Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

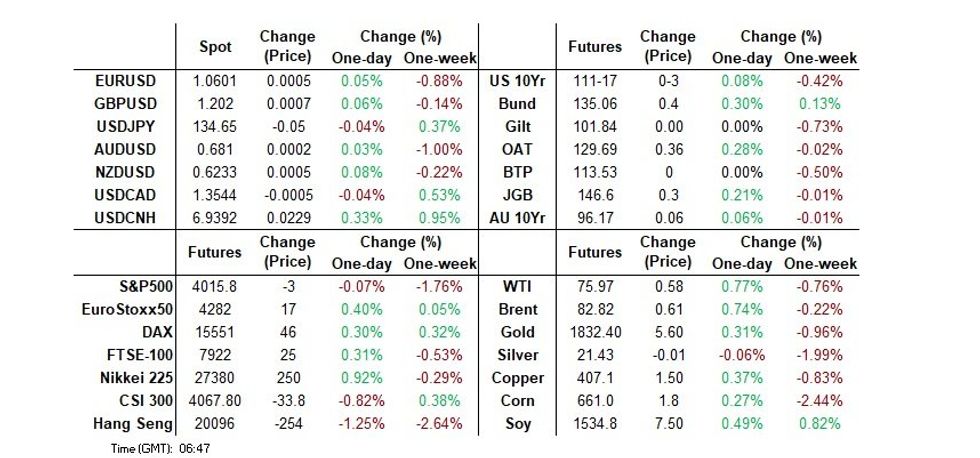

- JGBs sit just off best levels at the close, with futures +30 and cash JGBs running 0.5-4.0bp richer, with 20s presenting the firmest point on the curve. 10-Year JGB yields have dealt pretty much spot on the BoJ’s 0.50% YCC limit all day. Swap rates are 0.5-6.0bp lower, with swap spreads tightening across the curve. A lack of overt hawkish rhetoric in BoJ Governor-in-waiting Ueda’s initial nomination hearing allowed an early bid to extend. All in, Ueda seemed quite Kuroda-esque, stressing the need for continued monetary easing, with the initial impulse tempered by a hat tip towards the conditions that would facilitate the need for policy tweaks and an acknowledgement of the side effects of prolonged monetary easing.

- USD/JPY prints at ¥134.65/70. As Ueda was speaking the JPY initially pressured before paring gains and firming in a volatile trade. Ultimately USD/JPY found support ahead of ¥134.00 and the pair firmed to sit at current levels.

- Today we have a slew of U.S. data including personal income/spending, PCE deflator, U. of Mich consumer sentiment (final) and new home sales. There are also a number of Fed speakers scheduled to cross, as well as BoE's Tenreyro.

US TSYS: Marginally Richer In Asia

TYH3 deals at 111-15+, +0-01+, a range of 0-06 has been observed on volume of ~118K.

- Cash Tsys sit flat to 2bps richer across the major benchmarks, the curve flattened.

- Tsys largely tracked gyrations in JGBs as BOJ Governor Nominee Ueda faced parliament, an early bid spilled over seeing TY briefly look through yesterday's high.

- There was little follow through and Tsys retreated off best levels, dealing in a narrow range for the remainder of the session.

- BOJ Governor Nominee Ueda's comments were balanced, noting that there was no need for an immediate policy adjustment whilst also flagging the conditions that would facilitate the need for such a move in the future which capped gains in JGBs.

- BOJ-aside little meaningful macro headline flow crossed.

- The NY docket consists of a slew of U.S. data, including personal income/spending, PCE deflator, UofMich consumer sentiment (final) and new home sales. There a number of Fed speakers scheduled to cross, Fed Gov Waller is the highlight.

JGBS: Ueda Sticks To The Middle Lane, Supporting JGBs

JGBs sit just off best levels at the close, with futures +30 and cash JGBs running 0.5-4.0bp richer, with 20s presenting the firmest point on the curve. 10-Year JGB yields have dealt pretty much spot on the BoJ’s 0.50% YCC limit all day. Swap rates are 0.5-6.0bp lower, with swap spreads tightening across the curve.

- A lack of overt hawkish rhetoric in BoJ Governor-in-waiting Ueda’s initial nomination hearing allowed an early bid to extend. All in, Ueda seemed quite Kuroda-esque, stressing the need for continued monetary easing, with the initial impulse tempered by a hat tip towards the conditions that would facilitate the need for policy tweaks and an acknowledgement of the side effects of prolonged monetary easing.

- The nominees for the two BoJ Deputy Governor roles, Uchida & Himino, were also balanced, largely reflecting matters and ideas portrayed in Ueda’s speech, while Uchida pointed to methods to deal with the side effects of elongated policy easing, outside of an exit from easy policy.

- When it comes to the handover from the old BoJ leadership to the new there is seemingly a continued focus on generating wage growth to promote sustainable demand-pull inflation, in a bid to meet the BoJ’s inflation goal on a sustainable basis.

- National core CPI readings provided 0.1ppt misses in January, although all three of the major readings moved to fresh Y/Y cycle highs (Ueda suggested inflationary pressures would likely start to fade from February).

- Ueda, Himino & Uchida will appear in front of the upper house of parliament in their second round of confirmation hearings on Monday, with BoJ Rinban operations also slated.

AUSSIE BONDS: BOJ Talk & Well-Digested Supply Assists Mid-Session Reversal

Early weakness gives way to a bull flattening of the curve with YM +3.0 and XM +6.0 at the close. A JGB-inspired bid for ACGBs builds over the session, aided by U.S Tsys strength, leaving bonds 3-6bp stronger. Firm demand at the latest ACGB Nov-29auction wouldn't have done the bid any harm. 3/10 cash curve closes -2bp.

- AU/US cash yield differential closes at -3bp after touching flat early.

- Swaps, mirroring bonds, close at the day’s high with rates 2-6bp lower and the curve 3bp flatter.

- Bills are +1-4bp led by the reds.

- Subdued trading in RBA-dated OIS leaves pricing little changed on the day with a 95% chance of a 25bp hike priced for the March meeting and terminal rate pricing around ~4.28%.

- Next week sees the local calendar deliver a batch of quarterly partial releases leading up to the release of Q4 GDP on Wednesday. With WPI’s undershoot sparking an ACGB rally this week, the market will give the National Accounts’ Compensation of Employees measure a cursory glance to see if it tells a similar story. Monthly reads on January Retail Sales and Private Sector Credit are also due early in the week.

- Also on the calendar next week is the AOFM’s now standard issuance of A$1.5bn of ACGBs, split between A$300mn of ACGB May-47 on Monday & A$1.2bn of Nov-32 on Wednesday.

NZGBS: Selling Fatigue Sets In

NZGBs stage a sharp mid-session reversal after a 3-day weakening comes to an end. NZ Treasury comments, reinforced by the RBNZ Meeting and its subsequent communique, had managed to bring the cumulative rise in the 2-year yields this week to 35bp at the session’s cheaps. The 10-year yield had a similar rise fuelled by the threat of future NZGB supply. With the NZ-AU 10-year yield differential 30bp wider on the week domestic factors were clearly the dominant driver.

- It was however clear that selling fatigue had set in mid-session when hawkish comments from RBNZ Deputy Governor Silk were unable to hold yields at their highs. Silk stated that all options were on the table at the April meeting (25bp, 50bp or 75bp, but not a pause) and that the bank’s forecast for the peak cash rate “was not set in stone”.

- NZGBs close -1 to -3bp with the curve 2bp more inverted.

- Swaps underperformed bonds with the 2-year rate 4bp higher and the 2s10s curve 4bp more inverted.

- RBNZ dated-OIS closed unchanged with pricing for the April meeting at 39bp of tightening and terminal OCR at 5.46%.

- After this week's rise in yields, the market was clearly too complacent going into the RBNZ meeting. Today’s mid-session reversal suggests the market needs to catch its breath. Next week’s Antipodean data drop however threatens to make it a brief pause.

FOREX: Yen Volatile On Ueda Comments, Limited Ranges Elsewhere

Yen was volatile as BOJ Governor-Nominee Ueda appeared before the parliament, USD/JPY was dealt in ~100 pip range however Ueda was ultimately balanced in his commentary and the pair sits unchanged from yesterday's closed levels.

- USD/JPY prints at ¥134.65/70. As Ueda was speaking the JPY initially pressured before paring gains and firming in a volatile trade. Ultimately USD/JPY found support ahead of ¥134.00 and the pair firmed to sit at current levels.

- Kiwi marginally outperformed its G-10 peers, however there was little follow through on moves and NZD/USD continues to observe narrow ranges as it consolidates above $0.62. A large option expiry ($940mn) at $0.6250 may cap gains today. Early in the session RBNZ Assistant Gov Silk noted that there are still upside risks to inflation, the forecast terminal rate is not “set in stone” and all rate hike options are on the table for April meeting.

- AUD/USD is a touch firmer, last printing at $0.6810/15. Westpac lifted their terminal rate call to 4.1% from 3.85%, with 25bp hikes now seen in March, April and May.

- Weakness in CNH may also be capping gains in the Antipodeans. USD/CNH is ~0.4% firmer and dealing a touch below 6.94, onshore equities are lower as US-Sino tensions weigh.

- Elsewhere EUR and GBP are flat, with narrow ranges observed.

- Cross asset flows are mixed, US Equity Futures are a touch lower and BBDXY is marginally firmer. 10 Year US Treasury Yields are ~2bps lower.

- In Europe today GDP data from Germany provides the highlight. Further out we have a slew of U.S. data including personal income/spending, PCE deflator, U. of Mich consumer sentiment and new home sales. There are also a number of Fed speakers scheduled to cross.

FX OPTIONS: Expiries for Feb24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0535-50(E1.9bln), $1.0560(E548mln), $1.0600(E627mln), $1.0680-00(E2.7bln)

- USD/JPY: Y134.00($678mln), Y134.50($1.5bln)

- GBP/USD: $1.1950-52(Gbp510mln), $1.2200-10(Gbp644mln)

- AUD/USD: $0.6750(A$1.4bln), $0.6790-00(A$822mln)

- USD/CAD: C$1.3485-00($1.1bln)

- USD/CNY: Cny6.7000($1.6bln), Cny6.7180($1.4bln)

ASIA FX: ADXY Threatening Downside Test Of 200-Day MA

USD/Asia pairs are higher today, with Asian FX underperforming the steady to slightly weaker USD trend evident in the majors. USD/CNH has continued to track higher, breaching the 6.9400 level, before selling interest emerged. Regional equities are mostly on the back foot. The J.P. Morgan ADXY index is close to its simple 200-day MA, see the chart below. The data calendar is quiet in the first part of next week, Indian Q4 GDP prints on Tuesday, then China PMIs are due on Wednesday.

- USD/CNH has kicked higher after breaking its simple 200-day MA (6.9091). The pair touched a higher of 6.9450, but we now sit slightly lower at 6.9380/85. There is no push back from the CNY fixing bias to the weaker yuan trend. Onshore equities continue to correct, the CSI 300 down another 1.00%, while northbound stock outflows are also evident. US-China tensions are likely weighing on China related asset sentiment.

- 1 month USD/KRW is back above 1300, although hasn't made fresh highs. USD/JPY supported on dips, coupled with higher USD/CNH levels, has likely weighed on won sentiment today. USD/TWD is also higher, last near 30.48, with KRW and TWD hurt by weaker local equities as well.

- The SGD NEER (per Goldman Sachs estimates) is marginally firmer today, the measure dipped yesterday after softer than expected Jan CPI. NEER currently sits around ~0.6% below the top of the trading band. USD/SGD is little changed today, last printing at $1.3420/30. The close above $1.34 opens the 200-Day EMA at $1.3636 for Bulls. Downside support comes in at 2023 lows ($1.3098). IP figures remained around recent levels in terms of y/y momentum, -2.7%, but the m/m was better than expected.

- USD/THB continues to track higher. The pair up a further 0.40% so far today, around the 34.80 level, with baht erasing its YTD gains in recent sessions. The 200-day EMA is not too far above current levels (34.85), beyond that rests the 35.00 figure level. Broader USD sentiment has clearly turned around, although the THB NEER (J.P. Morgan Index) has lost 3.7% from late Jan highs, but remains comfortably above July 2022 lows. Onshore equities continue to weaken, down a further 0.80% so far today, with the SET index also eroding YTD gains. Offshore investors have sold nearly $1bn of local equities in Feb to date, with nearly half the outflows coming in the past week.

Fig 1: ADXY Approaching 200-Day MA

Source: J.P. Morgan/MNI - Market News/Bloomberg

EQUITIES: Japan Outperforms, HK Tech Back Below 200-Day MA

(MNI Australia) Regional equities are a mixed bag today. Japan stocks have outperformed as Ueda's confirmation hearing took place. China and HK equities have continued to weaken though. US futures are modestly lower, but ranges have been tight overall, ahead of key US inflation data later.

- The Nikkei 225 is tracking +1.15% higher at this stage. New BoJ Governor nominee Ueda struck a balanced tone, with no shocks relative to market expectations. USD/JPY dips were generally supported, with Ueda not hinting at any imminent policy shifts.

- The HSI is off around 1.20% at this stage, with the tech sector down 2% at this stage and the index is tracking below its 200-day MA. Mixed earning results and greater competition concerns has clouded the tech backdrop this week.

- The CSI 300 also continues to correct lower, last down -0.90%. On-going tensions with the US, reflecting both Taiwan (potential for more US troops to be based there, although Taiwan officials denied this) and Ukraine issues (extent of alleged China support) are likely weighing at the margin as well.

- The Kospi (-0.50%) and Taiex (-0.25%) are both lower as well. Thailand stocks remain underperformers, down 1% at one stage. Offshore investors continue to sell Thai stocks (nearly $1bn in outflows in Feb to date).

GOLD: Support Evident Around $1820 Ahead Of Key US Data

Gold is modestly higher so far today, tracking +0.20%, to be back around the $1825.70 region. This would be the first daily gain in the precious metal since the end of last week. At this stage we are still -0.90% lower for the week.

- Some support is evident sub the $1820 level, which we saw on Thursday's session. This level was also a support point on Feb 17, so is likely to be eyed in the near term, particularly with further key US data out later today (PCE deflator and U. of Mich Sentiment).

- Gold continues to track broader USD indices closely, while gold ETF holdings remain on a downtrend.

OIL: Brent Support Evident Ahead Of $80/bbl, Holding Steady In Terms Weekly Change

Brent crude has continued to recover today, last near $83.00/bbl. This puts us +0.95% above NY closing levels and follows Thursday's +2% gain. Support appears evident for Brent around the $80/bbl level, as we haven't spent much time below this level in February. Brent is close to unchanged versus closing levels from last week. For WTI, we are back above $76.00/bbl.

- Overall, oil trends still look to be in somewhat of a holding pattern. Dips broadly remain supported, while prompt spreads continue to suggest tightness from a supply point.

- This is a little at odds with the continued rise in US inventory levels though.

- The market may also be waiting for greater clarity around the China outlook/policies from the upcoming National People's Congress.

- From a technical standpoint, the 20 and 50-day EMAs are above ($83.70 & $84.3), but arguably we need to break above the 100-day ($86.70) to form a more constructive outlook.

- Outside of tonight's US data (PCE and U. Of Mich Sentiment) next week EU energy ministers hold an informal meeting on Monday energy security. Then on Tuesday Internation Energy Week kicks off from London. Wednesday sees China PMIs for Feb.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/02/2023 | 0700/0800 | *** |  | DE | GDP (f) |

| 24/02/2023 | 0700/0800 | * | | DE | GFK Consumer Climate |

| 24/02/2023 | 0745/0845 | ** |  | FR | Consumer Sentiment |

| 24/02/2023 | 0800/0900 | ** |  | SE | Economic Tendency Indicator |

| 24/02/2023 | 0800/0900 | ** |  | ES | PPI |

| 24/02/2023 | - |  | EU | ECB Lagarde & Panetta at G20 Finance Minister Meet | |

| 24/02/2023 | 1330/0830 | ** |  | US | WASDE Weekly Import/Export |

| 24/02/2023 | 1330/0830 | ** | | US | Personal Income and Consumption |

| 24/02/2023 | 1500/1000 | *** | | US | New Home Sales |

| 24/02/2023 | 1500/1000 | *** | | US | Final Michigan Sentiment Index |

| 24/02/2023 | 1515/1015 | | US | Fed Governor Philip Jefferson | |

| 24/02/2023 | 1515/1015 | | US | Cleveland Fed's Loretta Mester | |

| 24/02/2023 | 1600/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 24/02/2023 | 1630/1130 | | US | St. Louis Fed's James Bullard | |

| 24/02/2023 | 1630/1630 |  | UK | BOE Tenreyro Panellist at NY Fed | |

| 24/02/2023 | 1830/1330 | | US | Boston Fed's Susan Collins | |

| 24/02/2023 | 1830/1330 | | US | Fed Governor Christopher Waller |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.