Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI INTERVIEW: Fed Might Not Cut At All In '24-Ex-Fed Economist

- MNI US: Beige Book Sees Minor Dent In Otherwise Sharp Increase In Fed Rates

- MNI US: IP In Line After Revisions, Ends 2023 With A Weak Quarter

- MNI US: MBA Mortgage Applications See Second Strong Weekly Increase

- MNI US: Retail Sales Control Group Ends Q4 With Surprising, Relatively Broad-Based Strength

US

US FED (MNI): Stubborn price pressures could prevent the Federal Reserve from lowering interest rates this year as the economy remains strong and officials worry about easing prematurely, ex-Philadelphia Fed economist Dean Croushore told MNI. Markets have gotten way ahead of themselves by pricing in as many as six quarter-point rate cuts this year, he said, adding investors are engaged in wishful thinking about how dovish the U.S. central bank will actually be.

NEWS

INTERVIEW (MNI): EP Takes Aim At "Stricter" EU Fiscal Rules

The European Parliament will try to water down proposals for member states to limit fiscal deficits to 1.5% of gross domestic product over the medium term, the legislature’s representative in “trilogue” talks on the bloc’s new fiscal rules with the European Commission and the European Union’s Belgian presidency told MNI.

US (MNI): Trump On Track For Presidential Nomination Ahead Of New Hampshire Primary

Former President Donald Trump's decisive victory at this week's Iowa Caucuses has placed him firmly on track to secure the Republican presidential nomination, according to a new tracker published by FiveThirtyEight/ABC News. The New Hampshire primary on January 23 is the next event of the Republican primary calendar with polls putting former South Carolina Governor Nikki Haley in touching distance of Trump.

SECURITY (MNI): White House Re-Designates Houthis As Terrorist Group

White House National Security Adviser Jake Sullivan has released a statementconfirming that the Houthi rebels in Yemen have been re-designated as a 'specially designated terrorist group'.

US State Dept (MNI): No Sign Of "Full-Blown Conflagration" Despite Mid-East Flareups

US State Department Spokesperson Matthew Miller has told reporters that the US assesses positively that the conflict between Israel and Hamas remains unlikely to expand into a broader regional war, despite numerous cross-border flashpoints, including most recently an Iranian missile and drone strike on targets in Balochistan, Pakistan.

US-MEXICO (MNI): Cabinet-Level Talks On Migration To Take Place Friday

US Secretary of State Antony Blinken and Homeland Security Secretary Alejandro Mayorkas will host their Mexico counterparts in Washington on Friday to discuss bilateral measures to stem the flow of migrants into the US.

US TSYS Strong Data Weighs on Tsys, Rate Cut Projections Recede

- Treasury futures gapped lower after stronger than expected in December, rising 0.55% M/M (cons 0.4) after a marginally upward revised 0.35% M/M (initial 0.28). The control group, which feeds into GDP, was the clear standout, jumping 0.76% M/M (cons 0.2) after a slightly upward revised 0.47% (initial 0.40).

- A flurry of additional data kept Tsys anchored: Import/Export index come out higher (0.0% vs. -0.5% est) / lower (-0.9% vs. -0.7% est) respectively. Industrial production fared slightly better than expected in December, rising 0.05% M/M (cons -0.1) but the beat was offset by a downward revised 0.0% M/M (initial 0.2) in Nov.

- March'24 10Y futures initially fell to 111-11 (-16) before trading down to 111-09 by midmorning, just above initial technical support at 111-06+ (Low Jan 05). Tsy 10Y climbed to 4.1268% high before finishing at 4.1019%. After climbing to the highest levels since October, curves bear flattened: 2Y10Y -8.268 at -24.833.

- Tsy futures dipped (TYH3 111-13.5) after $13B 20Y bond auction re-open (912810TW8) tailed: drawing 4.423% high yield vs. 4.415% WI; 2.53x bid-to-cover vs. prior month's 2.55x.

- This morning's data dampened rate cut projections for the first half of 2024: January 2024 cumulative -0.6bp at 5.323%, March 2024 chance of rate cut falls to -57.2% w/ cumulative of -14.9bp at 5.180%, May 2024 no longer pricing in 25bp cut -- currently at -85.6% w/ cumulative -36.3bp at 4.966%. June 2024 still pricing in a 25bp cut, cumulative -61.5bp at 4.714%. Fed terminal at 5.315% in Feb'24.

- Cross asset summary: stocks weaker with S&P eminis -27.5 at 4771.0, oil near steady (WTI +0.27 at 72.67), Gold weaker (-22.60 at 2005.85).

OVERNIGHT DATA

MNI US DATA: Retail sales were stronger than expected in December, rising 0.55% M/M (cons 0.4) after a marginally upward revised 0.35% M/M (initial 0.28).

- The control group, which feeds into GDP, was the clear standout, jumping 0.76% M/M (cons 0.2) after a slightly upward revised 0.47% (initial 0.40).

- Within the control group, there were strong increases across clothing sales (1.5% M/M), general merchandise stores (1.3%, especially department stores 3%) and non-store retailers (1.5%).

- On a quarterly basis, overall retail sales climbed a 3.9% annualized in Q4 after 6.9% in Q3 and 0.4% in Q2. Control group retail sales meanwhile climbed 4.4% in Q4, after 6.2% in Q3 and 2.4% in Q2.

- Manufacturing production also increased 0.05% M/M (cons 0.0) after a more modest downward revised 0.24% M/M (initial 0.32) in Nov.

- Utilities offered a fourth consecutive monthly decline in seasonally adjusted terms, -1.0% M/M after -0.7%.

- It left overall industrial production up just 1.0% Y/Y (from the SA data) in December and with momentum fading quickly towards year-end with IP down -3.1% annualized in Q4 after +1.8% in Q3. These sort of contractions are more in keeping with an ISM manufacturing index that has been sub-50 since late 2022.

MNI US DATA: MBA composite mortgage applications for a second strong weekly gain in the week to Jan 12, rising a seasonally adjusted 10.4% after 9.9% the week prior.

- Gains were more balanced after the prior week’s refi-led increase, with refis up 10.8% and purchases 9.2%.

- The 30Y conforming mortgage rate unwound last week’s increase, down 6bps to 6.75% and closer to recent lows of 6.71%, 115bps below the late October cycle high.

- The decline in mortgage rates has helped mortgage purchase activity lift above 60% of 2019 levels, although refis are still barely 25%.

FED BEIGE BOOK (MNI): Fed Funds implied rates have dipped on the Fed’s Beige Book, but still see very strong increases on the day after a sizeable beat for retail sales built on prior upward pressure.

- March implied rates have now dipped 1bp from earlier brief highs of 5.20% (and currently imply a cumulative 14bp of cuts vs 19bp pre-Waller).

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 128.16 points (-0.34%) at 37230.68

- S&P E-Mini Future down 33 points (-0.69%) at 4764.75

- Nasdaq down 115.1 points (-0.8%) at 14828.16

- US 10-Yr yield is up 4.4 bps at 4.1019%

- US Mar 10-Yr futures are down 13/32 at 111-14

- EURUSD up 0.0003 (0.03%) at 1.0878

- USDJPY up 1.01 (0.69%) at 148.2

- WTI Crude Oil (front-month) up $0.29 (0.4%) at $72.66

- Gold is down $21.86 (-1.08%) at $2006.52

- European bourses closing levels:

- EuroStoxx 50 down 43.43 points (-0.98%) at 4403.08

- FTSE 100 down 112.05 points (-1.48%) at 7446.29

- German DAX down 139.99 points (-0.84%) at 16431.69

- French CAC 40 down 79.31 points (-1.07%) at 7318.69

US TREASURY FUTURES CLOSE

- 3M10Y +2.931, -128.583 (L: -139.856 / H: -127.175)

- 2Y10Y -8.037, -24.602 (L: -27.479 / H: -15.973)

- 2Y30Y -10.806, -3.613 (L: -6.88 / H: 8.469)

- 5Y30Y -6.882, 29.155 (L: 27.116 / H: 37.004)

- Current futures levels:

- Mar 2-Yr futures down 7.75/32 at 102-22.5 (L: 102-20.625 / H: 102-31.5)

- Mar 5-Yr futures down 12/32 at 107-29.75 (L: 107-25.75 / H: 108-13.75)

- Mar 10-Yr futures down 12.5/32 at 111-14.5 (L: 111-09 / H: 112-01.5)

- Mar 30-Yr futures down 10/32 at 120-24 (L: 120-12 / H: 121-18)

- Mar Ultra futures down 3/32 at 127-1 (L: 126-10 / H: 127-30)

US 10Y FUTURE TECHS: (H4) Support Remains Intact

- RES 4: 114-06+ 2.00 proj of the Oct 19 - Nov 3 - Nov 13 price swing

- RES 3: 114-00 Round number resistance

- RES 2: 113-12 High Dec 27 and the bull trigger

- RES 1: 112-26+ High Jan 12

- PRICE: 111-16 @ 1140 ET Jan 17

- SUP 1: 111-06+ Low Jan 05

- SUP 2: 111-02+ 50-day EMA

- SUP 3: 110-16 Low Dec 13

- SUP 4: 109-31+ Low Dec 11 and a key short-term support

Treasuries traded lower Tuesday and first resistance has been defined at 112-26+, the Jan 12 high. The trend outlook remains bullish and the recovery that started Jan 5 suggests that the correction between Dec 27 - Jan 5, may be over. If correct, this signals scope for a move towards the key resistance and bull trigger at 113-12, the Dec 27 high. Clearance of this level would open 114-00. A breach of 111-06+ support, Jan 5 low, would be bearish.

SOFR FUTURES CLOSE

- Mar 24 -0.050 at 94.895

- Jun 24 -0.120 at 95.340

- Sep 24 -0.160 at 95.750

- Dec 24 -0.165 at 96.105

- Red Pack (Mar 25-Dec 25) -0.165 to -0.12

- Green Pack (Mar 26-Dec 26) -0.10 to -0.07

- Blue Pack (Mar 27-Dec 27) -0.055 to -0.035

- Gold Pack (Mar 28-Dec 28) -0.03 to -0.02

FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00302 to 5.33478 (-0.00320/wk)

- 3M +0.01166 to 5.30957 (-0.00696/wk)

- 6M +0.02709 to 5.11611 (-0.03736/wk)

- 12M +0.03590 to 4.68892 (-0.10086/wk)

- Secured Overnight Financing Rate (SOFR): 5.32% (+0.01), volume: $1.854T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $695B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $667B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $85B

- Daily Overnight Bank Funding Rate: 5.31% (-0.01), volume: $253B

FED Reverse Repo Operation:

NY Federal Reserve/MNI

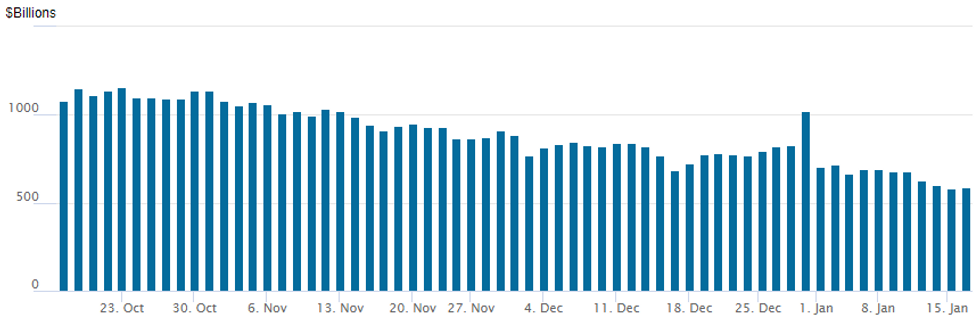

- RRP usage inches back up to $590.191B vs. $583.103B yesterday - the lowest level since mid-June 2021.

- Meanwhile, the number of counterparties bounces to 77 vs. 65 yesterday, the lowest since July 7, 2021.

PIPELINE: $2.5B PNC 2Pt Launched

- Date $MM Issuer (Priced *, Launch #

- 1/17 $4B *CADES 3Y SOFR+38

- 1/17 $2.5B #PNC Financial $1B 4NC3 +118, $1.5B 11NC10 +158

- 1/17 $1.75B #CAF 5Y SOFR+130

- 1/17 $1.75B #Republic of Chile 5Y +85

- 1/17 $1.5B *Kommunalbanken 5Y SOFR+50

- 1/17 $1.5B #Council of Europe Development Bank (COE) 5Y SOFR+41

- 1/17 $1.25B *Province of Alberta 10Y SOFR+87

- 1/17 $1B *Japan Bank for International Cooperation (JBIC) 7Y SOFR +77

- 1/17 $750M #EQT Corp 10Y +165

- 1/17 $700M *Woori Bank $300M 3Y +75, $400M 5Y 85

- 1/17 $500M #Air Lease 5Y +135

- 1/17 $650M #Aircastle 5Y +205

- 1/17 $Benchmark Banque Federative du Credit Mutuel (BFCM) 3Y +97, 3Y SOFR+113

- 1/17 $Benchmark Blue Owl Capital 5Y +220

- US$ Issuance expected for Thursday

- 1/18 $Benchmark European Bank for Reconstruction/Development 5Y SOFR+42a

- 1/17 $Benchmark African Development Bank 3YSOFR+33a

- 1/18 $Benchmark BNG Bank 5Y SOFR+52a

EGBs-GILTS CASH CLOSE: Strong Bear Flattening Move As Cuts Priced Out

European curves bear flattened sharply Wednesday as central bank cutting expectations receded further.

- Stronger-than-expected UK inflation data set a bearish tone for the session (headline, core and services all surprising to the upside - our review is here), while ECB's Lagarde noted in an interview this morning that "too optimistic" markets regarding cuts could impair disinflation progress.

- The bear-flattening sell-off extended through the afternoon on strong US retail sales data.

- Market-implied 2024 BoE cuts retraced by a full 25bp reduction (now just 104bp seen this year vs 130bp yesterday), while ECB 2024 cuts pulled back by 10bp.

- The UK inflation data ensured Gilts underperformed Bunds, while periphery spreads widened modestly on the more hawkish ECB outlook and broader risk-off moves amid the repricing.

- ECB's Nagel speaks after the close. Thursday sees largely 2nd tier European data, with another appearance by ECB's Lagarde, and the accounts of the ECB December meeting.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 9.8bps at 2.698%, 5-Yr is up 8.8bps at 2.242%, 10-Yr is up 5.8bps at 2.316%, and 30-Yr is up 0.4bps at 2.469%.

- UK: The 2-Yr yield is up 21.5bps at 4.378%, 5-Yr is up 23.7bps at 3.907%, 10-Yr is up 18.8bps at 3.985%, and 30-Yr is up 15.5bps at 4.64%.

- Italian BTP spread up 2.9bps at 160.1bps / Spanish bond spread up 1.4bps at 93.5bps

FOREX Higher US Yields & Lower Equities Prompting Further JPY Declines

- Further upward pressure on US yields, and the notable 15bp move for the 2-year, has prompted an extension of overall greenback strength on Wednesday. The 0.2% advance for the USD index screens as more moderate than the prior session, but extends the week’s advance to 1.12%. Greenback gains have once again been most notable against the struggling Japanese Yen.

- USDJPY registered another near 1% range on the session, reaching as high as 148.52 in the aftermath of the stronger-than-expected US retail sales data, and in particular the substantially higher control group figure. The data has weighed on the front-end of the Treasury curve, which continues to filter through to a weaker JPY, which remains the most sensitive to diverging yield differentials.

- Additionally, risk-off sentiment continues to permeate through to equity markets, with the S&P 500 dropping close to 1% on the session, weighing on the likes of AUD and NZD. Notably, AUDUSD’s low of 0.6525 closely matches a strong medium term pivot point and touted key support at the December 7 low.

- Bucking the trend in G10 is GBP, which relatively outperforms following the above-estimate inflation data this morning, with headline, core and services all surprising to the upside. As such, GBP retains its crown as one of the best performing major currencies this year, with cable up 0.32% as we approach the APAC crossover.

- In emerging markets, it’s worth noting that USDMXN had a decent extension higher early on Wednesday, reaching as high as 17.3860, briefly extending yesterday’s impressive 2% advance by a further percentage point, before those gains were steadily pared across the afternoon.

- Australian employment will headline Thursday’s APAC docket, before focus will turn to US jobless claims and Philly fed manufacturing data. Wires will continue to be monitored for any significant headlines emanating from officials at the World Economic Forum in Davos.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/01/2024 | 0030/1130 | *** |  | AU | Labor Force Survey |

| 18/01/2024 | 0900/1000 | ** |  | EU | EZ Current Account |

| 18/01/2024 | 1000/1100 | ** | | EU | Construction Production |

| 18/01/2024 | 1230/0730 |  | US | Atlanta Fed's Raphael Bostic | |

| 18/01/2024 | 1330/0830 | *** | | US | Jobless Claims |

| 18/01/2024 | 1330/0830 | *** | | US | Housing Starts |

| 18/01/2024 | 1330/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 18/01/2024 | 1445/0945 | *** | | US | MNI Chicago Business Barometer Seasonal Adjustment |

| 18/01/2024 | 1515/1615 | | EU | ECB's Lagarde participates in Stakeholder Dialogue at WEF | |

| 18/01/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 18/01/2024 | 1600/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 18/01/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 18/01/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 18/01/2024 | 1705/1205 | | US | Atlanta Fed's Raphael Bostic | |

| 18/01/2024 | 1800/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 19/01/2024 | 2330/0830 | *** |  | JP | CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.