Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- AUD/USD is up ~0.5% printing at $0.6680. Resistance is seen at $0.6818 10 May high. NAB has returned to its February call that rates will peak at 4.1% in August or possibly July. ACGBs are weaker (YM -8.0 & XM -7.5), near session cheaps, with these moves aided by the US Tsy sell-off from Friday.

- Yen is weaker, last back at 136.15, despite an indifferent equity lead for much of the session and higher than expected PPI data locally. Oil prices continued to drift lower.

- Regional equity sentiment has improved as the session progressed, particularly in HK and China, which has taken CNH and KRW away from their respective lows for today. The THB has outperformed in SEA FX on optimism around the economic outlook, following Sunday's election result.

- In Europe today we have German Whole Prices and Eurozone Industrial Production, further out US Empire Manufacturing crosses.

MARKETS

US TSYS: Little Changed In Muted Asian Session

TYM3 deals at 115-13+, -0-00+, with a 0-04 range observed on volume of ~44k.

- Cash tsys sit little changed across the major benchmarks.

- Tsys have observed narrow ranges with little follow through on moves in Monday's Asian session.

- A recovery off session lows in e-minis, and mild pressure on the USD helped tsys firm off early lows. A fall in WTI futures also added a layer of support.

- Little meaningful macro news flow crossed.

- A meeting between President Joe Biden and Congressional leaders to discuss the US debt ceiling has been set for Tuesday.

- In Europe today we have German Whole Prices and Eurozone Industrial Production, further out US Empire Manufacturing is on the wires. Fedspeak from Atlanta Fed President Bostic, Chicago Fed President Goolsbee and Minneapolis Fed President Kashkari will cross.

JGBS: Futures Sitting Weaker, Near Cheaps After PPI Beat

JGB futures sit near Tokyo session cheaps in afternoon trading, -24 versus settlement levels.

- Higher-than-expected April PPI, which came ahead of monthly CPI data later in the week, appears to have assisted today’s relatively weak performance.

- 5-year supply saw relatively smooth digestion with the low price coming in line with dealer expectations, although the cover ratio did decline, and the tail increased since last month's auction.

- Cash JGBs are 0.3-1.2bp weaker across the curve, except for the 2-year zone, with the curve steeper. The benchmark 10-year yield is 1.2bp higher at 0.402%, below the BoJ's YCC limit of 0.50%. The 5-year benchmark is 0.4bp cheaper at 0.111%, little changed from levels prevailing before the JGB supply.

- The swap curve bear steepens with swap spreads wider outside of the 1-year zone.

- The local calendar is light tomorrow ahead of Q1 GDP (preliminary) on Wednesday and National CPI on Friday.

- BoJ Rinban operations covering 1-10-year and 25-Year+ JGBs are scheduled for tomorrow ahead of 20-year JGB supply on Wednesday.

- Further afield, the global calendar is light ahead of tomorrow’s data dump in China, the Euro Area's Q1 GDP and US Retail Sales.

AUSSIA BONDS: Weaker, At Cheaps, RBA Minutes Tomorrow

ACGBs are weaker (YM -8.0 & XM -7.5), near session cheaps, after trading in a relatively narrow range for the Sydney session. Without meaningful economic data or headlines, the local market has traded in sympathy with US tsys, ahead of a heavy domestic calendar. US tsys are little changed in Asia-Pac trade, holding near cheaps seen in the NY session ahead of the weekend.

- Cash ACGBs are 7-8bp cheaper with the AU-US 10-year yield differential unchanged at -7bp.

- Swap rates are 7-8bp higher with the 3s10s curve flatter.

- The bills strip has bear steepened with pricing -5 to -11.

- RBA dated OIS are 2-9bp firmer across meetings with late ‘23/early ’24 leading. A 16% chance of a 25bp hike is priced for June. the expected terminal rate has moved back to 3.96%, just shy of the post-May hike high of 3.97%. The move higher in terminal rate expectations has been assisted by a firming in US STIR, which troughed ahead April non-farm payrolls.

- The local calendar heats up tomorrow with the release of RBA Minutes for May, ahead of Q1 Wage Price Index (Wed) and the April Employment (Thu).

- Further afield, the global calendar is light ahead of tomorrow’s data dump in China, the Euro Area's Q1 GDP and US Retail Sales.

NZGBS: Cheaper, Tight Range, Budget on Thursday

NZGBs closed 3-4bp, near session cheaps, after trading in a relatively tight range. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined announcement of the NZ$1 billion flood and cyclone recovery package. Accordingly, local participants appeared content to be on headlines and US tsys watch throughout today’s session.

- Swap rates closed 2-3bp higher with the 2s10s curve flatter, and the implied long-end swap spread tighter.

- RBNZ dated OIS closed 1-5bp firmer out to Feb’24 with 22bp of tightening priced for the upcoming May 24 meeting.

- The PSI index fell from a revised 53.8 in March to 49.8 in April. The current level is below the long-term average of 53.6 for the first time since December.

- The local calendar is light ahead of the Budget on Thursday.

- Before then, the local market is likely to eye the release of Australia's of the RBA Minutes for May tomorrow, Q1 Wage Price Index on Wednesday, and the April Employment Report on Thursday.

- Further afield, the global calendar is light ahead of tomorrow’s data dump in China, the Euro Area's Q1 GDP (2nd estimate) and US Retail Sales.

FOREX: Antipodeans Firmer, Yen Pressured In Asia

AUD and NZD are the strongest performers in the G-10 space at the margins today, both are ~0.2% higher on Monday. The Yen is pressured, USD/JPY has printed its highest level since May 3.

- AUD/USD is now up ~0.2% printing at $0.6660/65. Resistance is seen at $0.6818 10 May high. NAB has returned to its February call that rates will peak at 4.1% in August or possibly July.

- Kiwi is also 0.2% firmer, benefitting from spillover in the AUD as well as improved risk sentiment as e-minis tick off session lows to sit unchanged from Fridays closing levels.

- Yen is pressured, USD/JPY prints at ¥136.10/20 this is the highest level in the pair since May 3rd, bulls target high from May 3 at ¥136.63. Apr PPI was marginally firmer than expected, printing at 0.2% M/M above the expected 0.0%.

- Elsewhere in G-10 EUR is 0.1% however ranges have been narrow thus far.

- Cross asset wise; e-minis are flat however the contract was down ~0.3% in early dealing. BBDXY is little changed as are US Treasury Yields.

- In Europe today we have German Whole Prices and Eurozone Industrial Production, further out US Empire Manufacturing crosses.

EQUITIES: Japan Still Outperforming, While China Shares Struggle

Most regional equity markets are tracking lower, although Japan markets remain a standout performer. The HSI is positive, but only modestly higher, while China mainland shares remain under pressure. US equity futures have mostly been in the red, but have recovered this afternoon from earlier lows. Eminis last near 4138.5, almost unchanged for the session.

- China shares continue to track lower, the CSI down 0.24% at this stage, while the Shanghai Composite Index is down nearly 1%. The CSI 300 is very close to multi-month lows. The on-hold MLF decision may have disappointed some in the market, while China's clamp down on data security may also be weighing on the outlook.

- The HSI is a touch higher, last +0.14%, while the Tech sub-index is down slightly. We did see a pull back in the China Dragon index during Friday trade in the US.

- Japan stocks are showing more positive momentum, the Topix around +0.85% firmer at this stage. Weaker yen levels (with JPY back to 136.15/20) are helping at the margin, while positive carry over from corporate earnings results is the other positive.

- The Kospi and Taeix are both down modestly, while the ASX isn't too far away from flat.

- The SET, in Thailand, couldn't sustain early positive momentum post Sunday's election results, with the opposition parties outperforming those aligned with the military. The SET was last -0.80%.

OIL: Crude Weaker Again Today, Tuesday Contains Key Events

Oil is down around 0.8% during APAC trading after falling 1.1% on Friday, as the market remained nervous regarding US debt ceiling negotiations and China’s lacklustre recovery. It is now down over 5% since the May 9 close. Brent is now around $73.58/bbl while WTI is under $70 at $69.50. The USD index is flat so far today.

- Brent and WTI remain above support levels of $71.28 and $68.43 respectively.

- Key events for crude this week include a swathe of data relating to China’s domestic economy and the IEA monthly outlook both released on Tuesday, as the demand outlook has been a key concern for oil markets. There is also US API inventory data on the supply side.

- Later today the European Commission releases updated economic forecasts. There is also March euro area IP data and the US New York Empire manufacturing index for May.

GOLD: Slightly Stronger In Asia-Pac, Showing Relative Resilience

In early Asia-Pacific trading, gold has firmed $3.29 (+0.16%) to 2014.02, continuing the relative resilience it displayed in trading ahead of the weekend. Gold declined a modest 0.2% to 2010.77 despite an increase in US tsy yields and a second day of dollar strength.

- MNI's technical team reports that gold is still on an uptrend, marked by a series of higher highs and higher lows. Moving average studies are also indicating a bullish setup. Investors are closely monitoring the March 8 high of $2070.4, which is the immediate target before the all-time high of $2075.5. Meanwhile, the key support level remains at $1969.3, which was the low point recorded on April 19th.

- Gold prices have remained above $2000 for the month of May, as investors anticipate the end of the Federal Reserve's tightening cycle. Concerns about the impasse over the US debt ceiling have also contributed to bullish market sentiment.

- Gold could reach $US2100 per ounce by December as US banking woes, high interest rates and uncertainty around the debt ceiling dampen the global economic outlook and boost safe-haven demand, ANZ economists predict.

ASIA FX: CNH & KRW Move Off Session Lows, THB Outperforms

USD/Asia pairs have been mixed. A recovery in equity sentiment has helped CNH and KRW move away from session lows. THB has outperformed post Sunday's election result, while PHP and IDR have been laggards. Still to come today is Indian wholesale prices and trade balance, both for Apr. The focus tomorrow will largely rest on April activity figures in China.

- USD/CNH got to fresh highs of 6.9750, but has stabilized this afternoon, as onshore equities have improved. The pair was last at 6.9660/70. Equities have recovered from steeper losses in the first part of the session. As expected, the 1yr MLF rate was left unchanged at 2.75%, while the USD/CNY fixing was neutral.

- 1 month USD/KRW has moved lower this afternoon, last near 1333. Some positive carry over from higher AUD and NZD levels has helped, while a recovering equity backdrop has also been positive. This is comfortably away from Friday session highs above 1340 for the pair.

- USD/THB was down sharply in the first part of trade, post Sunday's election outcome. The pair last tracked in the 33.70/75 region, around 0.80% firmer in baht terms versus Friday's closing levels. This is all the more impressive given broad USD gains through Friday's session. We have since stabilised somewhat, last near 33.77. Local equities are weaker, -0.65%. Still, there is hope that a new government can be formed with a pro-growth agenda.

- USD/PHP sits just above 55.95 currently, down slightly from session highs above 55.99. The main focus has been on earlier comments from BSP Governor Medalla that the central bank may keep rates unchanged at the May 18 meeting (this Thursday). Finance Secretary who also sits on the BSP board stated he would vote for a pause at this week's meeting. For USD/PHP, the pair hasn't been to sustain gains above 56.00 recently. Note the 200-day MA is at 56.10.

- USD/IDR has pressed higher today, but this is line with the USD gains post the onshore close from Friday. We were last at 14820, around +0.50% above Friday closing levels.. The 1 month NDF is slightly lower versus NY closing levels though, last 14835/40. We are at fresh highs for the month though in terms of USD/IDR spot. Late April highs in the pair came in around 14930/35. Still elevated US real yields and weaker commodity prices continue to weigh on IDR. Palm oil prices are only a touch above recent lows.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing today. The measure ticked lower late last week after printing its highest level since mid March. We now sit ~0.9% below the top of the band. USD/SGD firmed today printing its highest level 21 March this morning and last prints at $1.3390/1.3400. The pair has continued to tick away from its 20-Day EMA ($1.3321) after breaking above the measure last week, Bulls look to target high from March 10 at $1.3576. Bears first target the low from 14 April at $1.3204.

THAILAND ELECTION: Move Forward Wins Election, Leader Begun Coalition Talks

The Election Commission has announced that Move Forward has won the election with a total of 151 seats, although the final results won’t be published for another 5 days. Move Forward’s leader Pita has said that he is ready to take over as premier and has already spoken to Pheu Thai’s Paetongtarn and has approached 8 parties. He currently has 309 parliamentarians in his coalition but another 77 are needed to avoid the need for support from the military-aligned senate for the coalition’s preferred PM.

- Pita said that he wants to form a government as soon as possible, which if he achieves would take away the uncertainty of weeks of negotiations. A panel will be created for coalition talks. He also stated that the days of military coups in Thailand are over. But he will push for changes to the laws against insulting the monarchy.

- Pheu Thai was in second place with 141 seats, Bhumjaithai on 71, pro-military PPRP 40, UTN 36 and the Democrats 25. Smaller parties gained 28 seats.

- Turnout was a record 75.22% up from 2011’s 75.03%.

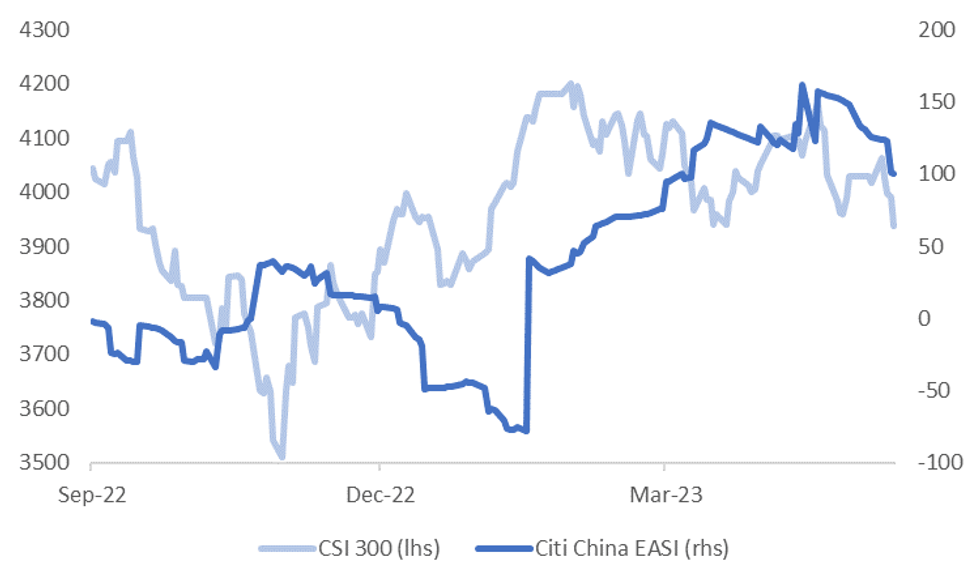

CHINA DATA: Apr Activity Figures To Show Strong Y/Y Improvement, But Recovery Momentum Has Eased

A reminder that we get April activity figures tomorrow, with IP, retail sales, fixed asset investment, property sales the jobless rate all due. Favorable base effects from last year (when Shanghai was in lockdown) should ensure better y/y outcomes, but the market will be focus on momentum from March and any significant surprises relative to expectations. The chart below shows Citi's China EASI has rolled off recent highs, ending a run of generally positive data surprises. This has weighed on China's recovery theme and related asset performance (albeit not the only driver).

- IP is forecast at 10.9% y/y (prior was 3.9%, forecast range is 3.5% to 12.6%).

- Retail sales is forecast at 21.9% y/y (prior 10.6%, forecast range is 11.0% to 35.0%)

- Fixed asset investment is projected at 5.7% ytd y/y (prior 5.1%, forecast range is 5.0 to 6.7%)

- Property investment is projected at -5.7% ytd y/y (prior -5.8%, forecast range is -4.2 to -7.0%)

- Property sales are also due, no expectation is given via Bloomberg, the prior print was 7.1% ytd y/y.

- The jobless rate is projected to remain steady at 5.3% (prior was 5.3%).

Fig 1: CSI 300 Versus Citi China EASI

Source: Citi/MNI - Market News/Bloomberg

THAILAND DATA: Stronger Growth & Upside Inflation Risks Make May Rate Hike Likely

Thai Q1 GDP came in stronger than expected at 1.9% q/q and 2.7% y/y after falling 1.5% q/q in Q4. Growth was supported by net exports driven by tourism which boosted services exports. The government expects 2023 GDP growth to be between 2.7% and 3.7%, while the BoT said that the economic recovery is in line with expectations but dependent on China’s recovery. The tourism forecast is unchanged. Given the better Q1 GDP result and continued concern over upside risks to inflation, the BoT is likely to hike again at its May 31 meeting.

- Net exports contributed 1.3pp to quarterly growth and 2.8pp to annual, seasonally adjusted. Exports of goods & services rose 4.5% q/q and 2.9% y/y whereas imports grew 2.6% and fell 1.1%. Services exports are up 87.8% y/y due to the tourism recovery.

- Private consumption eased slightly to 5.4% y/y after 5.6% in Q4, but remains solid. Investment growth was lower at 3.1% y/y from 3.9%.

- Government expenditure fell 6.2% y/y after -7.1% and the government’s NESDC said following the data that public investment is likely to slow in Q4 2023 due to the expected delay in the budget to Q1 2024 because of the election. It also noted that this delay plus political uncertainty was a downside risk to Thai growth.

Source: MNI - Market News/Refinitiv

Source: MNI - Market News/Refinitiv

INDONESIA DATA: Trade Surplus Widens As Imports Weaken Sharply

The April trade surplus widened more than expected to $3.94bn from $2.83bn the previous month and is elevated historically. While both exports and imports were weaker than forecast, the downturn in imports was sharper due to capital goods imports plummeting. The data is unlikely to have any implications for the May 25 meeting as the BI was expecting a solid trade position this year.

- Imports fell 22.3% y/y down from -6.3% and exports fell 29.4% y/y down from -11.6%, driven by lower commodity prices.

- Exports to China fell 15.9% y/y, -37.7% to Japan and -35.9% to the US. Indonesia runs a surplus with each of those economies.

- Oil & gas exports fell 12.2% y/y driven by lower prices but gas was only down 6.2%.

Source: MNI - Market News/Refinitiv/Bloomberg

SOUTH KOREA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of South Korean Newspapers and some other major news outlets from the past day or so.

Inflation: S. Korea to hike Q2 electricity, gas rates by 5.3 pct on high costs, losses (link)

Economy: Exporters Pessimistic About Shipments to China (link)

South Korea/Japan: Samsung to invest $221 mn to build R&D chip line in Japan: Nikkei (link)

South Korea/India: Hyundai to invest $2.45 bn in India, eyes spot in global EV top 3 (link)

Geopolitics: Yoon to meet with Biden, Kishida on margins of G-7 summit (link)

Geopolitics: North Korea slams U.S. for being behind Japan's military 'collusion' with NATO (link)

Geopolitics: China suspected of hampering Busan's World Expo bid (link)

Fiscal: Fiscal Deficit Reaches W54 Trillion in Q1 (link)

Tech: Samsung’s Jay Y. Lee, Tesla’s Elon Musk discuss tech alliance (link)

Shipping: Container freight rates for major destinations fall on-month in April (link)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/05/2023 | 0600/0800 | *** |  | SE | Inflation report |

| 15/05/2023 | 0900/1100 | ** |  | EU | Industrial Production |

| 15/05/2023 | - | | EU | ECB Lagarde & Panetta in Eurogroup Meeting | |

| 15/05/2023 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 15/05/2023 | 1230/0830 | ** | | CA | Wholesale Trade |

| 15/05/2023 | 1230/0830 | ** |  | US | Empire State Manufacturing Survey |

| 15/05/2023 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 15/05/2023 | 1315/0915 | | US | Minneapolis Fed's Neel Kashkari | |

| 15/05/2023 | 1400/1000 | | CA | BOC Financial System Survey report | |

| 15/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 15/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 15/05/2023 | 1600/1700 |  | UK | BOE Pill Monetary Policy Report Q&A | |

| 15/05/2023 | 2000/1600 | ** | | US | TICS |

| 15/05/2023 | 2100/1700 | | US | Fed Governor Lisa Cook Fed Governor Lisa Cook |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.