Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- PBoC bucks wider expectations and leaves MLF rate unchanged.

- 2-Year JGB yields taps 0%.

- ECB-speak, Swedish CPI and Canadian data provide the points of interest on Monday with U.S. markets closed for MLK day.

US TSYS: Futures Slightly Cheaper, Cash Bonds Closed For MLK Day

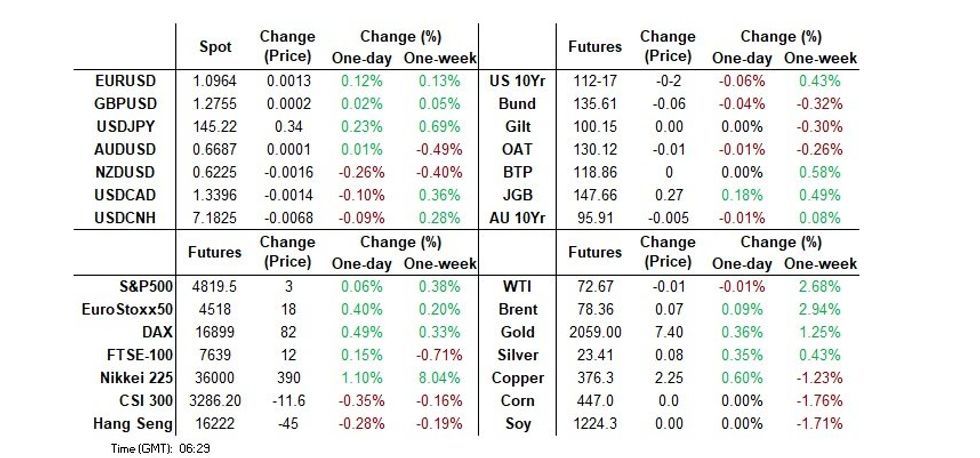

TYH4 is trading at 112-16+, -0-02 from NY closing levels.

- Meaningful newsflow has been light in today’s Asia-Pac session.

- A reminder cash tsys are closed today for observance of the Martin Luther King Day public holiday. For FI futures: Globex will close at 1300ET on Monday and re-open at 1800ET, preceding normal session hours on Tuesday.

JGBS: Richer With 10Y Leading The Rally, 5Y Supply Tomorrow

JGB futures are richer and at session highs, +33 compared to the settlement levels.

- There hasn’t been much in the way of domestic data drivers to flag, outside of the previously outlined M2 & M3 Money Stock data. Machine Tool Orders data is due later.

- US tsy futures are slightly weaker in today’s Asia-Pac session, with newsflow light. TYH4 is dealing at 112-15+, -0-03+ compared to NY’s close on Friday. Cash US tsys are closed today for observance of the Martin Luther King Day public holiday.

- The cash JGBs are richer across benchmarks, with yields 1-5bps lower. The benchmark 10-year yield is 4.6bps lower at 0.561%, outperforming the curve. 5-year supply is due tomorrow.

- The 2-year JGB yield is at 0.1% after falling to 0% briefly for the first time since July. The move has been driven by the view that the BoJ is unlikely to tweak its monetary policy at a meeting next week following a powerful earthquake on Jan. 1.

- The results of the BoJ’s Rinban Operations covering 1-3-year and 5-25-year JGBs showed negative spreads but higher cover ratios, apart from the 10-25-year bucket. As expected, the results generated some slight support, particularly for the longer end of the curve, in the Tokyo afternoon session.

- Swap rates are lower across maturities, with swap spreads wider.

AUSSIE BONDS: Narrow Ranges, US Tsy Futures Slightly Cheaper

ACGBs (YM +2.0 & XM -0.5) have maintained their twist-steepening throughout the Sydney session after dealing with relatively narrow ranges. Today’s domestic data drop failed to provide a market-moving catalyst.

- In addition to the previously outlined inflation gauge and job ads data, CBA household spending data showed a 3.1% y/y rise (-3.9% m/m) in December.

- US tsy futures are slightly weaker in today’s Asia-Pac session, with newsflow light. Cash US tsys are closed today for observance of the Martin Luther King Day public holiday.

- Cash ACGBs have twist-steepened too, yields 2bps lower to 1bp higher. The AU-US 10-year yield differential is 4bps wider at +14bps.

- Swap rates are flat to 3bps lower, with the 3s10s curve steeper.

- The bills strip is richer, with pricing flat to +4, reds leading.

- RBA-dated OIS pricing is 1-2bps softer across meetings beyond February, with December leading.

- Tomorrow, the local calendar sees Westpac Consumer Confidence.

- On Wednesday, the AOFM plans to sell A$800mn of the 3.50% 21 December 2034.

- ICYMI, TCV has launched a new A$-denominated Sep-38 fixed-rate benchmark bond, UBS said. Bond initial price guidance of EFP+115-119bps, equating to ACGB 3.75% 21 Apr-37 +103.4-107.4bps. Pricing is expected to take place tomorrow.

NZGBS: Richer, Narrow Ranges, Cash US Tsys Are Closed For MLK Day

NZGBs closed 3-5bps richer across benchmarks after dealing with relatively narrow ranges in today’s local session. With the domestic data calendar empty and cash US tsys closed for observance of the Martin Luther King Day public holiday, the local market has held the morning’s levels.

- US tsy futures are slightly weaker in today’s Asia-Pac session, with newsflow light. A reminder that Globex will close at 1300ET on Monday and re-open at 1800ET, preceding normal session hours on Tuesday.

- Swap rates closed 2-6bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 1-5bps softer across meetings, with July/August leading. A cumulative 98bps of easing is priced by year-end.

- Tomorrow, the local calendar sees the NZIER Business Opinion Survey.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 0.25% May-28 bond, NZ$175mn of the 3.5% Apr-33 bond and NZ$50mn of the 2.75% Apr-37 bond.

EQUITIES: Expected Fed Cuts Support Markets, Tech Weighs On Some Indices

MNI (Australia) - Equity markets are mixed during APAC trading with the MSCI APEX 50 down 0.2% but the S&P and Nasdaq futures are flat to moderately higher as UST futures have range traded. The outlook for Fed easing provided some support but tech weighed on other indices.

- Japan’s markets continued to climb higher following the US with the Topix up 1.2% and the Nikkei +1%.

- The unexpected hold of China’s 1-year MLF rate at 2.5% didn’t rattle China’s indices with the CSI 300 up 0.1% and the property component +0.7%. But the Hang Seng is 0.3% lower with the tech index down 2%. Korea is another market that was driven down by tech with the KOSDAQ 1.3% lower and the overall KOSPI -0.3%.

- Despite the tech trends, Taiwan’s TAIEX rose 0.3% supported by the weekend’s election, according to Bloomberg.

- Australia’s ASX 200 closed flat with stronger energy stocks outweighed by weaker miners, but the NZX 50 sank 0.7%.

- India’s Nifty 50 has rallied 0.6% so far in today’s trading.

- ASEAN is also mixed with the Philippines PSEi up 0.8% and Singapore’s Straits Times +0.3% but the Jakarta Comp down 0.2% and the SE Thai flat%.

- US markets are either closed or have shortened trading hours today due to the Martin Luther King holiday. The World Economic Forum is running in Davos. In terms of data, there are euro area IP and trade.

GOLD: Stronger On Back Of PPI Data & Middle East Tensions

Gold is 0.3% higher in the Asia-Pac session, after closing 1.0% higher at $2049.06 on Friday.

- The move higher was assisted by lower-than-expected PPI data. US producer prices decreased 0.1% in December compared with expectations for a 0.1% increase. This saw the annual rate for headline and core prices at 1% and 1.8% respectively. Ex Food and Energy were lower than expected as well. The PPI report more than offset the impact of Thursday's slightly hotter CPI.

- Short-end US Treasuries held richer into Friday’s close, indicative of higher projected rate cuts through mid-2024: March 2024 chance of a rate cut was 77% w/ cumulative of -20.9bp at 5.120%, May 2024 was fully pricing in 25bp cut now, cumulative -50.1bp at 4.828%. June 2024 has cumulative -80.4bp at 4.525%.

- Some haven demand also provided support for US Treasuries amid increased worries over tensions in the Red Sea after the U.S. and U.K. attacked Houthi targets in Yemen.

OIL: Crude Holds Gains On Middle East Tensions, But Supply/Demand Remains Focus

Crude has held onto Friday’s gains during APAC trading today with WTI up 0.1% to $72.74/bbl and Brent +0.2% to $78.44/bbl. The benchmarks are off their intraday highs of $72.91 and $78.63 respectively. Further reports of Houthi attacks on Red Sea shipping provided support but oil markets remain concerned regarding excess supply and slowing demand. The USD index is flat.

- Houthi attacks on Red Sea shipping and the US/UK retaliation on Friday have increased concerns that the conflict could spread outside of Israel/Gaza and potentially become region-wide. While this is not the base case, crude remains on edge re any further escalation of the situation as the region accounts for around a third of global oil, according to Bloomberg. Iran supports Hamas and the Houthis.

- Three firms are redirecting tankers away from the southern Red Sea accounting for 350 vessels, according to Bloomberg.

- China unexpectedly left the 1-year MLF rate unchanged when a 10bp cut had been forecast. This development didn’t weigh on prices, even though China is the world’s largest crude importer.

- US markets are either closed or have shortened trading hours today due to the Martin Luther King holiday. The World Economic Forum is running in Davos. In terms of data, there is euro area IP and trade.

FOREX: USD Flat, A$ & Yen Stronger

With the US mainly closed for the Martin Luther King holiday and little news flow, there haven’t been big moves in currency markets today. The BBDXY USD index is off its intraday low but flat on the day at 1224.40 with UST futures in narrow ranges. The unexpected hold of the China’s 1-year MLF rate at 2.5% hasn’t rattled FX either with USDCNY also flat at 7.17.

- USDJPY is 0.2% higher to 145.15, just off the intraday high of 145.23. It has spent most of the session above 145. Continued Middle East tensions haven’t driven any further safe haven flows into yen today. Oil prices are only slightly higher.

- AUDUSD is up 0.1% in APAC trading to 0.6692. It broke above 67c briefly earlier to make a high of 0.6704, still well below resistance of 0.6771, but has now given up most of those gains.

- NZDUSD is 0.2% lower to 0.6230 after a high of 0.6251 early in the session. As a result, aussie has gained 0.25% against kiwi and it hovering just above 1.0740.

- The World Economic Forum is running in Davos and the Eurogroup meeting is taking place. In terms of data, there is euro area IP and trade.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/01/2024 | 0700/0800 | *** |  | SE | Inflation Report |

| 15/01/2024 | 0900/1000 |  | DE | German Annual 2023 GDP First Estimate | |

| 15/01/2024 | 0900/1000 |  | EU | ECB's Lagarde and Cipollone in Eurogroup meeting | |

| 15/01/2024 | 1000/1100 | ** | | EU | Industrial Production |

| 15/01/2024 | 1000/1100 | * | | EU | Trade Balance |

| 15/01/2024 | 1330/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 15/01/2024 | 1330/0830 | ** | | CA | Wholesale Trade |

| 15/01/2024 | 1400/0900 | * | | CA | CREA Existing Home Sales |

| 15/01/2024 | 1530/1030 | ** | | CA | BOC Business Outlook Survey |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.