Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- NZGBs closed 4-7bps cheaper following the RBNZ’s decision to leave the OCR at 5.50%. The 0.2pp overshoot of the RBNZ’s Q1 CPI forecast seems to have driven a hawkish shift. Rates may now need to stay restrictive for “longer than anticipated”. A cumulative 33bps of easing is priced by year-end versus 43bps before today’s decision.

- NZD/USD surged on the hawkish hold, but has moved away from session highs, as RBNZ officials appeared to push back against a rate hike before year end. Still, NZD is comfortably the best performer in the G10 space so far today.

- Elsewhere, the cash JGB curve has bear-steepened following today’s lacklustre 40-year auction, with yields flat to 4bps higher. The benchmark 10-year yield is 1.5bp higher at 0.995%, a new cycle high.

- Later the Fed’s Goolsbee appears and the May FOMC meeting minutes are published. There are US existing home sales and UK April CPI/PPI print. The BoE’s Breeden speaks.

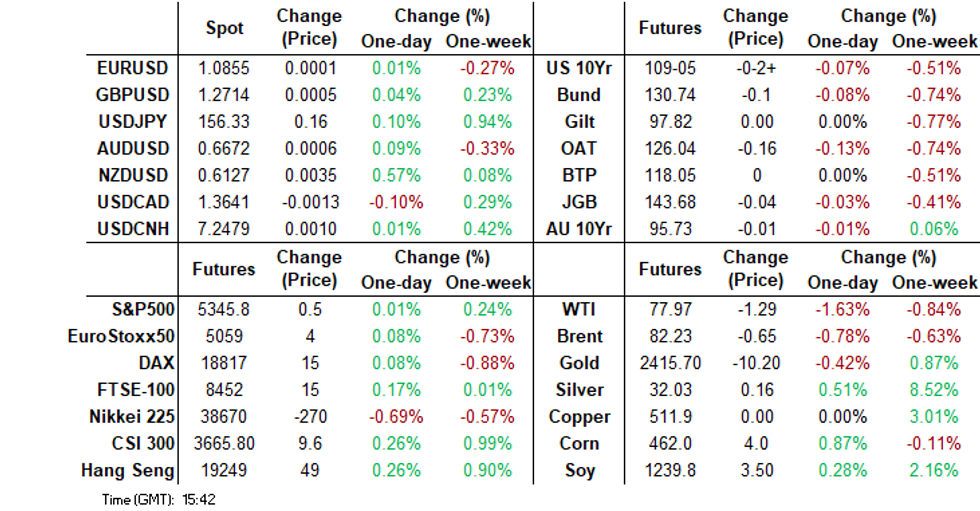

MARKETS

US TSYS: Treasury Futures Edge Lower, Ahead Of FOMC Mins Later

- Treasury futures have ticked lower in the second half of the trading session, the 10Y contract is (- 02) at 109-05+, while the 2Y contract is ( - 00.375) at 101-21+.

- Volumes: TU 35k, FV 42.5k, TY 50k

- Tsys flows: Large SOFR futures strip block, totaling 1.7mm DV01, looks to be a buyer.

- The treasury curve is little changed today, yields are about 1bps higher, the 2Y yield +0.8bp at 4.839%, 10Y +0.8 at 4.420%

- Regionally: ACBGs yields are 1-2bps higher curve has bear-flattened, NZGBs yields are 3-7bps higher, curve bear-flattened post a hawkish RBNZ, while JGBs are 0.5bps to 6bps higher, with the 10y now trading at 0.99%

- Earlier, the Fed's Bostic, Collins & Mester have been involved in a moderated discussion, with the key points from each; Bostic stated that the economy is incredibly resilient and that it will take longer for interest rates to influence decisions, Mester believes economic growth will be above trend this year, inflation will take longer to decrease, and current policy is well-positioned but needs monitoring while Collins emphasized the importance of patience in policy adjustments, noting that it will take longer to see progress and that a methodical, holistic approach is needed.

- Rate cut projections hold steady vs. late Monday: June 2024 at -5% w/ cumulative rate cut -1.2bp at 5.318%, July'24 at -20% w/ cumulative at -6.3bp at 5.267%, Sep'24 cumulative -19.9bp, Nov'24 cumulative -27.6bp, Dec'24 -43.7bp.

- Looking ahead: May 1 FOMC Minutes, Existing Home Sales and US Tsy 20Y Bond Sale.

JGBS: Bear-Steepener After A Poor 40Y Auction, FOMC Minutes Later Today

JGB futures are weaker and at session lows, -4 compared to the settlement levels, in afternoon trading.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Trade Balance and Machine Orders data.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session ahead of the release of the May Meeting FOMC Minutes later today.

- The cash JGB curve has bear-steepened following today’s lacklustre 40-year auction, with yields flat to 4bps higher. The benchmark 10-year yield is 1.5bp higher at 0.995%, a new cycle high.

- The 40-year yield zone is 2.0bps in post-auction trading and approximately 4bps higher on the day.

- The swaps curve has bear-steepened, with rates flat to 4bps higher.

- Tomorrow, the local calendar sees Weekly International Investment Flow, Jibun Bank PMIs and Machine Tool Orders data alongside BoJ Rinban Operations covering 1-10-year JGBs.

AUSSIE BONDS: Slightly Richer, Narrow Ranges Ahead Of FOMC Minutes

ACGBs (YM flat & XM +1.0) are slightly stronger after dealing in narrow ranges in today’s Asia-Pac session. With the local calendar empty, local participants have been content to sit on the sidelines ahead of the release of the May FOMC Minutes later today.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s modest gains.

- Cash ACGBs are flat to 1bp richer, with the AU-US 10-year yield differential 2bps higher at -17bps.

- ACGBs have significantly outperformed their NZ counterparts, with the AU-NZ 10-year yield differential 7bps more negative, after the RBNZ delivered its policy decision. NZGBs closed 4-7bps cheaper. The 0.2pp overshoot of the RBNZ’s Q1 CPI forecast seemed to drive a hawkish shift. Rates may now need to stay restrictive for “longer than anticipated”. The RBNZ’s upward revision to its OCR path and the discussion of another hike reflect this. It said “rate cuts continue to be delayed”.

- Swap rates are flat.

- The bills strip is flat to -2.

- RBA-dated OIS pricing is flat to 1bps firmer across meetings. A cumulative 9bps of easing is priced by year-end.

- The local calendar will see Judo Bank Preliminary PMIs and Consumer Inflation Expectations data tomorrow.

AUSTRALIA: Bloomberg Consensus Continues To See Q4 Rate Cut

Bloomberg has released its May economist survey showing that most still expect a soft landing with the probability of a recession at around 30%. The survey was taken between May 16 and 21 and so includes the last RBA meeting and the federal budget. There were few revisions from the April survey.

- Consensus’ rate profile is unchanged with a 25bp cut expected in Q4 with another one in Q1. Q2 2025 only has 15bp of easing. Rates are forecast at 3.35% at end-2025.

- 2024 CPI has been revised up 0.1pp to 3.4% y/y with 2025 unchanged at 2.8%. Q4 2024 is 0.1pp higher at 3.2%, below the RBA’s 3.8%, and Q2 2025 is unchanged at 2.9%, lower than the RBA’s 3.2%.

- 2024 GDP growth is slightly lower at 1.3% but 2025 is unchanged at 2.2%. Consensus expects Q1 and Q2 to rise by 0.3% q/q before rising towards 0.6% by H1 2025. Private consumption is unrevised at 0.8% for this year and 2.1% for next. GFCF was revised higher across the forecast horizon.

- The unemployment rate is still forecast at 4.1% for Q2 but it is now expected to peak at 4.5% rather than 4.6%.

- The budget deficit has been revised lower for 2024 to -0.1% from -0.5% of GDP but 2025 is 0.1pp higher at -0.8%, a relatively minor adjustment given the increase in government spending announced.

RBNZ: Rates High For Even Longer

The 0.2pp overshoot of the RBNZ’s Q1 CPI forecast seems to have driven a hawkish shift. Rates may now need to stay restrictive for “longer than anticipated”. The RBNZ’s upward revision to its OCR path and the discussion of another hike reflect this. It said “rate cuts continue to be delayed”. Rates are now not expected to be materially below 5.5% until H2 2025. The decision to leave rates at 5.5% was unanimous.

- Risks to inflation are skewed to the upside but the MPC is more confident though “that inflation will decline to within the target range over the medium term” helped by easing capacity pressures. The RBNZ is concerned that certain higher services prices, which it has little impact on, will boost inflation expectations.

- Q3 2024 CPI is now expected to be at the top of the 1-3% target band, similar to the November 2023 forecast but 0.4pp higher than assumed in February. It now does not reach the mid-point until Q2 2026, half a year later than expected in both February and November. The slow moderation in services inflation is to blame as well as low productivity.

- As a result the Q4 2024 and Q1 2025 OCR assumptions have been revised up 10bp with Q2 up 20bp to 5.5%. Governor Orr has said in the past that the OCR path is not a target and small moves can reflect subtle changes in the bank’s model, but it is monitored by markets closely. The path assumes rates will be 20bp higher than in February for end-2025 and -2026.

- Quarterly growth was revised lower over 2024 and 2025 with the unemployment rate 0.1pp higher in Q4 2025 and 2026.

RBNZ: RBNZ Decided It Needed To Be Patient Rather Than Hike Again

RBNZ Governor Orr said that raising rates was a “real consideration” at the May meeting because of the higher starting point for domestic inflation and lower potential growth but decided that patience was needed as policy is restrictive and the output gap growing. The RBNZ will keep policy restrictive until it is confident that it has returned inflation to target.

- The first rate cut was delayed in the forecast due to the higher inflation starting point, lower potential output and sticky domestic price components.

- Governor Orr dismissed that there is an 80% chance of a rate hike by year end and Conway added that it is a “spurious” interpretation. Orr said the 2024 path reflects the RBNZ’s asymmetric reaction function to upside inflation surprises. The RBNZ focuses on 18 months or more ahead and knows the near term is volatile.

- Orr said that NZ is at the slow moving, less rate sensitive moment for inflation. The domestic components currently slowing the disinflation process, such as rents, rates and insurance, have low rate sensitivity and so will be slow to fall. It is these factors that need to see disinflation to bring overall inflation from 4% to 2% and that is going to be slower than the disinflation that has already taken place, but that is usual and is occurring globally.

- A further rate hike would have affected the rate sensitive components the most and these are not the ones that need to slow, whereas there would have been limited impact on the areas that need to see material disinflation.

- A new development was the downward revision of the potential growth rate due to low productivity growth, which is creating more domestic inflationary pressures. The best thing the RBNZ can do to boost productivity is to have low and stable inflation.

NZGBS: Closed Sharply Cheaper After The RBNZ Pushes Out Rate Cut Expectations

NZGBs closed 4-7bps cheaper following the RBNZ’s decision to leave the OCR at 5.50%. The 0.2pp overshoot of the RBNZ’s Q1 CPI forecast seems to have driven a hawkish shift. Rates may now need to stay restrictive for “longer than anticipated”. The RBNZ’s upward revision to its OCR path and the discussion of another hike reflect this. It said “rate cuts continue to be delayed”.

- The NZ OCR is now not expected to be materially below 5.5% until H2 2025. The decision to leave rates at 5.5% was unanimous.

- (Dow Jones) The RBNZ signalled that interest rates might need to remain restrictive for longer than expected due to stubborn inflation, delivering a hawkish shock to money markets. (See link)

- Swap rates closed 5-9bps, with the 2s10s flatter.

- RBNZ dated OIS pricing closed 5-11bps firmer for meetings beyond July. A cumulative 33bps of easing is priced by year-end versus 43bps before today’s decision.

- Tomorrow, the local calendar will see Retail Sales Ex Inflation data along with RBNZ Governor Orr's appearance in front of the Parliamentary Finance & Expenditure Select Committee.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 3% Apr-29 bond, NZ$175mn of the 2% May-32 bond and NZ$75mn of the 1.75% May-41 bond.

FOREX: USD Index Steady, NZD Surges On Hawkish RBNZ Hold Before Trimming Gains

The BBDXY is little changed in the first part of Wednesday dealings, last around 1247.55. This has masked noticeable outperformance from the NZD, post a hawkish hold from the RBNZ.

- The RBNZ revised the OCR track higher, along with the inflation outlook. We have seen a sharp rise in NZGB yields as a result (5-8bps, led by the front end).

- NZD/USD got to highs of 0.6152 but we sit back around 0.6120/25 in recent dealings, still +0.50% firmer for the session. RBNZ Chief Economist Conway pushed back against market pricing of a Dec hike at the press conference. Still, Governor Orr noted raising rates at this meeting was a real consideration.

- Upside focus for NZD is likely to rest at 0.6200/20 (round number, March 8 High). Note the 200-day EMA is back near 0.6075.

- AUD/USD has been relatively steady, dragged higher by NZD but now back to flat at 0.6665. The AUD/NZD cross got to lows of 1.0861 (close to the 100-day EMA at 1.0857), but we sit slightly higher now, around 1.0880/85.

- Trends have been relatively quiet elsewhere. USD/JPY has drifted higher but remains within Wednesday ranges. We were last 156.30/35.

- In the cross asset space, US trends have been very steady in terms of equity futures and yields.

- Looking ahead, Wednesday’s calendar is highlighted by UK inflation data and the FOMC minutes of the May meeting.

ASIA PAC EQUITIES: Equities Mixed Ahead of Nvidia Earnings And FOMC Minutes

Asia markets have traded mixed today, while ranges have been tight. Stocks in Japan are lower as yields tick higher, yen ticked lower and some investors await Nvidia's earnings, while elsewhere in the region markets are higher with Taiwan's chip related stocks in particular TSMC performing the best. Today, we had Fed official speaking earlier this morning where they reiterated their higher for longer message, the RBNZ left rates unchanged which was widely expected, however they were more hawkish than the markets were expecting. Later today we have the BI rate decision who are also expected to keep rates on hold and the FOMC minutes will be a focus later tonight.

- Japanese equities have opened slightly lower today, and have remained rangebound since as investors await results from Nvidia and the minutes from the FOMC meeting. Earlier, Trade balance data show the deficit has increased to -¥462.5b from a revised ¥387.0b, exports increased to 8.3% from 7.3% in March, while imports increased to 8.3% from a revised -5.1% in March, core machine orders beat estimates coming in at 2.9% m/m vs -2.0% m/m. The Topix is down 0.57%, while the Nikkei 225 is faring slightly worse due to the higher concentration of tech stocks, down 0.69%.

- South Korean equities are off earlier highs and now trade unchanged for the day. Earlier, PPI was 1.8% y/y in Apr, up from a revised 1.5% y/y in March, while both business surveys increased with manufacturing rising to 76 from 74, and non-manufacturing rising to 72 from 71.

- Taiwan equities are are the top performing in the region today, led higher by TSMC in a sign markets may be expecting positive results out from Nvidia. Later today we have the unemployment rate due out which is expected to be unchanged at 3.40%. The Taiex is up 1.35%.

- Australian equities are little changed today and off earlier highs Australian related chicken stocks have fallen after the agriculture department said they are investigating an incident of bird flu. Gains in Financials & materials are being offset by losses in Consumer discretionary and Communications, with the ASX200 now unchanged.

- Elsewhere in SEA, New Zealand equities closed up 0.20%, however off about 0.40% post the hawkish RBNZ, Indonesian equities are up 0.68% ahead of BI later today,Indian equities are up 0.15% and Philippines equities are down 0.47%

ASIA STOCKS: HK & China Equities Off Earlier Highs, Short Positions Increase

Hong Kong & Chinese equities are mixed today, and off earlier highs, there has been very little in the way of domestic drivers today with no economic data out for either region. Short positions have increased against iShares China Large-Cap Fund & iShares MSCI China ETF, while short positions against iShares MSCI EM Ex-China fund fell to near zero, in a sign investors may think the recent equity rally has come to an end.

- Hong Kong equities are mostly higher today with property leading the way, the Mainland Property Index is up 1.93%, while the Hang Seng Property Index is up just 0.55%, the HSTech Index is up 0.75% after being down over 3% on Tuesday while the HSI is up 0.19%. In China onshore markets, equities are little changed after initial opening in the red the CSI300 is up 0.06% while the small-cap indices CSI1000 is down 0.32% & CSI2000 is unchanged, the growth focused ChiNext is up 0.15%

- (MNI) China Lacking Meaningful Opening - Britcham (See link)

- Looking ahead, quiet week for China on the data front.

OIL: Crude Continues Slide, Waiting For EIA Data

Oil prices have continued falling during today’s APAC trading after a 1.4% drop on Tuesday driven by a reported US crude stock build. Brent is down 0.7% to $82.31/bbl after a low of $82.15, and WTI -0.8% to $78.05 with a couple of brief breaks below $78. The USD index is little changed.

- Bloomberg reported that oil rose 2.5mn barrels and gasoline 2.1mn but there was a distillate drawdown of 300k, according to people familiar with the API data. The official EIA numbers are released later today but the market’s focus is on the June 1 OPEC+ meeting.

- OPEC has cut output by around 2mbd and while an extension into H2 is widely expected the details, such as how much and how long, remain unclear.

- Later the Fed’s Goolsbee appears and the May FOMC meeting minutes are published. There are US existing home sales and UK April CPI/PPI print. The BoE’s Breeden speaks.

GOLD: Consolidating Ahead Of FOMC Minutes

Gold is 0.3% weaker in the Asia-Pac session, after closing 0.2% lower at $2421.05 on Tuesday. With the release of the May FOMC Minutes later today, Tuesday’s price action represented a consolidation after the yellow metal hit a fresh all-time high on Monday.

- The US Short-Term Interest Rate market has this week reduced the odds that the Federal Reserve will deliver two rate cuts this year, even as some US policymakers deliver cautiously optimistic views on the path forward for borrowing costs. Higher rates are negative for gold, as it doesn’t pay interest.

- According to MNI’s technicals team, yesterday’s initial gains resulted in a print above resistance at $2431.5, the Apr 12 high and bull trigger. The break confirmed a resumption of the primary uptrend and paved the way for a climb towards 2452.5 next, a Fibonacci projection.

- On the downside, the 50-day EMA, at $2288.7, represents a key support. A clear break of it would be bearish.

BOK: MNI BoK Preview - May 2024: On Hold, Easing Timeline Likely Delayed

- None of the economists surveyed by Bloomberg see a change at tomorrow’s BoK policy meeting. This is also our firm bias, which would leave the policy rate at 3.50%, which is where it has been since January last year.

- Overall, our sense is that the BoK is likely to retain confidence in a further softening in the inflation backdrop as we progress through H2 this year. However, given developments since the last policy meeting, we expect a cautious stance around near term rate cuts (i.e. in the next few months).

- The balance of risks points more towards easing at the end of the second half rather than the beginning.

- Full preview here:

SOUTH KOREA DATA: Business Sentiment Improves, But Large Manufacturers Outperforming

Earlier BOK business survey data for June painted a resilient picture across manufacturing and non-manufacturing sentiment. The manufacturing index rose to 76 from 74 in May, this is highs back to Q3 2022. The non-manufacturing index firmed to 72 from 71, levels seen in Q4 last year.

- The rate of ascent in these survey measures is fairly modest, particularly compared to the 2020 cycle. Still, up moves are likely to be welcomed by the authorities and it helps offset some of the recent downshift in headline consumer sentiment readings from a broader economic standpoint.

- In terms of the detail, on the manufacturing side, larger firms saw a spike in conditions to 86 from 81. SMEs actually saw a small fall. This probably points to the more externally focused firms doing better relative to those more domestically focused.

- This is reinforced by the domestic conditions at 73 from 72 prior, while the export outlook rose to 83 from 80. The chart below plots this export forecast against Souht Korean export growth in y/y terms.

- On the non-manufacturing side, we saw steadier outcomes in terms of sub-components, which is again consistent with these types of firms being more domestically focused.

Fig 1: South Korea Exports Y/Y & Manufacturing Export Outlook

Source: MNI - Market News/Bloomberg

ASIA FX: Steady Trends, BI Still To Come, BoK Tomorrow

USD/Asia pairs have had a relatively quiet session. Mixed trends have been evident, but tight ranges have prevailed in the first part of Wednesday trade. The yuan is a little weaker, but USD/CNH has not breached 7.2500. KRW rallied with the NZD post the hawkish RBNZ hold, but we have since pared gains. Still to come today is the BI decision, with no changes expected. Tomorrow, the BoK meeting in South Korea is also expected to deliver an unchanged outcome.

- USD/CNH has drifted a little higher, but remains sub 7.2500 for now. USD/CNY onshore spot is close to 7.2400. Equity trends have been close to flat, leaving little in the way of spill over for FX markets.

- 1 month USD/KRW got to lows near 1358 amid positive spill over from the NZD bounce post the hawkish RBNZ hold. However, there was no follow through. We sit back near 13060, slightly off end NY closing levels from Tuesday. Earlier data showed a slight pick up in PPI momentum, while the BOK survey of business sentiment showed large manufacturers outperforming.

- USD/HKD has stabilized somewhat following the recent break below the mid-point of the peg band. The pair was last around 7.8050. We sit below all key EMAs on a spot basis. The 20-day is the nearest, which is trending lower and last around 7.8125. US-HK yield differentials are trending lower, last at +60.5bps, albeit still in the USD's favor. This has been more reflective of higher HK rates, with the 3 month Hibor back to +4.78%, fresh highs going back to Jan. US front end yields remains very steady near 5.58%. Near term trends in spreads will continue to be dictated by the HK leg, as there seems little prospect of a meaningful shift lower in US front end.

- Elsewhere, trends have been steady. USD/PHP sits off recent highs, last near 58.17, but still comfortably above the 58.00 figure level. USD/IDR is hovering close to 16000, also little changed for the session.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/05/2024 | 0600/0700 | *** |  | UK | Consumer inflation report |

| 22/05/2024 | 0600/0700 | *** | | UK | Producer Prices |

| 22/05/2024 | 0600/0700 | *** | | UK | Public Sector Finances |

| 22/05/2024 | 0600/0800 | ** |  | SE | Unemployment |

| 22/05/2024 | 0805/1005 |  | EU | ECB's Lagarde at ESMA event on effectiveness of capital markets | |

| 22/05/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 22/05/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 22/05/2024 | 1245/1345 | | UK | BOE's Breeden Panellist on macroprudential policies | |

| 22/05/2024 | 1400/1000 | *** | | US | NAR existing home sales |

| 22/05/2024 | 1400/1000 | * | | US | Services Revenues |

| 22/05/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 22/05/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 22/05/2024 | 1800/1400 | *** | | US | FOMC Minutes |

| 23/05/2024 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.