Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

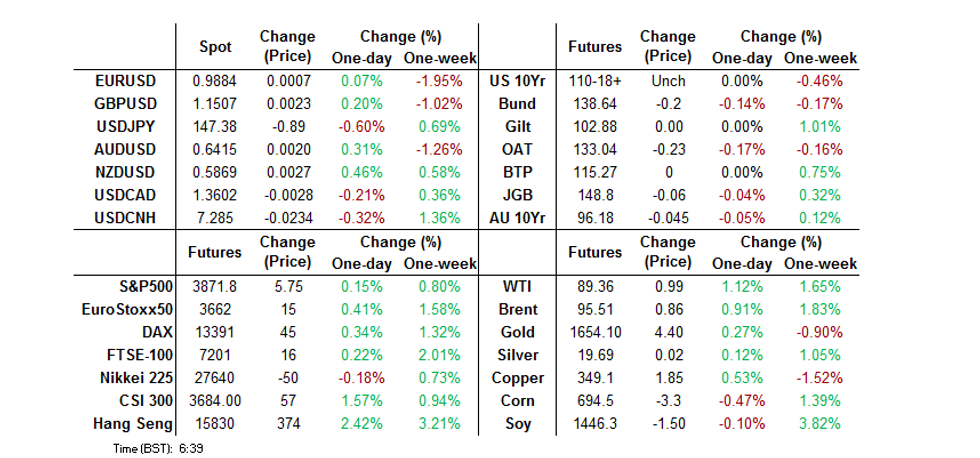

- The major Asia-Pac equity indices were little changed to firmer on Wednesday, with Hong Kong & Chinese equities leading the charge, building on Tuesday’s gains, even after the Chinese government played down any knowledge of the formation of a COVID re-opening committee late on Tuesday (with rumours surrounding that matter deemed the major driver of Tuesday’s move higher).

- The greenback traded on the back foot amid positive risk tone and pre-FOMC positioning. The BBXY index shed 2 figs through the session, with short-end U.S. Tsy yields easing off in a steepening move. E-mini futures crept higher, trimming Tuesday's losses, underpinning positive market sentiment.

- When it comes to scheduled events, Wednesday is all about the Fed's monetary policy decision, with policymakers expected to raise interest rates by 75bp.Outside of Fed Chair Powell's presser, we will hear comments from ECB's Makhlouf, Villeroy & Nagel. U.S. ADP employment change, German jobless rate and manufacturing PMI readings from several European economies will take focus on the data front.

US TSYS: Twist Steepening Pre-FOMC

The cash Tsy curve has twist steepened in Asia Pac hours, with the region seemingly keen to fade Tuesday’s twist flattening impulse, aided by block blow in FV (+5K & +5.75K) & TY futures (-2K).

- An early uptick came alongside a weaker USD and the latest batch of North Korean missile launches.

- The bid then moderated/unwound, dependent on the point of the curve that is being examined, with weakness in Antipodean rates and the longer end of the JGB curve introducing a cross-market element to price action.

- Cash Tsys run 3bp richer to 2bp cheaper, twist steepening (as mentioned above) with a pivot around 10s. TYZ2 has stuck to a fairly limited 0-09 range, last dealing a between its base and midpoint, +0-01 at 110-19, on solid volume of ~!00K.

- Participants are zeroed in on risk events due during Wednesday’s NY session, which will be dominated by the latest FOMC decision (see our preview of that event here) and quarterly Tsy refunding announcement (see our preview of that event here)

JGBS: Steeper With Lack Of Demand Evident In Longer End

Cash JGBs run flat to ~5bp cheaper, with the super-long end struggling despite the presence of BoJ Rinban operations in the 25+-Year zone and even after the U.S. Tsy curve twist flattened on Tuesday.

- Participants may have been exhibiting increased caution ahead of the impending FOMC decision, as yesterday’s cheapening in super long paper extended, with wider FI market flows also eyed.

- Futures were -8 at the bell, with the contract’s overnight low giving way as wider core global FI markets cheapened as Asia-Pac dealing wore on, before the contract corrected from Tokyo lows into the bell.

- Local headline flow saw Finance Minister Suzuki sound a little more worried re: the impact of a weaker JPY, while BoJ Governor Kuroda reiterated the need for the BoJ to persist with its current monetary policy settings, although he did concede that YCC settings may need to be altered at some point down the line.

- BoJ Rinban operations covering 1- to 5- & 25+-Year JGBs had no real impact on the space, with relatively vanilla offer/cover ratios unearthed in the details.

- Looking ahead, Thursday’s local docket will see the latest batch of weekly international securities flow data cross.

AUSSIE BONDS: Weaker On Wednesday

Aussie bonds were seemingly driven by cross-market flows on Wednesday, with an early U.S. Tsy-inspired bid giving way as trans-Tasman impetus from a softer NZGB complex post-NZ labour market data applied pressure, before a second round of cheapening was seen as U.S. Tsys came back from highs.

- Some desks pointed to set up ahead of next week’s ACGB May-34 syndication as a source of pressure, but it is hard to be sure on that front, especially as the curve flattened on the day.

- YM finished -9.0, with XM -4.5.

- Local data was mixed vs. consensus exp., with a lack of meaningful market impetus derived from the housing finance and building approvals prints.

- EFPs were wider all day, but pulled back from extremes, with the 3-/10-Year box steepening a touch.

- Bills were 2-14bp cheaper through the reds at the bell, bear steepening.

- Looking ahead Thursday’s local docket will see final services and composite PMI data from S&P Global, as well the monthly trade balance reading. Elsewhere, RBA’s Kearns, who is Head of the Bank’s Domestic Markets divison, will participate on a panel discussing the topic of “Wholesale Market Conditions and Resilience.”

NZGBS: NZGB Post Data Weakness Extends

NZGBS continued to cheapen in the wake of the release of the domestic labour market report, with the major benchmarks ultimately going out 12-14bp cheaper as the curve bear steepened.

- Swap rates lagged the move in yields resulting in some tightening of swap spreads.

- A reminder that the domestic data saw firmer than expected employment growth and average hour earnings, although the unemployment rate held steady as participation jumped.

- Elsewhere, RBNZ Deputy Governor Hawkesby flagged that the data was in line with the Bank’s own expectations, while highlighting the need to slow demand against the backdrop of a “very hot” labour market.

- RBNZ dated OIS firmed at the margins post data, with ~71bp of tightening now priced for this month’s meeting, while a terminal OCR of ~5.25% is now priced.

- Looking ahead, Thursday’s domestic docket will be headlined by the latest round of NZGB supply (’28, ’33 & ’51 paper will be auctioned).

FOREX: Greenback Heads Into FOMC Meeting On Back Foot, Yen Gains Despite Risk-On Tone

The greenback traded on the back foot amid positive risk tone and pre-FOMC positioning. The BBXY index shed 2 figs through the session, with short-end U.S. Tsy yields easing off in a steepening move. E-mini futures crept higher, trimming Tuesday's losses, underpinning positive market sentiment.

- The yen bucked the risk-on trend which sent other safe havens (USD and CHF) losing altitude. Spot USD/JPY fell 1.20 fig. top-to-bottom, before trimming losses to last trade at Y147.58. U.S./Japan 2-Year spread tightened 3.8bp & 10-Year differential stayed little changed, which may have aided the downswing in USD/JPY.

- Bloomberg cited trader sources attributing sharp yen purchases to the BoJ minutes, which showed that several board members made reference to FX markets at the September meeting. The minutes underscored the central bank's intention to maintain dovish bias, but Governor Kuroda told lawmakers that Japan is no longer in deflation since the launch of the current easing programme.

- High-beta currencies traded on a firmer footing, outperformed only by the yen. The kiwi paced gains in the space, after New Zealand's Q3 employment and wage data smashed expectations, driving a marginal uptick in RBNZ rate-hike pricing.

- Offshore yuan garnered some strength, while holding yesterday's range, amid broader dollar weakness. The PBOC set its USD/CNY reference rate at a new cyclical high and 643 pips below sell-side estimate, while Governor Yi reiterated his pledge to keep the yuan stable.

- When it comes to scheduled events, Wednesday is all about the Fed's monetary policy decision, with policymakers expected to raise interest rates by 75bp.

- Outside of the much awaited Fed Chair Powell's presser, we will hear comments from ECB's Makhlouf, Villeroy & Nagel.

- U.S. ADP employment change, German jobless rate and manufacturing PMI readings from several European economies will take focus on the data front.

FX OPTIONS: Expiries for Nov02 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9700(E1.1bln), $0.9725(E702mln), $0.9800(E1.3bln), $0.9820-25(E702mln), $0.9850-70(E1.1bln), $0.9900(E862mln), $1.0000(E2.4bln)

- USD/JPY: Y150.00($1.0bln)

- GBP/USD: $1.2000-22(Gbp1.3bln)

- EUR/JPY: Y141.10(E738mln)

- AUD/USD: $0.6720(A$1.2bln)

- NZD/USD: $0.6175(N$713mln)

- USD/CNY: Cny7.2500($715mln)

ASIA FX: Pre-FOMC USD Weakness Aids Asia EM FX, Baht Supported By Equity Inflows

The BBG/J.P. Morgan Asia Dollar Index (ADXY) crept higher, consolidating above the 96 figure, as the greenback lost shine across the board. Reflections ahead of the FOMC meeting today came to the fore, while regional participants scrutinised recent signals on the outlook for China's COVID-Zero policies.

- CNH: Greenback weakness helped USD/CNH fall for the second consecutive day, even as the PBOC set its USD/CNY mid-point at a new cyclical high going back to early 2008. Gov Yi spoke at a Hong Kong event, vowing to keep the exchange rate stable.

- KRW: Spot USD/KRW operated above neutral levels as heightened geopolitical risk prevented the South Korean won from strengthening. North Korea fired its largest daily barrage of missiles on record, hitting international waters south of the inter-Korean maritime boundary known as the Northern Limit Line.

- IDR: The rupiah was among the worst performer in the region, after data released Tuesday showed that inflationary pressures in Indonesia eased across headline and core price measures, raising questions about the magnitude of Bank Indonesia's next rate move.

- MYR: The ringgit softened, with USD/MYR refreshing its 24-year highs, ahead of Bank Negara Malaysia's monetary policy decision tomorrow. The local FX space ignored a continued rally in palm oil prices.

- PHP: Spot USD/PHP advanced as onshore markets re-opened after a holiday. The BSP released a statement pointing to the need to smoothen FX moves.

- THB: The baht was among the best performers in emerging Asia amid positive developments in Thai equity markets. Foreign inflows continued to pick up, while the SET index tested its 200-DMA following a breach of the 50-DMA.

EQUITIES: Hong Kong & China Lead The Way, Even After China Plays Down Re-opening Rumours

The major Asia-Pac equity indices were little changed to firmer on Wednesday, with Hong Kong & Chinese equities leading the charge, building on Tuesday’s gains, even after the Chinese government played down any knowledge of the formation of a COVID re-opening committee late on Tuesday (with rumours surrounding that matter deemed the major driver of Tuesday’s move higher).

- News of fresh overt and stealth COVID-related restrictions surrounding some Chinese cities also failed to dent sentiment.

- The Hang Seng was subjected to shortened trading hours owing to adverse weather conditions in Hong Kong, closing 2.6% higher, while the CSI last prints ~1.4% better off.

- Elsewhere, the Nikkei 225 was limited by a firmer JPY, closing around unchanged levels, with the latest North Korea missile launch also doing little to aided sentiment in Japan.

- U.S. equity index futures lodged marginal gains, with the 3 major e-mini contracts last 0.1-0.3% higher, likely benefitting from the uptick in Hong Kong & Chinese equities.

GOLD: Consolidating Tuesday’s Gain Pre-FOMC

Gold has benefitted from the pull lower in our weighted U.S. real yield monitor over the past 24 or so hours, with some intraday volatility in the USD providing les clarity in terms of direction for bullion. This leaves spot gold at $1,650/oz, with Asia-Pac trade limited by the impending U.S. Federal Reserve monetary policy decision.

- The November FOMC meeting is mainly about the message the Fed wants to send about its plans for December. A 4th consecutive 75bp hike is assured this time. A step-down to a 50bp hike at the following meeting looks like the path of least resistance for now - the question is, how strongly does the FOMC seek to express that view.

- In a close call, we expect only limited changes to the Statement - but anticipate that Chair Powell will signal that the Committee is currently eyeing either 50bp or 75bp in December, with the decision to be data-dependent. If there are substantive changes to the Statement, the risks are almost certainly that they lean dovish, with either an overt nod to slowing the pace of increases, or a reference to the impact of cumulative hikes on the economy.

OIL: Prices Supported Ahead Of Fed Meeting

Oil prices posted solid gains during the day with both WTI and Brent up over a percent to around $89.60/bbl and $95.75 respectively on a softer USD ahead of the Fed and hopes that China will reopen.

- US EIA inventory data is published tonight and is expected to show a 200k drawdown of crude after 2.588m build last week (Dow Jones) pointing to further tightness in the market. Gasoline stocks are expected to shrink by 900k. The API reported a 6.5mn crude drawdown and -2.6mn for gasoline in the latest week.

- The US and Saudi Arabia are concerned that Iran may be about to attack not only Saudi Arabia but also Erbil in Iraq, according to Dow Jones.

- Brent contracts continue to signal market tightness.

- The Fed meeting later will be important for gauging the outlook for oil demand. It is expected to raise rates 75bp again.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/11/2022 | 0700/0800 | ** |  | DE | Trade Balance |

| 02/11/2022 | 0815/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 0845/0945 | ** |  | IT | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 0850/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 0855/0955 | ** | | DE | Unemployment |

| 02/11/2022 | 0855/0955 | ** | | DE | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 0900/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 02/11/2022 | 1215/0815 | *** | | US | ADP Employment Report |

| 02/11/2022 | 1400/1000 | ** | | US | housing vacancies |

| 02/11/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 02/11/2022 | 1515/1115 |  | CA | BOC director Ron Morrow speaks on payments supervision | |

| 02/11/2022 | 1800/1400 | *** | | US | FOMC Statement |

| 03/11/2022 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.