Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

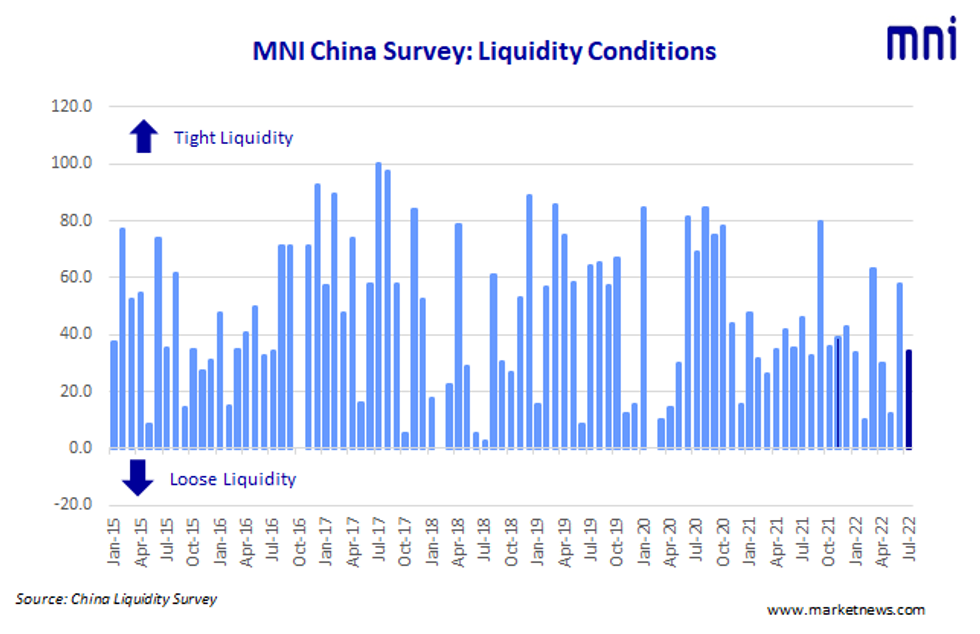

China’s interbank markets saw a recovery in liquidity levels in July despite the People’s Bank of China withdrawing funds to ensure no liquidity flood after the half-year passed, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index, fell to 34.4 from 57.8 in June, with as many as 37.5% of the participants reporting improved liquidity after the half year adjustments.

The higher the index reading, the tighter liquidity appears to survey participants.

“The entire (liquidity) situation remained stable in July with fewer factors or bonds issuance to impact conditions,” a Liaoning based trader told MNI, with a senior trader with a state-owned bank in Beijing noting the central bank continues to provide liquidity to support the real economy

The People’s Bank of China conducted CNY100 billion MLF in July, offsetting the equivalent maturity. PBOC drained net CNY72 billion via its open market operation as of July 26, MNI calculated.

SLOWING RECOVERY

The Economy Condition Index, slipped to 73.4 in July from June’s 14-month high 79.7, weighed by some modest concerns over the risk of fresh Covid disruptions.

The PBOC Policy Bias Index edged down to 35.9 in July, from 40.6 in June, with nearly three-quarters of survey participants seeing current policy on hold and another the rest seeing a looser stance.

“The authorities are providing a wide credit environment for market participants, the loose stance won’t tighten anytime soon,” a trader with a leading commercial bank in Zhejiang commented.

The Guidance Clarity Index stood at 59.4 in July, picking up from 56.3 last month. The high level of the reading underlines the market’s current understanding of the central bank’s action.

“It’s still clear to see that the central bank is taking care of fund availability, with an increase in liquidity of little necessity just now,” the Beijing trader told MNI.

RISING RATES

The 7-Day Repo Rate Index edged down to 51.6 from 60.9 reading, with rates expected not to deviate from policy rate by 59.4% participants. The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 1.5766% Tuesday.

The 10-year CGB Yield Index stood at 56.3 in July, down from the previous 68.8 reading, with 21.9% of respondents predicting lower yields.

“The domestic economy, especially service sector and employment, is facing downward pressure due the over and over again covid lockdowns, thus the overall return on assets will decline, and the bond yields will also move lower,” the Shanghai trader said.

The MNI survey collected the opinions of 32 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted July 11 – July 22.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.