Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- China equity markets have turned more positive post the lunchtime break. We heard from a host of regulators at a forum in Shanghai, while earlier the large banks confirmed deposit rate cuts. Financials and property indices are leading the move higher. Equity trends are mixed elsewhere, with Japan markets among the weakest performers, unwinding some recent outperformance.

- AU yields continued to climb, the 3yr yield +14bps to 3.84%, which provided some support to AUD FX, but all the majors are firmer against the USD today. USD/JPY is back sub 139.80, but remains within recent ranges.

- The calendar is light over the rest of today with US jobless claims the main release. The ECB has a public holiday, and the Fed is in the blackout period ahead of the June 14 meeting.

MARKETS

US TSYS: Narrow Ranges In Asia

TYU3 deals at 113-04+, -0-02+, with a 0-05 range observed on volume of ~65k.

- Cash tsys sit little changed from opening levels across the major benchmarks.

- Tsys were a touch firmer in early dealing as Asia-Pac participants faded yesterday's cheapening, which was driven by spillover from the Bank of Canada's rate hike, perhaps using the opportunity to close short positions/enter fresh longs.

- Spillover pressure from ACGB's saw tsys retreat from session highs however there was little follow through on the move. Narrow ranges were observed for the remainder of the session and little meaningful macro newsflow crossed.

- FOMC dated OIS price ~9bps hike into next week's meeting with a terminal rate of ~5.30% in July. There are ~25bps of cuts priced for 2023.

- In Europe today the final read of Eurozone GDP and Employment crosses. Further out we have Initial Jobless Claims and Wholesale Trade crosses.

GLOBAL DATA: OECD Revises Up Growth Forecasts, Inflation Eases But Sticky

The OECD published its Economic Outlook and revised up its global growth forecasts from its November estimates. It expects growth to slow to 2.7% this year from 3.3% in 2022 (revised up from 3.1%). Then it should strengthen slightly to 2.9% in 2024. In November, it was forecasting growth at 2.2% in 2023 and 2.7% in 2024. The upward revision has been driven by lower energy prices, recovering business/consumer confidence and the reopening of China.

- The OECD projects China to grow by 5.4% this year and 5.1% next. The US 1.6% and 1% and the euro area 0.9% and 1.5% with Germany at 0% and 1.3%. The OECD is forecast to grow at a lacklustre 1.4% in both years.

- Risks to growth are skewed to the downside driven by uncertainties around inflation, the war in the Ukraine and the upcoming European winter.

- It expects improved supply chains, tighter monetary policy and lower food & energy prices to drive an easing in price pressures with OECD inflation moderating to 6.6% in 2023 from 9.4% in 2022 and then easing further in 2024 to 4.3%. Inflation remains sticky especially in the services sector. With inflation still expected to be above the 2% target of most OECD central banks, rate cuts may be some way off. The OECD says that monetary policy should remain restrictive until there are clear signs that there is an enduring reduction in core inflation.

- Like RBA Governor Lowe, OECD Secretary-General Cormann said that reforms are needed to boost productivity.

- See report here.

Source: MNI - Market News/IMF/OECD/World Bank

JGBS: Futures Weaker In Afternoon Trade

JGB futures weaken in Tokyo afternoon trade with pricing, -15 compared to settlement levels, after today’s 5-15.5 years until maturity liquidity enhancement auction showed less demand than the previous outing with mixed internals (better spread dynamics but a lower cover ratio).

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Q1 GDP (Final) data, which surprised on the upside.

- JGB futures continue to operate close to recent lows, with 148.48 marking the near-term support. According to MNI's technicals team, the recent bounce off the lows helped stall a more protracted pullback, although the gap with key resistance at 149.17 remains.

- In the afternoon Tokyo session, cash JGBs are trading cheaper across the curve apart from the 1-year and 7-year zone which are respectively 0.4bp and 0.7bp richer. The benchmark 10-year yield is 0.6bp higher at 0.433%. The underperformer on the curve is the 40-year zone which sees its yield 1.3bp higher at 1.462%.

- Swap rates are higher across the curve apart from the 10-year rate, with yield movements ranging from 0.3bp to 2.1bp higher. The 10-year rate is 0.3bp lower. Swap spreads are wider across the curve.

- The local calendar tomorrow is light with M2 & M3 data as the only releases.

- Tomorrow will also see BoJ Rinban operations covering 1-5-year, 5-10-years and 25-year+ JGBs.

AUSSIE BONDS: Sitting Near Cheaps, Light Local Calendar, On US Tsys Watch

ACGBs are sitting cheaper on the day (YM -16.0 & XM -15.0) after April trade data fails to generate a domestic driver. Accordingly, local participants are likely to have been on headlines and US tsys watch through Sydney's afternoon.

- Cash US tsys are sitting slightly richer in Asia-Pac after paring early gains. However, ranges do remain narrow thus far.

- Cash ACGBs are just off session cheaps, 15-16bp weaker, with the AU-US 10-year yield differential 4bp higher at +19bp.

- Swap rates are 15bp higher on the day.

- The bills strip continues to bear steepen with pricing -2 to -18.

- RBA dated OIS is 5-16bp firmer for meetings beyond July, with early ’24 meetings leading.

- Australia’s major cities posted the largest annual rent increase on record in May, fueled by rapid population growth and a significant shortfall in property listings that highlight powerful inflation pressures in the economy, according to CoreLogic data. (link)

- The local calendar is light tomorrow. The next key data is on Tuesday with the release of Westpac Consumer Confidence (June) and NAB Business Confidence (May). Next week’s highlight undoubtedly will be the May Employment Report on Thursday.

- Later today sees Q1 GDP (Final) in the Euro Area, ahead of US Jobless Claims.

AUSSIE BONDS: Yield Curve Flattest & 3-Year Yield Highest Since 2011

The Australian 3/10 cash curve has reached its lowest level since 2011, as the 3-year yield climbs to its highest level since 2011. At 13bp, the curve is approximately 9bp flatter compared to Friday's closing level, while the 3-year yield has risen by 40bp.

- The flattening of the Australian curve and the upward movement in the 3-year yield coincide with multiple factors.

- Firstly, there was a global surge in bond yields overnight triggered by the unexpected rate hike from the BoC, which occurred just one day after a similar move by the RBA.

- Secondly, the flattening comes following yesterday’s hawkish speech by RBA Governor Lowe and disappointing Q1 GDP data, which revealed concerning updates on productivity and unit labour costs (ULC). Productivity slowed to -4.5% year-on-year, the lowest annual rate since the series began in 1979. Additionally, ULCs increased from 6.9% year-on-year in Q4 to 7.9%, marking the highest annual rate outside of the pandemic since 1990. These data points will contribute to inflation risks and are likely to raise concerns for the RBA.

- The RBA's surprising 25bp rate hike, bringing the cash rate to 4.10%, coupled with the Q1 GDP data, has led to heightened expectations for the terminal cash rate, which has reached a cycle high of 4.45%.

Figure 1: AU 3/10 Yield Curve (%) Vs. 3-Year ACGB Yield (%)

Source: Bloomberg / MNI - Market News

AUSTRALIAN DATA: Commodities Weigh On Exports, But Trade Remains Solid

The April trade surplus narrowed more than expected to $11.16bn from a downwardly-revised $14.82bn driven by weaker exports but still rising imports. It remains elevated and within the range seen since 2021. The series is nominal and so was impacted by declining commodity prices.

- Exports fell 5% m/m after rising 4.1% due to weaker metals ores and minerals. While goods exports were down 7% m/m after +4.4%, services rose 7.8% (Mar +2.4%) with tourism up 13.4%. Services exports are now +55.6% y/y with merchandise -2.8%. There was a sharp drop in rural goods as well as the main commodity exports. Metal ores fell 10.4%, coal -7.1% and metals -17.9% due to lower prices and volumes.

- Imports rose 1.6% m/m after an upwardly-revised 3.7% in March, driven by civil aircraft (+103.4% m/m), with goods up 1.1% (Mar +3.9%) and services +3.7% (+2.7%). Services imports are now +23.6% y/y and merchandise +5.4%. Machinery & equipment rose 4.7%, implying that the capex recovery seen in Q1 should continue into Q2. Consumer goods rose 0.7% driven by food & beverages. Tourism imports increased 7.3%, as the recovery in travel continues.

Source: MNI - Market News/Refinitiv

AUSTRALIAN DATA: ULC Growth Probably Peaked But Remains Challenge To Services

RBA Governor Lowe noted in his remarks on Wednesday that one of the reasons for the June hike was due to upside risks to inflation from persistent services inflation, which he stated is now “here” and not just an overseas phenomenon (see MNI: Lowe: Persistent Services Inflation "Here", Tightening Not Done). He also observed that strong services inflation is linked to current high unit labour cost growth (see MNI: Lowe: Upside Inflation Risks Increased Since April Pause).

- Q1 productivity fell 4.5% y/y, the lowest annual rate since the series began in 1979, and ULC rose 2% q/q to be up 7.9% y/y from Q4’s 6.9%, the highest since 1990 outside the pandemic (see MNI: Q1 Productivity Growth New Record Low). The RBA has 1% productivity growth in its inflation forecasts. Our estimates show that no increase in hours worked from Q3 2023 is required to achieve that by Q1 2024, which would bring ULC down to 3% (using RBA GDP and WPI forecasts). It also appears that Q1 2023 was the peak in ULC growth.

- Given Lowe’s comments and the chart below, the Q1 data is only going to increase inflation risks and the RBA’s concerns. There is a 64% correlation between ULC y/y% and services inflation since 1988. While ULC troughed 2 quarters after services inflation, they have been moving higher together since mid-2022.

Source: MNI - Market News/ABS

Australia ULC y/y% with scenarios

Source: MNI - Market News/ABS/RBA

NZGBS: Cheaper But Outperforms ACGBs

NZGBs closed on a low note with the benchmarks 11-13bp cheaper and the 2/10 cash curve steeper. Weekly supply sees solid demand (cover ratio above 3.00x) for the Apr-33 and Apr-37 bonds, but a somewhat weaker bid for the May-30 bond (cover ratio at 2.64x). The lines richened around 0.5bp post-auction in line with the broader market.

- NZGBs have shown stronger performance compared to ACGBs, with the NZ/AU 10-year yield differential -4bp. At +59bp, the NZ/AU differential is back near its tightest level since mid-February. The 10-year differential hit a 20-year+ high in March at around +100bp.

- Swap rates closed 11-14bp higher with the 2s10s curve 3bp steeper.

- RBNZ dated OIS pricing closed 6-10bp firmer for meetings beyond October with May’24 leading. Terminal rate expectations sit at 5.64% (October).

- Q1 manufacturing volumes fell 2.1% q/q after -4.6% in Q4. Statistics NZ said that the data has been impacted by recent severe weather events but that it is difficult to isolate that from other special factors. Q1 GDP is published on June 15.

- The local calendar is light tomorrow with Retail Card Spending for May slated for Monday. The highlight of next week, however, will be Q1 GDP on Thursday.

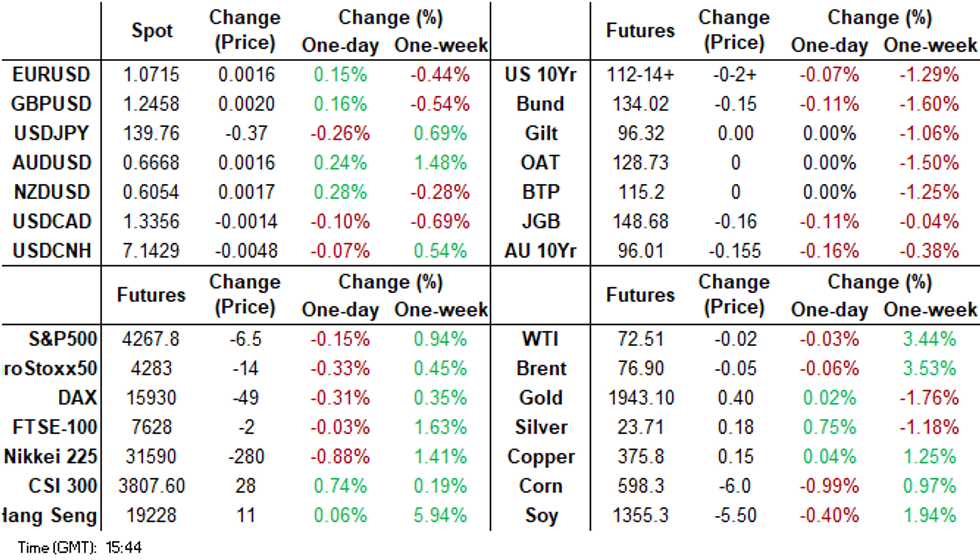

FOREX: USD Edges Lower In Asia

BBDXY is ~0.1% lower in Asia paring some of Wednesday's gains. The Antipodeans and the Yen are all marginally outperforming in the G-10 space at the margins.

- USD/JPY is ~0.2% lower, and sits at session lows. The pair last prints at ¥139.80/90, support comes in at ¥138.45 the low from June 1 and 20-Day EMA. The final read of Q1 GDP printed this morning at 0.7% Q/Q a rise of 0.5% had been expected.

- Kiwi is paring some of Wednesday's losses, NZD/USD is up ~0.2% however the pair has met resistance above $0.6250. Early in the session Q1 Mfg Activity printed at -2.1% Q/Q (volume) and -2.8% Q/Q (sales), there was little reaction in FX markets.

- AUD/USD is also ~0.2% higher, last printing at $0.6660/65. April's Trade Surplus was narrower than expected printing at $11.158bn vs $13.65bn.

- Elsewhere in G-10 ranges have been narrow with little follow through on moves.

- Cross asset wise; e-minis are ~0.1% lower and US Treasury Yields are little changed. WTI futures are marginally lower.

- On the wires today we have the final read of Eurozone GDP and US Initial Jobless Claims.

FX VOL: G10 Implied Volatility Continues To Tick Lower

1 Month Implied volatility in FX markets, measured using the JP Morgan G-10 Volatility Index, sits a touch off the lowest levels seen since early 2022, which were printed last week.

- The index prints at 7.69%, having printed its lowest level since March 2022 on Friday at 7.68%.

- Option markets remain calm with implied vol well below elevated levels seen in the wake of the SVB crisis, despite unexpected rate hikes from the RBA and BOC and the winding back of Fed rate cut expectations for 2023 which now sit at ~20bps.

Fig 1: JPMorgan G10 FX Volatility

Source: JP Morgan/MNI/Bloomberg

EQUITIES: Japan Stocks Lose Further Altitude, US Futures Tracking Lower

Equity sentiment has softened throughout the region as the Thursday session progressed, although China markets were more mixed as we heard from a host of regulators at a forum in Shanghai. Japan markets have been among the weakest performers. US equity futures are also tracking lower, with Eminis down 0.25% (last near 4264), while Nasdaq futures have dipped -0.45%, sitting around session lows currently.

- In Japan, the Nikkei 225 is off by around 1% continuing its recent pull back. This has perhaps weighed on US futures moves. Deutsche Bank cut its Japan stock weight to 5% from 25%, amid waning Asia momentum from a strategy standpoint. Mizuho also cut its long term prime rate to 1.3%, effective tomorrow. Tech related plays have been another source of weakness for Japan bourses.

- We heard from a host of China officials, including the head of NFRA and the PBoC Governor. A lot of focus was regulation and reducing financial risks, whilst also encouraging innovation and greater access to foreign firms. They pledged that the financial sector would support the real economy.

- Property equities rebounded from earlier losses, the CSI 300 property index up 1.25% at the break. Li, the head of the NFRA, stated China will push redevelopment of urban villages in big cities. Aggregate China equity indices are more muted though. Earlier we got confirmation of the major bank deposit rate cut.

- The Taiex lost 1% and the Kospi is down 0.65% at this stage.

- SEA markets are mixed.

OIL: Market Demand Worries Outweigh Output Cuts

Oil prices are marginally lower during APAC trading today, as demand worries came to the fore again, but are off their intraday low. Crude is finding some support from mixed US inventory data. The USD has been trending down and is around 0.1% lower, which hasn’t boosted oil prices.

- Crude has been moving in a narrow range. Brent is down 0.3% to around $76.72/bbl, off the low of $76.61. It reached an intraday high of $77 earlier. WTI is also 0.3% lower at $72.34 following a low of $72.23 and a high of $72.61.

- A large increase in US refinery utilisation to the highest since August 2019 drove an unexpected drawdown in US crude inventories. But they remain below the 5-year seasonal average. Refiners are expecting strong demand through the summer. The DOE reported a 1.6% increase in US oil production to a 3-year high.

- The calendar is light over the rest of today with US jobless claims the main release. The ECB has a public holiday, and the Fed is in the blackout period ahead of the June 14 meeting.

GOLD: Back At 3-Month Lows After BoC’s Surprise Hike

Gold is 0.3% higher in the Asia-Pac session, after closing at 1940.02 (-1.2%) on Wednesday as global bond yields surged after a surprise BoC rate hike fueled bets that global central banks are not yet done with tightening.

- Treasury yields rose 8-13bp across major benchmarks and the dollar erased earlier losses on Wednesday after the BoC decision.

- The BoC's 25bp increase brought the policy rate to 4.75% and marked a significant shift in direction, considering rates were left unchanged at the previous two meetings. The decision was attributed to stronger-than-expected GDP growth in Q1, a recent upturn in housing market activity, persistent excess demand in the economy, and a higher-than-anticipated CPI in April. Prior to the announcement, the market had assigned a 45% probability of a 25bp rate hike.

- In recent weeks, the price of the precious metal has remained relatively stable in a range centred on $1,950 per ounce, as investors eagerly await clearer signals regarding the future direction of US monetary policy.

ASIA FX: USD/CNH Hits Fresh Highs Before Retracing, Won Outperforms

Most USD/Asia pairs haven't been able to rally today, which goes against the trend seen for the majors. USD/CNH got to fresh highs but is slightly lower now, headlines dominated by regulator speeches in Shanghai today. KRW has outperformed at the margins, while MYR and THB have underperformed. Tomorrow, May inflation data in on tap for China, which will be the main focus point. Philippines trade figures are also due and Malaysia IP as well.

- China SAFE Head Pan Gongsheng has spoken at the Lujiazui forum in Shanghai. Comments came across as quite relaxed around the current FX backdrop that China faces. Pan stated that the FX rate is basically stable and that the market is functioning normally. He added that USD strength is unsustainable as the Fed hiking cycle nears an end. He said it was likely the US economy was likely facing a recession and that this would support the yuan. Pan reiterated the authorities have increasingly amply forex policy tools. Pan's comments hint the China authorities are looking to ride out this wave of USD strength. USD/CNH sits slightly below the 7.1500 handle, unchanged for the session so far.

- 1 month USD/KRW sits modestly below NY closing levels, last just under 1303.50. This is slightly outperforming steady CNH trends, although higher beta majors are firmer against the USD (A$ and NZD), while USD/JPY is lower, which may also be helping at the margins. Spot is above yesterday's closing levels, but not by much, last in the 1305/06 region.We have heard commentary from FinMin Choo. He stated growth may be weaker than expected and that the 1.6% 2023 GDP forecast may need to be nudged down. For the FX though, the trade deficit is expected to improve further in June and that FX volatility has eased of late. The authorities also haven't decided whether power prices will rise in Q3, but Choo stated June CPI could fall to the 2% level. BoK Deputy Governor Lee Sang-hyeong also spoke and stated the tightening cycle is not over yet, and it is too early to relax about inflation, per Reuters reports.

- The RBI has left its Repo Rate unchanged at 6.50% today there was a unanimous decision in holding rates steady. Governor Das has said that the bank remains focused on withdrawing accommodation, 5 out of 6 members voted for the stance decision. The rupee had a muted reaction to the RBI's decision holding steady in a narrow range thus far. USD/INR last prints at 82.57/59, little changed from opening levels. 10 Year Bond Yields are up ~3bps rising to an intra-day high of 7.01%. In the domestic equity market the Nifty is edging higher from pre-RBI levels.

- USD/MYR is ~0.5% firmer this morning, the pair is dealing above the 4.60 handle last printing at 4.6170/90. The pair continues to see-saw around the 4.60 handle, and has been unable to sustain a break of the handle this week. A short time ago BNM Deputy Gov Fraziali noted that Malaysia is not entering recession, reaffirming the 2023 inflation forecast. Fraziali also said that the BNM is slightly accommodative and they don't see inflation "misbehaving". Earlier today Bank Negara Malaysia Gov. Shamsiah Yunus noted this morning that receding cost pressures are not feeding through to product prices as demand remains high. She also noted that the central bank's role is to ensure that the value of the currency doesn't swing too fast or too much.

- The SGD NEER (per Goldman Sachs estimates) is firmer this morning, the measure printed its highest level since 22 March this morning. We now sit ~0.6% below the upper end of the band. USD/SGD is a touch lower in early trade today, however ranges have been narrow thus far with broader USD/Asia flows dominating recent dealing. Singapore's Foreign Reserves rose to $325.7bn in May which is the highest in a year, increasing by 13.7bn from a month earlier. The local docket is empty for the remainder of the week.

- THAILAND: The alliance of 8 political parties expected to form a new government is hoping to bring forward the formation by 2-3 weeks if the Election Commission speeds up the endorsement of MPs-elect, according to the Bangkok Post. There were further coalition talks held on Wednesday and all parties are scheduled to meet again on June 20. The group have already begun to work on certain issues. USD/THB has tracked higher today, the pair last close to 34.90.

INDONEISIA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of Indonesian Newspapers and some other major news outlets.

Markets: “Indonesian crude oil prices to hold steady in 2024: energy minister” – Jakarta Globe (see here)

- The Energy Minister Arifin sees oil prices in 2023 and 2024 stable within $70-$80, “given the current geopolitical situations”. He also said that OPEC+ will manage output to try and stop prices falling below $80/bbl.

ASEAN: “Malaysia, Indonesia solve 18-year-old border issues, sign pacts” - Bloomberg (see here)

- As well as the agreement on the maritime border dispute, the two leaders signed pacts on trade and migrant workers. Both countries will speak as one to defend palm oil producers in face of EU deforestation rules.

ASEAN: “Indonesia to hold ASEAN Indo-Pacific Forum on 5-6 September 2023” – Antara News (see here)

ASEAN: “ASEAN-BAC committed to promote economic growth in the region” – Antara News (see here)

Business: “Indonesia, S Korea agree to develop ICT ecosystem for SMEs” – Antara news (see here)

Economy: “Indonesia has best market potential in Southeast Asia: Minister” – Antara news (see here)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/06/2023 | 0900/1100 | *** |  | EU | GDP (final) |

| 08/06/2023 | 0900/1100 | * | | EU | Employment |

| 08/06/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 08/06/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 08/06/2023 | 1400/1000 | ** | | US | Wholesale Trade |

| 08/06/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 08/06/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 08/06/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 08/06/2023 | 1920/1520 |  | CA | BOC Deputy Beadury speech |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.