Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

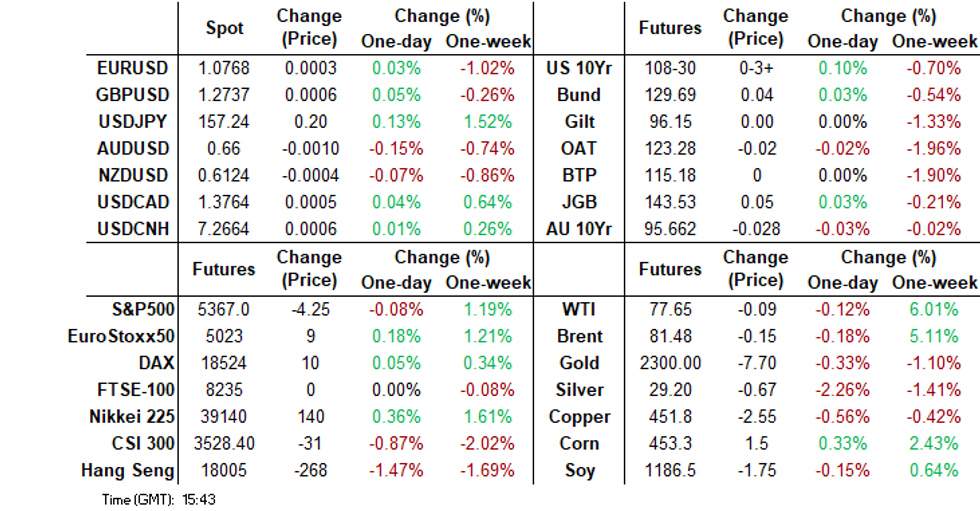

- US Treasury futures have edged slightly higher today, ahead of key event risks on Wednesday. The USD has mostly stayed on the front foot, although sits off recent highs.

- Regional equity sentiment has been weighed by weakness in China and Hong Kong markets, as they returned from a long weekend. Tourism spending and property market concerns weighed. USD/CNY rose to fresh highs for 2024, but the pace of yuan depreciation remains very modest. Iron ore also fell to fresh multi week lows.

- In Australia, the May NAB business survey showed further deterioration in conditions and confidence.

- Later there are UK employment & wage data and US NFIB small business optimism for May. The ECB’s Lane, Buch and Elderson speak.

MARKETS

US TSYS: Tsys Futures Edge Higher, Ranges Tight Ahead Of FOMC & CPI This Week

- Treasury futures have edged slightly higher today trading near session's best and overnight highs. TU is +00+ at 101-28⅞, while TY is + 04 at 109-06+.

- Volumes are on the low side with: TU 24k, FV 34k & TY 63k

- Tsys Flow: 1500 Block Likely Buyer of FVU4 at 106-01¼

- Looking at TYU4 technical levels, initial support is at 109-02 (Jun 10 lows), with the 108-27+(Jun 3 lows) the next target. While to the upside initial resistance is at 110-21 (June 7 highs), a break here would see a test of 110-27+ (1.00 proj of the Apr 25 - May 16 - 29 price swing)

- Cash treasuries yields opened the session 0.5bp higher, the 2y is -1.1bps at 4.87%, while the 10y is -1.8bps at 4.449%

- Looking ahead: NFIB Small Business Optimism, FOMC Begins Two-Day Meeting, 10y Bond Auction

JGBS: Richer Across Benchmarks, Ranges Narrow, PPI & BoJ Rinban Operations Tomorrow

JGB futures are holding in positive territory, +10 compared to settlement levels.

- Outside of the previously outlined M2 & M3 Money Stock, there hasn't been much in the way of domestic drivers to flag. May Machine Tool Orders are due soon along with a Liquidity Enhancement Auction covering OTR 5-15.5-year JGBs.

- Reuters poll: 63% of economists predict the BoJ will decide to start reducing the size of bond buying at the June meeting (up from 41% in the May poll). Also, 92% of economists expect the BoJ to hike the interest rate to at least 0.20% by the end of 2024 (up from 88% in May).

- Cash US tsys are 1-2bps richer in today’s Asia-Pac session.

- Investors now keenly await two key events on Wednesday: the latest US CPI data and the latest thoughts from Federal Reserve Chairman Jerome Powell following the FOMC Decision.

- Cash JGBs are richer across benchmarks, with yields flat to 2bps richer. The benchmark 10-year yield is 1.9bps lower at 1.025% versus the cycle high of 1.101%.

- The swaps curve has bull-flattened, with rates flat to 1.3bps lower. Swap spreads are mixed.

- Tomorrow, the local calendar will see PPI data alongside BoJ Rinban Operations covering 1-10-year and 25-year+ JGBs.

AUSSIE BONDS: Off Cheaps, Narrow Ranges, Focus On Wednesday’s US CPI & FOMC

In roll-impacted dealings, ACGBs (YM -0.4 & XM -1.3) are little changed and off early session cheaps after resuming trading following yesterday’s holiday.

- Outside of the previously outlined NAB business survey, there hasn't been much in the way of domestic drivers to flag.

- Cash US tsys are 1-2bps richer in today’s Asia-Pac session as investors keenly await two key events on Wednesday: the latest US CPI data and the latest thoughts from Federal Reserve Chairman Jerome Powell following the FOMC Decision.

- A Bloomberg survey showed that 41% of economists expect the central bank to signal two cuts, while an equal percentage forecast either one cut or none at all.

- Cash ACGBs are 7-9bps higher than Friday’s close and well above session cheaps, with the AU-US 10-year yield differential at -14bps.

- Swap rates are 6-8bps higher, with EFPs tighter and the 3s10s curve steeper.

- The bills strip is little changed after giving up the early bear-steepening.

- RBA-dated OIS pricing is 4-7bps firmer for meetings beyond September, with early 2025 leading. 5bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty, ahead of the Employment Report and CBA Household Spending data on Thursday.

AUSTRALIAN DATA: Business Activity Weakening But Cost/Price Pressures Worrying

The May NAB business survey showed further deterioration in conditions and confidence. They fell one point to +6, lowest since January 2022, and 5 points to -3, the first negative since November 2023, respectively. Despite the survey showing slower business activity, price and cost measures picked up which NAB pointed out is consistent with the return of inflation to target being “gradual and uneven”. The RBA believes that supply and demand are not yet in balance and this survey is in line with that view.

Australia NAB business survey

Source: MNI - Market News/Refinitiv

- There has been no progress on the inflation side in 2024, which is likely to concern the RBA. On the cost side, labour costs rose 2.3% in the 3 months to May (Apr 1.5%) and purchase costs rose 1.9% (1.3%). Despite tough retail conditions, retail prices rose 1.6% in the 3 months to May (April 1.0%) and final product prices 1.1% (0.8%).

Source: MNI - Market News/Refinitiv

- Business conditions are now below the series’ long-run average with consumer-related sectors particularly soft. Components were mixed with trading and profitability both down 3 points but employment up 3 points and above the series average. Capacity utilisation remains elevated picking up to 83.3%.

- Forward-looking orders rose 1 point but were still negative and below average at -6. Inventories rose 2 points to 4.6, highest since July 2023, which may weigh on orders going forward.

NZGBS: Closed On A Positive Note, US Tsys Richen In Today’s Asia-Pac Session

NZGBs closed near the session’s best levels, flat to 1bp richer across benchmarks. With the domestic calendar light, the move away from the morning’s cheaps was linked to a 1-2bps richening in US tsys across benchmarks in today’s Asia-Pac session.

- US investors now keenly await two key events on Wednesday: the latest US CPI data and the latest thoughts from Federal Reserve Chairman Jerome Powell following the FOMC Decision.

- The Federal Reserve is widely expected to keep borrowing costs steady for the seventh consecutive meeting.

- Consumer spending is likely to be weak this year as households temper their spending to cover higher mortgage costs and purchase necessities, the Treasury Dept. says in a Fortnightly Economic Update (per BBG).

- Swap rates closed 3-4bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 2-4bps softer for meetings beyond October. A cumulative 23bps of easing is priced by year-end.

- The local calendar will see Net Migration tomorrow, ahead of Card Spending data on Thursday.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 3% Apr-29 bond, NZ$200mn of the 2% May-32 bond and NZ$50mn of the 2.75% Apr-37 bond.

FOREX: Dollar Firmer, But Off Highs, A$ Weighed By Softer China Equities

The USD is off earlier highs, the BBDXY last just above 1264.3, only marginally above end NY levels from Monday.

- Regional equity sentiment is mostly negative with returning China and Hong Kong markets close to the weakest in the region. Tourism spending concerns and housing developments weighing.

- This hurt A$ sentiment. AUD/USD got to 0.6591, but now sits back around 0.6600. Recent lows under 0.6580 remain intact. Iron ore prices remain under pressure, the active SGX contract back to the $104/ton handle.

- On the data front, Australia's NAB business survey showed a further deterioration in conditions and confidence. However, it also showed price and cost measures picked up. NZD/USD is down slightly last near 0.6120.

- USD/JPY got to highs of 157.33, but we now sit slightly lows, back near 157.25. We had money supply data, which didn't move sentiment. A Reuters survey ahead of this Friday's BOJ decision showed 61% of economists expect bond buying to be reduced at the meeting, up from the 41% polled previously.

- In the cross asset space, US yields sit lower, off around 1-2bps across the key benchmarks. Gold and oil sit off Monday highs.

- Later there are UK employment & wage data and US NFIB small business optimism for May. The ECB’s Lane, Buch and Elderson speak.

ASIA STOCKS: HK & China Equites Lower, State Council Looks To Stabilize Housing

Hong Kong and China stocks opened lower on Tuesday after the long weekend break, reflecting a broader sell-off across Asia. Chinese tourism-related stocks faced pressure as Citigroup reported weak travel demand during the recent three-day holiday. Despite some growth in domestic travel traffic and revenues, average spending per traveler remained subdued compared to pre-pandemic levels. Tech stocks are lower following Apples recent AI event.

- Hong Kong equities are lower today, HSTech Index is down 1.24%, while the Mainland Property Index is down 2% and the HS Property Index is down 2.60%, the HSI is down 1.70%

- China onshore equities are mixed today, the CSI300 Real Estate Index is down 0.20%, small-cap indices are lower with the CSI1000 is up 0.15% the CSI2000 is unchanged, while the CSI300 is down 1.20%.

- In the property space, Builder Dexin China is facing court-ordered liquidation in Hong Kong following a winding-up case, initiated by China Construction Bank due to the nonpayment of $350 million in senior notes. Despite receiving approval from scheme creditors in May 2023, Dexin failed to restructure in line with the plan, leading to the court's decision. The State council has urged officials to keep formulating new policies that will help absorb existing housing stocks and stabilize markets, per BBG.

- China plans to increase fiscal spending in the latter part of the year by issuing 920 billion yuan ($127 billion) in ultra-long special sovereign bonds between June and November, alongside the acceleration of local government special bond issuance, aiming to strengthen its economic recovery.

- Banks are likely to lower deposit rates due to shrinking net interest margins, prompting investors to shift focus to short-term government bonds amid expectations of further policy easing by the PBoC. This move aims to deter corporations from seeking higher returns by depositing low-cost credit into accounts with better interest rates, especially as substantial deposits have recently flowed into wealth management products for enhanced yields.

- (MNI) China Press Digest June 11: Housing, Economy, Tourism (See link)

- Looking ahead: China PPI & CPI are due out tomorrow

ASIA PAC STOCKS: Asian Equities Mixed, Market Cautious Ahead Of FOMC & BoJ This Week

Asian equities had a mixed performance today, Japanese & South Korean stocks are up, driven by higher tech shares following gains in the US, with the Philadelphia SE Semiconductor Index hitting records highs on Monday. Conversely, Australian stocks were down, impacted by falls in mining and real estate sectors after a public holiday. Overall, investors across the region are cautious ahead of the policy decisions by the Federal Reserve and Bank Of Japan later this week.

- Japanese stocks opened trading near session best and have since given up about half of those gains. The technology sector led the gains, inspired by the Philadelphia Stock Exchange Semiconductor Index reaching a record high. The Topix index increased up 0.14%, supported by resource shares benefiting from rising crude oil prices, with companies like ENEOS Holdings and Inpex among the gainers, while the Nikkei 225 is up 0.40%. Investors are cautiously optimistic, awaiting significant economic events later in the week, including the Federal Reserve meeting, the US consumer price index report, and the Bank of Japan policy decision.

- South Korean stocks are higher today. This uptick follows overnight gains on Wall Street, driven by investor caution ahead of the upcoming FOMC meeting and US inflation data. Large caps showed mixed performance, with Samsung Electronics and SK hynix experiencing slight declines, while Hyundai Motor and Kia Motors advanced. Despite the positive start, investors remain wary of potential volatility stemming from US macroeconomic developments and ongoing political uncertainty in Europe. The Kospi is up 0.25%.

- Taiwan equities are slightly higher today, although shares of Taiwanese Apple suppliers dropped following disappointment over Apple's annual conference, which did not improve the outlook for iPhone shipments this year. Focus this week will turn to Taiwan rate decision on Thursday. The Taiex is currently trading up 0.10%.

- Australia equities are lower today, led by declines in mining and real estate stocks following Monday’s holiday closure. Investors are now awaiting this week’s Australian jobs report, along with the Federal Reserve decision and US inflation data later this week. The ASX200 is down 1.35%

- Elsewhere in SEA, New Zealand Equities are 0.15% higher, Indonesian equities are 0.14% lower, Singapore & Malaysian equities are 0.25% lower, Philippines equities are unchanged, while Indian equities continue their moves higher and now trade back of pre-election highs.

Asian Equity Flows Remain Mixed, India See Inflows Post Election

- South Korean equities edged lower on Monday, and ended two days of solid inflows with a small -$90m outflow, the past 5 trading sessions has still netted a total inflow of just under $1b. The 5-day average is $196m, now above the 20 day average of -$30m and the longer-term trend at $140m.

- Thailand equities made new yearly lows on Monday, foreign investors continue to sell equities as we now have marked the 13th straight session of selling for a total outflow of $666m with $209m of that coming in the past 5 sessions. The 5-day average is now -$42m, below both the 20-day average at -$27m and the 100-day average at -$24m.

- Indonesian equities have now also marked 13 straight sessions of selling from foreign investors, with the past 5 session seeing a net outflow of $147m. The JCI did trade slightly higher on Monday, although we still trade below 7,000. The 5-day average is now -$29.50m, the 20-day average at -$35.5m and the 100-day average at -$4m.

- Philippines equities were lower on Monday, flows recently have been largely mixed with the past 5 trading sessions have seen a net outflow of -$28m. The 5-day average is -$6m, below the 20-day average at -$10m and the 100-day average at -$5m.

- Indian equities are now trading back above pre-election levels, we ended three days of heavy outflows on Friday with an inflow of $641m, with the past 5 trading sessions have seen a net outflow of $1.38b. The 5-day average is now -$277m, 20-day average is -$147m, both below the 100-day average at $10.75m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -89 | 982 | 14289 |

| Taiwan (USDmn) ** | 0 | -65 | 2545 |

| India (USDmn)* | 642 | -1387 | -4149 |

| Indonesia (USDmn) | -18 | -18 | -497 |

| Thailand (USDmn) | -44 | -209 | -2490 |

| Malaysia (USDmn) * | 40 | 10 | -46 |

| Philippines (USDmn) | -3 | -28.6 | -462 |

| Total | 528 | -716 | 9189 |

| * Data Up To Jun 7 | |||

| **Public Holiday |

OIL: Crude Holds Onto Gains Ahead Of OPEC & EIA Monthly Reports Later Today

After Monday’s strong surge, oil prices are holding onto most of those gains and are only slightly lower during APAC trading today. WTI is down 0.1% to $77.65/bbl, off the intraday low of $77.55. Brent is 0.2% lower at $81.47/bbl after a low of $81.37. The benchmark has traded briefly above $82 yesterday. Crude is range trading ahead of key events this week. The USD index is up around 0.1%.

- There are a number of events for oil markets this week. Later today OPEC and the US EIA publish their monthly reports including the outlook with the IEA scheduled for Wednesday. Today also sees US API inventory data. Wednesday’s Fed decision will also be important as it will shape the US demand outlook for energy products.

- Crude rallied on Monday as traders bought the lows after the market flashed oversold following OPEC’s decision at the start of the month to reduce output cuts from October. Subsequent Saudi statements that the plan can be changed if needed have also supported the market. But the demand outlook remains uncertain with Saudi exports to China to be down for a third consecutive month in July and the outlook for the US driving season uncertain.

- Russia reduced its output in May but it still remains above what it has promised OPEC+, according to Bloomberg. It said at the June OPEC+ meeting it would make further efforts to achieve target.

- Later there are UK employment & wage data and US NFIB small business optimism for May. The ECB’s Lane, Buch and Elderson speak.

GOLD: Rebounds On Monday After Friday’s Collapse

Gold is trading 0.3% lower in the Asia-Pacific session, following a 0.7% rise to $2310.88 on Monday. Monday's increase came after a 3% decline on Friday, driven by stronger-than-expected US employment data.

- Investors now keenly await two key events on Wednesday: the latest US CPI data and the latest thoughts from Federal Reserve Chairman Jerome Powell following the FOMC Decision.

- The Federal Reserve is widely expected to keep borrowing costs steady for the seventh consecutive meeting.

- A Bloomberg survey showed 41% of economists expect the central bank to signal two cuts, while an equal percentage forecast either one cut or none at all.

- According to MNI’s technicals team, last week’s sharp sell-off in gold reinforced a short-term bearish theme. The yellow metal has cleared support around the 50-day EMA, at $2,313.5, opening $2,277.4, the May 3 low. Initial resistance to watch is $2,387.8, Friday’s high.

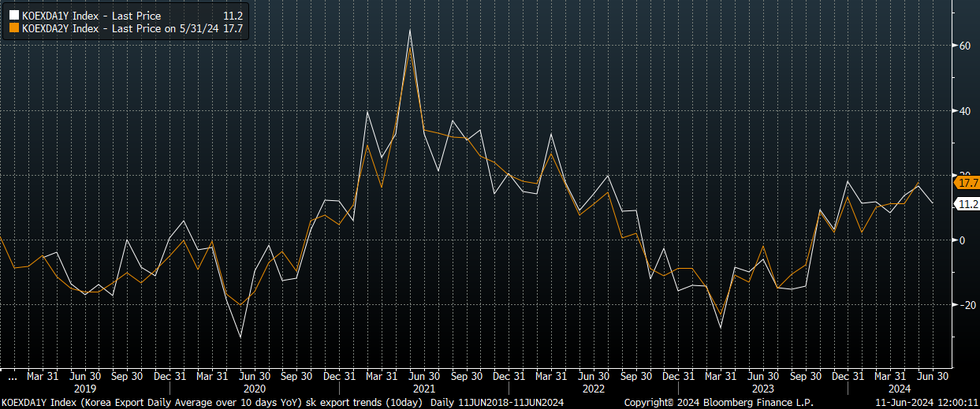

SOUTH KOREA DATA: First 10-days Export Growth Eases, April Current A/C Deficit Due To Dividend Outflows

Earlier data showed South Korea's first 10-days of June trade figures with softer headline results. Exports fell -4.7% in y/y terms, while imports were down -7.4% y/y. The trade position was in deficit for the first 10-days of the month to the tune of $829mn, although this position tends to improve as the month progresses.

- The weaker headline export result partly reflected day count differences with June last year. Daily average exports were up 11.2% y/y, although this was down from the first days of May figure (16.5%y/y).

- The chart below plots the y/y average daily exports for the first 10-days of the month, along with the 20-day daily average in y/y terms. The 10-day series (the white line on the chart), suggests some flattening in the y/y trend, albeit at positive levels.

- In terms of the detail, chip and oil product exports were positive, but car exports fell -18.9% in the first 10 days of the month. Exports to the US stayed positive (10.2%) but fell to China (-8.5%).

- Overall, we will know more with the 20-day update later in the month.

- Elsewhere, data on the April goods balance showed a lower surplus of just over $5.1bn, against a prior March outcome above $8bn. The current account swung back into deficit in April to -$285mn (March's surplus was $6.93bn).

- Along with lower goods surplus, with saw a sharp outflow on the primary income side, down to a net $5bn swing in terms of investment income, as dividend outflows on foreign holdings of local equities picked up sharply.

Fig 1: South Korea First 10-days Export Growth Eases Slightly In June

Source: MNI - Market News/Bloomberg

BOT: MNI Bank Of Thailand Preview: June 2024: Many Reasons To Wait

- The Bank of Thailand (BoT) meets on June 12 and we expect it to leave rates at 2.5%, where they have been since September 2023, as there has not been anything since the April meeting to drive a dovish shift. Three analysts from 23 on Bloomberg are forecasting a 25bp cut.

- BoT has numerous reasons to remain on hold rather than easing. There is significant uncertainty over the impact of government stimulus and how the global economy will develop, including when the Fed will begin its easing cycle. It is also unlikely to want to be seen as giving in to persistent government pressure to cut rates.

- Also, BoT believes that its policy rate is not holding growth back and thus while it is close to neutral there is little reason to change it. But 2 MPC members voted for rate cuts at the last two meetings and it will be seen as dovish if their number grows.

- See full preview here.

PHILIPPINES DATA: Trade Deficit Widens, Higher Imports Driven By Raw Materials & Capital Goods

The Philippines April trade deficit was wider than forecast. It printed at -$4761mn, versus -$3700mn expected. The deficit is back to late 2023 lows, but we remain above the Q3 2022 trough point at -$6000mn.

- Both exports and imports surprised on the upside relative to expectations. Export growth was +26.4% y/y (+13.0% forecast and -7.3% prior), while imports were +12.6%y/y (versus -2.5% forecast and -17.7% prior).

- The deterioration in the trade deficit comes despite a better terms of trade proxy backdrop (per Citi), although the metric remains in negative territory.

- In terms of the detail, exports rose 1.4% m/m, as a 0.4% rise in manufacturing offset a small fall in electronic exports. In y/y terms export growth is at its highest since 2021, although base effects clearly helped.

- On the import side, we surged 14.7% in m/m terms. Raw material imports surged 28.6% in the month, which was one of the largest contributors.

- Capital good imports and consumer good imports were also up firmly for the second straight month, suggesting some resilience in the domestic demand backdrop.

ASIA FX: Mixed Trends, Spot USD/CNY To Fresh 2024 Highs

USD/Asia trends have been mixed in Tuesday trade to date. In North East Asia we are seeing some softness, while parts of South East Asia are stronger, although gains are quite limited at this stage. Tomorrow the main focus is likely to rest on China's CPI and PPI prints for May. We also have the BoT decision in Thailand, no change is expected.

- USD/CNH has once again found selling interest above 7.2700, although pullbacks have been limited. The pair last tracks near 7.2670 in recent dealings, little changed for the session. Onshore equities have returned from the long weekend, seeing further downside pressure. The CSI 300 is off around 1% at this stage, tourism and property headwinds weighing. Spot USD/CNY has pushed higher to +7.2530, which is fresh highs back to November last year.

- 1 month USD/KRW is firmer, last around 1375, up +0.20%, but we remain within recent ranges for the pair. Onshore equities are higher by +0.40%, while earlier data showed some slowing in early June export momentum, while the April current account slipped back into deficit due to strong equity related dividend outflows.

- Spot USD/TWD has risen 0.40% to 32.40, but the 1 month NDF is little changed. Onshore markets were closed yesterday, so this likely reflects some catch up to recent USD strength. Local equities are flat.

- Spot USD/PHP has edged down from recent highs, last just under 58.70. The pair has been unable to sustain levels beyond 58.80 so far in June. The 20-day EMA remains back near 58.33, while in 2022 upside gains were capped just ahead of 59.00 in spot terms. Earlier we had April trade figures, which showed a noticeably wider than forecast deficit (over -$4.7bn). This remains a headwind for PHP, particularly with a still elevated Fed rate backdrop. Elsewhere comments from BSP Governor Remolona, who was attending a Reuters forum, have crossed. The Governor reiterated that they don't intervene in PHP much, only when the market becomes disorderly and a specific level of PHP is not targeted. The greater concern is sharp moves in the FX rate can impact inflation.

- USD/IDR sits around recent highs, last at 16290/95, little changed for the session. Earlier highs were at 16298. The 1 month NDF is hovering just above 16300, sub earlier June highs of 16365. Comments from a BI official crossed the wires earlier. Edi Susianto, Executive Director for Monetary Management stated the central bank will continue its triple intervention in FX spot (DNDF) and the bond market. USD/IDR levels beyond 16300 are manageable it was added, and that the local currency will get support from exporters dollar supplies (BBG).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/06/2024 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 11/06/2024 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 11/06/2024 | 1100/1300 |  | EU | ECB's Lane chat at Banking and Payments Federation Conference | |

| 11/06/2024 | - | *** |  | CN | Money Supply |

| 11/06/2024 | - | *** | | CN | New Loans |

| 11/06/2024 | - | *** | | CN | Social Financing |

| 11/06/2024 | 1230/0830 | * |  | CA | Building Permits |

| 11/06/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 11/06/2024 | 1400/1000 | * | | US | Services Revenues |

| 11/06/2024 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 11/06/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 11/06/2024 | 1645/1845 | | EU | ECB's Elderson at Annual Banking Supervision Conference | |

| 11/06/2024 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.