Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

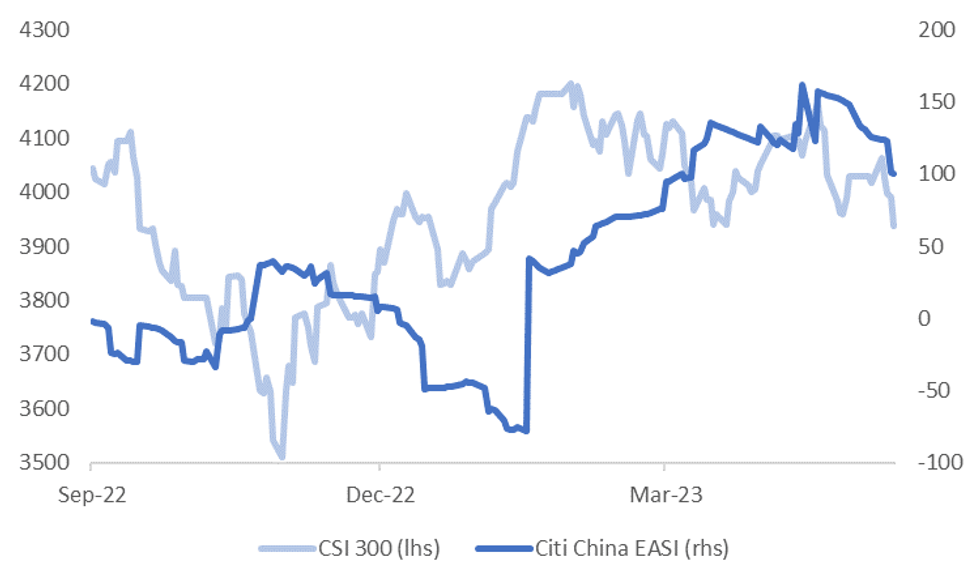

A reminder that we get April activity figures tomorrow, with IP, retail sales, fixed asset investment, property sales the jobless rate all due. Favorable base effects from last year (when Shanghai was in lockdown) should ensure better y/y outcomes, but the market will be focus on momentum from March and any significant surprises relative to expectations. The chart below shows Citi's China EASI has rolled off recent highs, ending a run of generally positive data surprises. This has weighed on China's recovery theme and related asset performance (albeit not the only driver).

- IP is forecast at 10.9% y/y (prior was 3.9%, forecast range is 3.5% to 12.6%).

- Retail sales is forecast at 21.9% y/y (prior 10.6%, forecast range is 11.0% to 35.0%)

- Fixed asset investment is projected at 5.7% ytd y/y (prior 5.1%, forecast range is 5.0 to 6.7%)

- Property investment is projected at -5.7% ytd y/y (prior -5.8%, forecast range is -4.2 to -7.0%)

- Property sales are also due, no expectation is given via Bloomberg, the prior print was 7.1% ytd y/y.

- The jobless rate is projected to remain steady at 5.3% (prior was 5.3%).

Fig 1: CSI 300 Versus Citi China EASI

Source: Citi/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok