Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

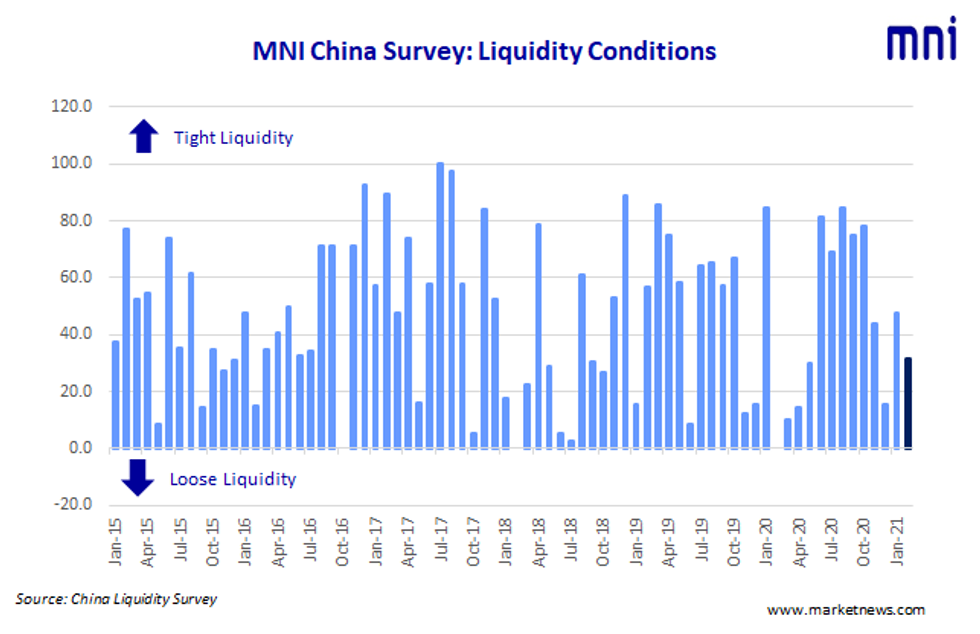

Condition across China's interbank market returned to a semblance of normality after the Lunar New Year holiday with money rates back in a familiar trading ranges after the sharp rises in late January, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index eased to 31.6 in February from 47.4, with twice as many traders reporting 'looser' conditions than last month. Just over half of participants said liquidity was little changed from January.

The higher the index reading, the tighter liquidity appears to survey participants.

Source: MNI China Liquidity Index

Source: MNI China Liquidity Index

The Guidance Clarity Index stood at 71.1 in February, up from a previous 68.4, as 42.1% traders pointed to the PBOC's policy transparency. The central bank, against tradition, explained its reasoning behind reduced injections before the holiday and said markets had focused on money market rates rather than OMO volumes. The move eased tension, with markets more convinced monetary policy had not been tightened.

"Liquidity conditions eased with the overnight repo rate and 7-day repo rate falling into a normal range," a trader with State-owned bank based in Shenzhen told MNI. The central bank conducted CNY200 billion MLF in February to replace those maturing, although draining a net CNY264 billion from the market via open market operations as of February 23, MNI calculated.

ECONOMY RECOVERING

The Economy Condition Index stood at 81.6, up from a previous 76.3 and marking the tenth reading above 70. Almost two-thirds of participants were encouraged by robust retail sales during the holiday period.

Retail sales were better than expected during the Spring Festival holiday, with catering and excursions well supported despite the government's stay-at-home message, a Shanghai-based trader said, adding that the economy is continuing to recovery.

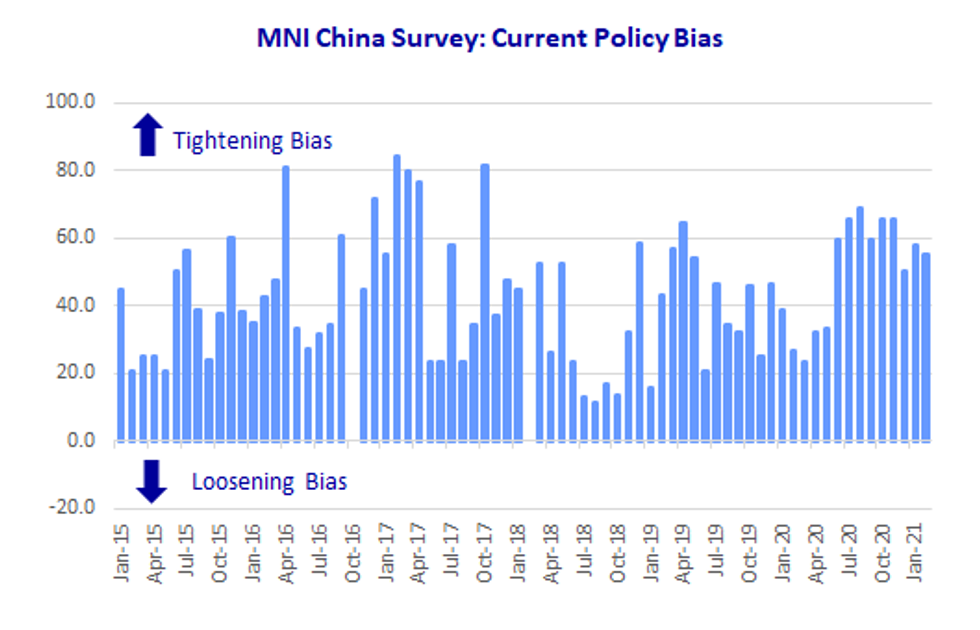

The PBOC Policy Bias Index slid to 55.3 in February from 57.9 in January, with the vast majority traders -- 89.5% of them -- are certain of policy persistence, with one Beijing based trader at the leading state-owned bank saying he saw "no sharp turn in the short term)."

Source: MNI China Liquidity Survey

Source: MNI China Liquidity Survey

REPO MARKET SETTLES

The 7-Day Repo Rate Index dropped to 44.7 from January's 65.8, with some 47.4% of the participants seeing rates fall as conditions have eased since the end of January. The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 2.2770% Tuesday.

The 10-year CGB Yield Index, jumped to 76.3 from 36.8 in the previous month. "The 10-Y CGB yield is likely to rise, or trade between between 3.1% – 3.3% on back of the rise in U.S. treasuries and the domestic recovery," a trader in southeast China Fuzhou explained.

The MNI survey collected the opinions of 19 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed-income and currency instruments, and the main funding source for financial institutions. Interviews were conducted Feb 1 – Feb 19.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.