Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Credit Suisse is taking decisive action to pre-emptively strengthen its liquidity by intending to exercise its option to borrow from the Swiss National Bank (SNB) up to CHF 50 billion under a Covered Loan Facility as well as a short-term liquidity facility, which are fully collateralized by high quality assets. Credit Suisse also announces offers by Credit Suisse International to repurchase certain OpCo senior debt securities for cash of up to approximately CHF 3 billion.

- U.S. & European equity futures were bid, while U.S. Tsys went offered on the above. Those moves have moderated from session extremes.

- The ECB's monetary policy decision headlines today, coming against a more complex backdrop than was envisaged one week ago.

EUROZONE: March To Date Signals Increased Recession Risk But Still Low

There is a significant risk that recent banking-related developments, which have now spread across the Atlantic to Europe, could result in a more severe slowdown in growth. March estimates of the probability of a euro area recession 6-months ahead are up 16pp from February but it still remains very low at 36% and well below the 50% signal point. Assumptions had to be made for March and so this estimate is just a very early indication that recent events are likely to increase the risk of a recession, especially if they are sustained, but at the current level of severity are unlikely to result in a slump.

- In terms of the effect of recent moves, the lower exchange rate and oil prices reduce the probability of a recession, whereas the expected March 16 rate hike and fall in equities add to it.

- Given it is only mid-March we had to make some assumptions. We used the monthly average for market variables such as equities, OIS market pricing for the ECB rate, and then used previous monthly changes/levels for non-market variables.

Fig. 1: Euro area recession probability estimation

Source: MNI - Market News/Refinitiv/Bloomberg

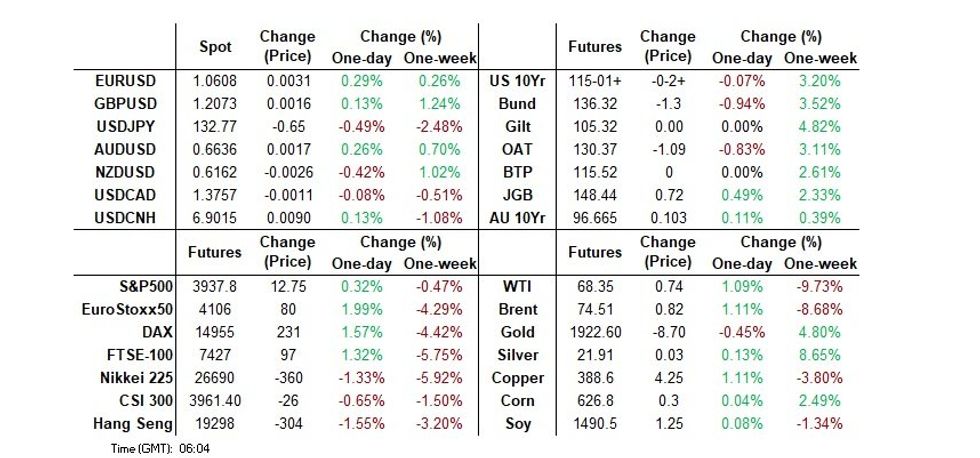

US TSYS: Cheaper In Asia, Credit Suisse Takes Action to Strengthen Liquidity

TYM3 deals at 115-02+, -0-01+, with a 0-24+ range observed thus far on volume of ~233k.

- Cash tsys sit 2-7bps cheaper across the major benchmarks. The curve has bear flattened.

- In early dealing a bid in Antipodean FI spilled over, in lieu of weaker than expected NZ GDP and a repricing of RBA cash rate expectations, and tsys richened in early dealing.

- Pressure as Credit Suisse reported, link here, they are taking action to strengthen liquidity saw tsys extend losses. The bank are to borrow CHF50bn from the Swiss National Bank, as well as buying back debt securities of up to CHF3bn.

- Tsys held cheaper through the Asian afternoon.

- Flow wise a block seller in TU (2k lots) was the highlight.

- Fed dated OIS pricing for March and May meetings have ticked higher in Asia, with ~30bps of hikes before a terminal rate of ~4.9% is reached. There are ~100bps of cuts priced in for 2023.

- In Europe today the ECB's monetary policy decision headlines. We also have jobless claims, Housing Starts and Philadelphia Fed Manufacturing Index.

JGBS: Off Best Levels But Comfortably Richer

JGB futures built on the move away from overnight session (cycle) highs in early afternoon trade, with a particularly poorly received round of 20-Year JGB supply aiding that dynamic after news that Credit Suisse is entering a liquidity pact with the SNB applied pressure during the Tokyo morning. Still, the space held firmer on the day, given the general worry re: banks. JGB futures then kicked higher into the close to sit ~80 ticks firmer on the day ahead of the bell (no catalysts seen), but still reside ~85 ticks shy of post-Tokyo bests.

- Cash JGBs run 4-11bp richer, with 7s outperforming all day given the gains in futures since yesterday’s close, while 10-Year JGB yields sit around 0.29%, trading within the recently established range after the pull away from the BoJ’s YCC cap.

- Swap spreads are unchanged to wider, excluding 10s, where they are tighter.

- In terms of 20-Year auction specifics, there was a wide tail and a low price that was comfortably below general expectations. That came alongside a depressed cover ratio, which printed at the lowest level seen at a 20-Year JGB auction since September’s offering. A reminder that September’s cover ratio represents the lowest level seen at a 20-Year JGB auction since ’12. The recent outright richening, ongoing market vol. and uncertainty re: BoJ Rinban purchases provided the major headwinds for takedown.

- There wasn’t much meaningful domestic headline flow for markets to digest.

- Looking ahead, tomorrow’s local docket is particularly light.

JAPAN: Recent Norms Observed In Weekly International Flow Data

The weekly international security flow data from the Japanese MoF revealed a return to net purchases of international bonds on the part of Japanese investors (a fifth such instance in six weeks), with the SVB situation factoring into late Thursday & Friday trade.

- Elsewhere, Japanese investors were a small net seller of international equities, registering the seventh straight week of net sales there.

- International investors were small net sellers of Japanese bonds in BoJ week. Net sales ahead of the BoJ meeting were smaller than in recent instances, with the Bank ultimately standing pat on policy settings, as guided.

- Finally, international investors were net sellers of Japanese equities for a third straight week, registering the largest round of net selling observed since September in the process.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | 909.5 | -160.1 | 3667.0 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | -169.7 | -48.2 | -863.6 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | -156.8 | -800.4 | -938.9 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -834.2 | -594.6 | -1634.1 |

AUSSIE BONDS: Stronger Despite Jobs Data, Focus Shifts To ECB

ACGBs remain richer on the day (YM +24.8 & XM +10.3) but pare back morning gains in line with softer U.S. Tsys in Asia-Pac trade and stronger-than-expected employment data (+64.4k Vs. +50k expected and 3.5% unemployment rate Vs. 3.6% expected). U.S. Tsys have been pressured in Asia-Pac trade by reports that Credit Suisse was taking action to strengthen liquidity.

- Cash ACGBs are 10-23bp stronger with the 3/10 curve +13bp.

- AU/US 10-year yield differential +8bp at -16bp.

- Swaps are 8-23bp richer but 3-5bp off session bests. EFPs wider.

- Bills strip is 19-40bp richer led by whites.

- Today’s strong employment data along with the robust NAB Business Survey should have encouraged the market to price another 25bp hike from the RBA in April given these releases were explicitly cited as important inputs to the policy decision. Nonetheless, with global banking concerns front and centre, RBA-dated OIS has continued to price an end to the tightening cycle. April meeting pricing remains at -3bp with 38bp of easing priced by year-end.

- With no local data slated until next week, the market will remain transfixed on banking crisis headlines. With the focus, at least temporarily, shifting to European banks, all eyes will be on the ECB policy decision tonight (BBG consensus expects a 50bp hike).

Fig. 1: RBA Cash Rate & RBA Dated OIS Pricing

Source: MNI – Market News / Bloomberg

AUSTRALIA: Labour Market Remains Tight, RBA Uncertain Given Bank Concerns

Employment bounced back 64.6k after declining the previous two months and the unemployment rate returned to 3.5%, close to its October 2022 low. The labour market remains very tight with little sign of easing pressures, thus this data along with the solid NAB business survey point to a further 25bp hike in April. However, market turmoil and overseas banking issues are muddying the waters for the next RBA meeting.

- There were 64.6k new jobs in February more than expected and more than reversing the cumulative 27.5k drop in Dec/Jan. There was also a return to the trend of rising full-time employment (+74.9k) and falling part-time (-10.3k), reflecting ongoing labour shortages. The ABS noted that the majority of the people waiting to start a new job in January returned to work in February and the numbers waiting to start a new job are back to normal.

- The number of unemployed fell 16.5k helping to bring the unemployment rate down along with strong jobs. However, the number of unemployed is 4.1% higher than the October trough, which is not surprising given the increase in labour supply through immigration.

- Underemployment and underutilisation rates all eased back to their recent lows; another indicator of a tight labour market. The former fell 0.4pp to 5.8% and the latter -0.4pp to 9.4%, the lowest since 1982 apart from November 2022.

- Hours worked also rebounded after three consecutive falls. They rose 3.9% m/m and 5.1% y/y in February with full-time up 4.4% m/m and part-time +1.3% m/m. The ABS commented that there were “almost no major disruptions” to hours worked, as the economy normalises.

- The participation rate rose 0.1pp to 66.6% but remains below November’s peak of 66.8%.

Source: MNI - Market News/ABS

Fig. 2: Australia underemployment rate vs underutilisation rate %

Source: MNI - Market News/ABS

AUSTRALIA: Inflation Expectations Ease And Suggest End 2022 Price Peak

Melbourne Institute consumer inflation expectations in March eased to 5% from 5.1% but still didn’t break below 5% where it has been stuck for the last year, despite a recent drop in petrol prices. It is now down 1.7pp from its June 2022 peak. Q1 inflation expectations have eased to 5.2% from Q4’s 5.5%, which is another indicator suggesting that price pressures peaked at the end of last year, in line with the RBA’s thinking.

Fig. 1: Australia CPI y/y% vs MI consumer inflation expectations %

Source: MNI - Market News/Refinitiv

NZGBS: Off Bests Despite Weaker GDP Data

After opening stronger in sympathy with global FI developments, NZGBs add to gains on the weaker-than-expected GDP data (-0.6% Q/Q Vs. -0.2% expected) but fail to hold at best levels as U.S. Tsys and ACGBs cheapen in Asia-Pac trade. NZGBs close 9-16bp richer, but 9bp off bests with the 2/10 curve +7bp.

- Swaps close well off richest levels with rates 13-23bp lower, implying significantly tighter swap spreads.

- While the GDP data was weaker than analysts expected, it was much weaker than the RBNZ’s forecast of +0.7% Q/Q. On the surface, the data could be seen as supporting a tightening pause in April, but that ignores recent volatility in the data. The RBNZ is likely to want clearer signals that it has done enough in its fight against capacity constraints and inflation before halting tightening.

- RBNZ dated OIS pricing is 10-18bp softer on the day, but 4-7bp firmer than pre-data levels. April meeting pricing shows 15bp of tightening.

- With no antipodean data slated until next week, the market will remain transfixed on headlines associated with the global banking crisis. With the focus, at least temporarily, shifting to Europe given Credit Suisse developments, all eyes will be on the ECB policy decision tonight (BBG consensus expects 50bp hike).

NEW ZEALAND: Q4 Growth Disappoints Opening Possibility Of April RBNZ Pause

Q4 GDP was weaker than analysts expected and a lot more so than the RBNZ’s +0.7% q/q forecast. It fell 0.6% q/q but followed two very strong quarters of over 1.5%. This left 2022 growth at 2.4%. This disappointing result with another contraction expected in flood-affected Q1 opens the possibility of a pause in RBNZ tightening in April so it can wait for Q1 CPI data on April 19, the OIS market has a 50% chance of 25bp priced in.

- The main driver of the contraction in production-based GDP in Q4 was the manufacturing sector which fell 1.9% q/q. There was also weakness in retail, recreation, transport, accommodation and other services. Tourism disappointed in the quarter and overseas visitors were still below pre-pandemic levels.

- The expenditure measure of GDP fell 0.8% q/q after rising 1.9% in Q3, as private consumption was flat but investment fell 1.9% and government spending down 2.4%. New Zealanders had also made a shift from durable goods spending to services. Net exports detracted 0.7pp, as exports of goods fell 5.3% q/q.

FOREX: Yen Firmer In Asia, Credit Suisse Takes Action to Strengthen Liquidity

JPY is the standout performer in the G-10 space at the margins today in Asia. News that Credit Suisse would shore up its liquidity via a CHF50bn loan from SNB, and buy back debt securities of up to CHF3bn, saw US and European equity futures rise and the USD marginally pressured.

- USD/JPY prints at ¥132.60/70 down ~0.6%. The pair is mostly following intra-day gyrations in US yields, albeit with yen slightly outperforming these trends. Earlier the latest round of North Korean missile launches, may have sparked some safe haven demand, but only at the margins. Data wise, the trade deficit was narrower than expectations and core machine orders printed above expectations. Support comes in at 50-Day MA (¥132.54) then ¥132.22, the low from March 15.

- Pressure in NZD came as Q4 GDP printed below expectations at -0.6% Q/Q and much weaker than the RBNZ forecast of +0.7%. NZD/USD pared some of its losses on the Credit Suisse news. ASB revised their call for the April RBNZ meeting to a hike of 25bps.

- AUD/USD firmed as the Australian unemployment rate printed lower than expectations. However, pressure was seen as Iron Ore slid on concerns that cuts to Chinese steel production will be cut once again as the government mandates reduced output in order to limit carbon emissions.

- Elsewhere in G-10 CHF is ~0.3% firmer, USD/CHF prints at CHF0.9300/05, marginally paring yesterday's Credit Suisse driven weakness as USD/CHF rose 2%.

- Cross asset wise; US Treasury Yields are firmer and S&P500 futures are up ~0.5%. BBDXY is 0.2% softer.

- In Europe today the ECB's monetary policy decision headlines. Further out we have US Jobless Claims, Housing Starts and Philadelphia Fed Manufacturing Index.

FX OPTIONS: Expiries for Mar16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0610-20(E1.5bln), $1.0628-40(E1.2bln), $1.0700-15(E1.7bln)

- GBP/USD: $1.2150-55(Gbp588mln)

- EUR/GBP: Gbp0.8800(E829mln)

- AUD/USD: $0.6600-25(A$1.0bln)

- USD/CAD: C$1.3815($716mln)

ASIA FX: USD/Asia Off Session Highs, THB Outperforming

USD/Asia pairs are down from session highs currently, with USD indices off by 0.15% at this stage, helping sentiment in the region. Regional equities are mostly weaker but away from lows, with higher EU/US futures a positive. Still to come is the BI decision, which is expected to see rates left on hold. Tomorrow, Singapore Feb trade figures are out, along with Malaysia trade figures as well.

- USD/CNH was weaker in the first part of trade (6.8846 low), but didn't see much follow and we spike towards Wednesday highs (6.9139) before settling back to the 6.9000 level. Onshore equities are weaker, although we have seen modest Northbound Stock Connect flows (0.5bn yuan).

- 1 month USD/KRW got close to the 1314 level, but we now sit back at 1308/09. Local equities are close to flat, but offshore investors have sold over $300mn in local equities. USD/KRW remains fairly close to the mid-point of its recent ranges.

- The SGD NEER (per Goldman Sachs estimates) is marginally firmer today, post the fallout from the shift lower in global tightening expectations has seen volatile swings in the NEER but today NEER sits within recent ranges. We now sit ~1% below the top of the band. USD/SGD failed to break below the 20-Day EMA ($1.3453) in yesterday's trading. The pair was offered this morning as Credit Suisse said they will enter a liquidity pact with the SNB, however the losses have been pared as the USD consolidates its recent gains and the pair sits at $1.3510/20.

- USD/IDR got to 15450 not long after today's open. We sit slightly lower now, just under 15400. We aren't too far away from earlier March highs from last week in the 15465/15475 region. Note that we did see BI intervene in FX markets when we touched those highs. Later today we have the BI decision, no change is expected, see our full preview here.

- USD/INR sits in the 82.65/70 region currently. We were above 82.80 not long after the open. As we edge closer to the 83.00 level, RBI intervention risks will no doubt firm. Like elsewhere in the region, the rupee is being weighed by a weaker equity market backdrop, with the Nifty now 10% off Dec highs. This leaves the index in technical correction territory.

- USD/THB sits around 34.50 currently. Through March dips towards 34.40 have been supported in the pair, although the baht is still ~2.50% up for the month so far, comfortably ahead of the next best performer (the won +0.90%). If the baht was following ADXY trend closer it would arguably be closer to 35.00. The currency may be seen as a somewhat of a safe haven in the region given the current turmoil in global banking stocks. Anecdotes from China suggest further momentum around outbound tourism.

EQUITIES: Higher EU Futures Help Contain Losses

Regional equities are down across the board, although we are away from worst levels for a number of indices. This largely owes to higher EU and US equity futures. EU futures are ~2% higher at his stage, thanks to Credit Suisse efforts to boost its liquidity outlook (including a CHF50bn loan from the SNB). US futures are around +0.40% for both eminis and Nasdaq futures at this stage.

- The HSI is down roughly 1.5%, but we were down by more than 2% at one stage. Onshore shares are off by close to 0.70% for the CSI 300 and Shanghai Composite.

- The Topix is off by ~1.30% in Japan, with the underlying bank index down over 3.6%, reversing all of yesterday's 3.3% bounce.

- The Kospi is down slightly, with offshore selling -$305.8mn of local shares. The Taiex is down close to 1%.

- Indian shares are trying to firm. The Nifty was weaker at the open and is 10% below Dec peaks, which puts the index in a technical correction. The Philippines index saw the same fate, with the main index off by 2% at this stage.

- NZ shares rose 0.70%, perhaps on hopes the RBNZ tightening cycle is getting closer tot he end following today's weaker than expected Q4 GDP contraction. The ASX 200 fell by nearly 1.5%, despite robust jobs data for Feb.

GOLD: Prices Ease As CS Reassures Markets & US Yields Rise

Gold prices rose 0.8% on Wednesday and reached a high of $1937.39/oz on the back of further flight to quality flows driven by banking troubles extending across the Atlantic to Europe. During APAC trading they are down slightly and are currently trading around $1913.70. Bullion had reached a high of $1924.38 in early trading but then fell to a low of $1907.62 following a Credit Suisse report that reassured markets that it was strengthening its liquidity position. US 2-year yields rose in response which weighed on gold. The USD index is currently down slightly.

- Bullion remains above its 50-day simple moving average. On Wednesday it cleared resistance of $1923.20 but has been unable to hold above that today.

- Weaker-than-expected US PPI data supported gold as it tempered inflation concerns. The OIS market now has about 15bp of tightening priced in for the March 22 Fed meeting. Bullion is expected to rally above $2000/oz if the Fed pivots (bbg).

- The ECB meets later and is expected to hike rates by 50bp but the OIS market currently has about 29bp priced in. In the US, there is only second-tier data including February housing starts/permits, trade prices, jobless claims and the Philly Fed index.

OIL: Crude Stabilises After Growth Fears Hit The Energy Source Hard

Oil prices are off their intraday lows and are currently up on the day, which if sustained would be the first rise since last Friday. On Wednesday crude plummeted to lows not seen since late December 2021 on concerns of a global recession. WTI is up 0.8% today and is trading just around $68.15/bbl and Brent is 0.9% higher to around $74.35.

- While the sharp move lower in crude in recent days was driven by banking troubles, bullish positioning in the lead up to the collapse of SVB has exacerbated the move. Despite the CS announcement that it was strengthening its liquidity position, volatility in the oil market is likely to persist and banking sector developments remain the focus.

- The IEA reported on Wednesday that it expects the oil market to remain in surplus over H1 2023, as Russian output has proved resilient. Demand in France is being reduced by striking refinery workers and US official EIA data showed another US crude stock build while products were run down. There is still optimism regarding China’s demand outlook as refining has picked up strongly in 2023.

- The ECB meets later and is expected to hike rates by 50bp but the OIS market currently has about 29bp priced in. In the US, there is only second-tier data including February housing starts/permits, trade prices, jobless claims and the Philly Fed index.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/03/2023 | 0700/0800 | ** |  | NO | Norway GDP |

| 16/03/2023 | 0900/1000 | ** |  | IT | Italy Final HICP |

| 16/03/2023 | 1230/0830 | ** |  | CA | Wholesale Trade |

| 16/03/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 16/03/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 16/03/2023 | 1230/0830 | *** | | US | Housing Starts |

| 16/03/2023 | 1230/0830 | ** | | US | Import/Export Price Index |

| 16/03/2023 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 16/03/2023 | 1245/1345 | *** |  | EU | ECB Deposit Rate |

| 16/03/2023 | 1245/1345 | *** | | EU | ECB Main Refi Rate |

| 16/03/2023 | 1245/1345 | *** | | EU | ECB Marginal Lending Rate |

| 16/03/2023 | 1345/1445 | | EU | ECB Press Conference Following Rate Decision | |

| 16/03/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 16/03/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 16/03/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.