Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

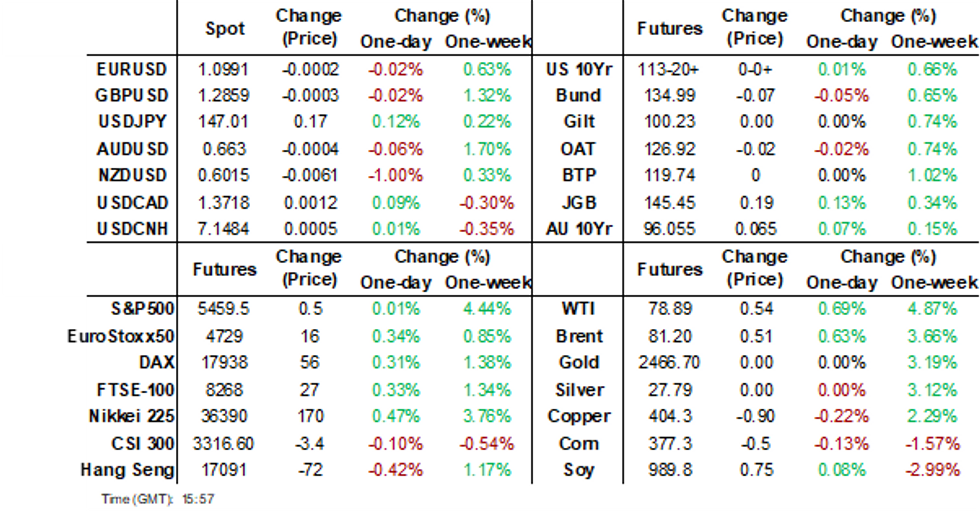

- The RBNZ commenced its easing cycle, cutting rates by 25bps, but considered a 50bps cut. RBNZ dated OIS pricing is 10-18bps softer across meetings after the Decision. The market had attached a 58% chance of a 25bp cut today. NZD/USD is off 1%.

- PM Kishida will not run in the ruling Liberal Democratic Party’s leadership election in September, meaning Japan will have a new Prime Minister post these elections. JGB yields initially rose on the news but have subsequently reversed the move, with yen behaving in a similar fashion.

- In China, following several days of higher yields, the bond market grabbed hold of the drop in aggregate financing and rallied hard throughout the day.

- Later the focus will be on US July CPI which is forecast to remain at 3% y/y but for core to ease 0.1pp to 3.2% (see MNI CPI Preview). UK July CPI/PPI, euro area Q2 employment/GDP and June IP are also released.

MARKETS

US TSYS: Tsys Futures Little Changed Ahead Of US CPI Later

- Treasury futures saw some initial weakness in the first half of the session, although have since recovered to now trade little changed and at session's best levels.

- TUU4 is + 00⅛ at 103-12¾, while TYU4 was + 01+ at 113-21 and sits comfortably below initial resistance of 114-03 (Aug 6 highs), while support rests at 112-15 (20-day EMA)

- Earlier there was block buying in SOFR futures, we have since ticked a touch higher.

- RBNZ has cut rates by 25bps, while Japan's Prime Minister has announced that he will not be seeking re-election, neither of these events have had any impacts on us tsys so far.

- The tsy curve is little changed today with yields flat to 1bps higher, the 2yr is +0.8bps at 3.937%, while the 10yr is +0.2bp at 3.845%

- MNI US CPI Preview: Large Miss Needed For Fed To Guide 50bp Cuts - (See link)

- Focus will be all on CPI data later today while we also have MBA Mortgage Applications & $75B 42D CMB Tsy bill auction.

JGBS: Cash Curve Bull-Flattener, PM Kishida To Exit, US CPI Due

JGB futures are sharply richer and at session highs, +29 compared to settlement levels, despite a poor showing at today’s 5-year auction.

- The auction's low price failed to beat dealer expectations, and the cover ratio declined to 3.5109x from 4.256x at July’s auction. The auction tail was also longer. Today’s auction followed a disappointing 10-year JGB auction in August.

- The results were likely affected by a bid that faced a lower yield, coupled with a 2/5 curve that was flatter than the July auction and is now near the lower end of its range since December 2022.

- PM Kishida will not run in the ruling Liberal Democratic Party’s leadership election in September. JGB yields initially rose on the news but have subsequently reversed the move.

- Cash US tsys are flat to 1bp cheaper in today's Asia-Pac session ahead of US CPI data later today.

- The cash JGB curve has bull-flattened, with yields flat to 4bps lower. The benchmark 10-year yield is 3.0bps lower at 0.817% versus the cycle high of 1.108%.

- The swaps curve has also bull-flattened, with rates 1-3bps lower. Swap spreads are mostly tighter.

- Tomorrow, the local calendar will see Q2 GDP, and June Capacity Utilisation and Industrial Production data alongside BoJ Rinban Operations covering 1-3-year and 5-25-year+ JGBs.

JAPAN: Prime Minister Kishida Not To Seek Second Term

Japan Prime Minister Kishida is reportedly set to announce he won't seek re-election as leader of Japan's LDP party. Kishida's tenure won't extend beyond September. The LDP will elect a new leader, who will then become Japan's new Prime Minister, bringing an end to Kishida's 3 year run as premier.

- Low approval ratings, reflecting a funding scandal, and high inflation, is cited as a contributing factor to Kishida's decision not to seek a second term.

- Outside of a brief round of yen strength, market reaction has been limited to the news. BBG notes Defence Minister Shigeru Ishiba is a potential successor per onshore media.

AUSSIE BONDS: Richer, Spillover From NZGBs Ahead Of US CPI Data, Jobs Data Tomorrow

ACGBs (YM +9.0 & XM +7.5) are richer and near Sydney session highs.

- The local market saw a positive spillover from the RBNZ decision to cut its OCR by 25bps to 5.25%. Governor Orr said it was not a difficult decision as the RBNZ is now “confident” about inflation returning to target due to pricing behaviour adjusting to lower inflation and greater spare capacity. Also, a 50bp move was discussed. Future cuts will be data-dependent.

- July labour market data will print tomorrow, with Bloomberg consensus looking for a 20k increase in employment and a stable unemployment rate of 4.1%.

- We see risks to this outlook but not from the cycle but from seasonal patterns. If this occurs, then August is likely to show a rebound.

- The underemployment and youth unemployment rates plus hours worked are additional indicators monitored by the RBA monitors.

- Cash US tsys are flat to 1bp cheaper in today's Asia-Pac session ahead of US CPI data later today.

- Cash ACGBs are 7-9bps richer, with the AU-US 10-year yield differential at +8bps.

- Swap rates are 7-8bps lower.

- The bills strip has bull-flattened, with pricing +1 to +9.

- RBA-dated OIS pricing is 6-9bps softer for 2025 meetings. A cumulative 23bps of easing is priced by year-end.

RBNZ: Rate Cut As Economy Significantly Surprises To The Downside

The market and forecasters were split between a 25bp cut and no change going into today’s RBNZ decision. The RBNZ delivered a 25bp rate cut to 5.25% as it decided to “ease the level of monetary policy restraint” due to greater excess capacity, confidence that inflation will return to the band in Q3:24, downside risks and inflation expectations at the target mid-point. There were large forecast revisions implying that the degree of weakness in the economy had taken the bank by surprise.

- There were significant downward revisions to the OCR path which is now 80bp lower by end-2024, 130bp by end-2025 and 60bp by end-2026 with the terminal rate still 3% in Q2 2027. This profile implies 1-2 cuts by end-2024 and at least 100bp in 2025.

- Governor Orr has previously said that the OCR path is not a target but in the meeting record the MPC “felt that the OCR track in the projection reflected its view on the policy strategy that would best deliver on its remit.” If the economy is as weak as the RBNZ believes, then there could be a 25bp cut at each of the next MPS meetings, but further easing will be “conditional” on inflation expectations remaining anchored and “pricing behaviour” adapting to the “low inflation environment”.

- There were large downward revisions to 2024 GDP growth with a technical recession forecast for Q2/Q3. This has led to a widening of the negative output gap and increase in unemployment rate expectations.

- As a result of greater excess capacity and lower import prices, there was a large downward revision to Q3 2024 CPI to 2.3% from 3.0% in May, close to the band mid-point. It is expected to stay around this rate through 2025 before reaching the 2% mid-point in Q2 2026, which is unchanged.

RBNZ: MPC In Strong Position To Ease “Calmly”

Governor Orr said that today’s 25bp rate cut was not a difficult decision as the RBNZ is now “confident” about inflation returning to target due to pricing behaviour adjusting to lower inflation and greater spare capacity. Also a 50bp move was discussed, but the MPC took the cautious approach and the revised OCR path reflects this. Future cuts will be data dependent.

- The significant change in forecasts was discussed and Orr said this was typical of turning points. The RBNZ had noted risks in both directions in May and that the growth risks had materialised. The possibilities are now more balanced.

- There is now a technical recession forecast for Q2/Q3 and Orr stated that the economy is currently in the “darkest period” and that while Q2 GDP is not yet available, high frequency data showed significant weakness, which is incorporated in the forecast. This data is covered in Box A of the MPS.

- The economy will normalise as inflation and rates come down and this is reflected in the RBNZ’s upward revisions to 2025 GDP.

- The recent government budget was neutral as spending reductions offset tax cuts (see MPS Box B). The RBNZ assumes that around 50% of tax cuts will be spent. Announced electricity price changes are in its CPI forecast and can be seen by the 0.9% q/q forecasts for Q3s from 2025, but the MPC doesn’t see this threatening price stability as inflation expectations are well anchored.

- See MPS here.

NZGBS: Strong Post-RBNZ Rally, 74bps Of Additional Easing By November

NZGBs closed 6-13bps richer on the day, with a steeper 2/10 curve, after the RBNZ cut the OCR 25bps to 5.25%.

- Governor Orr said that today’s 25bp rate cut was not a difficult decision as the RBNZ is now “confident” about inflation returning to target due to pricing behaviour adjusting to lower inflation and greater spare capacity.

- Also, a 50bp move was discussed, but the MPC took the cautious approach, and the revised OCR path reflects this. Future cuts will be data-dependent.

- The significant change in forecasts was discussed and Orr said this was typical of turning points. The RBNZ had noted risks in both directions in May and that the growth risks had materialised. The possibilities are now more balanced.

- Swap rates are 7-13bps lower on the day.

- RBNZ dated OIS pricing is 10-18bps softer across meetings after the RBNZ Decision. The market had attached a 58% chance of a 25bp cut today.

- The market is pricing another 32bps of easing for the October meeting and an additional 74bps by November.

- RBNZ Governor Orr will front of the Parliament Select Committee on MPS tomorrow.

- Tomorrow, the NZ Treasury plans to sell NZ$225mn of the 4.50% Apr-27 bond, NZ$200mn of the 4.25% May-34 bond and NZ$75mn of the 1.75% May-41 bond.

FOREX: NZD Slumps As RBNZ Considered A 50Bp Cut , USD/JPY Dip Supported As PM Kishida Bows Out

Outside of a sharp slump in NZD, post the RBNZ rate cut, aggregate G10 FX moves have been modest so far today. We did see some yen volatility, as PM Kishida announced he won't seek a second term, but net USD/JPY changes have been minimal.

- The RBNZ cut rates by 25bps, which wasn't fully priced by the market. There were significant downward revisions to the OCR path which is now 80bp lower by end-2024, 130bp by end-2025 and 60bp by end-2026 with the terminal rate still 3% in Q2 2027.

- The central bank also expects the economy to be in a recession at the moment, while RBNZ Governor Orr stated the board considered a 50bps cut today.

- NZD/USD initially stabilized in the 0.6030/40 region post the outcome, but fell further when Orr stated a 50bps cut was considered. We hit lows of 0.6006 and track just above this level in recent dealings. We opened today closer to 0.6075. Lows this week rest at 0.5990.

- AUD/USD has been relatively steady, last down slightly to 0.6625. The AUD/NZD cross is back above 1.1000, last near 1.1030, fresh highs back to the start of the month.

- USD/JPY was volatile today, tracking above 147.00 in early dealings, before falling to 146.08 after it was announced PM Kishida would not seek a second term in office. This appeared to pressure Japan equities somewhat, with some fresh uncertainty injected into the political outlook. Still, dips have been supported for both USD/JPY and Japan equities. The pair was last back near 147.00, little changed for the session.

- Looking ahead, all eyes will be on the US CPI print later.

ASIA STOCKS: China & HK Equities Lower As Weak Loan Demand Continues

Chinese & Hong Kong stocks declined after data showed a contraction in bank loans to the real economy, the first in 19 years. The weak demand underscores ongoing sentiment issues following the real estate market decline, and while bond issuance trends are encouraging, further policy rate cuts may be necessary to stimulate demand.

- Hong Kong equities initially opened the session higher, before paring gains. The HSI is down 0.10%, while both property and tech indices are 0.40% lower. China mainland equities are trading slightly worse than their HK peers, with CSI 300 down 0.40% while the growth focused ChiNext Index is off 1%.

- China's stock market turnover dropped to its lowest level in over four years, with combined transactions on the Shanghai and Shenzhen exchanges hitting just 496b yuan. This decline reflects growing pessimism as investors shift focus to government bonds amid a weakening economy and an ongoing housing crisis.

- In the property space, Moody's downgraded China Vanke's debt rating to B1 from Ba3 and further into junk territory due to weakening sales and ongoing margin pressure amid China's property market slump. Despite efforts to secure financing and deleverage, concerns remain about Vanke's financial health, with its dollar bonds trading at significant discounts, reflecting fears of long-term risk.

- Tomorrow, we have China Industrial Production & Retail Sales followed by Hong Kong's GDP on Friday

ASIA PAC STOCKS: Asian Equities Track US Markets Higher

Asian equities are mostly higher today driven by hopes that softer US inflation data will prompt the Fed to start easing rates as early as September. The MSCI Asia Pacific Index advanced, with significant gains in New Zealand and Taiwan, while Japanese stocks fluctuated due to political uncertainty following Prime Minister Fumio Kishida's decision not to seek re-election. Chinese stocks dipped as data showed a contraction in bank loans to the real economy for the first time in 19 years, and investors are keenly awaiting earnings reports from major Chinese tech firms. The RBNZ has cut rates by 25bps, which saw the NZD fall about 1% and OIS soften about 10bps cutting meetings. US equity futures are little changed today, US Tsys yields are about 1bps higher after rallying overnight on soft PPI data, with markets now turning their attention to CPI data tonight.

- Japanese equities opened 1-2% higher this morning, before selling off on the back of news that the Prime Minister would not seek re-election, while the 5yr bond auction showed poor demand metrics, with bid/cover ratio falling to 3.5109 from 4.256 prior. Major benchmarks are trading just below key resistance levels (200-Day EMAs), the Nikkei is 0.12% higher, while the TOPIX is trading 0.75% higher, with banks the top performers.

- South Korean equities are higher today, led by gain overnight in tech stocks, Samsung Electronics (+1.50%), SK hynix (+2.25%) are contributing the most to the KOSPI's gains, while the small-cap focused KOSDAQ is 1.40% higher.

- Taiwan equities, similar to SK equities are higher on strong tech moves overnight, the Philadelphia SE Semiconductor Index was 4.18% higher overnight. The Taiex is 1.10% higher today, with TSMC (+1%) contributing the most to index gains.

- Australian equities are higher today, with healthcare & tech stocks the best performers while energy & materials the worst performers. New Zealand equities have rallied on the back of RBNZ cutting interest rates by 25bps, the board also commentated that they considered cutting 50bps which has seen all sectors jump higher.

- In Asia EM, most markets are trading higher with the USD falling against most Asian currencies. Indonesia's JCI is 0.75% higher, Thailand's SET is 0.50% higher, Singapore's Straits Times is 0.45% higher, Philippine's PSEi is 0.90%, while Malaysia's KLCI & India's Nifty 50 are little changed.

OIL: Prices Recover Somewhat After Data Show US Crude Drawdown, US CPI Later

Oil prices fell on Tuesday but are higher today after industry data showed another US crude inventory drawdown. Risk sentiment is also supportive while the USD is little changed. Brent is up 0.5% to $81.11/bbl following a low of $80.89 but off the high of $81.40. WTI is 0.6% higher at $78.81 after rising to $79.10 and then falling to $78.62.

- Despite downward risks to prices from OPEC reducing its output cuts from October while also revising down its demand outlook, both Citigroup and Goldman Sachs believe that Brent could rise to the mid-$80s, according to Bloomberg.

- Bloomberg reported another large US crude stock drawdown of 5.2mn barrels last week, according to people familiar with the API data. Gasoline fell 3.69mn but distillate rose 612k. The official EIA data is out later today and if it is in line with API, it will be the seventh consecutive weekly decline.

- As well as demand/supply fundamentals, geopolitical uncertainty remains at the fore with an attack by Iran or Hezbollah on Israel expected and Ukraine’s continued incursion into Russian territory.

- Later the focus will be on US July CPI which is forecast to remain at 3% y/y but for core to ease 0.1pp to 3.2% (see MNI CPI Preview). UK July CPI/PPI, euro area Q2 employment/GDP and June IP are also released.

ASIA EQUITY FLOWS: Asian Equity Flows Muted Ahead Of Key US Data

- South Korea: South Korean equities saw a small outflow of $31m yesterday, with an outflow of $696m over the past five trading days. The 5-day average outflow is $139m, compared to the 20-day average outflow of $145m and the 100-day average inflow of $88m. Year-to-date, South Korea has had substantial inflows totaling $16.712b.

- Taiwan: Taiwan recorded an outflow of $147m yesterday, with a net outflow of $914m over the past five trading days. The 5-day average outflow is $183m, compared to the 20-day average outflow of $671m and the 100-day average outflow of $188m. Year-to-date, Taiwan has experienced outflows totaling $11.080b.

- India: Indian equities saw an outflow of $335m Monday, with a net outflow of $1.110b over the past five trading days. The 5-day average outflow is $222m, compared to the 20-day average outflow of $34m and the 100-day average inflow of $24m. Year-to-date, India has seen inflows totaling $1.962b (up to August 12th).

- Indonesia: Indonesian equities recorded an inflow of $31m yesterday, resulting in a net inflow of $169m over the past five trading days. The 5-day average inflow is $34m, compared to the 20-day average inflow of $20m and the 100-day average outflow of $9m. Year-to-date, Indonesia has had inflows totaling $200m.

- Thailand: Thai equities saw an inflow of $5m yesterday, leading to a net inflow of $19m over the past five trading days. The 5-day average inflow is $4m, in line with the 20-day average of $1m, but better than the 100-day average outflow of $24m. Year-to-date, Thailand has experienced outflows amounting to $3.319b.

- Malaysia: Malaysian equities had an inflow of $4m yesterday, resulting in a 5-day net outflow of $103m. The 5-day average outflow is $21m, which is worse than the 20-day average outflow of $7m and the 100-day average outflow of $1m. Year-to-date, Malaysia has experienced outflows totaling $52m.

- Philippines: The Philippines recorded an inflow of $2m yesterday, with a net outflow of $1m over the past five trading days. The 5-day average outflow is $0m, compared to the 20-day average inflow of $1m and the 100-day average outflow of $8m. Year-to-date, the Philippines has seen outflows totaling $495m.

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -31 | -696 | 16712 |

| Taiwan (USDmn) | -147 | -914 | -11080 |

| India (USDmn)* | -335 | -1110 | 1962 |

| Indonesia (USDmn) | 31 | 169 | 200 |

| Thailand (USDmn) | 5 | 19 | -3319 |

| Malaysia (USDmn) | 4 | -103 | -52 |

| Philippines (USDmn) | 2 | -1 | -495 |

| Total | -471 | -2637 | 3929 |

| * Up to Date 12-Aug-24 |

GOLD: Steady Ahead Of US CPI Data

Gold is slightly lower in today’s Asia-Pac session, after closing 0.3% lower at $2465.16 on Tuesday.

- Bullion’s relative stability came despite a strong rally in US Treasuries following lower-than-expected PPI data. The front end paced the gains in a bull-steepener, with the 2-year yield declining 9bps to 3.93%, the lowest since last Monday. The 10-year yield fell 6bps to 3.84%.

- PPI final demand was softer than expected in July at 0.10% m/m (cons 0.2%). Within the components that feed into PCE calculations, hospital inpatient services offer the greatest moderation on the month as inflation slowed from 0.41% to 0.16% m/m. It was however partly offset by portfolio management fees rising 2.3% m/m after 0.6% in June.

- Fed Bostic said interest rates will fall by the end of the year if the economy performs as he expects.

- US CPI is due for release later today, with the market hoping for more clues on the Federal Reserve’s interest rate path.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- According to MNI’s technicals team, attention is on $2483.7, the Jul 17 high and a bull trigger. Clearance of this hurdle would resume the uptrend.

IRON ORE: To Fresh Multi Month Lows Amid Onshore Steel Headwinds

The active SGX iron ore contract is tracking to fresh multi month lows in Wednesday trade. We were last near $96/ton. Early April lows came in close to $93.50/ton in terms of potential downside targets.

- Sentiment is being weighed by broader concerns around the steel outlook in China. The Chairman of China Baowu Steel Group (the world's largest producer) warned that the steel industry faced a severe industry crisis (see this BBG link).

- This likely reflects broader economic headwinds for China, particularly in the property sector. Yesterday's July credit figures also painted a fairly bleak picture in terms of consumer and business loan demand. Onshore China equities are mostly weaker today as well, bucking the positive trend seen elsewhere in the region.

- Steel related futures are down around 2.5% in onshore China trade today. Rebar futures are at fresh cycle lows.

ASIA FX: Supported By Lower US Yields, Firmer Equities, IDR Outperforms, CNH& PHP lag

USD/Asia pairs are mostly lower, albeit to varying degrees. Sentiment has been supported by positive regional equity sentiment, although China equities have been a noticeable laggard. IDR spot has rallied close to 1%, while those currencies exposed to tech related equities (KRW & TWD) have also risen. USD/PHP has seen support sub 57.00 ahead of tomorrow's BSP outcome.

- USD/CNH is sub 7.1500 but has seen limited ranges overall. The USD/CNY fixing was set lower than yesterday's outcome, although markets expected such an outcome. Onshore equities have struggled though, amid on-going growth concerns following yesterday's poor July credit data. Onshore bond yields have turned lower after sharp gains in recent sessions.

- Spot USD/KRW has tested sub 1360, but hasn't seen any follow through, the pair last near 1361, which is still 0.40% stronger in won terms for the session. The lower than expected unemployment rate data from earlier should see easing odds for next week trimmed. On the equity front, the Kospi sits 0.70% higher, off session best levels.

- Spot USD/TWD is down to sub 32.30, as local equities have gained more than 1% today. This is fresh lows for the pair back to early June, as the TWD rebound continues.

- IDR gains were in excess of 1% at one stage before we stabilized somewhat. USD/IDR was last near 15685. This is fresh lows in the pair back to March this level. This likely reflects both the lower US yield backdrop and better global equity tone. This month has seen better net bond inflow momentum from offshore investors. We have the budget outlook still to come this week.

- USD/PHP is back above 57.00, slightly weaker in PHP terms. Tomorrow's BSP meeting is seen as a close call around whether the central bank will commence its easing cycle.

- Both MYR and THB are up around 0.40/0.505 at this stage.

CHINA RATES: Bond Wrap

- Following several days of higher yields, the bond market grabbed hold of the drop in aggregate financing and rallied hard throughout the day.

- The focus level for authorities of 2.20% in the 10 Yr was breached with ease today as bonds across the curve rallied 1-5bps

- Suggestions that market traders are finding ways to circumvent the crack down on government bond trading show the demand for bonds remains.

- Tomorrow sees significant data releases with both retail sales and industrial production providing further insight into the pace of slowdown in China.

2yr 1.592% (-1bp) 5yr 1.85% (-1.5bp) 10yr 2.16% (-4.5bp) 30yr 2.35% (-1.5bp)

PHILIPPINES: MNI BSP Preview - August 2024: A Close Call, But Mixed Data Points To No Change

- On balance, the economic data presents a mixed picture for the economy and as such many economists are calling for the BSP to cut rates at tomorrow’s decision. This is a line call at best and a difficult one for the BSP ahead of the Federal Reserve’s decision on interest rates next month and the recent period of extreme market volatility.

- Historically, Central Bank’s in Asia have tended to remain on hold ahead of the FED and for that reason, we remain surprised by survey’s suggesting a cut tomorrow, but acknowledge it is a close call.

- Click to view the full preview here:

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/08/2024 | 0600/0700 | *** |  | UK | Consumer inflation report |

| 14/08/2024 | 0600/0700 | *** | | UK | Producer Prices |

| 14/08/2024 | 0600/0800 | *** |  | SE | Inflation Report |

| 14/08/2024 | 0645/0845 | *** |  | FR | HICP (f) |

| 14/08/2024 | 0900/1100 | ** |  | EU | Industrial Production |

| 14/08/2024 | 0900/1100 | *** | | EU | GDP (p) |

| 14/08/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 14/08/2024 | 1230/0830 | *** | | US | CPI |

| 14/08/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.