Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- China stocks remain under pressure. The CSI 300 Index off ~0.80%, with the index hitting fresh YTD lows sub 3800. Weaker economic momentum, coupled with US/China tensions remain meaningful headwinds. The Hang Seng China Enterprise Index has now lost 20% from its late Jan highs, thereby moving into bear market territory. These moves helped push USD/CNH to fresh highs today, last tracking near 7.1050. AUD and NZD have faltered in sympathy with the CNH move.

- Elsewhere, after Memorial Day holiday, the cash tsy curve twist flattens with yields lower beyond the 2-year, which is 0.6bp higher. The 2-year had been as much as 3.3bp higher in early Asia-Pac trade.

- Later the European Commission May survey, March US house prices and May US consumer confidence & Dallas Fed manufacturing are released. Also, Fed’s Barkin speaks on monetary policy. US API inventory data prints too.

MARKETS

US TSYS: Futures Richer But Off Bests, Cash Curve Twist Flattens

TYU3 is currently trading at 113-16, +10 from NY closing levels, after reaching Friday’s high at 113-19+.

- After Memorial Day holiday, the cash tsy curve twist flattens with yields lower beyond the 2-year, which is 0.6bp higher. The 2-year had been as much as 3.3bp higher in early Asia-Pac trade.

- Among the benchmarks, the standout performer is the 20-year, which has witnessed a 5.8bp decline, currently yielding at 4.092%. The 10-year.

- With the calendar light in Asia, local participants have been on headlines watch.

JGBS: Futures Stronger, Mid-Range, Heavy Local Calendar Tomorrow

JGB futures sit in the middle of the Tokyo session range, +10 versus settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined comments from BoJ Governor Ueda in parliament regarding BoJ losses from sovereign debt holdings during an exit from monetary easing.

- JGBs slid sharply on Thursday, but the bounce on Friday helped stall any more protracted pullback, although the gap with the next resistance at 149.17 remains, according to MNI’s technical team.

- On the data front, April jobless data printed 2.6% versus expectations of 2.7%, from 2.8% prior. The job-to-applicant ratio printed in line with expectations at 1.32, unchanged from March. The data didn’t appear to have a material impact on the market.

- Cash JGBs are richer across the curve beyond the 1-year zone. The benchmark 10-year yield is 0.4bp lower at 0.438%, below the BoJ's YCC limit of 0.50%.

- The 2-year JGB is slightly richer in post-auction trade after 2-year supply sees solid demand with the low price above dealer expectations, the cover ratio higher and the tail reduced.

- Swap rates are lower across the curve with rates are 0.3-0.8bp lower. Swap spreads are tighter out to the 7-year zone and wider beyond.

- The local calendar sees Retail Sales (Apr), IP (Apr P) and Housing Starts (Apr) tomorrow.

AUSSIE BONDS: Richer, Off Bests, CPI Monthly & RBA Lowe's Testimony Tomorrow

ACGBs sit slightly stronger (YM +2.0 & XM +2.5) but well off Sydney session bests as cash tsys give up some of their early gains in Asia-Pac trade.

- After the Memorial Day holiday, the cash tsy curve has twist flattened with yields lower beyond the 2-year. Among the benchmarks, the standout performer has been the 20-year, which has witnessed a 5.4bp decline, currently yielding at 4.086%.

- Cash ACGBs are 3bp richer with the AU-US 10-year yield differential at -9bp.

- Swap rates are 2-3bp lower with EFPs little changed.

- The bills strip has twist flattened with pricing -2 to +4.

- RBA-dated OIS pricing is 1-3bp softer for meetings beyond September.

- Building approvals fell 8.1% m/m (estimate +2.0%) in April versus revised -1.0% in March. “Total dwellings approved fell to the lowest level since April 2012”, according to the ABS.

- Tomorrow's schedule presents the week's: RBA Governor Lowe's testimony to parliament and the release of April CPI monthly data. Bloomberg consensus expects the annual rate to show a slight increase to 6.4%, with a range of 6.1% to 6.6%, compared to 6.3% in March.

- The local calendar also releases Construction Work Done (Q1), Private Sector Credit (April), and CoreLogic House Prices (May).

- The AOFM plans to sell A$300mn of the 1.75% 21 June 2051 bond tomorrow.

AUSTRALIAN DATA: Home Building Yet To Respond To Housing Shortage

Building approvals in April came in significantly weaker than expected with an 8.1% m/m drop and March revised down to -1.0%. This brought the annual rate down to -24.1% y/y from -17.6%. With demand for housing very high, house prices rising again and rents soaring, the April data is not good news and indicates that the supply of housing has not yet responded to current conditions. While it is negative for the growth outlook, it signals further upside pressure on rents and thus overall inflation.

- While the highly volatile multi-dwelling component sank 16.9% m/m, private houses were down 3.8% after -3.7% the previous month to be 18.6% lower than a year ago.

- At 11594, this was the lowest number of building approvals since April 2012. A concerning result. The weakness was driven by Queensland, Victoria and WA with the other states posting rises.

- The value of residential building work fell across components with only non-residential building rising both on the month and year.

Source: MNI - Market News/ABS

NZGBS: Richer, Outperforms $-Bloc

NZGBs closed at session bests, 6bp richer across benchmarks, as cash US tsys opened richer across the curve beyond the 2-year after yesterday’s Memorial Day holiday.

- NZGBs nonetheless outperformed the $-Bloc with the NZ/US and NZ/AU 10-year yield differentials respectively 2bp and 3bp tighter.

- Swap rates closed 4-6bp lower with implied swap spreads wider.

- RBNZ dated OIS closed 1-7bp softer across meetings with late’23 /early’24 leading.

- Home-building approvals fell 2.6% m/m in April versus a revised +6.6% in March. Standalone house approvals fall 2.1% m/m.

- In a Bloomberg article, ANZ (NZ) expects house prices to start rising in the second half of 2023, several quarters earlier than expected, in response to looser monetary conditions and surging immigration (link).

- The local calendar sees the release of ANZ Business Confidence (May) and CoreLogic House Prices (May). The upcoming May confidence survey is anticipated to reveal a persisting weakness in business sentiment. Nevertheless, the overall economic landscape presents a mixed picture. While retailers and participants in the construction sector are expected to report subdued conditions, businesses operating in service sectors such as hospitality are expected to experience more robust activity levels.

EQUITIES: China Weakness Offsets Positive US Futures

Ongoing China/Hong Kong equity market weakness has cast a shadow over regional bourses today. There are still some pockets of strength but major indices are down. US equity futures have weakened a touch in response to the China moves, but remain in positive territory as US markets re-open from the long weekend later. Eminis were last around 4223/24, still +0.25%. Nasdaq futures were slightly better, last holding +0.40% higher.

- As we noted earlier on-going China related equity market weakness remains a theme. The HSI is off by 1% at the break, while the HS China Enterprise index is down nearly 1%, more than 20% off late Jan highs and hence in bear market territory.

- On-going US/China tensions particularly in the tech space, coupled with economic slowdown fears continue to weigh on broader China sentiment. The CSI 300 is down 0.80% at the break, sitting at fresh YTD lows near 3800. Sentiment may stabilize somewhat after the break.

- The Kospi is tracking higher, last near 2575, +0.65% as markets return from yesterday's holiday, which has seen some catch up. The Taiex is down slightly, -0.25%, along with the Topic, -0.35%, with both indices giving back some of the recent gains.

- In SEA sentiment is mixed, but gains and losses are within the +/-0.50% range.

FOREX: USD/CNH Break Higher Aids USD Recovery

The USD was initially on the back foot, as US cash Tsy yields re-opened with a weaker tone, as the market digests the debt ceiling deal from the weekend. However, after USD/CNH broke to fresh highs above 7.1000, USD indices turned higher, the BBDXY last 1246, versus earlier lows near 1243.40.

- AUD/USD fell from highs near 0.6560 to 0.6510. We sit slightly higher now, last near 0.6520. Apr building approvals data was weaker than expected, but didn't have a lasting impact on sentiment.

- NZD/USD got to fresh lows back to Nov of last year. We printed 0.6030, but like AUD have recovered some ground, last 0.6040. Apr building permits for NZ also showed a pull back.

- JPY has outperformed slightly, the pair last sits at 140.30/35, with a 139.97/140.53 range for the session so far. The risk averse tone in regional equities has helped yen, along with a pullback in US yields.

- EUR/USD sits above 1.0700 for now, while GBP/USD is slightly higher, 1.2355/60.

- Later the European Commission May survey, March US house prices and May US consumer confidence & Dallas Fed manufacturing are released. Also, Fed’s Barkin speaks on monetary policy. US API inventory data prints too.

OIL: Crude Lower As China Demand Fears Resurface

Crude rallied in early APAC trading with WTI reaching a high of $73.36/bbl but has now pulled back to be down on the day driven by weaker equity sentiment across most of the region. China is weak on growth fears and US-China tensions particularly over chips. Fading optimism on a strong rebound in China’s oil demand has been a driver of lacklustre oil price trends. The USD index is up slightly.

- WTI is down 0.4% to around $72.40, just off the intraday low of $72.34. It is still higher than Monday’s low. Brent is down 0.6% to $76.64, also close to the low, and well off the intraday high of $77.59. Both have broken below even number support of $73 and $77 respectively.

- The market remains jittery over demand from China, US rates and supply ahead of the June 3-4 OPEC meeting. Also, the uncertainty is not over yet re the US debt deal, as it still has to pass through both houses of Congress.

- Later the European Commission May survey, March US house prices and May US consumer confidence & Dallas Fed manufacturing are released. Also, Fed’s Barkin speaks on monetary policy. US API inventory data prints too.

GOLD: Hovering At Six-Week Lows

Gold is at 1939.44 (-0.2%) in the Asia-Pacific session, after closing 1943.19 on Monday.

- Gold remained close to its lowest level since mid-March as investors assessed the likelihood of the US debt-ceiling deal being approved and its potential impact on government expenditure.

- President Biden and House Speaker McCarthy expressed confidence that the bipartisan agreement would pass through Congress, with voting anticipated to take place as early as Wednesday.

- Bullion is also confronted with the prospect of additional interest rate hikes from the Federal Reserve. The yield on 2-year tsys has experienced a significant increase in recent weeks, indicating that persistent inflationary pressures may prevent the Federal Reserve from halting its tightening measures.

- In addition, the US dollar remains strong, hovering around a six-week high, further creating headwinds for the precious metal.

CHINA STOCKS: CSI 300 At YTD Lows, HS China Enterprise Index Off 20% from Jan Highs

China stocks remain under pressure. The CSI 300 is down slightly at this stage, off ~0.80%, with the index hitting fresh YTD lows near 3800. We remain above lows late Oct/Early Nov last year (close to 3500), before China exited CZS, but we are more than 10% off late Jan highs. The Shanghai Composite is faring better, but is only modestly above its simple 200 day MA.

- A combination of waning economic momentum, with the best of the recovery impulse now behind us, is certainly a headwind. The Citi China EASI has slumped, now at +16.40, we were +150 back in April, while the market has also started to downgrade China growth expectations for Q2 and 2023 as a whole.

- US-China tensions, which is seeing the US place chip/tech export constraints on China, is the clear other constraint.

- Since mid-May Northbound stock connect outflows have been -22.3bn yuan. YTD inflows are still +172bn yuan for the year, but we are down from a high of 195.6bn yuan.

- The Hang Seng China Enterprise Index is faring worse than mainland shares, with this index off around 20% from late Jan highs, so in bear market territory.

- This may increase the value opportunity, but the market may wish to see a combination of improved data momentum (we get official PMIs tomorrow), reduced tensions with the US and/or greater signs of stimulus from the authorities.

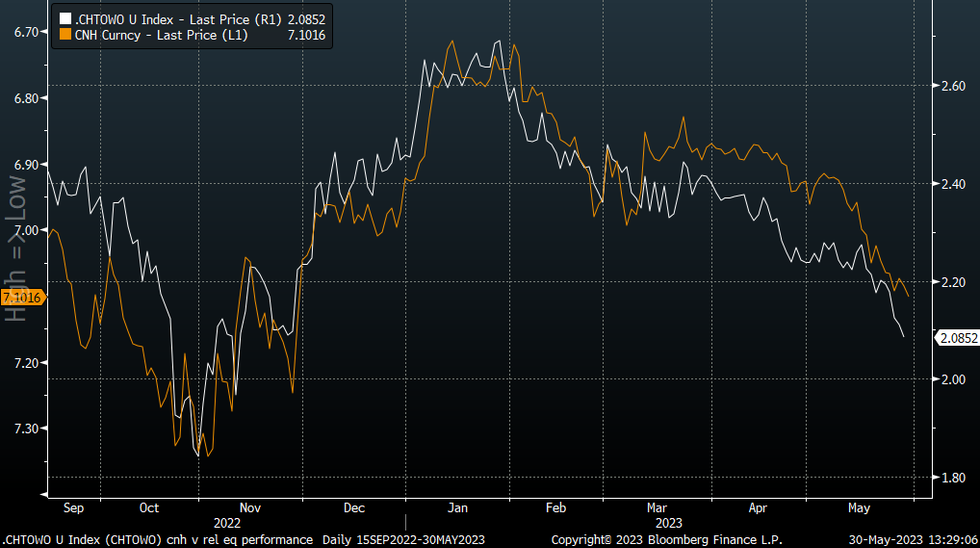

CNH: Fresh Highs In USD/CNH, Testing Above 7.1000

USD/CNH is tracking higher, pushing above 7.1000 in latest dealings. This is through highs from early Friday last week, which reportedly saw state owned banks sell dollars onshore, per Reuters reports. This is fresh highs in the pair going back to Nov last year.

- Renewed weakness in the equity space, with headlines crossing of the HS China Enterprise Index entering bear market territory (-20% from late Jan peaks) is weighing. Onshore equities are also under pressure, the CSI 300 down ~0.60% and threatening a test of the 3800 level.

- As the chart below highlights, relative equity performance between China and the rest of the world has been a good gauge of CNH trends in the past 6 months (note USD/CNH is inverted on the chart). Northbound stock connect flows are modestly negative so far today.

Fig 1: USD/CNH (Inverted) Versus China To World Equity Ratio

Source: MNI - Market News/Bloomberg

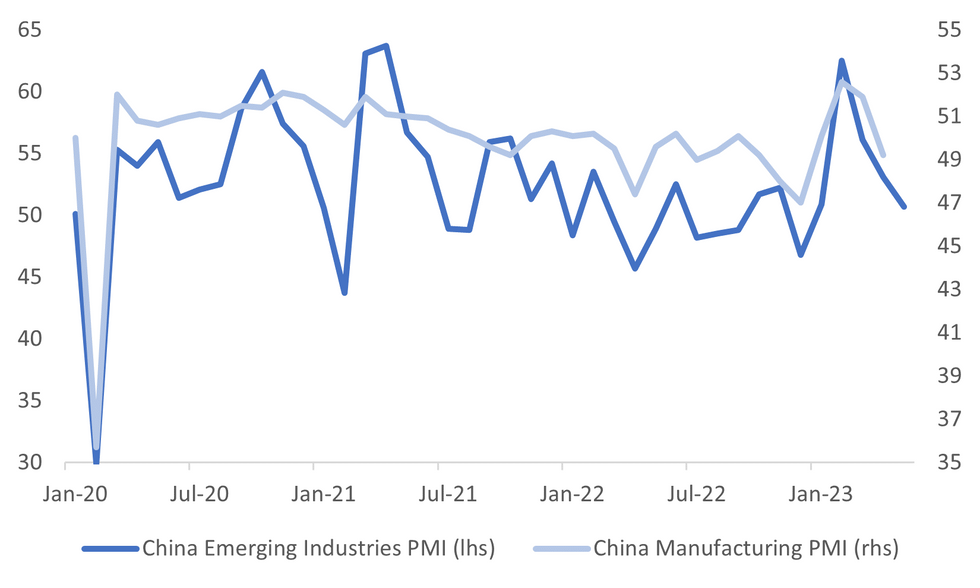

CHINA DATA: Official May PMIs On Tap Tomorrow

A reminder that the official China PMIs for May print tomorrow. The market expects a slight uptick in the manufacturing outcome to 49.5 (from 49.2, range of forecasts is 48.8 to 50.1). On the non-manufacturing or services side the market expects a pull back to 55.2 from 56.4 (range of forecasts is 51.0 to 57.0).

- Interestingly, the emerging industries PMI has already printed for May. It moved down to 50.7 from 53.1 in Apr. The chart below overlays this index against the manufacturing PMI.

- At face value it is arguing for downside risks around the manufacturing PMI, although the correlation between the two series is far from perfect.

Fig 1: China Official Manufacuring PMI Versus Emerging Industries PMI

Source: MNI - Market News/Bloomberg

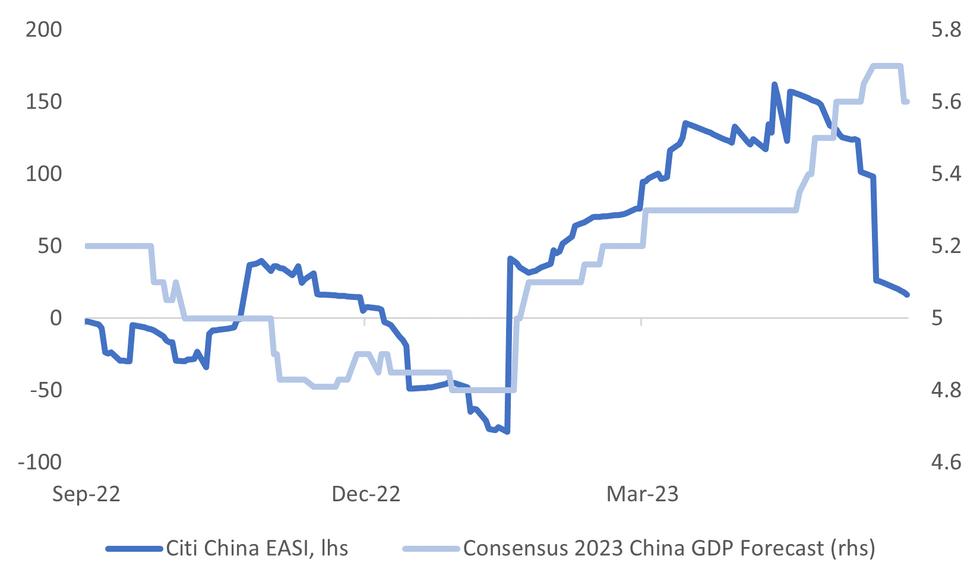

- More broadly, tomorrow's prints will be important for assessing economic momentum in China, particularly the weaker Apr activity data prints and the growth downgrades that followed.

- The second chart below is the Citi China EASI index against the consensus 2023 GDP growth expectation for China.

Fig 2: China 2023 GDP Growth Consensus Forecast Versus Citi China EASI

Source: Citi/MNI - Market News/Bloomberg

BoT: MNI Bank Of Thailand Preview: May 2023: 25bp Hike, Statement Tone Key

- The Bank of Thailand (BoT) is widely expected to hike another 25bp bringing rates to 2% at its May 31 meeting. BoT’s Sethaput has made clear since the March meeting that policy still needs to be normalised. Two analysts surveyed by Bloomberg expect rates to be unchanged though.

- The question is what the outlook for rates will be with many economists forecasting that they will stay at 2% for the rest of the year and into 2024. Any changes to the accompanying statement following the decision will be important for gauging if further tightening is in the pipeline.

- See full preview here.

ASIA FX: Fresh Highs In USD/CNH Weighs On Regional FX Sentiment

Initially, some USD/Asia pairs were weaker, in line with softer US yields and some positive regional equity market trends. However, the USD saw fresh support as USD/CNH broke to fresh highs. Only USD/TWD is down for the session at this stage. Tomorrow the focus is likely to rest on China manufacturing PMIs.

- After breaking above 7.1000, USD/CNH got to a fresh highs of 7.1073. The CNY fixing was neutral, but on-going equity market weakness remains a constraint. The CSI 300 is at fresh YTD lows sub 3800, while the HS China Enterprise Index is in bear market territory, off 20% from Jan highs.

- 1 month USD/KRW traded weaker in the first part of trade, but couldn't sustain lower levels. We got to 1315.75, but now sit back at 1322/23 due to higher USD/CNH levels. Onshore equities are still higher, as markets play catch up after being closed yesterday. The Kospi sits 1% higher and offshore investors have added $473.1mn so far to local shares.

- USD/TWD is still lower for the session, last 30.61/62, but we sit slightly higher from earlier lows around 30.53/54.

- SEA FX is mostly weaker. USD/PHP has rebounded, pushing up to fresh highs near 56.40, +0.40% firmer for the session. This is very close to previous YTD highs. USD/THB has rebounded, back to 34.82, although we remain below yesterday's highs.

- In the high yield space, USD/IDR is relatively steady, last around 14970, while USD/INR is a touch higher, last 82.70/75, but is maintaining a lower beta with respect to moves elsewhere in the region.

Indonesia: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of Indonesian Newspapers and some other major news outlets.

Politics: “Jokowi wants to pair up Ganjar with Prabowo for 2024: Projo” – Jakarta Globe (see here)

- President Jokowi is reported to want Defence Minister Prabowo to run with the PDI-P’s chosen presidential election candidate Ganjar. Prabowo has the support of his party Gerindra to run but has yet to announce formally his candidacy, as he needs support of other parties.

Economy: “Nusantara offers 80-year land titles for industrial use” – Jakarta Globe (see here)

- Nusantara is Indonesia’s planned new capital in East Kalimantan and the government has said that long land title will be granted to enable improve the ease-of-doing business plus compete with Singapore, who only offers 30 years.

Economy: “President Jokowi and ministers discuss Golden Visa Policy” – Antara News (see here)

Business: “Indonesia ready to supply EV batteries to the US: minister” – Antara News (see here)

Trade: “MSMEs must adopt high tech to expand export market: minister” – Antara News (see here)

Trade: “Indonesia commits to increasing trade under AANZFTA: minister” – Antara News (see here)

Tech: “Government imposes zero percent tax on electric vehicles” – Antara News (see here)

SOUTH KOREA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of South Korean Newspapers and some other major news outlets from the past day or so.

ECONOMY: Passengers on Korea-China routes only 13% of pre-pandemic level in Q1 (link)

ECONOMY: S. Korea's household debt to GDP at highest level among 34 economies (link)

MARKETS: Foreign investors return to Korean stock market (link)

MARKETS: Foreign purchases of tech, auto stocks amount to over W16t this year (link)

MARKETS: Retail investors' battery frenzy continues (link)

TECH: Chinese battery makers threaten Korean lead in EU (link)

TECH: Vietnam emerges as major market for Korean chipmakers (link)

TECH: S.Korean chips’ hefty reliance on China, US poses risk to national economy (link)

GEOPOLITICS: China's ban on Micron tests Washington-Seoul alliance (link)

GEOPOLITICS: Japanese warship arrives in S. Korea for multinational WMD-interception naval drill (link)

SOUTH KOREA/NORTH KOREA: S.Korea warns of stern response in case of N.Korea satellite launch (link)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/05/2023 | 0700/0900 | *** |  | ES | HICP (p) |

| 30/05/2023 | 0700/0900 | *** |  | CH | GDP |

| 30/05/2023 | 0700/0900 | ** |  | SE | Economic Tendency Indicator |

| 30/05/2023 | 0700/0900 | * | | CH | KOF Economic Barometer |

| 30/05/2023 | 0800/1000 | ** |  | EU | M3 |

| 30/05/2023 | 0800/1000 | ** |  | IT | PPI |

| 30/05/2023 | 0900/1100 | ** | | EU | EZ Economic Sentiment Indicator |

| 30/05/2023 | 1230/0830 | * |  | CA | Current account |

| 30/05/2023 | 1300/0900 | ** |  | US | S&P Case-Shiller Home Price Index |

| 30/05/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 30/05/2023 | 1300/0900 | ** | | US | FHFA Quarterly Price Index |

| 30/05/2023 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 30/05/2023 | 1430/1030 | ** | | US | Dallas Fed manufacturing survey |

| 30/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 30/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 30/05/2023 | 1700/1300 | | US | Richmond Fed's Tom Barkin | |

| 30/05/2023 | 1700/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.