Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

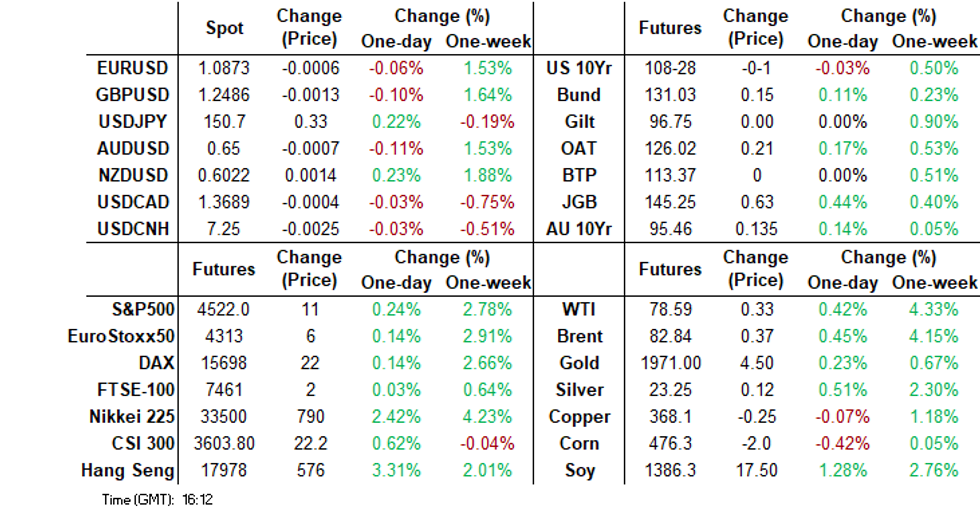

- The risk mood has stayed buoyant in Asia Pac markets post the US CPI miss. US equity futures are higher, with Nasdaq futures within striking distance of 2023 highs. Regional equities have posted strong gains.

- JPY has underperformed in the G10 space marginally, with weaker Q3 GDP not helping. JGB futures spiked but sit comfortably off intra-day highs. US cash tsys sit 1-2bps richer across the major benchmarks, light bull flattening is apparent.

- China October activity data was mixed, while the 1yr MLF rate was held steady. We did have a large (the biggest since Dec 2016) MLF injection though.

- Looking ahead, UK CPI/PPI and euro area IP are out. Later the Fed’s Barr and Barkin speak plus there is US October retail sales, the control group is expected to rise 0.2% m/m, and PPI data.

MARKETS

US TSYS: Marginally Richer In Asia

TYZ3 deals at 108-28+, -0-00+, a 0-07 range has been observed on volume of ~120k.

- Cash tsys sit 1-2bps richer across the major benchmarks, light bull flattening is apparent.

- Tsys have dealt in narrow ranges for the most part in Asia today, the space mostly looked through Japanese and Australian data releases as moves had little follow through.

- Post-CPI highs remain intact for TY. The next target for bulls is 109-20, high from Sep 19. Support comes in at 107-00, low from Nov 13.

- UK CPI provides the highlight in Europe today. Further out we have retail sales, business inventories, PPI and Empire manufacturing. Fedspeak from VC Barr is also due.

JGBS: 10yr JGB Yield Dips Sub 50-day EMA Before Recovering, Futures Off Highs

JGB futures sit off session highs. We were last 145.38, +.76. Earlier highs were at 145.55, which was just shy of mid October highs at 145.63.

- There doesn't appear any macro link to the pause in the uptrend, while US Tsy futures are just off session highs (last 108-28+). Earlier we had positive momentum buoyed by the Q3 miss amid weaker domestic demand.

- These moves have seen JGB yields pare losses. The 10yr yield sits back at 0.79%, up from lows near 0.77% earlier. The is close to the simple 50-day EMA, which we have been below since early July this year. We are still 5-8bps lower in yield terms across the 4-40yr tenors.

- It has been a similar story in the swap space, albeit with lower outright moves. The 10yr swap last near 0.96%.

- On the data front tomorrow, Oct trade figures, core machine orders are due, while weekly investment figures are also out.

- On the supply side, 1yr notes will be sold.

JAPAN DATA: Q3 GDP Falls More than Expected, Domestic Demand Contracts For 2 Straight Qtrs

Q3 Japan GDP surprised on the downside. Q/Q growth was -0.5% (-0.1% forecast and 1.1% prior). Annualized q/q growth was -2.1%, which was the weakest print since Q1 2022. The detail was also quite poor, nominal GDP q/q was flat, against a 0.6% projection (prior was 2.5%).

- Private consumption growth was flat against a 0.3% forecast and -0.9% prior (which was revised down from -0.6%). Business spending was -0.6%, against a 0.1% forecast and -1.0% prior.

- Inventories were also a drag -0.3% and net exports -0.1%, although both were close to expectations.

- Domestic demand was -0.4% q/q, against -0.7% in Q2. Weakness was evident across household consumption and private business investment.

AUSSIE BONDS: Marginally Extend Early Gains, Oct Employment Due Tomorrow

ACGBs sit 11-14bps richer across the major benchmarks, the belly is marginally outperforming. XM (+0.1500) and YM (+0.120) have ticked higher through the session.

- The early bid seen after the post-CPI richening in Tsys spillover into the wider space held through the session with ACGBs ticking marginally higher in the afternoon.

- RBA dated futures are steady, a terminal rate of 4.45% is seen in June 24 with ~15bps of cuts by Dec 24.

- There was little reaction to the Australian Q3 Wage Price Index which came in at expectations (1.3% Q/Q).

- Due tomorrow is the October Labour Market Report, the headline unemployment rate is expected to tick higher to 3.7% from 3.6%.

AUSTRALIAN DATA: Inflation & Tight Labour Market Also Drove Higher Q3 Wages

The Q3 WPI came in close to expectations rising 1.3% q/q and 4% y/y after an upwardly-revised 0.9% and 3.6% y/y. Q3 last year rose 0.9% q/q and the difference reflects not only higher minimum award wage increases but also “widespread increases in average hourly wages” with Q3 2023 the highest quarterly rise since the series began in 1997. This was not just because of government decisions but also due to high inflation and the tight labour market. This could become a concern if it continues.

- The WPI excludes bonuses and other one off benefits and so doesn’t truly reflect the impact of the tight labour market and inflation on take home pay. Data in the national accounts on December 6 will help with this as well as including productivity/unit labour cost to gauge the inflationary impact.

- Almost half of private sector jobs saw a Q3 pay increase with the average rise around 5.8% compared with 34% and 3.3% for the public sector. This is seasonal but 46% of private jobs had a rise in Q3 2022 averaging 4.3%, lower than 2023. 40% of Q3 2023 increases were above 4% with 13% above 6%.

Source: MNI - Market News/ABS/SEEK

- Private sector wages rose 1.4% q/q and 4.2% y/y up from 3.9%, which according to the ABS was driven by the Fair Work Commission’s wage review and the 15% rise for aged care workers. It also cites the tight labour market and high inflation being “factored into wage” decisions” as reasons for strong private wage growth.

- Public sector wages continued to underperform rising 0.9% q/q but the annual rate picked up to 3.5% from 3.1% helped by the end of state wage caps.

- Awards, enterprise and individual pay agreements contributed to the rise, especially the latter.

Source: MNI - Market News/ABS

NZGBs: Hold Early Gains

NZGBs have held their early gains through Wednesdays dealing and sit 9-16bps richer across the major benchmarks, the belly leads the bid.

- Spillover from Tuesday's US Tsys rally in lieu of a softer than forecast October CPI print supported the space this morning and the impact lingered through today's session.

- 10 Year NZ US Swap spreads sit at +55bps, we had been as wide as +70bps in the aftermath of the US CPI print.

- RBNZ dated OIS now price a terminal rate of 5.55% in Feb 24 with ~20bps of cuts by Oct24.

- On the wires early in the session Card Spending fell in October 0.3% M/M, the prior read was revised downwards to 0.2% M/M. Net Migration in September was 7,510, the August number was revised higher to 12,350.

- Looking ahead the docket is light tomorrow with just Oct House Sales and Non-Resident Bond Holdings due.

NZ DATA: Household Inflation Expectations Moderate, Good News For RBNZ

One-year household inflation expectations eased further in Q4, just as those for businesses did. The RBNZ said in a research report this year that the mean 1-year measure from households has the closest relationship with inflation. Simple correlations are over 80% with both headline and core. It moderated to 5.5% from 6% whereas the median was steady at 5%. The mean suggests that disinflation should continue in Q4 which is good news for the RBNZ. The next meeting is on November 29 and will include updated forecasts.

- The median perception of current inflation eased 0.2pp to 7% but the mean rose 0.6pp to 10.1%.

- Looking further out, 2-year mean household inflation expectations fell 0.1pp to 3.2% but the median returned to the top of the target band at 3%. Median 5-year expectations remain anchored at the bottom of the band.

- The survey also asks about house prices and a net 56.5% of households expect higher prices up from 30.1% in Q3 and 4.5% in Q1. They are expected to rise 2% in a year after flat expectations for some time and 7% in 5-years. Strong population growth driven by immigration is supporting the housing market.

Source: MNI - Market News/Refinitiv/RBNZ

NZ DATA: Card Spending Weak As Economy Develops As RBNZ Expects

Card spending data showed a second consecutive month of falling expenditure and is pointing to a weak start to Q4 for retailers. October retail spending fell 0.7% m/m after -0.8% to be down 0.9% y/y. The total fell 0.3% after -0.2% for annual growth to be only 1% higher on a year ago down from 3%, weighed down by the retail sector. 3-month momentum is stagnating. Consumption is weak and the economy continues to develop as the RBNZ expects and so rates are likely on hold for now. Next meeting is November 29.

- Services rose 0.5% and non-retail +0.2% m/m. Hospitality spending declined 2.3% y/y.

- Spending on fuel and motor vehicles was positive in October but apparel, consumables and durables all fell.

Source: MNI - Market News/Refinitiv

EQUITIES: Asia Pac Markets All Higher, Nasdaq Futures Closing In On 2023 Highs

Regional equities are a sea of green, post strong US gains in cash trading on Tuesday, as the US CPI miss buoyed risk appetite. Higher beta plays are outperforming in terms of Hong Kong and South Korea. US futures are tracking higher, Eminis last near 4521, +0.22%, not quite above Tuesday highs. Nasdaq futures are +0.28% (moving above Tuesday highs) and within striking distance of 2023 highs just above 16000.

- US yields have tracked down modestly further, following sharp post CPI losses on Tuesday. Market speculation of an end to the US tightening cycle buoying the risk mood.

- The HSI is up 2.83% at the break, with broad based gains. The HSTECH index up 3%, while the mainland properties index is up over 4.25%. Reports from BBG late yesterday of fresh support into China urban redevelopment and affordable housing aiding sentiment.

- Still, the mainland CSI 300 real estate index is only 0.30% higher at the break, the aggregate index 0.67% firmer. Earlier we had a steady 1yr MLF rate but a net 600bn yuan injection (the biggest since Dec 2016). October activity data was mixed, retail sales beating on the upside, but property headwinds weighing on investment.

- Headlines from BBG have also crossed the regulators will cap the OTC derivatives business for securities firms (see this link).

- South Korean markets are up over 2%, the Taiex is +1%. Japan's Nikkei 225 is +2.35% in latest dealings, shrugging off the disappointing Q3 GDP data earlier.

- In SEA, Thailand and Indonesia markets are up over 1.5%. Other markets are up less than 1% at this stage.

FOREX: Dollar Marginally Extends Post-CPI Losses

The Greenback has been pressured through the Asian session, BBDXY has breached its post-CPI lows and is down ~0.1%. However ranges across G-10 do remain narrow. US Tsys Yields are a touch softer and e-minis are up ~0.2%. The PBOC injected the largest amount of cash since 2016 to the banking system which also aided sentiment.

- Kiwi is the strongest performer in the G-10 space, NZD/USD is up ~0.3% and sits at its highest level since 11 Oct. Bulls now look to target the 200-Day EMA ($0.6565).

- AUD/USD pared early losses and sits a touch above the $0.65 handle. Q3 WPI came in as expected and there was little reaction in FX markets. Technically the bull cycle is still in play, resistance comes in at $0.6522 high from Aug 30 and $0.6582 50.0% retracement of Jul 13 - Oct 26 bear leg. Support is at $0.6339 low from Nov 10.

- Yen is marginally pressured after Japan's flash Q3 GDP print was softer than forecast. USD/JPY has trimmed some of yesterday's losses and is up ~0.1% at ¥152.55/60.

- Elsewhere in G-10 the broader USD move has been reflected, most majors are marginally firmer.

- The UK CPI print provides the highlight in Europe today.

OIL: Crude Higher But Demand Outlook Dampening The Market

Oil prices are slightly higher today boosted by slightly-better-than expected China activity data, although the property sector remains weak. Brent is 0.3% higher at $82.69/bbl, but off the intraday high of $82.79. WTI is up 0.2% to $78.42 after a high of $78.54. The USD index is down 0.1%.

- The upside to oil prices from the expectations that the Fed is done following the lower US inflation data was limited by the IEA saying that the market in Q4 won’t be as tight as expected especially due to increased supply. This was less optimistic than the OPEC monthly report on Monday.

- CBA expects Brent to average $85/bbl in Q4 and then $75 by Q2 2024 with the moderation driven by weaker demand.

- Bloomberg reported that US crude stocks rose 1.335mn in the latest week, according to people familiar with the API data. 2 weeks of official EIA inventory data are published later today, which will be key to the supply outlook.

- China’s refined output is down 3% on the September record but volumes are still up about 9% y/y, according to Bloomberg. China is the largest global crude importer but refining margins have been squeezed. Oil demand also fell 2.4% in October due to a weak recovery in air passenger transport and stabilising inventories.

- Later the Fed’s Barr and Barkin speak plus there is US October retail sales, the control group is expected to rise 0.2% m/m, and PPI data. There are also UK CPI/PPI and euro area IP.

GOLD: Bullion Holds Onto Post-CPI Gains, US Retail Sales Later

Gold prices are 0.1% higher during today’s APAC session after rising 0.8% on Tuesday following lower-than-expected US CPI data that resulted in the market pricing in the end of the tightening cycle and more rate cuts for 2024. Bullion is trading around $1966.85/oz, close to the intraday high but still below yesterday’s $1970.94. The USD rose early in the session but is now 0.1% lower.

- Gold prices remain below resistance at $1978.40, November 7 high, as the flight-to-quality war risk premium was unwinding prior to the US inflation data.

- ANZ believes that the lower US CPI read and the subsequent increase in Fed easing expectations may result in increased investment demand for gold. They also think that increased occurrences of global tensions will create structural geopolitical demand for bullion, including from central banks.

- Later the Fed’s Barr and Barkin speak plus there is US October retail sales, the control group is expected to rise 0.2% m/m, and PPI data. There are also UK CPI/PPI and euro area IP.

CHINA DATA: Retail Sales Recovers Further, But Property Drag Remains

China October activity data was slightly better than expected. IP was 4.6% y/y (4.5% was forecast and the prior outcome). Retail sales showed the most impressive beat at +7.6% y/y (7.0% forecast and 5.5% prior). Less upbeat was FAI, slipping to 2.9% ytd y/y, versus 3.1% forecast. Property investment was -9.3% ytd y/y against a -9.1% forecast. Property sales were -3.7% ytd y/y. The jobless rate held steady at 5.0%, in line with forecasts.

- On the IP side, most of the positive shift relative shift came from mining (+2.9% y/y from 1.5% prior) Manufacturing was steady at 5.1% y/y. By product chip production surged 34.5% y/y, but other parts of tech were mixed. Auto manufacturing was +8.5% y/y, led by new-energy vehicles (+27.9% y/y).

- On the retail side, strength was fairly broad based relative to Sep. Restaurants rose to 17.1%y/y from 13.8%, while consumer goods were +6.5% y/y, from 4.6% prior. Automobiles were +11.4% up firmly.

- On the FAI side, private investment remained soft at -0.5% ytd y/y. Infrastructure spending held up at 5.9%.

- Property investment remained weak, with total sales (-4.9% ytd y/y, -3.7% for residential) and new construction (-23.2% ytd y/y) remaining quite depressed and close to recent trends.

- Overall, the data was encouraging from a retail sales standpoint, but offsets are evident in term of continued property related headwinds.

BSP: MNI BSP Preview - November 2023: A Close Call But Likely On Hold

- The recent downside inflation surprise in the Philippines, coupled with less hawkish offshore developments (Fed on hold, US CPI miss) suggests that the BSP can hold steady tomorrow.

- It will be a close call though with risks to the rate outlook still skewed to the upside. The BSP is also still likely to leave a hawkish impression in terms of its commentary and reiterate that it stands ready to act again.

- Click to view the full preview here:

INDONESIA DATA: Trade Surplus Widens To Highest In 6 Months

Indonesia’s October trade surplus widened moderately to $3480mn from $3405mn, the highest in six months, due to export growth improving more than imports. Exports fell 10.4% y/y up from -16.2% the previous month and imports fell 2.4% up from -12.5%, both stronger than expected. The rupiah has strengthened 1.3% versus the dollar today on lower US CPI data. An improving trade position should support the currency over the medium-term.

- The trade data is nominal and so the totals are impacted by price movements, especially for commodities. Indonesia saw export prices fall on the month and year for its main commodities. Coal exports fell -38% y/y, palm oil -33.8% y/y and mining -28.6% y/y. Monthly export growth was driven by shipments of mineral fuels, precious metals, jewellery and footwear.

- YTD non-oil and gas exports fell 12.7% y/y to October due to lower prices but volume growth was positive.

- YTD imports fell 7.8% y/y with capital goods -12.7% but they rose 11.1% y/y for the month of October. Consumer goods rose 3.8% y/y.

Source: MNI - Market News/Refinitiv

ASIA FX: Asia FX Rallies, But Sits Away From Best Levels

USD/Asia pairs are lower across the board, albeit up from session lows. The best performers have been KRW, THB, IDR and MYR. USD/CNH tested early September lows sub 7.2400, but sits higher in latest dealings. Regional equity sentiment has been buoyant, while China's strong 1yr MLF liquidity injection was also notable amid mixed Oct activity figures. Still to come today is India Oct trade figures. Tomorrow, new China home prices are out, along with the BSP decision in the Philippines, no change expected.

- USD/CNH briefly touched lows sub 7.2390 (low at 7.2384), before moving back above 7.2470. This was fresh lows back to early Sep. We last tracked near 7.2450. Onshore equities are off earlier highs as the market continues to digest the early spike in 1yr MLF liquidity and whether it means less rate/RRR cuts going forward. October activity data was mixed, with retail sales better, but property headlines evident elsewhere.

- 1 month USD/KRW got to lows near 1295, but is tracking higher in recent dealings, last near 1298. Spot is still 2.20% firmer for the session. Offshore inflows into local equities have been present. The Kospi sits +2% higher, just off session highs.

- The Rupee has opened dealing on the front foot as participants digest yesterday's US CPI print and the softening in US Tsy Yields. USD/INR prints at 83.06/07 ~0.3% below Monday’s closing levels. On the wires this afternoon is the October Trade Balance, a deficit of $20.4bn is expected. The prior read was $19.37bn deficit.

- The Ringgit is firmer this morning as participants digest yesterday's US CPI print and the downtick in US Tsys Yields. USD/MYR is down ~1.2% last printing at 4.6585/4.6620. Looking ahead; the docket is empty until Friday's Q3 GDP print, a rise of 3.3% Y/Y is expected. Q3 Current Account Balance is also due.

- The SGD NEER (per Goldman Sachs estimates) printed a fresh cycle high this morning as participants digested yesterday's US CPI print before paring gains to sit a touch softer at typing. We are ~0.4% below the top of the band. USD/SGD fell ~1% yesterday, as US Yields fell after a soft CPI print, breaching the 200-Day EMA ($1.3547) and the $1.35 handle. In early trade today we sit close to post-US CPI lows at $1.3480/85.

- USD/THB has fallen sharply, getting to 35.45, before edging back to 35.50 this afternoon. We are above early Nov lows near 35.40. Thailand’s new government is going to persist with its digital wallet handout election promise despite criticisms and fears that it will boost inflation and go against fiscal rules. PM Srettha’s chief of staff Prommin has said that it is important to boost soft economic growth, according to Reuters.

- USD/IDR is up slightly from session lows, last near 15510. Earlier lows were at 15475. Indonesia’s October trade surplus widened moderately to $3480mn from $3405mn, the highest in six months, due to export growth improving more than imports.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/11/2023 | 0700/0700 | *** |  | UK | Consumer inflation report |

| 15/11/2023 | 0700/0700 | *** | | UK | Producer Prices |

| 15/11/2023 | 0745/0845 | *** |  | FR | HICP (f) |

| 15/11/2023 | 0900/1000 | ** |  | IT | Italy Final HICP |

| 15/11/2023 | 1000/1100 | ** |  | EU | Industrial Production |

| 15/11/2023 | 1000/1100 | * | | EU | Trade Balance |

| 15/11/2023 | 1000/1100 | | EU | European Commission Autumn Econ Forecasts | |

| 15/11/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 15/11/2023 | 1330/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 15/11/2023 | 1330/0830 | ** | | CA | Wholesale Trade |

| 15/11/2023 | 1330/0830 | *** | | US | Retail Sales |

| 15/11/2023 | 1330/0830 | *** | | US | PPI |

| 15/11/2023 | 1330/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/11/2023 | 1400/0900 | * | | CA | CREA Existing Home Sales |

| 15/11/2023 | 1430/0930 | | US | Fed Vice Chair Michael Barr | |

| 15/11/2023 | 1500/1000 | * | | US | Business Inventories |

| 15/11/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 15/11/2023 | 1800/1800 | | UK | BOE's Haskel speech at the Resolution foundation | |

| 15/11/2023 | 2030/1530 | | US | Richmond Fed's Tom Barkin |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.