Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- US TSY futures firmed in early trade as local participants digested the Hamas/Israel conflict which began over the weekend. TYZ3 was unable to sustain its rally above resistance at 107-14 (Oct 3 high), gains were pared, and ranges were narrow with little follow through on moves for the remainder of the session. Cash tsys are closed today due to the observance of the Columbus Day holiday.

- Oil prices rose sharply in response to raised tensions in the Middle East. Crude rose over 5% during APAC trading but is now off its intraday highs. There is concern that if hostilities spread to other parts of the region, then oil production could be impacted.

- The other focus point has been the return of China markets after the Golden Holiday week break. At this stage, sentiment is weaker, with the CSI 300 off by nearly 0.60% at the break. Anecdotes around holiday spending were below government estimates, albeit up strongly compared to 2022, while housing activity was also weaker than hoped for (see below for more details).

- Looking ahead, later the Fed’s Logan, Barr and Jefferson speak. There is no data due to the Columbus Day holiday. The ECB’s de Guindos is also scheduled to appear. IMF/World Bank annual meetings take place today and tomorrow.

MARKETS

GLOBAL: Strong Supply Helping Keep Food Prices Down, Rice Lower In October

FAO world food prices fell slightly in September to be down 10.7% y/y from -11.6%. The major categories were mixed with cereals and sugar higher on the month but dairy, meats and oils continuing to fall. The trough in food price deflation as well as energy prices appears to have slowed the pace of disinflation.

- Cereal prices rose 1% m/m but are still down 14.6% y/y. The September increase was driven by rough rice and maize prices but wheat prices fell due to strong supply from Russia. Processed rice prices are down 2% m/m in October to date after rising over 20% between June and September.

- Dairy prices fell for the ninth consecutive month and across all products and are now down 23.9% y/y following 22.4% in August due to lower import demand at a time of ample supply.

- Meat prices fell for the third straight month due to robust supply and they are now down 5% y/y. There has also been weak import demand from China for pork.

- Oil prices fell again and are now down 20.8% y/y due to strong production across varieties.

- In contrast, global sugar prices rose sharply and are now 48.4% higher than a year ago up from 34.1% in August due to a tight market but Brazil’s upcoming plentiful harvest should take some of the pressure off.

Source: MNI - Market News/Refinitiv

GERMANY: German Voters Show Disapproval Of Chancellor’s Coalition

On Sunday there were state elections in the German states of Bavaria and Hesse which account for around a quarter of voters. While local issues are always important, in both states voters appear to have sent a message to Chancellor Scholz and his ruling coalition of the centre-left SPD, Greens and liberal FDP as support fell for all three in both states. Nationwide election are due in around two years.

- Bavaria, the second most populous German state, has been governed by a coalition of the centre-right CSU and the Free Voters (FW) and it looks like that will continue following Sunday’s election with them increasing their share of the vote by 4pp to a combined 52.8%.

- Support for the SPD fell 1.3pp to only 8.4%, the Greens fell 3.2pp to 14.4% and the FDP -2.1pp to 3%. The right-wing AfD polled third with 14.6% up 4.4pp since the 2018 vote. Most states won’t form coalitions with the AfD.

- In Hesse, the incumbent centre-right CDU received more votes than polls had projected rising 7.6pp to 34.6%. Whereas its coalition partner the Greens fell 5pp to 14.8%, but they are also a member of the federal coalition. The AfD did better than expected polling second, the first time in a western German state, with 18.4% of the vote. Support for the other two federal coalition partners the SPD and FDP fell with the former down 4.7pp to 15.1% and the latter -2.5pp to just make the 5% threshold.

- The results mean that a continuation of the current CDU/Greens coalition is likely but a deal with the SPD is also possible. The risk is that both of the possible junior partners may not want to be in government given their poor results.

US TSYS: Futures Firmer In Asia, Cash Closed Today

TYZ3 deals at 107-07+, +0-12+, a 0-20 range has been observed on volume of ~153k.

- Cash tsys are closed today due to the observance of the Columbus Day holiday.

- Futures firmed in early trade as local participants digested the Hamas/Israel conflict which began over the week. The bid in TY was seen alongside the USD firming, and Oil rising ~5 before paring gains. WTI now sits a touch above the $86/barrel handle, up ~4%.

- TYZ3 was unable to sustain its rally above resistance at 107-14 (Oct 3 high), gains were pared and ranges were narrow with little follow through on moves for the remainder of the session.

- Flow wise, the highlight was block buyers in FV (2.7k and 2.2k lots).

- The data docket is empty today, Fedpseak from Dallas Fed President Logan and VC Barr is due.

AUSSIE BONDS: Futures Richer But Off Early Sessions Highs, Consumer & Business Confidence Data Tomorrow

ACGBs (YM +6.0 & XM +1.5) have pared early Hamas/Israel Conflict-inspired gains but continue to deal richer.

- US tsy futures are also off the early Asia-Pac session high of 107-20+ to be dealing at 107-08, +0-13 from NY closing levels. Cash US tsys are closed today for the Columbus Day holiday.

- The local calendar has been empty so far today, with Foreign Reserves data due later.

- Cash ACGBs are 2-5bps richer, with the 3/10 curve steeper.

- Swap rates are 3-5bps lower, with EFPs 1-2bps wider.

- The bills strip has bull-flattened, with pricing +1 to +6.

- RBA-dated OIS pricing is 2-6bps softer across meetings, with Dec’24 leading.

- Tomorrow, the local calendar sees Westpac Consumer and NAB Business Confidence data.

NZGBS: Richer But Early Geopolitical-Induced Gains Pared

NZGBs closed richer but off the session’s best levels, with benchmark yields 1-2bps lower. With the local docket empty today, local participants have been on headlines and US tsys watch following the weekend’s escalation in Middle East tensions.

- US tsy futures are dealing richer in early Asia-Pac dealings at 107-06, +0-11 from NY closing levels, but are well off the early session high of 107-20+.

- Cash US tsys are closed today for the Columbus Day holiday.

- Swap rates are flat to 1bp lower, with implied swap spreads mixed.

- BNZ Job ads index falls 2.3% m/m following a 2.1% gain in August.

- RBNZ dated OIS pricing is 1bp softer for meetings out to July’24 and 3-5bps softer beyond.

- The data docket is relatively light this week, with Net Migration on Wednesday, Food Prices on Thursday and Business NZ Mfg PMI and Card Spending on Friday.

NEW ZEALAND: Considerable Uncertainties Over Next Government’s Composition

RNZ’s poll of polls continues to show that the incumbent Labour Party is likely to lose government following elections to be held this Saturday October 14. However, if polls are correct the opposition coalition of Nationals/ACT won’t have enough seats to form a majority. This will either mean they make a deal with NZ First, or there is a minority government, or even new elections.

- The poll is projecting that Nationals will win around 46 seats and its ally ACT 13 which brings them 2 seats short of a majority. With NZ First on 8 seats, a coalition with this party would give the grouping a good majority with 67 seats. Labour is expected to win 34, the Greens 16 and Te Pati Maori 3, which would result in only 53 seats. A deal with NZ First would give them 61 – a slim majority.

- National’s leader Luxon has said that he will work to achieve an agreement with any leader he needs to be able to form a majority government, according to RNZ. He also believes that he can come to a deal with NZ First. Luxon said that he is standing by his income tax cut policy despite criticism, Nationals don’t support a treaty referendum and that he wants to focus on promoting NZ internationally to increase trade.

- Inflation remains the main concern for voters by far followed by crime, housing and healthcare.

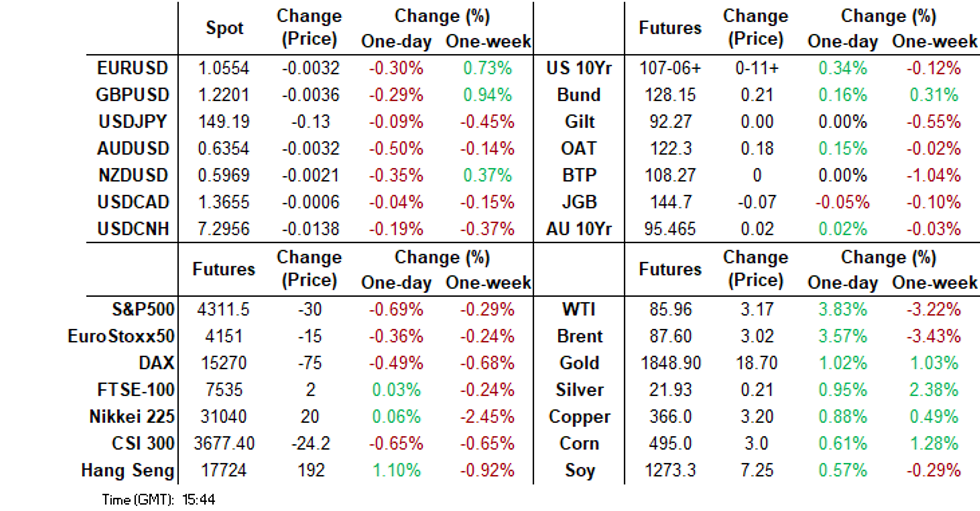

FOREX: Greenback Firms On Geopolitical Tensions

The USD has firmed in Asia and sits at session highs after the market digested the geopolitical tensions between Hamas and Israel. Oil has firmed, WTI is up ~4% and sits at the $86/barrel handle. US Tsy Futures are also firmer, cash Tsys are closed today due to the observance of a national holiday, whilst e-minis are down ~0.8%.

- AUD/USD sits down ~0.5% last printing at $0.6350/55 a touch above session lows. Technically the pair remains bearish, support comes in at $0.6287, 2.00 projection of the Jun 16-Jun 29-Jul 13 price swings. Resistance is at $0.6399 the 20-Day EMA.

- Kiwi marginally pared losses however NZD/USD remains down ~0.3% and sits at $0.5970/75. Support came in ahead of the 20-Day EMA ($0.5948) in early dealing.

- Yen is holding its early gains dealing in a narrow range for the most part a touch above the ¥149 handle. The uptrend in USD/JPY remains intact, resistance is at ¥150.13 the high from Oct 3 and bull trigger.

- Elsewhere in G-10 EUR and GBP are down ~0.3% following the broader USD move.

- The docket is thin today with the market firmly focused on any further development in the Hamas/Israel conflict.

EQUITIES: Geopolitical Tensions Weigh On US Futures, China Markets Down On Return

Regional equity markets are mostly tracking lower in the first part of Monday trade. A number markets are out though, with Japan, South Korea and Taiwan closed for holidays. Hong Kong stocks haven't commenced trading yet either due to adverse local weather conditions. US equity futures are down sharply, as the market digests the news from the weekend of the surprise Hamas attack on Israel.

- Eminis are down a little over 0.80% at this stage, last near 4306. We haven't tested sub 4300 yet, while Friday lows near 4240 remain some distance away. Nasdaq futures are down by a similar amount.

- No doubt focus will be on concern around escalation of the Israel/Hamas conflict to wider parts of the Middle East, with focus on spillover to oil prices and broader risk appetite.

- The other focus point has been the return of China markets after the Golden Holiday week break. At this stage, sentiment is weaker, with the CSI 300 off by nearly 0.60% at the break. Anecdotes around holiday spending were below government estimates, albeit up strongly compared to 2022 (per BBG reports, see this link), while housing activity was also weaker than hoped for (see this link).

- The CSI 300 was off by more than 1% in early trade, but these losses have been pared somewhat.

- Thailand shares remain under pressure in SEA. The SET off a further 0.70% at this stage. The index back to late 2020 levels. Criticism of the government's proposed cash hand out by former heads of the BOT is one area of concern, while higher oil prices will also be weighing.

- Most other markets are weaker, but losses are reasonably modest at this stage.

OIL: Crude Higher On Raised Geopolitical Tensions, Significant Uncertainty

Oil prices rose sharply in response to raised tensions in the Middle East following the weekend’s atrocities. Crude rose over 5% during APAC trading but is now off its intraday highs. There is concern that if hostilities spread to other parts of the region then oil production could be impacted. If it appears that they will be short-lived and contained, then the rise in prices is likely to be reversed. The USD index is 0.2% higher on safe haven flows.

- Brent rose 5.2% to an intraday high of $89 but is now around $87.69/bbl. WTI is now holding just above $86 at $86.06 but earlier it rose 5.4% to a high of $87.24. WTI prompt spreads widened but imply that fundamentals haven’t changed.

- There are reports that Iran was involved in the Hamas attack on Israel and reprisals on Iran could risk crude shipping through the Strait of Hormuz, which the state has previously warned it could close. According to Bloomberg, around 17mn barrels of crude and condensate are shipped through the passage every day. Only recently the US eased sanctions on Iran to allow more oil shipments.

- Later the Fed’s Logan, Barr and Jefferson speak. There is no data due to the Columbus Day holiday. The ECB’s de Guindos and Enria are also scheduled to appear. IMF/World Bank annual meetings take place today and tomorrow.

GOLD: Sharply Higher After Shock Attacks By Gaza Militants

Gold prices have risen by 1% in the Asia-Pacific trading session, driven by increased demand for safe-haven assets following a shock attack by Gaza militants over the weekend, which has escalated tensions in the Middle East.

- This gain follows a 0.7% increase observed on Friday, rebounding from its lowest level since March. Gold had been facing downward pressure due to signals from the Federal Reserve that indicated a commitment to maintaining tight monetary policy, which negatively impacted non-interest-bearing assets.

- Friday's surge in US nonfarm payrolls exceeded expectations, leading to a notable uptick in US Treasury yields. However, it's important to note that various aspects of the report presented a more mixed picture, which helped ease the initial knee-jerk spikes in Treasury yields. Dip buyers, short covering, and technical buying ahead of the Columbus Day long weekend helped trim bond losses.

- In addition to these market dynamics, over the weekend, Fed Governor Michelle Bowman expressed concern about persistently high US inflation rates and indicated that further monetary tightening was likely to be necessary.

- In summary, gold's recent price movements reflect a complex interplay of factors, with geopolitical events in the Middle East, monetary policy signals from the Federal Reserve, and economic data releases all influencing the precious metal's performance.

ASIA FX: USD Firms, But CNH Outperforms As China Markets Re-Open

USD/Asia pairs are mostly higher (except for USD/CNH) as broader market risk aversion, post the weekend's Hamas attack on Israel, has boosted safe have related currencies. Regional equity markets are lower, but losses are less than 1% at this stage. Tomorrow we have Philippines trade figure in an otherwise light data day. We are awaiting China aggregate/new loan figures, which should be out at some stage this week.

- China markets returned from the Golden Week holiday period today. The CNY fixing was close to levels that prevailed prior to the holiday period, while onshore equities have struggled for positive traction. Anecdotes around housing sentiment remain weak, and while holiday spending surged versus last year's levels, it was below government estimates. Still, USD/CNH is back sub 7.3000 this afternoon. Earlier highs were close to 7.3200.

- USD/IDR has hit fresh highs in the first part of dealing today. The pair was last near 15680, which is fresh highs back to late 2022. The pair got to 15763 late last year, which bulls in the pair may target on the continued trend move higher. The combination of global equity risk aversion and still elevated US real yields is a poor one for IDR. 5yr CDS is near 100bps, which is fresh multi-month highs.

- Rupee is little changed from Friday's closing levels in early trade. As of yet there has been no spillover from the escalating tensions in the Middle East which have seen the greenback firm and Oil prices rise ~4% today. USD/INR sits at 82.23/24, the pair has consolidated above 83 in a narrow range in recent dealing.

- USD/THB is back above 37.00 in the first part of Monday trade. The pair last near 37.09. This is below earlier October highs near 37.24, but dips in the pair sub 37.00 have generally been supported in recent dealings. Apparent friction between the government and monetary authorities remains a source of market concern. A number of former BoT Governors have expressed concern over the new Government's cash hand out scheme. Local equities remain under pressure, which will be impacting THB to some degree.

- The Ringgit has opened dealing on Monday softer as geopolitical tensions in the Middle East weigh on risk sentiment. Broader USD trends are dominated as safe havens strengthen this morning. USD/MYR is up ~0.3%, last printing at 4.7275.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing on Monday and remains well within recent ranges. The measure sits ~0.5% below the top of the band. USD/SGD is a touch firmer in early dealing on Monday, the pair sits ~0.1% above opening levels last printing at $1.3660/65. The fallout from geopolitical tensions in Israel has seen the greenback firm on Monday.

- USD/PHP has rebounded firmly in the first part of trade today. The pair is back to 56.85. We closed at the end of last week at 56.625. Today's loss is -0.450 in PHP terms, with the currency one of the weakest performers in the region so far today. The USD and safe haven currencies are outperforming amid broader risk off tone in markets. For PHP, a focus point on the fallout of the Hamas attack on Israel will be on the oil price impact, given it remains a stronger net oil importer.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/10/2023 | 0600/0800 | ** |  | DE | Industrial Production |

| 09/10/2023 | 0600/0800 | ** |  | NO | Norway GDP |

| 09/10/2023 | 0800/1000 |  | EU | ECB's de Guindos Speaks at Conference | |

| 09/10/2023 | 0900/0500 | * |  | US | Business Inventories |

| 09/10/2023 | 1315/0915 | | US | Fed's Michael Barr | |

| 09/10/2023 | 1500/1100 | ** | | US | NY Fed Survey of Consumer Expectations |

| 09/10/2023 | 1730/1330 | | US | Fed Vice Chair Philip Jefferson | |

| 09/10/2023 | 2000/2100 |  | UK | BoE's Mann speaks at NABE |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.