Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

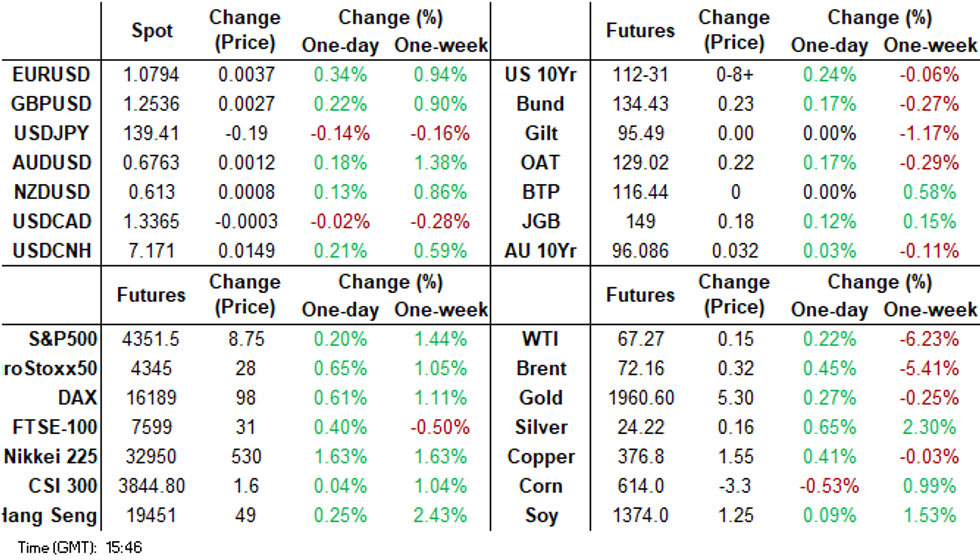

- USD/CNH surged post the PBoC's 7-day reverse repo cut by 10bps (to 1.90%). The first cut since August last year. We got just above 7.1780 before selling interest emerged. Dips back to the low 7.1600 region were supported, we last tracked above 7.1700. Onshore yields are weaker across the board. The 5yr NDIRS is down by 6.5bps to 2.375%, fresh lows back to Sep last year. Today's PBoC move has seen expectations rise for a 1 yr MLF cut on Thursday. Technically, there doesn't appear much preventing a move towards 7.2000 in USD/CNH.

- US Cash tsys sit 1-3bps richer across the major benchmarks, the curve has bull steepened. Spillover from the China move was evident. Weaker yields are weighing on broader USD sentiment (ex CNH). The BBDXY last under 1233.

- Later today the focus is on US May CPI, which could impact the Fed outcome, and the headline is expected to ease to 4.1% and core to 5.2%. There is also NFIB small business optimism and real earnings for May. In the UK, labour market/wages data print.

MARKETS

US TSYS: Marginally Richer In Asia, CPI In View

TYU3 deals at 113-20, +0-08+, with a 0-08+ range observed on volume of ~47k.

- Cash tsys sit 1-3bps richer across the major benchmarks, the curve has bull steepened.

- Tsys firmed to session highs on spillover from the PBOC cutting the 7-Day Repo Rate 10bps to 1.90%.

- Gains were marginally pared as there was no follow through on the move higher and tsys dealt in narrow ranges for the remainder of the Asian session. Perhaps the proximity to today's CPI print limited activity.

- FOMC dated OIS remain stable, ~6bps of hikes are priced in for Wednesday's meeting with a terminal rate of ~5.30% in July.

- Today's docket is headlined by May CPI print, the MNI preview is here. We also have the latest 30-Year supply.

JGBS: Futures Sit Slightly Off Session Highs

JBU3 sits slightly below session highs, last 148.29, +.20. Session highs came in at 148.35, which is just below mid-May highs for the Sep futures contract at 148.41. We have seen positive spill over post China's PBoC 7-day repo cut. This has also been evident in terms of US futures, with TYU3 last at 113-19, +07. US cash Tsys yields are lower across the board.

- For Japan Cash bonds we have seen a decent move lower in yield at the back end, 40yr off 3.5bps, 30yr nearly 2.5bps. The 10yr yield has ticked sub 0.42% in yield terms.

- Swap rates are lower across the board, the 10yr down nearly 2bps to 0.5775%.

- Earlier data on Q2 BSI industry activity showed a bounce from Q1 weakness, but this, along with an appearance in parliament by BoJ Governor Ueda hasn't shifted the sentiment needle today.

- Japan accepted ¥496.6bn for enhanced liquidity bonds (bids were ¥1426.5bn), leaving the bid to cover ratio at 2.87, down slightly from the prior result (3.10).

AUSSIE BONDS: Curve Flattens On Tuesday

ACGB's sit 1bp cheaper to 6bps richer across the major benchmarks, the curve has twist flattened piboting on 5s.

- XM (+0.03) and YM (+0.01) are a touch firmer, early gains extended as spillover from PBOC's cut to the 7-Day Repo Rate to 1.90%. The move didnt follow through and narrow ranges were observed for the remainder of the session.

- RBA dated OIS have been stable today, a terminal rate of 4.47% is seen in November.

- NAB has lifted their RBA terminal rate forecast to 4.6% from 4.35%, the bank now sees 25bp hikes in July and August.

- The CBA household spending intentions (HSI) rose 3.1% m/m and 4.7% y/y. Westpac Consumer Confidence rose 0.2% to 79.2. NAB Business Confidence fell to -4 from 0 in May and Business Conditions fell to 8 from 14.

- The local data docket is empty tomorrow.

AUSTRALIAN DATA: Consumer Sentiment Depressed, More Nervous On Jobs

Westpac consumer sentiment rose 0.2% m/m in June to hold steady at the depressed level of 79.2. It remains close to the March trough of 78.5. The further rate hike in June weighed on confidence post the decision but the minimum wage announcement helped to prevent it from falling on the month. The survey was done between June 5 and 9 and included RBA Lowe’s speech the day after the meeting (see MNI: Lowe: Persistent Services Inflation "Here", Tightening Not Done).

- Sentiment before the June 6 RBA meeting had risen to 89 from 79 due to the minimum wage announcement but then sank to 72.6 after the rate hike. With only a third of households holding a mortgage, the main concern is elevated inflation rather than rates. Inflation had a 62% recall amongst those surveyed and rates 27.6%, and news was considered negative.78% after the June meeting expected rates to rise in the next year up from 74% in May. Westpac expects another 25bp in July.

- Westpac noted that confidence sustained at these low levels hasn’t been seen since the late 1980s/ early 1990s recession. The outlook for the next year remained weak with “family finances next 12 months” falling 2.1% m/m and “economic outlook” almost unchanged after both falling sharply in May. “Time to buy a major household item” fell 6.5%.

- Consumers have become less confident regarding the labour market with unemployment expectations rising 6.6% m/m and 31.8% higher than its September 2022 trough.

- House price expectations were not impacted by the June 6 rate hike and rose 1.7% m/m to be well above the historical average. Rising house prices are worrying the RBA. But “time to buy a dwelling” fell 5.7% m/m due to higher prices and rising rates – this series has been weak since March 2022.

Source: MNI - Market News/Refinitiv/ABS

AUSTRALIAN DATA: NAB Survey Pointing To Slower Growth & Employment

NAB business conditions fell to 8.2 in May from 14.8, the lowest since January 2022 but still slightly above average. Business confidence fell to -3.7 from +0.3. NAB noted that there were “worrying signs of a slowing in activity”. All the activity components were lower while some of the price/cost measures rose slightly. A scenario of weak growth but stubborn inflation would make RBA decision making particularly difficult.

- The leading forward orders component fell to -4.8 from +0.9, the lowest since Covid-impacted July 2021. This signals that demand and business conditions are likely to slow further. The orders weakness was driven by the consumer sector.

- Trading conditions fell to 14.4 from 21.7, profitability to 6.6 from 11.8 and employment to 4.2 from 10.7. The latter with rising Westpac unemployment expectations are pointing to a turn in the labour market. Conditions were weaker across industries, but confidence rose in mining, manufacturing and transport & utilities in May.

- Exports were also down but remained just in positive territory. Exporters sales fell to 0.2 from 3.7.

Source: MNI - Market News/Refinitiv

Australia Employment y/y% vs NAB employment

Source: MNI - Market News/Refinitiv/ABS

AUSTRALIAN DATA: Cost Pressures Rising For Businesses

Despite the fall in NAB May business confidence and conditions, capacity utilisation remained elevated although easing gently. This is consistent with the increase in all of the survey’s price/cost measures except retail prices. Rising cost pressures are going to be something to watch to see if they’re persistent.

- Labour costs rose to 2.2% from 1.9% at the same time that the employment component fell 6.5 points. This component is likely to rise further over the coming months as agreements are negotiated and minimum award wages rise 5.75% on July 1.

- It was not just labour costs that rose for businesses but also purchase costs which were up 2.5% from 2.2% in April and 2% in March. As a result the price of finished products began to edge higher rising 1.3% from 1.1%, and may go further over the coming months. Retail price inflation fell further to 1.3% from 1.5%, as the sector has been the first to be hit by falling demand and is discounting to attract customers.

Source: MNI - Market News/Refinitiv

NZGBs: Marginally Firmer On Tuesday

NZGBs have finished dealing on Tuesday 1-3bps richer across the major benchmarks, the curve has bull flattened.

- Global FI richened on spillover from the PBOC cutting the 7-day repo cut 10bps to 1.90%. NZGBs firmed off session lows on the move but remained within daily ranges.

- RBNZ dated OIS pricing has eased a touch today, a terminal rate of 5.62% is now seen in October.

- Apr Estimated Net Migration rose 5785, the prior read was a touch higher to 13,176.

- On the wires early tomorrow we have Q1 Balance of Payments and May Food Prices.

FOREX: USD Tracking Lower Ahead Of CPI Print

The USD index hits high not long after the PBoC announced a 10bps cut to its 7-day repo rate. We got to 1235.35, but we now sit back near 1233.40, a little over 0.10% below NY closing levels. In the cross asset space, we have seen weaker US yields post the PBoC announcement (2yr yield back to 4.55%, off 2.5bps), while US equity futures have firmed, as have regional equities. These trends have weighed on the USD.

- AUD/USD fell in sympathy with weaker CNH levels post the PBoC announcement, but support was evident sub 0.6740, the pair back above 0.6760 now, +0.15% for the session. NAB raised its terminal rate forecast to 4.60% for the RBA, but we saw generally depressed consumer confidence prints, along with weaker NAB business confidence and conditions reads. Commodity prices are firmer, but haven't seen much positive follow post the China rate news.

- NZD/USD is a touch higher, but is lagging the A$ at the margins, the pair last just above 0.6125.

- USD/JPY is down slightly versus NY closing levels, last under 139.45. Better Q2 business conditions and Ueda comments not shifting sentiment much.

- EUR/USD is around 0.20% firmer, last near 1.0780, although this pair has been able to sustain breaches above the 1.0780 handle in recent sessions.

- Looking ahead, we have the UK labor market survey and German ZEW, but the main focus will be on US CPI out later.

EQUITIES: Tech Plays Still Outperforming, PBoC Rate Cuts Helps At The Margins

Regional equities are mostly tracking higher. The China PBoC 7-day cut providing some support, but other themes have been evident. Japan stocks once again leading the move higher. Tech related indices have also risen, following strong gains in Monday US trade. US futures are firmer, Eminis last near 4400, +0.20%, while Nasdaq futures continue to outperform (+0.40%).

- Japan bourses have benefited from positive tech spill over from Monday US trade, while SoftBank rose as much as 7.7% on reports that its Arm chip unit could receive investment from Intel.

- At the break, the HSI is up 0.40%, just below session highs, the tech sub index is +2.10%. China's CSI 300 is only +0.12% higher, with little aggregate benefit from the 7-day repo cut by the PBoC. Still, the real estate sub index is slightly firmer at +0.43%.

- The Taiex is up +1.60%, following the strong +3.3% rally in the US SOX on Monday. The Kospi is +0.40%, but the Kosdaq is doing better at +1.35%.

- In SEA trends are more mixed, Malaysia stocks off by 0.45%, while Indonesia stocks are struggling to stay in positive territory. Some carry over from weaker energy/crude palm oil prices may be weighing.

OIL: Crude Consolidates Ahead Of US CPI Data

Oil prices have stopped their slide during the APAC session ahead of the US CPI May data later, helped by lower US yields, USD index and the surprise cut in the PBoC’s 7-day repo rate. Brent is 0.7% higher to $72.31/bbl, close to the intraday high of $72.39, and WTI +0.5% to $67.45, following a high of $67.53.

- Crude markets continue to worry about the demand outlook but today seem to be hoping that US inflation will moderate and that the Fed will pause (see MNI’s Fed Preview here). Continued robust Russian supply and futures spreads signalling plentiful output have also weighed on prices. The market has looked through Saudi Arabia’s latest production cut scheduled for July.

- Later today the focus is on US May CPI (see MNI’s US CPI Preview here), which could impact the Fed outcome, and the headline is expected to ease to 4.1% and core to 5.2%. There is also API crude and product inventory data. NFIB small business optimism and real earnings for May are released. In the UK, labour market/wages data print.

GOLD: Bullion Higher Ahead Of US CPI

Gold has unwound Monday’s 0.2% loss during APAC trading today and is currently around $1961.27 helped by the lower US yields and USD index. It hasn’t traded above $2000/oz since mid-May, as sticky inflation outcomes have increased risks of further policy tightening. Today’s US CPI and Wednesday’s FOMC meeting will be key to bullion movements.

- Bullion reached an intraday high today of $1962.22 after a low of $1956.02. It remains clear of support at $1932.20, the May 31 low. Hopes of a pause in Fed tightening have put a floor under prices. Economists expect the FOMC to hold rates on June 14 (see MNI’s Fed Preview here).

- Later today the focus is on US May CPI (see MNI’s US CPI Preview here), which could impact the Fed outcome, and the headline is expected to ease to 4.1% and core to 5.2%. There is also NFIB small business optimism and real earnings for May. In the UK, labour market/wages data print.

ASIA FX: Fresh Highs For USD/CNH, But No Negative Spillover To The Rest OF the Region

USD/CNH hit fresh highs post the PBoC rate cut. However, there was very little negative spill over to the rest of the region. Indeed USD/KRW slumped further to fresh multi-month lows. Tomorrow, we get South Korea trade prices early, while India wholesale prices print later on. We are also still waiting for China May credit/new lending figures.

- USD/CNH surged post the PBoC's 7-day reverse repo cut by 10bps (to 1.90%). The first cut since August last year. We got just above 7.1780 before selling interest emerged. Dips back to the low 7.1600 region were supported, we last tracked above 7.1700. Onshore yields are weaker across the board, 2yr bond yield -2.5bps to 2.07%, the 10yr to 2.64%, -4bps. The 5yr NDIRS is down by 6.5bps to 2.375%, fresh lows back to Sep last year. Today's PBoC move has seen expectations rise for a 1 yr MLF cut on Thursday. Technically, there doesn't appear much preventing a move towards 7.2000 in USD/CNH.

- USD/KRW 1 month NDF has broken down through 1270 today, last slightly above session lows, with the pair near 1271. We saw a brief rise to 1283 after China cut the 7-day repo rate but this was used as a selling opportunity by the market. The won continues to ride the better tech equity sentiment wave. Offshore invesors have bought $105.5mn of local shares so far today, while the Kospi is up 0.40% at this stage. There is also some domestic optimism that the economy will be better in the second half.

- USD/INR prints at 82.41/44, little changed from yesterday's closing levels in early dealing. On the wires late yesterday May CPI printed at 4.25% Y/Y below the expected 4.31% Y/Y ticking lower from 4.70% in April. This was the lowest CPI print since April 2021. Industrial Production for April also crossed, the measure rose 4.2% Y/Y greater than the expected 1.4%. Looking ahead the domestic data calendar is empty today, however tomorrow May Wholesale Prices will cross. A fall of 2.50% Y/Y is expected.

- The SGD NEER (per Goldman Sachs estimates) has firmed in early dealing printing a fresh cycle high. We now sit ~0.5% below the upper end of the band. USD/SGD is a touch lower this morning, the pair firmed in the wake of the PBOC's 7 day repo rate cut, but resistance was seen ahead of the 20-Day EMA and gains were pared. Data-wise the only data of note this week is May Export data on Friday. Non-Oil Domestic Exports are estimated to have fallen 1.9% M/M and 7.7% Y/Y. Electronic Exports are also due, there is no estimate for the release.

- The Ringgit printed its weakest level since 26 May this morning before marginally paring losses. USD/MYR sits at 4.6200/30 up ~0.1% marginally paring gains after printing a high of 4.6283. Technically the uptrend remains in place, bulls now target the high from 26 May at 4.6398. Bears first look to break the 20-Day EMA (4.5812) to turn the tide. A reminder that the domestic data calendar is empty for the remainder of the week.

SOUTH KOREA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of South Korean Newspapers and some other major news outlets from the past day or so.

ECONOMY: Economy likely to rebound in 2nd half: KDI (Link)

ECONOMY: Has the Korean Economy Bottomed Out? (Link)

ECONOMY: Credit risks loom as tightening cycle nears end (Link)

ECONOMY: Rate freeze fuels optimism for housing market's recovery (Link)

FLOWS: Corporate tax cut spurs Korean companies to reshore funds to invest at home (Link)

MARKETS: Foreigners betting on Korean market despite record high interest gap (Link)

TECH: TSMC Surpasses 60% Market Share; Samsung Foundry Drops to 12% (Link)

FISCAL: Drastic tax reforms unlikely in July due to fiscal deficit (Link)

BOK: Bank of Korea chief to regulate the vulnerable non-banking sector (Link)

GEOPOLITICS: S. Korea, U.S. agree to additional efforts to cut off funds to N. Korea's weapons programs: nuclear envoy (Link)

INDONESIA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of Indonesian Newspapers and some other major news outlets.

Economy: “Indonesia’s consumer confidence index rises to 128.3 in May” – Jakarta Globe (see here)

- Consumer confidence rose 2.2 points in April driven by improving economic conditions and expectations. Better job prospects and current income were behind the improvement. Business activity expectations rose 7.8 points in May.

Economy: “Indonesian retail sales likely rise in May” – MT Newswires (see here)

- BI said that retail sales were flat on the year in May after 1.5% y/y in April.

Economy: “ASEAN promising investment destination for S Korea: ASEAN BAC Chair” – Antara News (see here)

Economy: “Agriculture sector cushioned Indonesia’s economy amid pandemic: Govt” – Antara News (see here)

Economy: “EU didn’t consult with Indonesia before passing EUDR: minister” – Jakarta Globe (see here)

Government: “Minister ensures Nusantara capital city development goes accordingly” – Antara News (see here)

Politics: “PDI-P, Democrats warm up for high-level negotiations” – Jakarta Globe (see here)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/06/2023 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 13/06/2023 | 0600/0800 | *** |  | DE | HICP (f) |

| 13/06/2023 | 0600/0800 | ** |  | NO | Norway GDP |

| 13/06/2023 | 0700/0900 | *** |  | ES | HICP (f) |

| 13/06/2023 | 0900/1100 | *** | | DE | ZEW Current Conditions Index |

| 13/06/2023 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 13/06/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 13/06/2023 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 13/06/2023 | 1230/0830 | *** | | US | CPI |

| 13/06/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 13/06/2023 | 1400/1500 | | UK | BOE Bailey Lords Economic Affairs Committee Hearing | |

| 13/06/2023 | 1400/1000 | | US | Treasury Secretary Janet Yellen | |

| 13/06/2023 | 1500/1600 | | UK | BOE Dhingra Speech at Manchester Metropolitan University | |

| 13/06/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 13/06/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 13/06/2023 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.