Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Yen volatility has been the main focus in FX markets today, with USD/JPY spiking above 160.00 in early trade, before retracing sharply this afternoon. Japan markets are out today. When currency chief Kanda was asked if the authorities intervened he said no comment.

- The buoyant risk mood in the equity space, led by tech, has helped broader risk appetite. China/Hong Kong shares have been firm in this space. China government bond yields have also continued to recover.

- In the rates space, there has been a modest drift higher in US Tsy futures, aided at the margin by lower oil prices.

- Today the April Dallas Fed manufacturing, European Commission April survey and preliminary April German CPI data print. The ECB’s de Guindos speaks later. The focus of the week will be on Wednesday Fed announcement and Friday’s April payrolls to gauge the rate outlook.

MARKETS

GLOBAL: Export Growth Recovering But Improvement Not Uniform

CPB global export volumes rose for the third straight month in February driven by emerging economies but developed ones also posted a monthly increase. The good news is that they are showing positive and increasing momentum but global IP growth is looking soft after falling sharply in January. However, the global manufacturing PMI is still in moderate expansionary territory.

- Global export volumes rose 0.2% m/m in February to be 2.8% higher on a year ago and 3.2% 3m/3m annualised. Shipments from emerging markets rose 6.7% y/y while from developed improved to 0.7% y/y from -0.6% with both posting increases on the month.

- The recovery is not broad based though with China, advanced Asia, eastern Europe and the US driving it but the euro area, UK and Africa weak. Emerging Asia and Japan are struggling.

Source: MNI - Market News/Refinitiv/CPB

- The JP Morgan global manufacturing PMI rose 0.3 points to 50.6 in March consistent with global IP growth remaining soft but still positive. Global IP rose 0.6% m/m in February after falling 0.8% the previous month which is driving soft growth of 0.2% y/y and 0.2% 3-month annualised momentum.

Source: MNI - Market News/Refinitiv/Bloomberg

- There is some correlation between the Baltic Freight Index and global trade growth (around 45% since 2001) and so developments are worth watching given the recent turn down in the former.

- Trade prices remain soft with export prices falling 3.1% y/y in February and import prices -1.5% y/y but they’re not as disinflationary as they have been with them troughing at -8.9% y/y and -6.8% in June 2023 respectively.

US TSYS: Treasury Futures Steady, Off Earlier Highs

- Jun'24 10Y futures edged higher this morning, reaching 107-23+. The contract has sold of since and now trades just 01+ higher at 107-20, while 2Y futures are unchanged from NY closing levels.

- The trend outlook in Treasuries is unchanged and the direction is down. The 10Y contract traded to a fresh cycle low Thursday Initial resistance is 108-13 (20-day EMA), while to the downside, initial support is at 107-04+ (Apr 25 low).

- Yields and the USD may continue their move higher after PCE has confirmed inflation remains sticky, the upcoming FOMC decision on Wednesday is anticipated to emphasize the importance of exercising patience.

- Across local rates markets; NZGB yields are 1.5-3bps lower & ACGBs 2-4bps lower with curves flatter.

- Looking ahead: US to Sell 140b of 13 & 26 week Bills, focus will be on FOMC policy announcement on Wednesday.

BOJ: MNI BoJ Review April 2024: Policy Unchanged, Notably Brief Statement, Data-Dependent

Executive Summary

- The BoJ convened its Monetary Policy Meeting on April 25-26, maintaining unanimous agreement to retain all major monetary policy parameters unchanged.

- Following a significant shift made in the March meeting, which saw the departure from the negative interest rate policy (NIRP), the decision to keep the policy rate guidance steady within a band of 0 to +0.1% was widely anticipated by markets.

- The accompanying statement was notably brief, spanning just three sentences.

- Governor Ueda refrained from offering a clear timeline for initiating the BoJ's balance sheet reduction.

- As anticipated, the primary focus of the press conference centred on the exchange rate. He noted that the Board members assessed the impact of the yen's depreciation thus far on inflation to be limited, influencing the decision to maintain the status quo at this meeting.

- In the Outlook Report, the overall economic outlook was assessed as unchanged at "has recovered moderately, although some weakness has been seen in part".

- Looking ahead, it is anticipated that the BoJ will adjust rates to mitigate disruptions to the real economy while ensuring overall financial conditions remain supportive.

- While the BoJ appears inclined towards further rate hikes, there are no indications in its outlook suggesting immediate policy tightening.

- Full review here:

AUSSIE BONDS: Richer, Cautious Dealing, Retail Sales Tomorrow, FOMC Policy Decision On Wednesday

ACGBs (YM +2.0 & XM +3.5) are holding stronger but in the middle of today’s Sydney session ranges. Local market participants have been cautious with no domestic data released today and no cash US tsy trading due to a public holiday in Japan. This caution may stem from lingering concerns following last week's unexpectedly high Q1 CPI figures.

- Cash ACGBs are 4bps richer.

- Swap rates are 4-5bps lower.

- The bills strip has bull-flattened, with pricing flat to +3.

- RBA-dated OIS pricing is slightly softer across meetings. A cumulative 4bps of easing is priced by year-end from an expected terminal rate of 4.46% (Sep-24).

- (AFR) The Reserve Bank of Australia board will almost certainly leave the policy rate unchanged when it meets next week. But given the higher-than-anticipated price pressures evident in the March quarter consumer price index and evidence of ongoing labour market resilience, do not expect Governor Michele Bullock to abandon her circumspection regarding the next move in the policy rate. (See link)

- The local calendar will see Private Sector Credit and Retail Sales data tomorrow.

- On Wednesday, the AOFM plans to sell A$800mn of 3.75% the May-34 bond.

NZGBS: Richer, Subdued Dealings, Q1 Employment Report On Wednesday

NZGBs closed in the middle of today’s trading range, 2-4bps richer. With a light domestic calendar and no cash US tsys trading due to a public holiday in Japan, local participants have largely sat on the sidelines.

- Tomorrow the local calendar will see ANZ Business Confidence & Activity Outlook, ahead of the Q1 Employment Report on Wednesday. The FOMC’s Policy Decision is due Thursday morning local time.

- Swap rates are 2-3bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is 1-2bps firmer for meetings out to Oct-24. A cumulative 26bps of easing is priced by year-end.

- (Bloomberg) NZ house-price inflation will be weaker than previously expected in the 1H before a recovery in the 2H, ANZ Bank NZ economists say in an emailed report containing fresh forecasts. (See link)

- The RBNZ will close its offer to repurchase NZGBs maturing May 2024 on May 1 at 4pm, according to a notice. RBNZ repurchased NZ$1.28bn of the May 2024 bond.

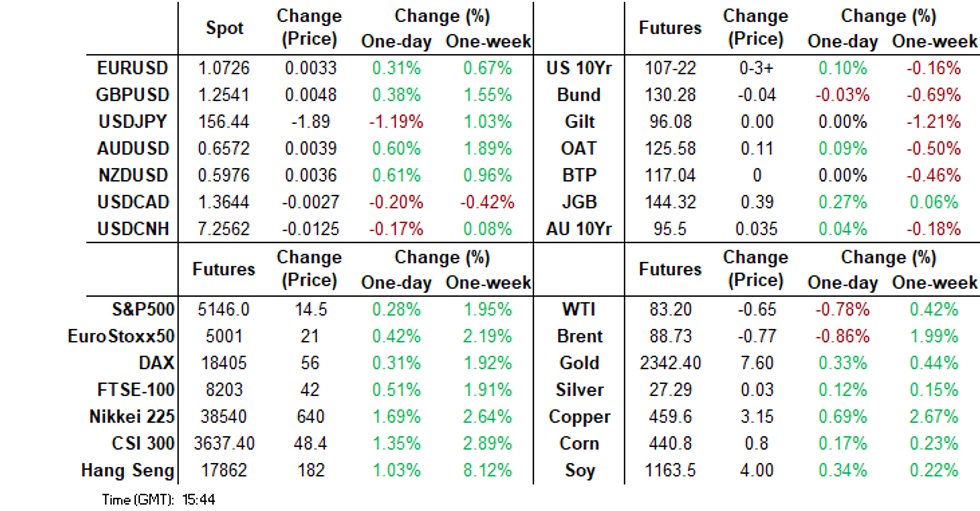

FOREX: USD/JPY Prints Above 160.00, But Sees 400pip Retracement, A$ & NZD Outperform

The BBDXY sits 0.30% lower, the USD index last near 1259.3. The USD has seen broad based weakness against the majors so far today, while sharp yen swings have been the other standout.

- USD/JPY rallied above 160.00 in early trade (fresh highs back to 1990 of 160.17). From there we consolidated in the 159.00/50 region before pulling back sharply this afternoon. Lows were seen near the 156.00 level, so more than 400pips off earlier highs.

- The afternoon moves will likely raise questions around whether intervention has taken place or not. We haven't seen confirmation or hints that this has taken place. Note post BoJ lows in USD/JPY came in around 155.00. With Japan markets out, liquidity has no doubt been lighter.

- Broader USD sentiment is also softer, as the equity mood has generally been a positive one. The regional markets are firmer, with Hong Kong and China performing strongly, led by property and tech names.

- AUD is the best performer, last near 0.6580, up 0.75% for the session. NZD/USD is trailing slightly in percentage terms, last around 0.5980.

- EUR/USD is up around 0.3%, last near 1.0730.

- Looking ahead, German and Spanish CPI data kick off this week’s economic data calendar for the EU. In the US we have the April Dallas Fed manufacturing.

ASIA EQUITIES: China & Hong Kong Equities Are Higher, Property and Tech Leading The Way

Hong Kong and China equities are higher today, the property sector has surged on CIFI holdings after the company announced an agreement with a group of bondholders regarding its offshore liquidity situation, with property indices now in bull market territory, Germany may reconsider plans to tighten screening of Chinese investments. It is a quiet day for economic data, locally this week we have China PMI on Tuesday and Hong Kong GDP on Thursday, while the Fed reverse decision on Thursday will also be closely watched

- Hong Kong equities are surging higher today with the HSTech Index up 0.96% after breaking back above the 200-day EMA on Friday and is now up about 16% from lows on the Apr 19th. The Mainland Property Index up 4.72% at 1,375.84 and is now up 21.20% from lows on Apr 19th with resistance now at the 200-day EMA, a level we have not traded above since June 2021, while the wider the HSI is up 1.10%. China Mainland equities are again underperforming this morning, with the CSI300 up 1.33%, the index has finally broken above the 200-day EMA, a level we have failed to break 5 times over the past month, small-cap indices are performing slightly better with the CSI1000 and CSI2000 both up about 2% while the ChiNext has surged 3.60%.

- China Northbound had an inflow of 22.4b yuan on Friday the largest inflow on record. The past 5-day saw just a single day of outflows, with a total inflow of 25.8b yuan. The 5-day average at 5.15billion, while the 20-day average sits at 0.18billion yuan.

- In the property space, Chengdu, a major city in southwest China, has lifted home-buying restrictions to stimulate real estate demand and economic growth, removing qualification reviews for home buyers and aiming to meet financing needs for property companies. This move follows similar actions in other Chinese cities amid a prolonged real estate downturn, which has weighed on economic growth and prompted concerns from authorities about market stabilization. CIFI Holdings shares surged by up to 25% alongside other Chinese property shares after the company announced an agreement with a group of bondholders regarding its offshore liquidity situation. The agreement involves holders controlling approximately 43% of CIFI's senior notes, perpetual securities, and convertible bonds. Additionally, there are currently no ongoing legal proceedings against the company initiated by any creditors

- Germany is reportedly reconsidering plans to tighten screening of Chinese investments, with fears that such scrutiny could impede economic revitalization efforts; however, the economy ministry spokesman couldn't confirm these claims. The proposed bill aims to expand government powers to review foreign investments for security risks, including in advanced technology sectors, but discussions are ongoing about its provisions and the need to balance security concerns with openness to foreign investment, according to the WSJ.

- Looking ahead, China PMI on Tuesday and Hong Kong GDP on Thursday.

ASIA PAC EQUITIES: Asian Equities Head Higher As Tech Rallies, JPY Sees Sharp Reversal

Asian markets have tracked US markets higher, Japan is closed today for a public holiday. There has been very little in term of headlines over the weekend and a slow day for economic data today. Local market equity flows have been mixed recently, Taiwan and South Korean have seen a pick up late in the week as tech rallied on the back of strong earnings, while Indonesian equities continue to see outflows. Focus in the region today has largely been on the JPY with large moves taking place, the USDJPY is down 2%.

- South Korean equities are higher, tech stocks are the top performing sector. Nasdaq futures are also testing Friday highs, a break higher could help drag the local market up further. The Kospi is up 0.97% at 2,682.23, holding back above the 20-day EMA, we have ticked above 50 on the 14-day RSI, while decreasing red bars for the MACD indicating buyers are in control. Looking ahead this week on Tuesday we have Industrial Productions with consensus at 3.8% falling from 4.8% y/y, Wednesday we have Trade Balance data consensus is a drop to $600m from $4.28b in March and finally on Thursday CPI is expected with consensus at 3% falling from 3.1% in March.

- Taiwan equities are higher today, local markets have benefitted from strong US tech earnings last week with the Taiex trading back above the 20,000 mark, and has now bounced 5.20% from the lows made during the Israel/Iran conflict, the index now trades back above all moving averages, the RSI is back above 50 while the MACD indicator is around 50 and up 1.65% for the day.

- Australian equities are higher today, largely tracking global markets. Most sectors are in positive territory day, with financials leading the way. Looking ahead, Tuesday we have Private Sectors Credit and Retail Sales, Wednesday we have Trade Balance and Building Approval data. The ASX200 closed on the 100-day EMA on Friday and have this morning bounced right off it trading up 0.86% at 7,641. The 20 & 50-day EMAs trade at 7,680/7,690 and are initial resistance.

- Elsewhere in SEA, New Zealand Equities are up 0.40%, jobs filled data showed an increase from the prior month to 0.4% from 0.3% in Feb, Malaysian equities are up 0.42%, Philippines equities have surged 1.60%, Indonesian equities are up 1.90%, while Singapore Equities are down 0.23%.

ASIA EQUITY FLOWS: Asian Equity Flows Mixed, Momentum Remains Negative

- China equity flows continue to see-saw, with a 0.34b yuan inflow on Thursday, equity markets were slightly higher, the CSI300 continues its rangebound trading, with the 200-day acting as resistance, while we trade on the 50 & 100-day EMA act as support. Flow momentum remains negative with the 5-day average now -0.62b, 20-day average at -0.66b and the longer term 100-day average now 0.32B yuan.

- Taiwan equities flows were again negative on Thursday while the market sold off over 1% erasing most of the prior days move higher, with US GDP the driver of the move lower. The 5-day average is now -$578m, vs the 20-day at -$392m, while the 100-day average is now just $48m.

- South Korean equity flows were again negative on Thursday as investors worried about US GDP, the Kospi was down 1.76% erasing the prior days move higher and trading back below the 20 & 50-day EMA. The 5-day average is now -$211m, the 20-day average to $83m and the 100-day average to $170m.

- Philippines equities ended their 14-day run of outflows with a small 2.2m inflow on Thursday. The PSEi has bounced off the 6,400 level and now trades at the 200-day EMA. The 5-day average is -$12m, the 20-day average is -$9.5m, while the 100-day average continues to edge lower now at $0.38m.

- Indonesian equities saw a tiny inflow on Wednesday, which ended a 15-day run of outflows, although the trend has now continued with another $79m outflow on Thursday, the market has now seen a net outflow of $1.12B over the past 17-days. The 5-day average is now -$39m, the 20-day average is -$52m, while the longer term 100-day average is still positive at $12.7m.

- Thailand's SET has been one of the worst performing equity markets in the region over the past year, and has recently broken back below the 20, 50, 100 & 200-day EMA's and broke the 1,350 level which we had traded above since November 2020. The 5-day average is $0.87m, 20-day average is $4.29m, while the longer term 200-day average is -$20m

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | 0.3 | -3.1 | 49.5 |

| South Korea (USDmn) | -385 | -1058 | 13214 |

| Taiwan (USDmn) | -877 | -2890 | -1879 |

| India (USDmn)** | 507 | -627 | 320 |

| Indonesia (USDmn) | -80 | -196 | 681 |

| Thailand (USDmn) | 49 | 4 | -1845 |

| Malaysia (USDmn) ** | 65 | -29 | -608 |

| Philippines (USDmn) | 2 | -64.1 | 13 |

| Total (Ex China USDmn) | -719 | -4860 | 9896 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To Apr 24th |

Oil Prices Lower On Hopes Of Gaza Ceasefire

Increased pressure on Israel from the US for a truce in Gaza and hostage deal has seen oil prices fall during the session as the geopolitical risk premium unwinds. The stronger greenback also weighed on crude earlier but when the USD index came off its high oil prices troughed. The USD index is down 0.2% driven by the yen rebound.

- WTI is down 0.8% to $83.21/bbl above support at $81.03. It fell to a low of $82.96 but breaks below $83 have been short lived. Brent is 0.8% lower at $87.54/bbl after a low of $87.31, above support at $85.88.

- US secretary of state Blinken has just arrived in Saudi Arabia for Gaza ceasefire talks. The US has said that Israel will delay a Rafah offensive until it has met with Blinken.

- Today the April Dallas Fed manufacturing, European Commission April survey and preliminary April German CPI data print. The ECB’s de Guindos speaks later. The focus of the week will be on Wednesday Fed announcement and Friday’s April payrolls to gauge the rate outlook and thus oil demand prospects.

GOLD: First Weekly Decline In Six Ahead Of FOMC Decision

Gold is 0.5% lower in the Asia-Pacific session, after closing 0.2% higher at $2337.96 on Friday.

- Despite this, the price of gold closed approximately 2% lower for the week, marking its first weekly decline in six weeks.

- This occurred ahead of the FOMC’s Policy Decision scheduled for Wednesday, where policymakers are anticipated to reiterate their commitment to maintaining higher interest rates for an extended period.

- In the US short-term interest rate market, expectations have shifted, with projections now suggesting only one Federal Reserve rate cut for the year. This forecast is notably lower than the approximately six quarter-point cuts that were anticipated at the beginning of the year.

- Historically, gold tends to react negatively to higher interest rates due to its lack of yield-bearing characteristics.

- According to MNI’s technicals team, gold is in consolidation mode. The piercing of the 20-day EMA last week could be the start of a possible corrective cycle. A continuation lower would signal scope for an extension towards $2229.4, the 50-day EMA.

ASIA DATA: March Asian Inflation Moderates

Most Asian countries saw a moderation in inflation in March with China posting one of the largest. Non-Japan Asian headline moderated to 1.7% from 2.1% with core at 1.0% from 1.5% but excluding China the regional moderation was more muted and inflation more elevated at 3.6% down 0.1pp and 2.0% down 0.2pp as food and fuel prices remain problematic. While headline remains high, core is contained and unlikely to worry most central banks with the focus in the region on currency weakness.

Non-Japan Asia ex China CPI y/y%

Source: MNI - Market News/Refinitiv/IMF

- The Philippines recorded the highest inflation rate of the countries in our aggregate at 3.7% for headline (up from 3.4%) and 3.4% for core (down from 3.6%) but they are well off their 2023 peaks of 8.7% and 8% respectively. April CPI prints on May 7 and may exceed BSP’s 2-4% band as rice and transport price pressures persist. There are also upcoming wage increases.

- Thailand’s inflation is one of the lowest in the region, lower than China’s, but as the Bank of Thailand points out it reflects government subsidies and price caps rather than weak domestic price pressures. Headline inflation improved to 0.5% in March from -0.8% while core was steady at 0.4%. BoT expects 0.6% and 0.6% respectively in 2024, and 1.3% and 0.9% in 2025. April prints on May 7.

- Even though headline and core inflation are within Bank Indonesia’s 1.5-3.5% band, it hiked rates at its April 24 meeting. The decision was made to ensure FX stability and limit the pass through to inflation after IDR weakened substantially but the 25bp rate rise has done little to strengthen the rupiah with USDIDR trading higher since the meeting and is currently around 16244 +0.6% since the hike.

Source: MNI - Market News/Refinitiv

ASIA FX: USD/Asia Pairs Off Highs As Yen Rebounds

USD/Asia pairs are either lower or off earlier session highs. Gains seen have been modest, particularly compared to the gains seen against the USD by the majors. The BBDXY is down 0.35%, as the yen saw a sharp rebound, while AUD is also higher. Equity sentiment in the region is positive, led by the tech side. Tomorrow, the main focus will be on official China PMIs. Also out is South Korea industrial production.

- USD/CNH sits lower, last near 7.2560, nearly 0.20% stronger in CNH terms. USD/CNY is also a touch lwoer, last near 7.2440. Onshore equities have rallied aided by property and tech sentiment. Local bond yields are also sharply higher. These factors, coupled with a sharp turnaround in yen sentiment, has aided the yuan today. Tomorrow, we get a growth update with the official PMI prints for April.

- 1 month USD/KRW sits off earlier highs, the pair taking cues from broader USD/JPY swings. We were close to 1382 in early trade, but now sit back near 1374, little changed for the session. Equity sentiment is firmer as well, aided by tech names, which is likely helping at the margin.

- USD/THB sits close to 37.00, near recent highs. The pair hasn't had a strong beta with respect to broader USD moves today. March customs data was weaker than expected, with exports falling -10.9%y/y, versus -4.0% forecast. Imports were close to expectations, at +5.6%y/y. This was enough to keep the trade balance in deficit territory (-$1163mn, against a $1000mn projected surplus).

- USD/IDR spot sits a little higher, last close to 16250, around 0.20% weaker in rupiah terms. Carry over from a stronger global yield backdrop last week is still impacting sentiment, along with company related dividend outflows. The better global equity backdrop should improve risk appetite for the rupiah if it continues though.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/04/2024 | 0600/0800 | ** |  | SE | Retail Sales |

| 29/04/2024 | 0700/0900 | *** |  | ES | HICP (p) |

| 29/04/2024 | 0800/1000 | *** |  | DE | North Rhine Westphalia CPI |

| 29/04/2024 | 0800/1000 | *** | | DE | Bavaria CPI |

| 29/04/2024 | 0900/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 29/04/2024 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 29/04/2024 | 1200/1400 | *** | | DE | HICP (p) |

| 29/04/2024 | 1430/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 29/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 29/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 29/04/2024 | 1920/2120 | | EU | ECB's De Guindos remarks at Euro50Group Dinner |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.