTS CASH CLOSE: Soft Inflation Data Sees Bunds Outperform

Bunds handily outperformed Gilts Monday as softer-than-expected German and Spanish inflation data cemented the likelihood that the ECB is done hiking.

- The German short-end/belly outperformed 10s as state-level data and then the national print confirmed a slowdown in both headline and core pressures, while Spanish HICP was also below expectations.

- MNI's Nowcast for Tuesday's Eurozone HICP figure points to a sub 3% Y/Y reading.

- Periphery spreads fell as ECB cut pricing mounted (over 80bp in reductions priced in 2024, vs under 60bp a couple of weeks ago) on the back of the soft inflation data, with BTPs outperforming.

- EGB gains faded however. A Nikkei sources story pointing to the Bank of Japan potentially adjusting its yield curve control regime in a hawkish direction at its meeting overnight tonight saw global bonds pull back in European afternoon trade.

- Gilts traded relatively soft ahead of Thursday's BOE decision.

- Attention overnight will be on the BOJ decision, followed by French / Italian / Eurozone inflation data Tuesday morning.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.4bps at 3.013%, 5-Yr is down 1.5bps at 2.668%, 10-Yr is down 1bps at 2.822%, and 30-Yr is down 2bps at 3.104%.

- UK: The 2-Yr yield is up 0.6bps at 4.783%, 5-Yr is up 3.1bps at 4.506%, 10-Yr is up 1.7bps at 4.561%, and 30-Yr is up 0.6bps at 5.031%.

- Italian BTP spread down 5.6bps at 191.6bps / Spanish down 2.3bps at 107.2bps

FOREX USD Loses Ground As Equities Rally To Start The Week

- Firmer price action for major equity benchmarks have kept the greenback on the backfoot on Monday, with a very busy week of data and event risk ahead. The USD index slides 0.4% to start the week, with the associated gains broadly spread out among other G10 currencies.

- The most notable move on the session came for USDJPY as Nikkei headlines surfaced ahead of the Bank of Japan decision overnight. Reports the BOJ may allow further flexibility in yield movements bolstered the Japanese Yen and saw USDJPY fall from around 149.75 all the way down to fresh lows of 148.81 amid the broader greenback offer. The 20-day EMA has been breached, exposing the 50-day EMA as next support, at 147.98.

- The very early dip for EURUSD was associated with some lower-than-expected state level inflation data in Germany. However, as the session progressed, the more benign inflation data and the positive equity backdrop filtered through to a consistent grind higher for the pair. While EURUSD remains below 1.0694, technical conditions remain in bearish territory.

- AUD and NZD are among the session's best performers, rising over 0.5%. Market moves were underpinned by Australia's September retail sales, which topped expectations at 0.9% vs. Exp. 0.3%. Resultingly, AUD/USD trades back above 0.6350 and is narrowing in on the 50-dma resistance of 0.6395. Clearance here could be one of the first signs of a bullish reversal off the 0.6270 bottom, however the medium-term downtrend remains intact.

- China manufacturing and non-manufacturing PMIs kick off the docket overnight before the aforementioned BOJ policy decision. Eurozone inflation then takes focus before Canada GDP and US employment cost index figures. Later in the session, the MNI Chicago PMI and consumer confidence for the US are scheduled.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 31/10/2023 | 2330/0830 | * |  | JP | Labor Force Survey |

| 31/10/2023 | 2350/0850 | ** | | JP | Industrial production |

| 31/10/2023 | 0001/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 31/10/2023 | 0130/0930 | *** |  | CN | CFLP Manufacturing PMI |

| 31/10/2023 | 0130/0930 | ** | | CN | CFLP Non-Manufacturing PMI |

| 31/10/2023 | 0300/1200 | *** | | JP | BOJ policy announcement |

| 31/10/2023 | 0630/0730 | *** |  | FR | GDP (p) |

| 31/10/2023 | 0630/0730 | ** | | FR | Consumer Spending |

| 31/10/2023 | 0700/0800 | ** |  | DE | Retail Sales |

| 31/10/2023 | 0700/0800 | ** | | DE | Import/Export Prices |

| 31/10/2023 | 0730/0830 | ** |  | CH | Retail Sales |

| 31/10/2023 | 0745/0845 | *** | | FR | HICP (p) |

| 31/10/2023 | 0745/0845 | ** | | FR | PPI |

| 31/10/2023 | 0900/1000 | *** |  | IT | GDP (p) |

| 31/10/2023 | 0900/1000 | *** | | DE | GDP (p) |

| 31/10/2023 | 1000/1100 | *** |  | EU | HICP (p) |

| 31/10/2023 | 1000/1100 | *** | | EU | EMU Preliminary Flash GDP Q/Q |

| 31/10/2023 | 1000/1100 | *** | | EU | EMU Preliminary Flash GDP Y/Y |

| 31/10/2023 | 1000/1100 | *** | | IT | HICP (p) |

| 31/10/2023 | 1100/1200 | ** | | IT | PPI |

| 31/10/2023 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 31/10/2023 | 1230/0830 | ** |  | US | Employment Cost Index |

| 31/10/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 31/10/2023 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 31/10/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 31/10/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 31/10/2023 | 1300/0900 | ** | | US | MNI Chicago Report |

| 31/10/2023 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 31/10/2023 | 1400/1000 | ** | | US | Housing Vacancies |

| 31/10/2023 | 1430/1030 | ** | | US | Dallas Fed Services Survey |

| 31/10/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.