Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

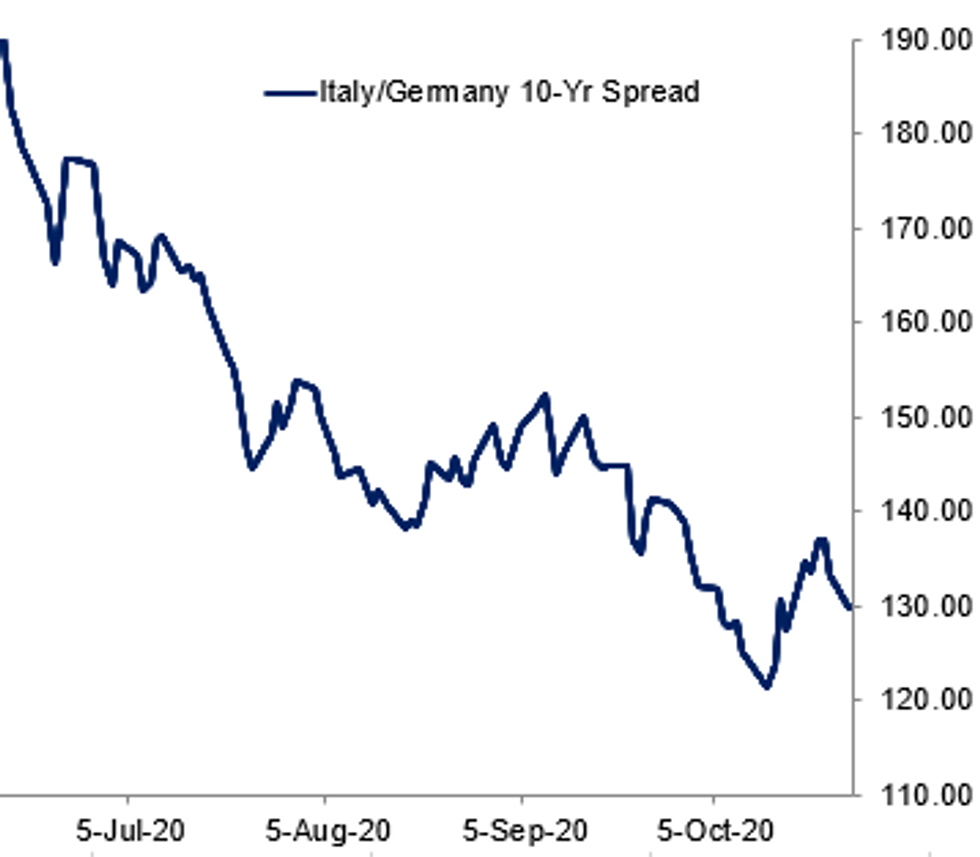

Fig. 1: BTPs Benefit From Ratings Surprise

BBG/MNI

BBG/MNI

EGB SUMMARY: Bunds largely ignore risk-off moves

Bunds have ignored the global risk-off move and in spite of a decent rally in Treasuries and gilts, Bunds yields are higher on the day.

- The move in Bunds is consistent with the move seen in EGB peripherals with spreads tightening mostly through the morning session before holding steady through the afternoon.

- BTPs had been the major outperformer in EGB space through the morning after the decision by S&P to affirm the BBB rating and upgrade the outlook to stable from negative. However, spreads have since come in a little.

- Focus remains on Covid-19, Brexit talks and the ECB meeting, with the announcement and press conference due Thursday.

- Bund futures are up 0.04 today at 175.30 with 10y Bund yields up 0.5bp at -0.572% and Schatz yields up 0.5bp at -0.758%.

- BTP futures are up 0.52 today at 149.38 with 10y yields down -2.9bp at 0.728% and 2y yields down -2.3bp at -0.366%.

- OAT futures are up 0.03 today at 169.37 with 10y yields up 0.5bp at -0.296% and 2y yields down -0.8bp at -0.700%.

GILT SUMMARY: Giving Up Early Gains

It has been a relatively uneventful session marked by weaker trading in equities.

- Gilts started the week on a strong footing but soon gave up the early gains to trade back to flat on the day. Last yields: 2-year -0.0422%, 5-year -0.0345%, 10-year 0.2702%, 30-year 0.8439%. The curve similarly trades flat on the day.

- The Dec-20 gilt future trades at 135.54, towards the bottom end of the day's relatively tight range (L: 135.36 / H: 135.80).

- Short sterling futures are broadly 0.5-1.5 ticks higher in whites/reds/greens/blues.

- Tomorrow the DMO will sell GBP3.25bn of the 0.125% Jan-24 gilt and GBP1.0bn of the 1.625% Oct-71 gilt.

- UK specific data releases this week will be largely second tier and unlikely to be market moving. Next up is CBI Retailing Reported Sales data for October, which will be published tomorrow.

- This week's ECB meeting is unlikely to yield any material policy changes, but any hint of further easing at the subsequent December meeting could spillover to the gilt market.

AUCTIONS/SUPPLY:

FRANCE T-BILL AUCTION RESULTS: France Sells E5.289bn of BTFs- E2.096bn of the 3-month BTF: Average yield -0.673%, bid-to-cover 2.60x

- E1.495bn of the 6-month BTF: Average yield -0.652%, bid-to-cover 3.32x

- E1.698bn of the 12-month BTF: Average yield -0.638%, bid-to-cover 2.39x

DEBT FUTURES/OPTIONS:

- ERH2 100.50^ bought for 20 in 2.75k (v 100.55, 17d)

- 2RZ0C 100.50 bought for 6 in 5k

- 2RH1 100.50/100.625 1x2 call spread bought for 2 in 2.5k

- RXZ0 174.00 put bought for 26 in 1k

- RXZ0 175.00/174.00 1x1.5 put spread bought for 16 in 0.75k

- LH1 99.875/100.125 ^^ sold at 2.75 in 36k

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok