Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

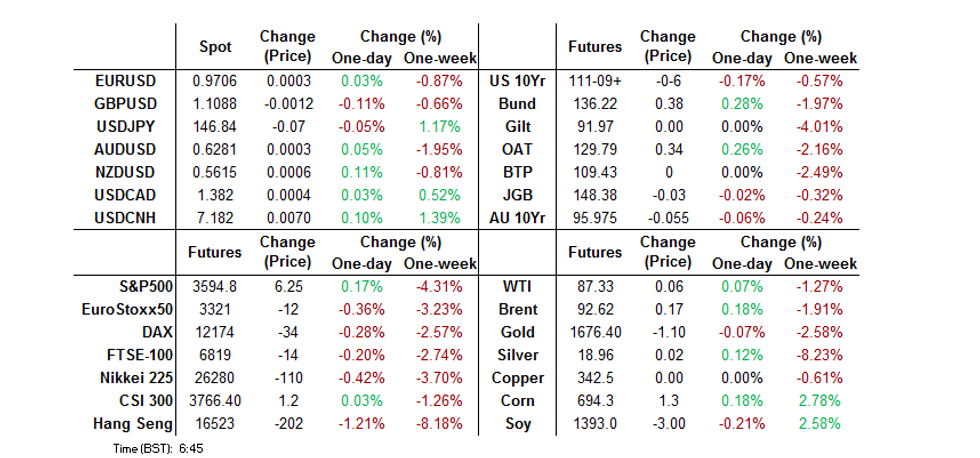

- The yen was in the spotlight after USD/JPY breached prior intervention levels on Wednesday and kept climbing as BoJ Gov Kuroda reaffirmed the central bank's dovish credentials. The rate got some reprieve in early Asia trade, but clawed back losses into the Tokyo fix and still operates within touching distance from the Y147.00 mark. Japanese FinMin Suzuki reiterated that officials are focusing on volatility rather than specific levels of the exchange rate and stand ready to take bold action if they see excessive moves. USD/JPY overnight implied volatility extended yesterday's upswing to 22.4%.

- The U.S. CPI report provides the highlight of today's session, with headline inflation expected to have slowed to +8.1% Y/Y in September, per a Bloomberg survey. The data will inform the debate on Fed tightening outlook. As things stand, another 75b rate hike is virtually fully priced for the November FOMC meeting.

- Other notable data releases include U.S. jobless claims, as well as German (final) and Swedish CPI figures. Speeches are due from ECB's Nagel & Riksbank's Breman.

MNI US CPI Preview: Upside Risk To Solid Core CPI Consensus

EXECUTIVE SUMMARY

- Core CPI inflation is seen slowing only moderately to 0.4% M/M after the surprise jump to 0.57% in August, and with analysts seeing some upside risk.

- A large part of this expected relative slowing is from used car prices with underlying strength in core services expected to remain a key trend, especially in shelter before rent growth begins to cool.

- With prior Fedspeak seeing no sign of inflation peaking and an u/e rate at historical lows, an extremely large miss is required to knock the Fed off course from a fourth 75bp hike on Nov 2 (74bp priced).

- There are greater implications for Dec and Feb meetings, which currently show a broad scaling back to 50bp and 25bp hikes, along with current pricing of a rate cut in 2H23. A beat could see a bear flattening in Treasuries, helped by the notable resistance around 4% 10Y yields, and continued USD strength.

- Click for full preview:USCPIPrevOct2022.pdf

US TSYS: Modest Cheapening Overnight, CPI Eyed

Spill over from weakness in ACGBs coupled with block sales in FV & TY futures applied some light pressure in pre-CPI Asia-Pac trade, leaving the major cash Tsy benchmarks 1.0-2.5bp cheaper as we moved towards London hours, with modest bear steepening of the curve in play.

- TYZ2 deals 0-06+ cheaper on the session, printing 111-09, 0-00+ off the base of its 0-08+ session range, on limited volume of ~59K.

- There hasn’t been much in the way of meaningful headline flow cross, outside of Fed Governor Bowman flagging uncertainty re: the required terminal rate of the current hiking cycle, as she reaffirmed the prospect of sizable hikes until inflation falls, alongside the need for restrictive policy settings for some time.

- FOMC dated OIS currently prices a terminal rate of ~4.65%, with ~74bp of tightening priced for next month’s FOMC.

- The previously flagged block sales in FV (-2K) & TY (-2.5K, -1.5K & -1.6K) futures were also accompanied by a block buyer of TYX2 110.00 puts (+5K)

- Gilt market gyrations and the impending U.S. CPI report provide the two focal points on Thursday, (see our full preview of the CPI release here). Elsewhere, weekly jobless claims data, 30-Year Tsy supply and Fedpseak from Waller, Cook & George will hit during NY hours.

JGBS: Twist Flattens, Possibly Aided By Lifers Being Active In Long End

The JGB curve twist flattened during the Tokyo morning, with domestic life insurers and pension funds perhaps eying the multi-year high ~120bp pickup for 30-Year yields over 10s as an entry point.

- Although it is hard to be certain of that dynamic given the lack of demand at Wednesday’s soft 30-Year auction.

- Spill over from Wednesday’s late UK Gilt/U.S. Tsy bid may also be supporting longer dated paper.

- Still, a modest downtick in U.S. Tsys during the Tokyo session has seemingly applied pressure to paper out to 7s, as well as JGB futures, with the major cash benchmarks in that zone running ~1bp cheaper on the day, while futures stick to a narrow range, last -3.

- Firmer than expected domestic PPI data likely played into the weakness in the sub-10-Year zone.

- BBG recently flagged that cash 10s have traded, breaking a run of 4 consecutive untraded sessions.

- Friday’s local docket is headlined by 5-Year JGB supply, with the latest round of weekly international security flow data from the MoF also set to provide the usual interest.

AUSSIE BONDS: Curve Steeper, U.S. CPI Eyed

Aussie bonds came under some steepening pressure on Thursday, leaving YM +0.5 & XM -4.5 ahead of the close, as wider cash ACGB trade sees 0.5bp of richening to 5.0bp of cheapening, with a pivot around 5s and a parallel shift in the 10+-Year zone.

- There wasn’t an overt driver for the move, leaving us to suggest that the lack of willingness to force a meaningful move below the 0bp level in the AU/U.S. 10-Year yield spread may be at the fore, with the latest bounce away from that level observed in Sydney trade, alongside the early weakness in ACGBs, before a correction off of worst levels.

- Bills run +2 to 1 through the reds, with RBA dated OIS pricing a terminal rate of ~3.95%, little changed on the day.

- Melbourne Institute inflation expectations data was unchanged at 5.4% in October, with the reading operating a little over 1.0ppt off its cycle peak.

- Looking ahead, Friday will see a A$700mn of ACGB Apr-27 supply, the release of the weekly AOFM issuance slate and local reaction to Thursday’s U.S. CPI print.

AUSTRALIA: Inflation Expectations Remain Anchored

The Melbourne-Institute’s measure of consumer inflation expectations was stable in October at 5.4%, despite the rise in petrol prices during the month.

- This is consistent with the RBA’s regular statement that inflation expectations continue to be anchored. Consumers seem to believe that the current monetary tightening cycle will be successful in reining in inflation.

- While +5% inflation is still too high, the stability in expectations supports the pivot to a slower pace of hiking.

- Inflation expectations are pointing to a pick up in Q3 CPI and while it is still very early in Q4, there could be a stabilisation in the final quarter of 2022.

Source: MNI - Market News, Refinitiv, Melbourne Institute

AUSTRALIA: RBA Hikes Not Yet Dampening Retail Spending

The National Retail Association (ARA)/Retail Doctor Group have published their 2022 Consumer Sentiment Report. It reveals that while consumers are changing their consumption behaviour, they are generally optimistic about the upcoming festive spending season.

- The ARA and Roy Morgan are forecasting that pre-Christmas sales will be up 3% on last year, according to The Australian. 250bp of rate hikes year to date appear not to have dampened household expenditure going into year end.

- ARA chief executive Zahra noted that consumers continue to spend and that there is “a sense of prosperity”. He thinks they are working through their savings and holidaying domestically as overseas travel costs are up 30%, reported by The Australian. If these trends continue, then the RBA’s tightening cycle could be prolonged.

- The ARA survey found that 71% of consumers have changed their spending behaviour or plan to because of inflation. The main ways they’ll do this is to cut back on non-essentials and look for more discounts and better prices. People are prepared to reduce expenditure to be able to spend more on special occasions.

- 46% are very or somewhat confident leading up to the Christmas shopping season with 20% expecting to spend more this year than last.

Source: MNI - Market News, ABS, CBA

NZGBS: A Little Flatter, Off Best Levels

NZGBs moved away from best levels as ACGBs and U.S. Tsys traded a little softer during Thursday’s Asia-Pac session, leaving the major benchmarks 1-3bp richer on the day come the bell, with some light bull flattening in play.

- NZGBs did regain some poise, moving away from worst levels, even with payside flow evident in swaps, which resulted in swap spread widening on the session.

- The latest round of NZGB supply (consisting of Apr-25, May-32 & May-41) saw firmer demand for the longer-dated paper on offer (cover ratios of 1.68x, 2.11x and 2.78x), which aided the flattening dynamic. Lower cover for the shorter-dated paper on offer was perhaps a function of uncertainty re: monetary policy and ongoing market vol.

- RBNZ dated OIS continues to price a terminal OCR of ~4.90%, little changed on the day.

- Friday’s domestic docket will be headlined by m’fing PMI data, although catch up to core FI market gyrations in lieu of the impending the U.S. CPI print will probably provide more market impact during the early rounds of Friday dealing.

FOREX: Yen Takes Focus, Tight Ranges Observed Ahead Of U.S. CPI

The yen was in the spotlight after USD/JPY breached prior intervention levels on Wednesday and kept climbing as BoJ Gov Kuroda reaffirmed the central bank's dovish credentials. The rate got some reprieve in early Asia trade, but clawed back losses into the Tokyo fix and still operates within touching distance from the Y147.00 mark.

- Japanese FinMin Suzuki reiterated that officials are focusing on volatility rather than specific levels of the exchange rate and stand ready to take bold action if they see excessive moves. USD/JPY overnight implied volatility extended yesterday's upswing to 22.4%.

- Sterling traded on a heavier footing, with uncertainty surrounding the UK's fiscal outlook still causing reverberations in the FX market.

- The U.S. CPI report provides the highlight of today's session, with headline inflation expected to have slowed to +8.1% Y/Y in September, per a Bloomberg survey. The data will inform the debate on Fed tightening outlook. As things stand, another 75b rate hike is virtually fully priced for the November FOMC meeting.

- Other notable data releases include U.S. jobless claims, as well as German and Swedish CPI figures. Speeches are due from ECB's Nagel & Riksbank's Breman.

ASIA FX: South Korean Won Slips Amid Rangebound Trade In Emerging Asia

South Korean won paced losses while most USD/Asia crosses held tight ranges ahead of the release of U.S. CPI figures, a key input to the debate on Fed tightening outlook.

- USD/CNH showed some weakness in early dealing before staging a rebound. The PBOC set the mid-point of permitted USD/CNY trading band below Bloomberg consensus for the 31st consecutive day, with the fixing error narrowing to -468 pips. The actual reference rate was little changed from the previous day, as officials fixed it in the vicinity of CNY7.1 for the seventh session in a row.

- KRW was the worst performer in emerging Asia after a strong Wednesday's session. Geopolitical concerns weighed on the won as North Korea said its nuclear units test-launched two long-range cruise missiles in a drill overseen by Kim Jong-un. Both KOSPI and KOSDAQ sank on a negative lead from European/U.S. equity markets.

- Spot USD/IDR steadied, with participants looking for fresh catalysts. Palm oil futures were marginally firmer, while the aggregate BBG Commodity Index oscillated around neutral levels.

- Spot USD/MYR refreshed 24-year highs, despite the release of above-forecast industrial output data on Wednesday.

- Spot USD/PHP traded in the vicinity of the PHP59 record high despite yesterday's comments from BSP Gov Medalla, who said that the peso's depreciation is accentuating inflationary pressures and "strengthens the case to act and to act decisively."

MNI MAS Preview - October 2022: Further Tightening Via Re-Centering, Double Tightening Can’t Be Ruled Out

EXECUTIVE SUMMARY

- This Friday is expected to deliver another tightening from the MAS. Much like BoK this week, the main question is how much the MAS will deliver. The hawkish views from the side-sell rest with both a re-centering of the NEER higher, coupled with a further lift in the rate annual NEER appreciation. Our view rests with a re-centering higher of the NEER (most likely to the prevailing level).

- With inflation continuing to surprise on the upside, the risks of another double tightening can’t be underestimated though. The risks are that the core inflation backdrop for the MAS may be stronger than the recently revised projection higher for 2022. A continued recovery in the domestic economy, coupled with a tight labour market, skews the core inflation outlook higher in the near term.

- The case for a less aggressive policy reaction, i.e. just a re-centering in the NEER higher, and leaving the rate of NEER appreciation unchanged, largely rests on uncertainties surrounding the growth outlook.

- Click for full preview: MAS Preview - October 2022.pdf

EQUITIES: Major Indices Mostly Lower In Asia

The MSCI Asia-Pacific Index is on track to record a fifth consecutive day of losses, with the negative lead from Wall St., worry re: the impending U.S. CPI print and continued woes for Chinese tech names, stemming from Sino-U.S. tensions, applying pressure to the space during Thursday dealing.

- The Hang Seng leads the way lower, last dealing 1.0% softer on the day.

- The latest, albeit well telegraphed, property developer debt default out of China got plenty of airtime.

- The ASX 200 has bucked the regional trend, adding a mere 0.1%, with guidance from Qantas supporting names linked to tourism, while financials benefited from Bank of Queensland’s earnings report. Still, a heavy day for real estate-linked names limited gains.

- The 3 major U.S. e-mini contracts are essentially unchanged on the day.

OIL: Global Growth Fears Driving Market, Watch US CPI

Oil prices are little changed from overnight trading and have been range trading ahead of the US September CPI data later. WTI has been in the tight range of $87.00-87.50/bbl, now at $87.11, and Brent $92.45-$92.90 and is currently $92.43/bbl.

- WTI has broken through both its 5- and 50-day moving averages and is now headed towards the 20-day MA.

- Global growth concerns have been weighing on commodities generally, as markets are expecting demand to fall. Confirming these fears OPEC cut its oil demand forecasts for 2022 and 2023. US and Japanese crude inventories rose in the latest data. These concerns have been driving the unwinding of last week’s output-driven rally.

- There was further talk regarding US plans to impose a price cap on oil from Russia. Bloomberg reported that some US officials are concerned that the strategy will actually cause a jump in oil prices, as Russian President Putin has said he won’t supply anyone who participates in the cap. It remains a very sensitive issue.

GOLD: Coiling Into U.S. CPI

Asia-Pac trade has seen spot gold stick within the confines of the narrow range established over the last couple of sessions, last dealing little changed, just below $1,670/oz.

- The broader USD remains within touching distance of cycle highs, with our weighted U.S. real yield monitor exhibiting a similar dynamic.

- The impending U.S. CPI print presents the next major macro risk event and will cross early in the NY morning.

- Market participants are assessing the potential terminal rate of the current Fed hiking cycle (last priced at ~4.65%, per dated OIS) , with the swift monetary tightening deployed YtD more than offsetting well-documented geopolitical worries, leaving gold ~19% off its YtD high, or the best part of 9% lower YtD.

- The initial technical support and resistance lines are well defined. The 3 Oct low ($1,659.7/oz) protects key support at the YtD base ($1,615.0/oz). Meanwhile, initial resistance is seen at the Oct 4 high ($1,729.5/oz)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/10/2022 | 0600/0800 | *** |  | DE | HICP (f) |

| 13/10/2022 | 0600/0800 | *** |  | SE | Inflation report |

| 13/10/2022 | 0730/0930 |  | EU | ECB de Guindos Speech at (M&A) España y Europa Event | |

| 13/10/2022 | - | | EU | ECB Lagarde & Panetta IMF/World Bank Annual Meetings | |

| 13/10/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 13/10/2022 | 1230/0830 | *** | | US | CPI |

| 13/10/2022 | 1300/1400 |  | UK | BOE Mann Speech at Peterson Institute for Internat. Economics | |

| 13/10/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 13/10/2022 | 1500/1100 | ** | | US | DOE weekly crude oil stocks |

| 13/10/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 13/10/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 13/10/2022 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 13/10/2022 | 1700/1300 | | US | Atlanta Fed Raphael Bostic | |

| 13/10/2022 | 1800/1400 | ** | | US | Treasury Budget |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.