Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

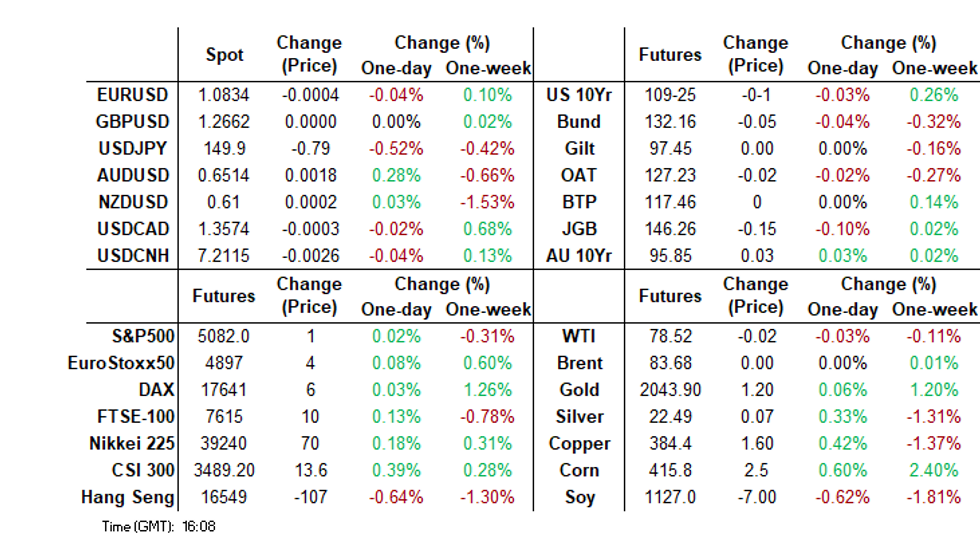

- JGB futures are holding weaker and close to session lows, -21 compared to settlement levels. The key driver of the move lower was comments from BoJ Board Member Takata. He sent a strong signal that the case for ending the negative interest rate policy is gaining momentum. Yen outperformed in the G10 space, but is away from best levels.

- Treasury futures have drifted lower during the Asian session on Thursday, although well within yesterday's ranges. The USD is mostly weaker though, across the G10 and Asia FX space.

- Regional Asian Equities have recovered from the lows of earlier to trade mixed to slightly higher, which also added to the risk tone for the region.

- Later the Fed’s Bostic, Goolsbee and Mester speak. January US income/spending data including the PCE deflators, jobless claims, February MNI Chicago PMI and Kansas Fed index print. There are also German, French and Spanish preliminary February CPIs and Q4 Canadian GDP.

MARKETS

US TSYS: Treasuries Edge Lower Ahead Of US Data Later

Treasury futures have drifted lower during the Asian session on Thursday, although well within yesterday's ranges. Treasury yields are 1-2bps higher, while there has been little in the way of market headlines apart from Yellen to meet with global leaders in Brazil, while the US house will vote on Stopgap Funding bill at 1.30pm ET.

- Jun'24 futures touched a early high of 110-14 on Asia open, but has only moved since then, touching a low 110-09 however still well within recent ranges. The trend direction in Treasuries is unchanged and remains down with the contract continuing to trade closer to its recent lows, taking a look at technical levels initial resistance holds at 110-28+ (20-day EMA), while initial support at 109-25+ (Low Feb 23).

- Treasury yields are giving up some of the moves lower from Wednesday, with yield curve 1-2bps higher. The 2Y yield is 1.4bp higher at 4.652%, the 10Y is 1.4bp higher at 4.278%, while the 2y10y is unchanged at -37.631

- There were a flurry of Fed Speaks on Wednesday with Atlanta Fed President Bostic remaining "comfortable" with a patient Fed strategy to address inflation, he still expects the first rate cut this summer. NY Fed President Williams reiterated the Fed has a "ways to go to sustained 2% inflation", while Boston Fed President Collins wants greater confidence in disinflation before soften policy

- Looking ahead: Personal Income/Spending, PCE, Jobless Claims & MNI Chicago PMI

JGBS: Bear-Steepener After BoJ Takata Comments, US PCE Deflator Due

JGB futures are holding weaker and close to session lows, -21 compared to settlement levels. The key driver of the move lower was comments from BoJ Board Member Takata. He sent a strong signal that the case for ending the negative interest rate policy is gaining momentum. (See link)

- JGB futures had earlier spiked higher after Industrial Production declined more than expected in January.

- The other domestic catalyst today was 2-year supply. The supply showed mixed demand metrics, as the low price failed to meet dealer expectations and the cover ratio declined. However, it is worth noting that today’s cover ratio was the second highest for a 2-year auction since July last year.

- Considering that today's auction took place with an outright yield at its highest level since 2011, the result highlights the impact that uncertainties surrounding the BoJ policy outlook are having on bond demand.

- Cash tsys are ~1bp richer in today's Asia-Pac session ahead of US PCE Deflator data later today.

- The cash JGB curve has bear-steepened, with yields 1-3bps higher. The benchmark 10-year yield is 1.7bps higher at 0.717%.

- The swaps curve has also bear-steepened, with rates 1-2bps higher. Swap spreads are little changed.

- Tomorrow, the local calendar sees Jobless Rate, Job-To-Applicant Ratio, Jibun Bank PMI Mfg and Consumer Confidence data.

AUSSIE BONDS: Richer, Mid-Range, Awaiting US PCE Deflator Data

ACGBs (YM +3.0 & XM +3.5) are richer but sit in the middle of today’s Sydney session ranges. Today’s mixed domestic drop (Retail Sales weaker, Capex Stronger and Private Sector Credit in line with expectations) failed to meaningfully move the market. At the time of writing, ACGB futures were 1-2bps weaker than pre-data levels.

- The Australian economy is facing a significant slowdown but will likely avoid a recession, Treasurer Jim Chalmers said on Thursday. Speaking from the G20 Finance Ministers and Central Bank Governors meetings in Brazil, he told the ABC that while inflation is falling in Australia, the country is "not immune" to weak global growth. (See link)

- Cash tsys are ~1bp richer in today's Asia-Pac session ahead of US PCE Deflator data later today.

- Cash ACGBs are 3-4bps richer, with the AU-US 10-year yield differential flat at -14bps.

- Swap rates are 3-4bps lower.

- The bills strip has bull-flattened further, with pricing flat to +4.

- RBA-dated OIS pricing is flat to 1bp softer across meetings. A cumulative 36bps of easing is priced by year-end.

- Tomorrow, the local calendar sees CoreLogic House Prices and Judo Bank PMI Mfg data.

- Tomorrow, the AOFM plans to sell A$800 million of 3.75% May-34 bond.

AUSTRALIAN DATA: Through The Volatility Retail Sales Stagnating

Retail sales have been volatile over the festive period. They rose a less-than-expected 1.1% m/m in January but December was revised up 0.6pp to -2.1% m/m. Spending was up 1.1% y/y but 3-month momentum while still positive moderated. With goods inflation at 3.7% y/y in January, sales volumes likely fell again, in line with the RBA’s assessment that “consumption growth is weak”. With higher rates and continued cost-of-living pressures, this situation looks unlikely to improve soon.

- The ABS notes that “retail turnover was unchanged in trend terms in January” signalling that retail sales have stagnated when we look through the volatility of recent months.

- There was a broad based increase in retail sales in January with only food retailing recording a decline which was -0.1% m/m. Restaurants saw their first monthly increase (+1.3%) since August boosted by large sporting events.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: Slower Momentum In SEEK Advertised Salaries

SEEK advertised salary increases have lost momentum with a 0.2% m/m rise in January bringing the 3-month annualised rate down to 3.7% from 4.5%, the lowest in almost two years. Annual growth in advertised wages was steady in January at 4.5% but is down from the 4.8% peak in September. The RBA continues to say that wage growth is consistent with the inflation contingent on an improvement in productivity growth. While it is difficult to measure, there will be further information in the March 6 national accounts.

- The large states of NSW and Victoria saw slightly lower advertised pay growth than the national average, as jobs growth has also underperformed in these regions.

- There was a strong 8.9% y/y increase in the community services sector due to the government’s 15% increase for aged care workers. In contrast IT jobs rose only 1.9% y/y.

Source: MNI - Market News/SEEK

RBNZ: MNI RBNZ Review – February 2024: High Bar To Shift Rates Either Way

- The RBNZ left rates at 5.5% and apart from updates to history and their impact on the forecasts, there was little change in its outlook, which it now has more confidence in. Governor Orr noted as a result the MPC is now more tolerant of upside inflation risks than it was. The threats of further tightening were toned down compared to November.

- A tightening bias was retained by the central bank though as there is “limited tolerance to increase the time to the target mid-point”, a hike was discussed but not a cut, and the peak in the OCR path is still above the current rate. Orr also said that while the risks to inflation are now seen as “more balanced” due to a combination of factors, its reaction function remains asymmetric towards upside risks as inflation is still above target.

- RBNZ dated OIS pricing has a cumulative 74bps of easing priced by year-end from an expected OCR peak of 5.54%.

- The RBNZ appears to be firmly on hold for now barring some unexpected shock. The economy is developing broadly as expected but policy needs to remain restrictive to bring inflation back to target. The OCR path has rates on hold this year and Orr reiterated that it is too early to discuss easing, which the MPC didn’t do in February.

- See full RBNZ review here.

NZ STIR: RBNZ Dated OIS Back To Pricing Two 25bp Cuts By Year-End

RBNZ dated OIS pricing closed 1-5bps softer across meetings today. This comes after late 2024 meetings shunted around 20bps softer yesterday following the RBNZ policy decision.

- A cumulative 54bps of easing is priced by year-end from an expected OCR peak of 5.54%.

- Before the decision yesterday, the market had attached a 29% chance of a 25bp hike at yesterday’s meeting, with an anticipated terminal OCR of 5.65% (reflecting a 61% probability of a 25bp hike) by the May meeting. A cumulative 40bps of easing by year-end was factored into the pricing.

- It is also worth noting that in late December, the market had expected over 100bps of easing by year-end, stemming from an anticipated terminal OCR of 5.53%.

Figure 1: RBNZ Dated OIS Expected Terminal & End-24 OCR (%)

Source: MNI – Market News / Bloomberg

NZ DATA: ANZ Survey Consistent With Policy Staying Restrictive

NZ February ANZ business data was overall quite robust with the outlook rising to 29.5 from 25.6, highest since June 2021, and while confidence fell to 34.7 from 36.6, it is still higher than December. The good news is that inflation expectations eased 0.3pp to 4.0%, the lowest in over 2 years, but cost and wage expectations remain elevated and as a result pricing intentions remain too high. The RBNZ said yesterday that rates need to stay restrictive for some time to ensure inflation returns to target, and this survey data corroborates that view.

NZ ANZ business activity vs confidence

Source: MNI - Market News/Refinitiv

- ANZ notes that the own activity measure is consistent with “low but positive annual GDP growth”.

- 73.5% of firms expect to see their costs rise in the coming 3 months, down from 75.6% in January, but ANZ says that this needs to be below 50% to signal a low inflation environment. While the series is below its peak, it has been very sluggish to ease. But the magnitude of the expected increase over the next 3-months eased to 3.1% from 3.4%. The retail, agriculture and construction sectors all reported freight disruption since Q4 2023.

- Pricing intentions 3-months ahead moderated 0.2pp to 1.9%. This measure has also been slow to decline. 48.2% of firms intend to increase prices down 1.5pp from January.

- Employment intentions improved to their highest since April 2022 driven by the services sector. 79% of firms still expect to increase wages over the year ahead with the expected rise 3.4%.

Source: MNI - Market News/Refinitiv

NZGBS: Slightly Richer As RBNZ Gov. Orr Shuts Door On Hike

NZGBs closed flat to 1bp richer and near the session’s best levels after RBNZ Governor Adrian Orr said policymakers had decided against raising interest rates this week because the latest data confirmed that inflation is slowing. (See link)

- (AFR) The RBNZ surprised pundits by appearing less inclined to raise interest rates further, sending the local currency and bond yields lower as traders sharply trimmed the chance of further tightening. (See link)

- Business Confidence lost -1.9 points from a month earlier in February to 34.7, according to ANZ. However, the Activity Outlook rose to 29.5 from 25.6 in January.

- Today’s weekly supply showed mixed results in terms of demand metrics. The May-28 and May-41 lines saw cover ratios of 2.6-2.7x, while the Apr-33 line showed 1.85x.

- Swap rates closed 3bps lower.

- RBNZ dated OIS pricing is 1-5bps softer across meetings today. This comes after late 2024 meetings shunted around 20bps softer yesterday following the RBNZ policy decision. A cumulative 74bps of easing is priced by year-end.

- Tomorrow, the local calendar sees CoreLogic House Prices, ANZ Consumer Confidence and Building Permits data, along with a speech from RBNZ Governor Orr to the Canterbury Chamber of Commerce.

FOREX: Yen Strengthens On BoJ Speech, A$ Higher, US PCE In Focus Later

Yen strength has been the main feature of G10 FX markets today. The BBDXY was last down a little over 0.1%, tracking close to 1242. AUD/USD is also higher, as is NZD, but the Kiwi has lagged somewhat.

- USD/JPY was drifting lower before BoJ Board member Takata spoke, but broke down through 150.00 on hawkish comments from the central banker. Most notably was reference to the price target finally coming into sight. References to current spring wage negotiations was also bullish.

- USD/JPY got to lows of 149.70, not too far from the 20-day EMA (near 149.63), but we now sit slightly higher at 149.85.

- AUD/USD has risen around 0.35%, last close to 0.6520. Firmer China equities have helped, although trends are mixed elsewhere in the region. Iron ore prices have also stabilized, last near $118/ton, up around 1.6%. Data was mixed with retail sales sub expectations, but capex slightly stronger. We didn't see an AUD reaction though.

- NZD/USD didn't react to the earlier data, and has remained in very tight ranges, although making new daily highs of 0.6104, if the pair is able to hold back above 0.6100 level, a further move higher wouldn't be unexpected after Wednesday's 1.20% move lower.

- AUD/NZD is edging higher as trading progresses today, nearing highs made during the US session on Wednesday (1.06857) to trade last at 1.0675/80.

- Looking ahead, the January PCE deflator will be the last reading of the Fed's preferred inflation gauge before the March FOMC meeting. Before this, regional inflation data from the Eurozone, including Germany, Spain and France is out.

ASIA STOCKS: HK & China Equities Higher Into Month End, CSRC To Restrict Quant Strategies

Hong Kong and China equities are higher today as investors after a decent sell-off on Wednesday driven by a crackdown on quants funds and their trading strategies, it has also been reported that a Top-performing Quant fund has been banned from the stock-index futures market for a year. Hong Kong Markets are lagging China Mainland equities in what could be due to disappointment in the Budget released on Wednesday. Month -end flows have been seen to help push markets higher today with Property and Growth stocks the top performers in the region.

- Equities markets are higher come out of the Asia break. Mainland Property Index is the top performer this morning up 0.90%, although the index was 3.80% lower Wednesday. HSTech Index in flat for the day, after Baidu's profits plunged 48% as AI costs hurt bottom line, while the wider HSI is up 0.15% led higher by Financials with HSBC up 1.50%. In China growth stock are leading the way higher, with the CSI1000 up 1.60%, after being up as much as 3.10%, while the CSI300 is 0.90% higher.

- China Northbound flows were +1.3b yuan on Wednesday, with the 5-day average now 3.1b, while the 20-day is at 2.81b yuan.

- JPM was earlier out recommending investors sell into any strength in Hong Kong Property Developers after the government announced it will be scrapping property curbs, as they view the easing will boost volumes, but home prices will continue their trend lower.

- China’s securities regulator (CSRC) will look to restrict Quant trading strategies that have been seen to be responsible for recent market turmoil, and guide funds in controlling the size and leverage of their DMA businesses.

- China banned a top-performing quant fund (Shanghai Weiwan Fund Management) from the stock-index futures market and vowed tighter oversight of high-speed trading, expanding a crackdown on computer-driven investment strategies that some have blamed for exacerbating market turmoil.

- Major companies with earnings due out today include Budweiser Brewing Co APAC, HK Exchanges & Clearing and NetEase. NetEase will be the most closely watch after they have recently had gaming content approved.

- Looking ahead, Hong Kong has Budget Balance & Money Supply data out.

ASIA PAC EQUITIES: Regional Asian Equities Rebound To Trade Mostly Higher

Regional Asian Equities have recovered from the lows of earlier to trade mixed to slightly higher. There hasn't been much in the way of market drivers or headlines so far today with markets largely following the moves from the US on Wednesday, tech stocks are the worst performers after US giants Nvidia and Apple traded lower overnight.

- Japan equities are now flat to slightly higher today, after previously being down about 0.50%. Tech stocks are the worst performers, with the Nikkei under-performing. Aozora Bank, who have been caught up with recent weakness from the US Commercial property space, surged higher today after Activist Investor Yoshiaki Murakami added positions in the company. Foreign investors sold ¥206b of Japanese stocks the first outflow for the year on Wednesday, while BoJ's Takata was out earlier with a hawkish tone, noting the price target is finally coming into sight, despite the economic uncertainty. Currently the Topix is up 0.10% while the Nikkei 225 is 0.10% lower.

- South Korean equities are lower today, after out-preforming the wider market on Wednesday on news that Zuckerberg had meet with the heads of LG and Samsung and discussed AI technology spurred the markets higher and helped attract foreign equity inflows with $473m coming in on Wednesday. Currently the Kospi is down 0.35%.

- Taiwan Equities were closed yesterday

- Australian equities are higher today, as markets pushed higher post Retail Sale missed estimate earlier today, markets now see higher chances of rate cuts earlier. The ASX200 closed up 0.50%.

- Elsewhere in SEA, NZ equities are lower today, down 0.20%, Indonesian equities saw positive foreign inflows on Wednesday, equities trading mostly unchanged today, while Singapore & Malaysia equities are a touch higher today up 0.20%

ASIA EQUITY FLOWS: Asian Equity Flows Start To Slow After Equities Markets Hit Highs

- China equities had a soft session on Wednesday, one of the countries largest property developers Country Gardens was given a wind-up notice in a HK court a day after it was report China Vanke was in talks to restructure there debt, although inflows remained positive with 1.3B yuan entering the market. The 5-day average is 3.1b, while the 20-day is at 2.81b yuan.

- South Korean equities out-performed in the region on Wednesday following reports Mark Zuckerberg met with LG & Samsung heads were they spoke about AI integration. Foreign equity inflows reach the highest since Feb 2 on this news. Total flows were overall negative for the day as individuals sold a total of $527m vs $473 of foreign buying inflows. The 5-day average is $160m, while the 20-day is at $297m.

- Taiwan equities were closed on Wednesday

- Indonesian broke their 4 days of outflows with a tiny $1.5m of foreign inflows, there was little in the way of headlines. The 5-day average is -$42m, while the 20-day is at $42m.

- Thailand saw $21m of inflows on Wednesday, ahead of BoP Current Account Balance data out later today. The 5-day average is $34m, while the 20-day is at $9m.

- India will see GDP data out later today, while equities markets have positive flow momentum with the 5-day average at $85m vs the 20-day at just $7m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | 1.3 | 15.9 | 29.6 |

| South Korea (USDmn) | 473 | 803 | 8189 |

| Taiwan (USDmn) *** | 0 | 1131 | 4802 |

| India (USDmn)** | 248 | 429 | -2997 |

| Indonesia (USDmn) | 2 | -211 | 1221 |

| Thailand (USDmn) | 21 | 174 | -667 |

| Malaysia (USDmn) ** | 40 | 92 | 512 |

| Philippines (USDmn) | 0 | 5.7 | 201 |

| Total (Ex China USDmn) | 784 | 2423 | 11261 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To Feb 27 | |||

| *** Market Closed Feb 28 |

JAPAN DATA: Offshore Buying Streak Of Local Equities Ends

The streak of offshore buying of Japan stocks has come to an end. Last week saw -¥206bn in net outflows from this segment. This was the first outflow since the end of 2023. Still, net inflows YTD stand at +¥3612.7bn. With Japan markets making fresh highs in recent weeks, the outflows from last week may have reflected some position squaring/profit taking. Offshore investors were modest net sellers of local bonds, making the second consecutive week of outflows.

- In terms of Japan offshore buying, local investors were net sellers of offshore bonds for the second straight week. Net outflows for this segment were still positive by over ¥1000bn for Feb as a whole.

- Japan purchases of offshore stocks continued for the third straight week.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending Feb 23 | Prior Week |

| Foreign Buying Japan Stocks | -206.0 | 382.5 |

| Foreign Buying Japan Bonds | -19.0 | -521.1 |

| Japan Buying Foreign Bonds | -257.0 | -570.9 |

| Japan Buying Foreign Stocks | 225.9 | 359.7 |

Source: MNI - Market News/Bloomberg

OIL: Crude Steady In APAC Session, Headed For A Second Monthly Rise

Oil prices are headed for their second straight monthly rise as they are little changed during APAC trading after falling around 0.8% yesterday. Expectations of an extension to OPEC cuts are outweighing continued US stock builds. WTI is unchanged at $78.53/bbl, close to the intraday high, and Brent is 0.1% lower at $82.11, closes to today’s $82.13 peak. The USD index is down 0.1%.

- Oil weakened on news that EIA crude stocks rose a more-than-expected 4.2mn barrels last week after 3.5mn the previous week. Gasoline fell 2.83mn and distillate -0.5mn but refinery utilisation rose almost 1pp to 81.5% resulting in increased product output.

- WTI timespreads widened further indicating a tightening of the market, according to Bloomberg. Trafigura’s chief economist Rahim noted that “you’re hearing the phrase ‘upside risk’ a lot more” from the manufacturing and petrochemicals sectors.

- Later the Fed’s Bostic, Goolsbee and Mester speak. January US income/spending data including the PCE deflators, jobless claims, February MNI Chicago PMI and Kansas Fed index print. There are also German, French and Spanish preliminary February CPIs and Q4 Canadian GDP.

GOLD: Slightly Firmer Ahead Of US Inflation Data

Gold is slightly stronger in the Asia-Pac session, after closing 0.2% higher on Wednesday.

- Bullion recovered off a low of $2024.59 to finish at $2034.55 as the USD gave up earlier gains and US Treasuries rallied.

- US Treasuries finished the NY session with modest gains. US Treasury curve bull-steepened ahead of key PCE Deflator data later today, with yields 2-5bps lower. US Treasuries were supported by a flurry of balanced Fed speak.

- While Atlanta Fed President Bostic remains "comfortable" with a patient Fed strategy to address inflation, he still expects the first rate cut this summer.

- More cautiously, NY Fed President Williams reiterated the Fed has a "ways to go to sustained 2% inflation", while Boston Fed President Collins wants greater confidence in disinflation before softening policy.

- According to MNI’s technicals team, recent price activity has defined key resistance at $2065.5, the Feb 1 high, and key support at $1984.3, the Feb 14 low - both levels represent important short-term directional triggers.

INDONESIAN SOVEREIGNS: Indonesian Yields Find Support, Offshore Investors Off-Load Bonds

Indonesian USD sovereign debt yields rose 1-2bps on Wednesday, under-performing moves tighter by US treasuries. As we head into the Asia break INDON curves trade unchanged to 1bps tighter with curves slightly steeper. Recent weakness in Indonesian Sovereign debt has been largely driven by concerns that budget deficit will continue to widen over the next year, as the new President will look to spend on his policies including his free lunch program.

- The 2Y is 1bp lower at 4.77%, while the 10Y is -0.8bp lower at 5.018%, out-performing moves in the US treasury curve.

- The spread difference between USD Indon & US Treasury yields has been closing for the past few months with the 2Y now 25bps from a low of 73bps, while the 10Y is now 78bps vs yearly lows of 112bps.

- Indonesia sold IDR22.1 Trillion in 5-30yr Bonds, and IDR6.54 Trillion in 7-91D Bills the past week

- Cross market moves, the USD/IDR is 0.20% lower, the JCI is 0.10% lower while US Tsys are 0.5bp higher across the curve

- Foreign Investors have largely been better sellers of Indonesian bonds over the past 20-days as the average daily flow currently sit at -$40.3m, while the longer term 200-day average sits at $4.34m

- Looking Ahead: S&P Global Indonesia PMI Mfg & CPI is due on Friday

ASIA FX: IDR Lags Firmer Asia FX, China PMIs Out Tomorrow

Most USD/Asia pairs are lower in the first part of Thursday trade. IDR is the exception, with weaker portfolio flows and BI rhetoric presenting headwinds today. CNH gains have been limited, while THB and won have rallied, albeit remaining within recent ranges. Tomorrow the focus will be on China official PMIs for Feb, along with South Korean trade data.

- USD/CNH drifted sub 7.2100 amidst stronger yen levels and a better onshore equity backdrop. There has been no follow through though. We are back to 7.2115 this afternoon, only marginally stronger in CNH terms. Volatility remains low for CNH, and USD/CNY onshore has edged down from the 7.2000 level.

- 1 month USD/KRW is lower, last near 1331, around 0.25% stronger in won terms. We remain within recent ranges though. Onshore equities are weaker after yesterday's outperformance. The firmer yen backdrop has likely helped at the margins. Tomorrow onshore markets are shut, but we still get Feb trade figures. Markets expect export growth to step down, with the LNY timing a factor.

- USD/IDR spot has drifted higher in the first part of Thursday trade. We were last near 15730, which is around 0.30% weaker in IDR terms. The 1 month NDF is also higher, last tracking at 15745/50, which is slightly above Wednesday highs. Earlier Feb highs in the 1 month NDF rested just above 15800. Portfolio flows remain a headwind for IDR. We saw close to flat net equity flows yesterday, while bond outflows were on Tuesday. Foreign investors' holdings of local bonds have fallen since late Feb. Bi Deputy Governor Juda Agung was on the wires today stating that the economy needs a rate cut to boost growth, but the BI can't adjust rates yet, given global conditions (BBG).

- USD/THB is back sub 36.00, the pair last near 35.92, around 0.35% stronger in THB terms. Once again we have seen selling interest in the pair above 36.00. IP growth for Jan was slightly better than expected but still contracted for the 16th straight month. Later on Jan BoP/trade figures are due.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/02/2024 | 0700/0800 | ** |  | DE | Retail Sales |

| 29/02/2024 | 0700/0800 | ** |  | SE | Retail Sales |

| 29/02/2024 | 0700/0800 | *** | | SE | GDP |

| 29/02/2024 | 0745/0845 | *** |  | FR | GDP (f) |

| 29/02/2024 | 0745/0845 | ** | | FR | Consumer Spending |

| 29/02/2024 | 0745/0845 | *** | | FR | HICP (p) |

| 29/02/2024 | 0745/0845 | ** | | FR | PPI |

| 29/02/2024 | 0800/0900 | *** |  | ES | HICP (p) |

| 29/02/2024 | 0800/0900 | ** |  | CH | KOF Economic Barometer |

| 29/02/2024 | 0800/0900 | *** | | CH | GDP |

| 29/02/2024 | 0855/0955 | ** | | DE | Unemployment |

| 29/02/2024 | 0900/1000 | *** | | DE | North Rhine Westphalia CPI |

| 29/02/2024 | 0900/1000 | *** | | DE | Bavaria CPI |

| 29/02/2024 | 0930/0930 | ** |  | UK | BOE M4 |

| 29/02/2024 | 0930/0930 | ** | | UK | BOE Lending to Individuals |

| 29/02/2024 | 1300/1400 | *** | | DE | HICP (p) |

| 29/02/2024 | 1330/0830 | *** |  | US | Jobless Claims |

| 29/02/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 29/02/2024 | 1330/0830 | *** |  | CA | GDP - Canadian Economic Accounts |

| 29/02/2024 | 1330/0830 | *** | | CA | Gross Domestic Product by Industry |

| 29/02/2024 | 1330/0830 | *** | | CA | CA GDP by Industry and GDP Canadian Economic Accounts Combined |

| 29/02/2024 | 1330/0830 | ** | | US | Personal Income and Consumption |

| 29/02/2024 | 1445/0945 | *** | | US | MNI Chicago PMI |

| 29/02/2024 | 1500/1000 | ** | | US | NAR Pending Home Sales |

| 29/02/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 29/02/2024 | 1550/1050 | | US | Atlanta Fed's Raphael Bostic | |

| 29/02/2024 | 1600/1100 | | US | Chicago Fed's Austan Goolsbee | |

| 29/02/2024 | 1600/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 29/02/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 29/02/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 29/02/2024 | 1815/1315 | | US | Cleveland Fed's Loretta Mester | |

| 01/03/2024 | 2200/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

| 01/03/2024 | 2330/0830 | * |  | JP | labor forcer survey |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.