- MNI US DATA: Initial Claims Surprise Lower In Payrolls Period But Still Trend Higher

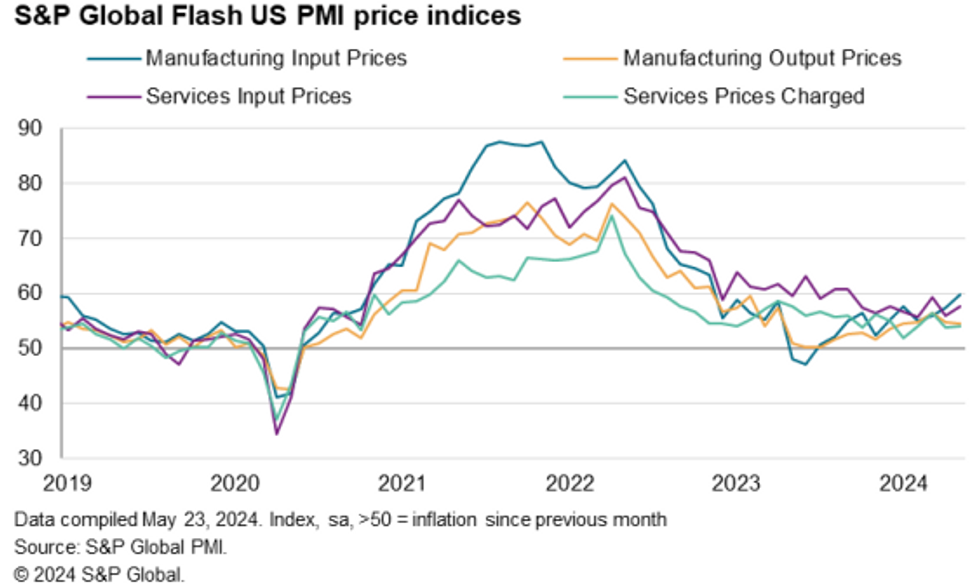

- MNI US DATA: A Large Services-Led Beat For Flash PMIs

US TSYS Near Lows, Flash PMIs Sapped Early Risk-On Tone

- Treasury futures remain weaker after the bell but off midmorning lows after higher than expected flash PMIs: Services PMI (54.8 vs. 51.2 est) and Composite PMI (54.4 vs. 51.2 est) while Manufacturing PMI slightly higher (50.9 vs. 49.9 est).

- The flash data had sapped the early risk-on tone with S&P Eminis and Nasdaq indexes marking new all-time highs before extending lows amid several rounds of program selling/profit taking ahead of the extended Memorial holiday weekend.

- Not a big reaction, Treasury futures did recede after lower than expected weekly claims at 215k vs. 220k est, prior revised to 223k from 222k. Continuing claims near in-line at 1.794M vs. 1.793M est, prior down-revised to 1.786M from 1.794M.

- Rate cut projections have receded vs late Wednesday levels (*): June 2024 at -0% w/ cumulative rate cut 0.0bp at 5.328%, July'24 at -10.0% (-16.0%) w/ cumulative at -2.5bp (-5.2bp) at 5.302%, Sep'24 cumulative -14.2bp (-17.8bp), Nov'24 cumulative -21.2bp (-26.2bp), Dec'24 -34.8bp (-40.6bp).

- Look ahead to Friday's data calendar: focus on Durables/Cap Goods and the latest UofM Sentiment. June Treasury options expire tomorrow as well.

NEWS

G7 (MNI): No Decision On Use Of Frozen Russian Assets Expected At G7 Meeting - Lindner: Wires carrying comments from Germany Finance Minister, Christian Lindner, speaking at the G7 foreign ministers and central bank governors meetings in Stresa, Italy stating that there are, "many open questions about use of Russian frozen assets, which will be discussed," at the meeting.

US-RUSSIA (MNI): Putin Signs Decree Authorizing Seizure Of US Assets In Russia: Russian President Vladimir Putin signed a decree authorizing the seizure of US assets in Russia to compensate for damages related to any potential US seizure of Russian assets. The Russian decree is likely to be triggered if the US pursues the seizure of Russian sovereign assets, authorized the US Congress via the REPO Act.

UK (MNI): Farage Confirms He Will Not Stand Providing Some Boost To Conservatives: Veteran euro-sceptic politician Nigel Farage has confirmed that he will not stand in the upcoming general election for the right-wing populist Reform UK.

ASIA (MNI): China, Japan, SK To Hold Trilateral Summit 26-27 May: A trilateral summit between China, Japan, and South Korea is set to take place 26-27 May in the South Korean capital Seoul. South Korean President Yoon Suk-yeol's office announced the meeting earlier today. Japan's Chief Cabinet Secretary Yoshimasa Hayashi confirmed a short time ago that PM Fumio Kishida would be in attendance, while Premier Li Qiang is set to represent China at the talks.

OVERNIGHT DATA

US DATA (MNI): A Large Services-Led Beat For Flash PMIs: The S&P Global US PMIs saw a large upside surprise in the flash May release, indicating its sharpest growth for just over two years, driven by services.

- Manufacturing: 50.9 (cons 49.9) after 50.0

- Services: 54.8 (cons 51.2) after 51.3

- Composite: 54.4 (cons 51.2) after 51.3

- Further details from the press release: "Although companies continued to report lower employment, the rate of job losses moderated amid improved business confidence for the year ahead and higher order book intakes."

US DATA (MNI): Initial Claims Surprise Lower In Payrolls Period But Still Trend Higher: Initial jobless claims surprised lower with a seasonally adjusted 215k (cons 220k) in the week to May 18, covering the payrolls reference period, after a marginally upward revised 223k (initial 222k).

- The four-week average still increased 2k to 220k for a 10k increase since late April, nudging above the 218k averaged in 2019 for the first time since Sep’23.

- In NSA terms, the 192k figure is firmly in keeping with recent years and there don’t look to be any particular standout readings in the state-wide data.

US DATA (MNI): Continuing Claims Close To Expectations, Keeping To Prior Trends: Continuing claims meanwhile were almost exactly as expected at a seasonally adjusted 1794k (cons 1793k) in the week to May 11 after a downward revised 1786k (initial 1794k).

- The seasonally adjusted figures remain firmly within the narrow range seen since August, below the mid-Jan high of 1829k.

- In non-seasonally adjusted terms, the 1694k in the week to May 11 drifts a little higher above comparable levels from 2023 plus also 2018-19, and remains far higher than 2022 levels, but there’s no sign of a meaningful break higher compared to the relative trends seen in recent months.

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 627.98 points (-1.58%) at 39043.02

- S&P E-Mini Future down 46.75 points (-0.88%) at 5281.25

- Nasdaq down 76.1 points (-0.5%) at 16725.75

- US 10-Yr yield is up 5.5 bps at 4.4767%

- US Jun 10-Yr futures are down 11/32 at 108-22

- EURUSD down 0.0015 (-0.14%) at 1.0809

- USDJPY up 0.1 (0.06%) at 156.9

- Gold is down $46.6 (-1.96%) at $2332.21

- European bourses closing levels:

- EuroStoxx 50 up 12.43 points (0.25%) at 5037.6

- FTSE 100 down 31.1 points (-0.37%) at 8339.23

- German DAX up 11.12 points (0.06%) at 18691.32

- French CAC 40 up 10.22 points (0.13%) at 8102.33

US TREASURY FUTURES CLOSE

- 3M10Y +5.381, -93.697 (L: -102.269 / H: -91.923)

- 2Y10Y -0.9, -45.853 (L: -46.976 / H: -44.038)

- 2Y30Y -1.718, -35.275 (L: -38.473 / H: -32.218)

- 5Y30Y -2.081, 5.276 (L: 3.044 / H: 8.504)

- Current futures levels:

- Jun 2-Yr futures down 3.375/32 at 101-15.75 (L: 101-14.5 / H: 101-20.125)

- Jun 5-Yr futures down 8/32 at 105-15.25 (L: 105-11.75 / H: 105-26)

- Jun 10-Yr futures down 11/32 at 108-22 (L: 108-17.5 / H: 109-06)

- Jun 30-Yr futures down 17/32 at 116-24 (L: 116-15 / H: 117-21)

- Jun Ultra futures down 23/32 at 123-19 (L: 123-06 / H: 124-26)

US 10Y FUTURE TECHS: (M4) Approaching First Support

- RES 4: 110-16 50.0% retracement of the Feb 1 - Apr 25 bear leg

- RES 3: 110-06 High Apr 4

- RES 2: 110-00 Round number resistance

- RES 1: 109-07/109-31+ 50-day EMA / High May 16 and bull trigger

- PRICE: 108-22 @ 17:14 BST May 23

- SUP 1: 108-15 Low May 14 and key support

- SUP 2: 108-06 Low May 3

- SUP 3: 107-25 Low May 2

- SUP 4: 107-04 Low Apr 25 and the bear trigger

Treasuries traded lower Thursday on the back of strong PMI data, extending the pullback from the recent 109-31+ high on May 16. Support to watch lies at 108-15, the May 14 low. A break of this level would undermine the recent bullish theme and instead signal scope for a deeper retracement. This would open 108-06, the May 3 low. On the upside, 109-31+ is the bull trigger where a break would confirm a resumption of the bull cycle.

SOFR FUTURES CLOSE

- Jun 24 -0.010 at 94.663

- Sep 24 -0.035 at 94.810

- Dec 24 -0.050 at 95.010

- Mar 25 -0.070 at 95.220

- Red Pack (Jun 25-Mar 26) -0.085 to -0.075

- Green Pack (Jun 26-Mar 27) -0.075 to -0.06

- Blue Pack (Jun 27-Mar 28) -0.055 to -0.04

- Gold Pack (Jun 28-Mar 29) -0.035 to -0.02

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00009 to 5.32216 (+0.00240/wk)

- 3M +0.00139 to 5.33085 (+0.00505/wk)

- 6M -0.00074 to 5.29392 (+0.01071/wk)

- 12M -0.01052 to 5.14754 (+0.02502/Wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.900T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $725B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $713B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $80B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $265B

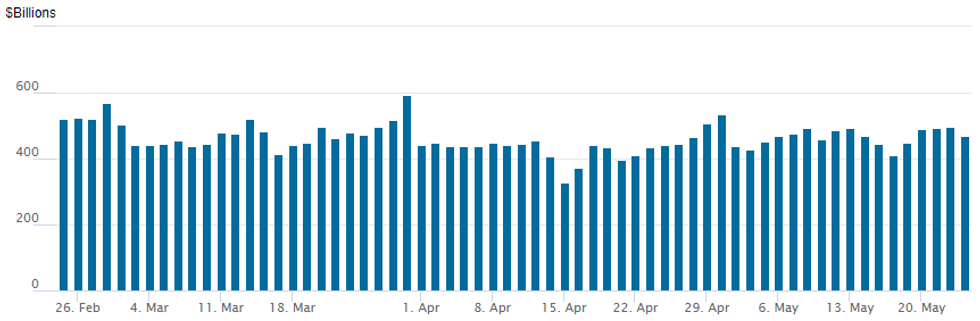

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage recedes up to $467.398B from $496.382B prior; number of counterparties 79. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

EGBs-GILTS CASH CLOSE: More Bear Flattening

European curves bear flattened for a second consecutive session Thursday, as central bank cutting expectations continued to be pared.

- The major market mover on the day was a surprisingly strong US April flash Services PMI reading, which saw Treasuries drop sharply, dragging Bunds and Gilts to session lows in the afternoon.

- Earlier, firmer-than-expected German flash PMIs more than countered the impact of a softer-than-expected French services print. UK (and to a lesser extent, Eurozone) PMIs were softer than expected, while the price components appeared mildly dovish.

- Eurozone Q1 negotiated wages accelerated versus Q4, but this brought limited reaction as it had been telegraphed by Wednesday's German data.

- By the cash close, implied ECB 2024 cuts had been pared to 59bp, vs 64bp Wednesday - the BoE equivalent was 33bp, vs 37bp yesterday and 55bp prior to Wednesday's CPI print.

- Bunds underperformed Gilts. Periphery EGB spreads were little changed.

- UK retail sales and German GDP data feature first thing Friday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 7.1bps at 3.079%, 5-Yr is up 7.4bps at 2.658%, 10-Yr is up 6.2bps at 2.596%, and 30-Yr is up 4.2bps at 2.711%.

- UK: The 2-Yr yield is up 4.9bps at 4.501%, 5-Yr is up 3.7bps at 4.173%, 10-Yr is up 2.7bps at 4.259%, and 30-Yr is up 1.3bps at 4.696%.

- Italian BTP spread up 0.1bps at 129.1bps / Spanish down 0.7bps at 75.7bps

FOREX: Two Stage USD Recovery Aided By Strong US PMI Data And Sell Programs

- After initially fading in early Thursday trade, the USD index received a firm boost following the stronger than expected US PMI data, which indicated its sharpest growth for just over two years, driven by services.

- The increase then saw a second leg as large equity sell programs rolled through in what appears profit taking from earlier record highs, with the DXY punching to new best levels for the week and above the 105 mark.

- CAD sits at the bottom of the FX pack, hindered by Can-US front-end yield differentials continuing the week’s sharp push lower after subdued core CPI trends in Tuesday’s release.

- The stronger greenback also saw the earlier Euro bid (kick-started by the stronger German PMIs) dissipate and EURUSD has edged back towards the 1.08 handle as we approach the APAC crossover.

- Meanwhile, the risk-off nature of the second leg saw JPY recover some of its underperformance, with USDJPY dipping back below 157.00 after a high of 157.20. The 157.00 handle initially saw some noisy two-way price action on the original breach higher.

- NZD is moderately outperforming most at near flat on the day. New Zealand retail sales for Q1 rose +0.5%, against a consensus expectation for a fall and added some bullish sentiment to the hawkish-to-expectations RBNZ meeting earlier in the week.

- Participants remain aware of the 0.8500 handle in EURGBP marking an important support over the past 18 months. The cross has failed to close below 0.8500 since August 2022, with several tests over the past year being well respected.

- Technically we noted that Wednesday’s move resulted in a break of short-term support at 0.8531, the Apr 30 low, confirming an extension of the reversal that started May 9. Note that the key support and bear trigger lies at 0.8493, and a sustained breach of this point would be required to enhance bearish momentum. Initial resistance moves down to 0.8566, the 20-day EMA.

- UK and Canada retail sales highlight the data docket on Friday before the revised set of UMich sentiment and inflation expectations data.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/05/2024 | 2301/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 24/05/2024 | 2330/0830 | *** |  | JP | CPI |

| 24/05/2024 | 0600/0700 | *** | | UK | Retail Sales |

| 24/05/2024 | 0600/0800 | *** |  | DE | GDP (f) |

| 24/05/2024 | 0600/0800 | ** |  | SE | PPI |

| 24/05/2024 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 24/05/2024 | 0700/0900 | ** |  | ES | PPI |

| 24/05/2024 | 0700/0900 |  | EU | ECB's Schnabel speech at Germany PhD conference | |

| 24/05/2024 | 1230/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 24/05/2024 | 1230/0830 | ** | | CA | Retail Trade |

| 24/05/2024 | 1230/0830 | ** |  | US | Durable Goods New Orders |

| 24/05/2024 | 1335/0935 | | US | Fed Governor Christopher Waller | |

| 24/05/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 24/05/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |