Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

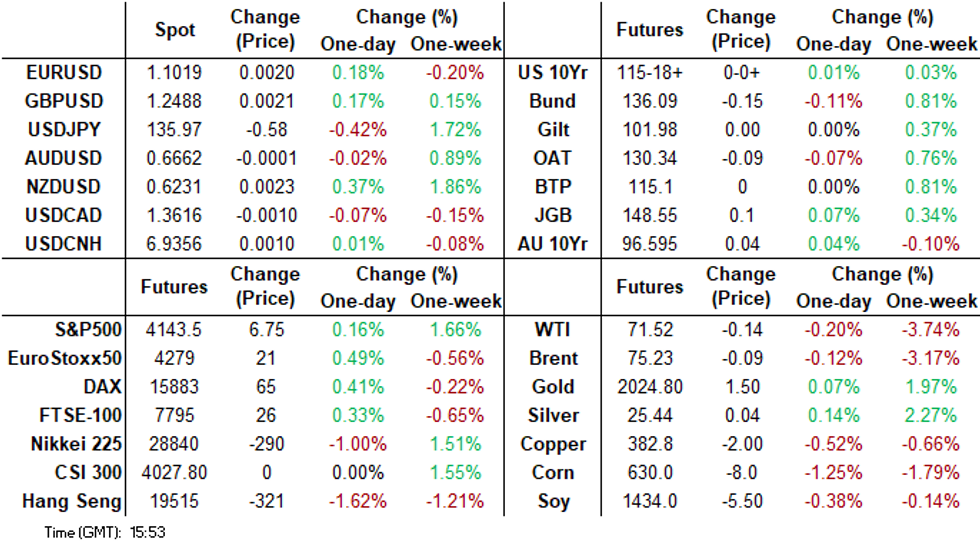

- The USD has lost further ground today, albeit in holiday impacted markets (with both China and Japan missing today). This looks to be a continuation of late NY moves from the Tuesday session. JPY and NZD have been the strongest performers, with the Kiwi aided by solid Q1 employment growth figures. Most USD/Asia pairs are also lower. AUD/USD has underperformed despite a retail sales beat.

- Regional equities have mostly tracked lower, in line with US weakness in the banking space from Tuesday's session. Elsewhere, oil has failed to take back any of its losses in the APAC session today as it treads water ahead of the Fed decision later. It fell over 5% on Tuesday and today it has been trading sideways.

- Looking ahead, the latest FOMC rate decision and Fed Chair Powells press conference provide today's highlights. There is also a slew of US data including ADP Employment, Services PMI and ISM Services.

MARKETS

US TSYS: Narrow Ranges In Futures, Cash Closed Until London, FOMC On Tap

TYM3 deals at 115-18+, +0-00+, with a narrow 0-03+ range observed on volume of ~29k.

- Cash tsys were closed due to the observance of a national holiday in Japan and will re-open in the London session.

- The space looked through the New Zealand Q1 employment report, which showed that the labour market remains very tight and isn’t easing, and firmer than forecast Retail Sales from Australia.

- Ranges in TY remained narrow with little follow through on moves.

- FOMC dated OIS price a 22bp hike for today's meeting with a terminal rate of 5.05% in May. There are ~60bps of cuts priced for 2023. The MNI preview of the event is here.

- The FOMC rate decision and Fed Chair Powells press conference provide the highlight today. Before the decision crosses we have ADP Employment, final read of Services PMI and latest ISM Services survey.

AUSSIE BONDS: Richer, Well Off Session Bests Ahead of FOMC Decision

ACGBs sit richer (YM +5.0 & XM +3.5) but off session bests as the local market mulls the RBA’s surprise 25bp hike yesterday, RBA Governor Lowe’s hawkish speech after market and stronger than expected retail sales. However, it's worth noting that liquidity was likely affected today due to cash tsys being closed until the London session, as Japan is observing a national holiday.

- RBA Kohler in her address to CEDA, text released on the RBA website, noted that Australia’s faster-than-expected population growth could have “unanticipated or more pervasive effects” on the economy. The market nudged a little lower on the release.

- Cash ACGBs are 4-6bp richer with the 3/10 curve 2bp steeper. The AU-US 10-year yield differential is +6bp at -1bp, after being -18bp ahead of the RBA decision.

- Swap rates are 3-5bp lower with EFPs 1bp wider.

- The bills strip is flatter with pricing +3 to +8.

- RBA dated OIS has softened by 2-8 basis points across meetings out to Feb'24, partially offsetting the firming yesterday. The market attaches a 14% chance of a 25bp rate hike at the RBA's June meeting, with a cumulative tightening of 10bp expected by August.

- The local calendar is slated to release March trade data tomorrow.

- Ahead of that, all eyes will turn to the FOMC decision later today.

AUSSIE SWAPS: 1y1y Vs. 2y1y - A Better Way To Play End Of RBA Tightening Cycle

Ahead of the April RBA Policy Meeting, we flagged the possibility for the 1-year swap Vs. 1-year swap rate 1 year forward (1y1y) to steepen if the RBA paused.

- Normally, the 1y Vs. 1y1y flattens into the last rate hike of the cycle and then steepens when the RBA pauses as the market shifts to expecting near-term rate cuts. However, these easing expectations often turn out to be premature, leading to a period of volatility for the 1y versus 1y1y until clearer signs of an RBA easing bias emerge.

- Since early April, the 1y versus 1y1y has followed this pattern precisely. In fact, the 1y versus 1y1y inverted to a new cycle low following the RBA's surprising 25bp rate hike yesterday.

- Given the likelihood of volatility for the 1y versus 1y1y rate around the end of the tightening cycle, we continue to suggest a 1y1y versus 2y1y steepener as a better play for when the RBA eventually shifts to an easing bias. Although this approach may offer less upside, it tends to be far less volatile.

- With the market currently pricing in 25bp of easing by April’24, a more favourable entry level for a 1y1y versus 2y1y steepener (currently around -25bp) could present itself, especially considering the RBA's explicit tightening bias.

Figure 1: Terminal Rate Expectations (%) & 1y1y Vs. 2y1y (%)

Source: Bloomberg / MNI - Market News

Australia: Spending Holding Up But Q1 Volumes Probably Fell

Retail sales surprised to the upside in March rising 0.4% m/m after 0.2% the previous month. Sales moderated to 5.4% y/y from 6.4% due to Covid-related base effects. Sales levels are in line with October last year and 17.9% above pre-pandemic results. The April RBA meeting statement noted continued uncertainties around the outlook for consumption.

- Q1 nominal sales were flat on the quarter to be up 6.4% y/y after 0.9% and 9.3% in Q4, implying that retail volumes contracted in the quarter. Retail sales volumes for Q1 are released on May 9.

- The ABS notes that the pull back in discretionary spending due to higher rates and cost of living has resulted in sales levels being steady for around the last 6 months. The increase in retail spending in March was driven by a 1% m/m rise in food retailing and 1.5% in restaurants & takeaway, boosted by higher food prices (the series are nominal). The other components fell with clothing & footwear down 1%.

- The ABS also said “Businesses in cafes, restaurants and takeaway food services are passing on their rising costs to consumers through price rises, while also benefitting from strong demand driven by the continued return of large-scale cultural and sporting events.”

- Today large consumer electronics retailer JB Hi-Fi said today that its sales growth is starting “to moderate” from elevated levels and that Q1 sales fell 0.1% q/q but remain well above pre-pandemic outcomes, as reported by The Australian.

Source: MNI - Market News/ABS

NZGBS: Twist Flattened After Strong Employment Data

NZGBs closed with the cash 2/10 curve twist flattening with the 2-year benchmark ending 5bp weaker, at the session’s cheap, and the 10-year 2bp richer. The local market opened grappling with the dual influences of post-RBA weakness in ACGBs and overnight strength in US tsys following softer data and US regional banks concerns. The local market was initially richer but weakened following the release of strong employment data.

- Q1 labour market data showed that the labour market remained very tight. Employment rose a stronger than expected 0.8% Q/Q to be +2.4% Y/Y after +0.5% and 1.6% in Q4. Unemployment held steady at a 3.4% rate versus expectations of 3.5%. Private sector wages undershot expectations of +1.1% Q/Q with a print of +0.9%.

- Swap rates closed 3bp higher to 4bp lower with the 2s10s curve twist flattening and implied swap spreads narrower.

- RBNZ dated OIS closed 4-7bp firmer across meetings.

- Building consents are slated for release tomorrow.

- All eyes will now turn to the FOMC decision later today with BBG consensus expecting a 25bp increase to 5.25%.

- The NZ Treasury announced that they plan to sell NZ$200mn of the May-26 bond, NZ$150mn of the May-32 bond and NZ$50mn of the May-41 bond tomorrow.

New Zealand: Strong Jobs And Wages Line Up Another Rate Hike In May

The Q1 labour data showed that the labour market remains very tight and isn’t easing and is generally likely to be a concern to the RBNZ. This information is likely to drive another hike on May 24.

- Employment rose a stronger-than-expect 0.8% q/q to be up 2.4% y/y after 0.5% q/q and 1.6% y/y in Q4 (revised up from 0.1% q/q). Job growth in NZ remains strong despite capacity constraints but a 0.3pp jump in the participation rate to 72% signals some improvement in the supply of labour. Despite the rise in participation, job growth was enough to keep the unemployment rate steady at 3.4%, only 0.2pp above the Q1 2022 trough even with 500bp of tightening.

- Hours worked fell 0.3% q/q, because “bad weather” as a reason for absences or working fewer hours rose to a series high. Stats NZ notes that the actual number may have been higher as the cyclones also impacted data collection in Q1.

- The underutilisation rate fell 0.3pp to 9%, near a record low. Full-time employment rose 0.6% q/q and 2.5% y/y and part-time was also higher up 0.4% and 2.4%, the highest since Q4 2021.

- Even though Q1 private wages rose less than expected in Q4 (+0.9% q/q), earnings growth remains elevated in NZ and is likely to remain a concern for the RBNZ. The labour cost index rose 4.3% y/y up from 4.1% and is the highest since the series began in 1992. Stats NZ said “This aligns with other wage measures, like the unadjusted LCI and average hourly earnings, both of which also had the largest annual increases on record.”

- Public sector salary & wages rose 1.3% q/q and private +0.9%. The largest contribution to wage inflation came from healthcare & social assistance, as a new agreement came into effect in Q1.

- Average ordinary time earnings (ex overtime) rose 7.6% y/y up from 7.2%, also a series high.

Source: MNI - Market News/Refinitiv

NZ wages y/y%

Source: MNI - Market News/Refinitiv

FOREX: USD Pressured In Asia, NZD Outperforms After Employment Data

The kiwi is the strongest performer in the G-10 space at the margins on Wednesday, Q1 labour data showed that the labour market remains very tight and isn’t easing. The greenback is pressured as moves seen in the NY session on Tuesday extended through todays Asian session.

- NZD/USD prints at $0.6235/40, the pair is up ~0.5% today. The 200-Day EMA provided resistance as bulls were unable to break through $0.6249.

- AUD/NZD is pressured, down ~0.4% and is dealing below the $1.07 handle. Bears target year to date lows at $1.0588.

- Yen is firmer, USD/JPY has extended losses through Tuesdays lows and deals a touch above the ¥136 handle after breaching support at ¥136.14 low from 1 May. Bears now target ¥135.13 high from Apr 19 and recent breakout level.

- Elsewhere in G-10 EUR and GBP are both ~0.2% firmer, BBDXY is ~0.2% lower.

- Cross asset wise; e-minis are marginally firmer and 10 Year Us Treasury futures are little changed in Asia.

- The latest FOMC rate decision and Fed Chair Powells press conference provide today's highlights. There is also a slew of US data including ADP Employment, Services PMI and ISM Services.

EQUITIES: Negative Spillover From US Losses Hits Asia Pac Markets

Asia equity markets are down across the board today, following the negative lead from Wall St on Tuesday. Fresh banking concerns have weighed on financial related plays today, although China markets are still closed, while Japan is off for the rest of the week, which has likely dampened liquidity to some extent. US equity futures have crept higher this afternoon, albeit just back into positive territory. This hasn't impacted sentiment much, as the market awaits the Fed decision later.

- The HSI is down 1.75% at this stage. The tech sub index was off by nearly 3% at one stage. Losses have been fairly broad based though. Note the China Golden Dragon Index lost 3.63% in Tuesday US trade. The HS China Enterprises Index is down by 1.91% at this stage.

- In Australia, the S&P200 is off by 1.40%, as local bank stocks are hit from negative US spillover. NZ markets are also off by more than 1%, not buoyed by resilient Q1 employment figures.

- The Kospi is down by over 1.00%, the Kosdaq 1.40%, while the Taeix has fared slightly better, down by 0.50% at this stage.

- In SEA markets are tracking lower, with the commodity sensitive JCI off by over 1%. Other markets are down but losses haven't been larger than 1% at this stage.

OIL: Prices Fail To Rebound, Waiting For The Fed Decision

Oil has failed to take back any of its losses in the APAC session today as it treads water ahead of the Fed decision later. It fell over 5% on Tuesday and today it has been trading sideways. WTI is currently trading around $71.60/bbl between the intraday low of $71.51 and $71.69 and Brent is holding above $75 at about $75.32 between a low of $75.18 and a high of $75.41. The USD index is down 0.2%.

- Russia announced earlier in the year that it was going to reduce output and then extended it when OPEC+ announced its recent production cut. But according to Bloomberg, tanker-tracker data is indicating that Russia’s oil shipments jumped to 4mbd last week from 3mbd the week before. Russian oil earnings have been rising again and the government is planning to restart FX purchases.

- It is generally expected that the Fed will hike rates 25bp today but that it could signal that it is about to pause (see MNI Fed Preview: May 2023).

- Oil has been weighed down by not only the upcoming FOMC decision but also weaker risk appetite, the US debt ceiling impasse and disappointing US job opening data suggesting slower growth plus this week’s bank rescue.

- April US ADP employment is released, which should give some direction for Friday’s employment data. It is expected to rise 148k after 145k last month. There is also the services PMI and non-manufacturing ISM for April. EIA US crude and fuel inventory data also print. The Fed announcement will follow after the data.

GOLD: Holding Above $2000 As US Economic Outlook Softens, Focus On Fed

Gold has held onto Tuesday’s gains during APAC trading on Wednesday and is holding above $2000/oz. It rose 1.7% yesterday on safe haven flows reaching a peak of $2019.44 and is currently trading around $2017.05/oz down off the intraday high of $2019.53, highest since mid-April, ahead of today’s Fed meeting. The USD index is 0.15% lower.

- It is generally expected that the Fed will hike rates 25bp today but that it could signal that it is about to pause (see MNI Fed Preview: May 2023). A dovish statement is likely to support gold prices, as the yellow metal is non-yield bearing and should rally on lower rate expectations and Treasury yields. This week’s gold rally has opened up the bull trigger of $2048.70, the April 13 high.

- Bullion has been boosted by not only the upcoming FOMC decision but also weaker risk appetite, geopolitical tensions, the US debt ceiling impasse and disappointing US job opening data suggesting slower growth plus this week’s bank rescue.

- April US ADP employment is released, which should give some direction for Friday’s employment data. It is expected to rise 148k after 145k last month. There is also the services PMI and non-manufacturing ISM for April. The Fed announcement will follow after the data.

ASIA: Inflation Continues Moderation In April Giving Central Banks Flexibility

Korea, Indonesia and Thailand have released CPI data for April and have all shown moderating inflation. If this trend is seen across most of the region then non-Japan Asian inflation should see another step down in April and continue to take the pressure off most central banks to tighten further.

- Korean CPI fell below 4% in April for the first time since February 2022 and is consistent with the Bank of Korea’s decision to leave rates on hold at its last meeting. CPI eased to 3.7% from 4.2%, well below the July 2022 peak of 6.3%, and while core is proving a bit stickier, it also moderated to 4.6% from 4.8%.

- Indonesian CPI moderated to 4.3% from 5%, its lowest since May 2022 and close to the top of BI’s target band of 2-4%. It said in its April meeting statement that it is “confident” that the CPI would return to target “sooner than previously projected”. Core inflation is just under the mid-point at 2.8% down from 2.9% in March.

- Inflation in Thailand is currently lower than most of the region and eased further in April to 2.7% from 2.8% with core at 1.66% from 1.75%. The government expects headline to be below 2% in May. While rates are also lower than other countries, Bank of Thailand likely has more tightening to do given its expectations that the rebound in tourism will boost domestic growth and add to inflationary pressures, but the sanguine CPI reads give it some flexibility if it decides to slow the pace.

Source: MNI - Market News/Refinitiv

ASIA FX: Most USD/Asia Pairs Tracking Lower Ahead Of FOMC

Most USD/Asia pairs are lower today, in with further USD weakness ahead of the FOMC later. USD/CNH hasn't seen much downside, but China markets have remained closed today, they re-open tomorrow. IDR is also lagging somewhat. The rest of the region is on the front foot, with lower energy prices likely helping at the margins. Still to come is the BNM decision, with no change expected, also out later is Singapore PMIs. Tomorrow, China Caixin PMIs print, along with South Korean FX reserves.

- USD/CNH couldn't sustain an earlier dip sub 6.9300. We now sit back above 6.9360, little changed for the session. China related equities have faltered in HK. Tomorrow, we get Caixin manufacturing and service PMI prints.

- 1 month USD/KRW is down around 0.40% at this stage, last near 1334/35, which is the bottom end of the recent range. Comments by BoK Governor Rhee that it is too early to talk about a pivot to rate cuts and stating that FX pressure should ease once we are clear of the dividend outflow period has aided sentiment today.

- Spot USD/IDR has crept higher today. The pair last near 14710, with offers evident above 14720. This is only slightly weaker than yesterday's close, but the rupiah is underperforming the rest of the USD/Asia bloc, where USD weakness is more evident. This likely reflects renewed risk aversion in the equity space, which has seen Indonesia 5yr CDS creep higher, last just above 97bps. Weaker commodities are also likely to be weighing at the margins. Palm oil prices are lower, back to 3969/MYR, with likely some spillover from the oil plunge on Tuesday.

- USD/INR prints at 81.80/81, the pair is down ~0.1% in early dealing on Wednesday. A 5% fall in WTI Crude futures yesterday as concerns grow about the US economy have aided the rupee today.• The pair continues to consolidate below the 20-Day EMA, bears look to target 200-Day EMA (81.14). Bulls first look to break the 20-Day EMA at 82.00. The Apr services PMI surged to 62.0 from 57.8 in Mar.

- USD/THB hasn't been able to sustain a breach of the 34.00 level. The pair last close to 34.04, against earlier lows of 33.993. Still, the baht is around 0.50% stronger versus yesterday's closing levels, aided by the continued pull back in the USD (particularly against the yen) during today's Asia Pac session. CPI outcomes were close to expectations.

- USD/MYR prints at 4.4560/4600, the pair is down ~0.1% as the ringgit marginally firms on Wednesday, not showing too much impact from the weaker oil price backdrop. The pair printed its highest level since mid-March yesterday, however narrow ranges continue to persist. USD/MYR continues to consolidate above the 20-Day EMA, rallies have been capped ahead of 4.47 with support seen at 4.45.

SOUTH KOREA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of South Korean Newspapers and some other major news outlets from the past day or so.

Economy: Korea to provide comprehensive financial support for major exporters (link)

Economy: S. Korea eyes to expand ties with Japan on chips, battery, climate change (link)

Economy: ADB chief optimistic about Korea's future economic growth (link)

Economy: Korea, China, Japan cooperation to serve as growth engine of global economy: Korean finance minister (link)

South Korea/China: Korea wary of China's economic retaliation following Yoon's Taiwan remarks (link)

BoK: Bank of Korea governor says it’s ‘premature’ to talk about rate cuts (link)

Markets: Korean retail investors net buy bonds at record $3.2 bn in April (link)

FX: Daily FX turnover hits all-time quarterly high in Q1 (link)

FX: Korea and Indonesia sign won-rupiah direct transaction agreement (link)

Reforms: With omens improving, Yoon should get serious about reform (link)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/05/2023 | 0900/1100 | ** |  | EU | Unemployment |

| 03/05/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 03/05/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 03/05/2023 | 1215/0815 | *** | | US | ADP Employment Report |

| 03/05/2023 | 1345/0945 | *** | | US | IHS Markit Services Index (final) |

| 03/05/2023 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 03/05/2023 | 1400/1000 | ** | | US | housing vacancies |

| 03/05/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 03/05/2023 | 1800/1400 | *** | | US | FOMC Statement |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.