Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

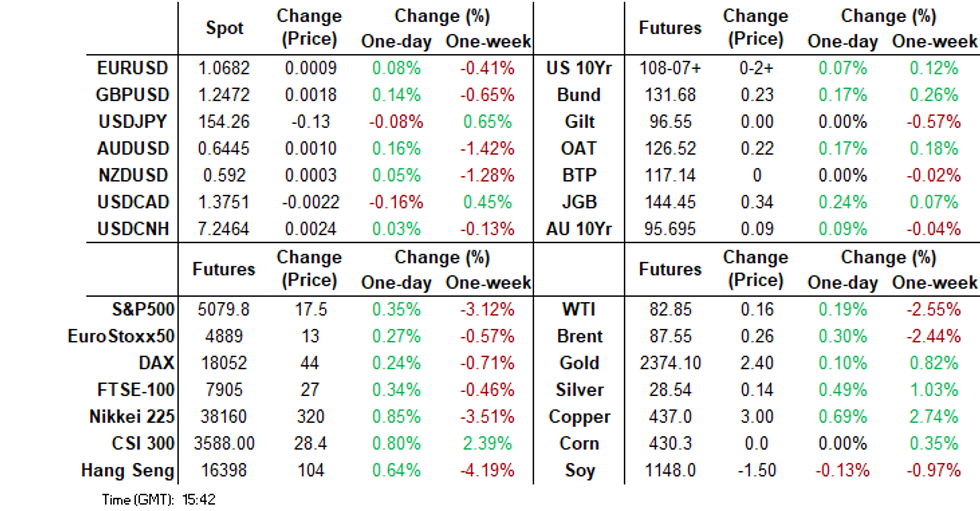

- US Tsy futures broke above Wednesday highs despite some earlier hawkish Fed remarks earlier. This weighed on broader USD sentiment, although overall G10 moves have been modest. The yen gained some support as headlines crossed that the G7 is in agreement that excessive FX moves are not desirable, but dips sub 154.00 were supported. The USD was also weaker against Asia FX, although CNH remained steady.

- In Australia, ACGBs (YM +5.0 & XM +8.0) are 2-4bps richer after the release of the Employment Report for March, which showed an unexpected drop. Still, the RBA focusses on a number of particular labour market indicators and while some still show gradual easing in the labour market continuing, a number have stalled. In aggregate, they point to some stabilisation in Q1 from the previous gradual easing, and so the RBA’s stance is unlikely to change for now.

- Later the Fed’s Bowman, Williams, Bostic and Collins, ECB’s de Guindos and Schnabel, and BoE’s Greene appear. IMF meetings continue and the Eurogroup meets. US jobless claims and April Philly Fed print.

MARKETS

US TSYS: Treasury Futures Off Intraday Highs, Job Claims & Home Sales

- Jun'24 10Y futures broke above Wednesday's higher earlier making a high of 108-09+, we are just off those levels at 108-07+ up + 02+ from NY closing levels. Earlier there was a 2/5/30 Fly block trade, while a 2y/10y block flattener has traded.

- Cash Treasury yields have reversed earlier moves and now trade 1-2bps lower, the 2Y yield -0.8bps at 4.924%, 10Y -1.6bps to 4.571%, while the 2y10y is -0.822 at -35.519

- (MNI) Fed Well-Positioned To Wait, Gather Data - Mester (See Link)

- Earlier, Fed's Bowman acknowledges that progress on inflation has slowed, if not stalled, despite strong economic conditions and ongoing job growth, suggesting that current monetary policy may be restrictive, but its sufficiency remains uncertain. She notes that consumers may be adjusting spending habits, trading down to lower goods while also spending large amounts on experiences like travel.

- Projected rate cut pricing steady vs. late Tuesday levels: May 2024 steady at -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 steady at -16.2% w/ cumulative rate cut -4.7bp at 5.282%. July'24 cumulative at -12.6bp, Sep'24 cumulative -24.9bp.

- Looking ahead: Weekly Claims, Exist Home Sales, Fed Speak from NY Fed Williams, Atlanta Fed Bostic and Boston Fed Collins.

JGBS: Futures Richer & At Session Highs, National CPI For March Tomorrow

JGB futures are holding stronger and at the top of today’s range, +23 compared to the settlement levels.

- Tertiary Industry Index for February printed +1.5% m/m versus +0.5% est and -0.5% (revised) prior. Today, the local calendar also sees later Tokyo Condominiums for Sale and Machine Tool Orders.

- (MNI ICYMI) BoJ board member Asahi Noguchi said on Thursday that the pace of raising the policy interest rate will be very slow as it takes considerable time for inflation to continue increasing as a trend.

- The BoJ must maintain accommodative monetary policy not only to keep favourable labour market conditions but also to achieve its inflation target, he added.

- Noguchi was against ending the negative interest rate and yield curve control policy simultaneously at the March meeting, he told business leaders in Saga City.

- The cash JGB curve has slightly bull-flattened, with yields flat to 2bps lower. The benchmark 10-year yield is 0.2bp lower at 0.881% versus the YTD high of 0.891% set yesterday.

- Swap rates are ~1bp lower across maturities. Swap spreads are tighter out to the 10-year and wider beyond.

- Tomorrow, the local calendar will see National CPI data for March.

AUSSIE BONDS: Richer After Jobs Report, Next Key Release Is Wednesday’s Q1 CPI

ACGBs (YM +5.0 & XM +8.0) are 2-4bps richer after the release of the Employment Report for March. Employment fell 6,585 m/m (estimate +10.0k) in March versus a revised +117.6k in February. The Jobless rate rose to 3.8% (3.9% est) from 3.7% in February.

- Employment growth slowed to 2.7% y/y in Q1 from 3.0% in Q4 – the RBA is forecasting 2.0% for Q2. Job creation rose in Q1 with 122.3k new positions after Q4’s 52.9k but below Q1 2023’s 157k.

- Hours worked posted their second straight increase in March to be marginally higher on the quarter and up 1.7% y/y with the strength again concentrated in FT. Underemployment fell 0.1pp as a result.

- Overall, today's data showed that the labour market remained tight, so the RBA’s stance is unlikely to change.

- Cash ACGBs are 6-8bps richer, with the AU-US 10-year yield differential 1bp higher at -27bps.

- Swap rates are 5-8bps lower, with the 3s10s curve flatter.

- The bills strip has bull-flattened, with pricing +1to +7.

- RBA-dated OIS pricing is 3-5bps softer for meetings beyond September. A cumulative 17bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty. The next key release is Wednesday’s Q1 CPI.

RBA: Labour Market Points To On Hold RBA

The RBA focusses on a number of particular labour market indicators and while some still show gradual easing in the labour market continuing, a number have stalled. In aggregate, they point to some stabilisation in Q1 from the previous gradual easing, and so the RBA’s stance is unlikely to change for now.

- The Q1 NAB business survey was also released today and showed that the “availability of suitable labour as a severe output constraint” improved 2.4pp to be now 22pp from its most severe but labour shortages remain with the series still 9pp above the historical average.

Source: MNI - Market News/Refinitiv

- Unemployment rates have been volatile. March was 0.1pp below December but it is 0.4pp above the October 2022 trough. Youth unemployment rose 0.5pp to 9.6% in March and stands 2.4pp above the July 2022 trough. The RBA sees it as a leading indicator of the labour market.

Source: MNI - Market News/ABS

- With hours worked recovering in Q1, the underemployment rate has stabilised with Q1 less than 0.1pp higher than Q4 and still very low at 6.6% (3-month average).

- While vacancies-to-unemployment remain elevated, the ratio is well off its high falling 3.5pp in Q1 to 64.3%. It reached a peak of 91.8% in Q3 2022.

AUSTRALIAN DATA: Gradual Labour Market Easing Stalled In Q1

The headline March jobs figure was weaker than expected showing employment down 6.6k but February was revised up 1.1k to 117.6k. Some payback was expected and given February’s outsized reading, but it was relatively muted and importantly focused in part-time jobs with full-time continuing to rise. The unemployment rate rose 0.1pp to 3.8%. Data show that the labour market remains tight and so the RBA’s stance is unlikely to change.

- The April employment report on May 16 might not give greater clarity on underlying labour conditions as it could be impacted by school holidays, as April 2023 was. Therefore it is important to look through the monthly volatility at averages and quarterly changes.

- The economy generated just over 10k more jobs in Q1 than the increase in the labour force, thus signalling that despite slower growth labour demand remains robust. The shift back towards full-time jobs and the increase in hours worked are consistent with this.

- Employment growth slowed to 2.7% y/y in Q1 from 3.0% in Q4 – the RBA is forecasting 2.0% for Q2. Job creation rose in Q1 with 122.3k new positions after Q4’s 52.9k but below Q1 2023’s 157k. Employment growth shifted back towards full-time (FT), signalling improved employer confidence. FT rose 125.9k in Q1 (Q4 -44.3k) whereas part-time (PT) fell 3.7k (Q4 +97.3k), the first drop since Q4 2022.

- Hours worked posted their second straight increase in March to be marginally higher on the quarter and up 1.7% y/y with the strength again concentrated in FT. Underemployment fell 0.1pp as a result.

- The decline in employment with the 0.1% m/m rise in the labour force meant that the unemployment rate ticked up after its sharp February fall. But it was a high 3.8% coming in at 3.843%, so not far from consensus’ 3.9% and prone to an upward revision next month. The RBA expects 4.2% in Q2.

Source: MNI - Market News/ABS

AU/NZ DATA: Strong NZ Domestic Inflation May Also Show In Australia’s Q1 Data

There is a high correlation between Australian and NZ annual CPI inflation across the major components. The NZ Q1 data showed headline inflation moving closer to the top of the band in line with expectations at 4.0% y/y. But most commentators, including MNI, were concerned with the strength and stickiness of the domestically-driven non-tradeables component which rose 5.8% y/y. There is a risk that this will be repeated when the Australian data is released on April 24.

- The RBA said that most of the benefit from lower goods prices in bringing inflation down is behind us and so it requires lower services inflation to return CPI to target. The NZ data showed that it is still goods prices reducing overall inflation.

- In Q4, the 3-year rolling correlation between Australian and NZ headline CPI was 90%. Given this, helpful base effects and the 3.4% January/February average, a similar moderation in Australian Q1 CPI is possible.

- The RBNZ’s Q1 measure of underlying inflation eased 0.4pp to 4.3% y/y and given the correlation with Australia is above 95%, core is also likely to ease considerably in Australia. The monthly data is consistent with this too.

- In NZ, the area of concern is domestic inflation and the RBA is also focused on sticky services prices. With NZ non-tradeables moderating only 0.1pp in Q1 and still elevated and services rising 5.3% y/y, there is a risk that there will be little improvement in Australia’s services CPI which printed at 4.6% y/y in Q4 and has a correlation with NZ of over 80%. Non-tradeables have a correlation of close to 90%.

Source: MNI - Market News/Refinitiv

NZGBS: Closed On A Positive Note, Tracking US Tsys With The Local Calendar Empty

NZGBs ended the day on a positive note, with benchmark yields down by 6-7bps. This outcome is notable considering the mixed demand metrics observed during today's weekly supply. Cover ratios varied from 2.02x for the May-51 bond to 3.42x for the May-32 bond.

- With the domestic market devoid of data today, the strengthening in today’s session mirrored the robust performance seen in US tsys overnight, which has extended into today's Asia-Pacific session. Cash US tsys have gained approximately 2bps across benchmarks.

- Furthermore, there is likely some positive spill-over effect from ACGBs, which have strengthened by 4-5bps following the release of the March Employment Report.

- Swap rates closed 5-6bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed is 3bps softer for meetings beyond August. A cumulative 52bps of easing is priced by year-end.

- The local calendar is empty again tomorrow. The next major release is Trade Balance data for March on Wednesday.

- Today’s US calendar will see Weekly Claims, Existing Home Sales and Fed Speak including Bostic and Collins.

FOREX: Dollar Weakness Continues Amid Lower Yields, A$ Aided By Higher Equities/Iron Ore Surge

The BBDXY sits a touch above session lows, the index last near 1260.20 (still off -0.15% for the session). US yields sit lower across the board, with 2 to 10yr benchmark yields down a little over 2bps. This reversed earlier momentum where yields tried to go higher post some hawkish Fed speak.

- These moves have weighed on USD sentiment, with 10yr Tsy futures above Wednesday highs.

- USD/JPY got sub 154.00, aided by headlines from currency chief Kanda that the G7 is in agreement that excessive FX moves are harmful for economies.

- We have since rebounded though back to 154.25/30. A better regional equity tone has likely weighed on yen performance versus crosses. We had dovish remarks from BoJ board member Noguchi earlier, but they didn't shift the sentiment needle.

- AUD/USD is up +0.25%, tracking just above 0.6450. The pair shrugged off the jobs miss (although other detail was mixed), with the better equity tone and higher iron ore prices providing support.

- NZD/USD is also higher, lagging AUD a touch, the pair last near 0.5925. EUR/USD was last near 1.0680.

- Looking ahead, US jobless claims, Philly Fed manufacturing and existing home sales are all scheduled. Further Fed speak is also due.

ASIA EQUITIES: HK & China Equities Erase Earlier Losses, Small-Cap Bounce

Hong Kong and China equity are higher today, with Hong Kong equities outperforming. It has been a quiet day for markets in terms of news and data flow. Moody's has downgraded China Oversea Land to Baa2, the UK is looking at imposing new restrictions on AI technology on countries like Russian and China. Some Chinese companies have revised down earnings due to tighter regulations, Taiwan Semiconductor Manufacturing Co will released earnings later today.

- Hong Kong equities have recovered from their opening levels with the Mainland Property Index now now up 1.30% after opening 0.80% lower, the HSTech Index has erased earlier losses to now trade up 1.14%, tech stocks throughout the region have bounce off earlier lows and the market eagerly awaits TSMC earnings, while the wider HSI is now up 1.23%. In China, equities are lagging the move higher by HK equities with the CSI300 up just 0.57%, while smaller-cap indices including are outperforming large-cap with the CSI2000 up 1.10% and the CSI1000 up 1.00%

- China Northbound saw an outflow of 0.23b on Wednesday, with the 5-day average at -0.05billion, while the 20-day average sits at -0.11billion yuan.

- In the property space, Moody's downgraded China Overseas Land's long-term rating to Baa2 from Baa1, with the outlook revised to stable from negative. The downgrade reflects concerns that COLI's credit metrics may not recover amid the extended downturn in China's property market. However, the outlook indicates expectations that COLI will maintain strong contracted sales performance and stabilize its credit metrics with robust liquidity over the next 6-12 months.

- The UK is considering imposing new restrictions on outward investments in emerging technologies like artificial intelligence and semiconductors, aiming to mitigate security risks associated with aiding adversarial states like Russia and China. Deputy Prime Minister Oliver Dowden plans to collaborate with G7 nations to assess these risks and explore the possibility of additional regulations, particularly in sectors crucial for national security.

- A group of A-share listed companies in China have adjusted their 2023 annual earnings estimates, a step likely taken to prevent potential delisting penalties for falsifying financial records, reports the official Shanghai Securities News. According to exchange filings, 35 companies have revised their initial earnings projections, with 31 of them lowering their estimates, including three shifting from profits to losses, with analysts attributing these adjustments to recent stricter regulations, particularly concerning accounting fraud.

- Looking ahead, Hong Kong has Unemployment data later today, while China's 1 & 5 yr LPR on Monday is the next focus

ASIA PAC EQUITIES: Asian Equities Head Higher, Buffets Yen Bond, TSMC Earnings Shortly

Regional Asian equities are higher today, after initially opening lower. Japanese equities have been boosted by Berkshire Hathaway pricing a ¥263.3 billion ($1.71 billion) of bond, the firms largest yen deal its debut sale in the currency in 2019, raising bets it may boost holdings of Japanese equities. Asian chipmakers such as TSMC which reports earnings later. The FX market has been quiet today, although most Asian currencies are a touch lower vs the USD, while global yields are edged lower. On the data front, focus was on Australian employment Report for March, with employment falling 6,585 m/m (estimate +10.0k) in March versus a revised +117.6k in February. The Jobless rate rose to 3.8% (3.9% est) from 3.7% in February.

- Japanese stocks initially opened lower this morning the focus has remained around the yen with the currency edging higher after a joint statement from Japan, South Korea and the US fueled speculation that the latter would tolerate any Japanese attempt to support its currency. Equities got a boost earlier when it was announced Berkshire Hathaway pricing a ¥263.3 billion ($1.71 billion) of bond, leading to speculation that that money would be put to work in the equity market after recent comments from Warren Buffett around his attraction to Japanese equities, especially Banks and Financials. The Nikkei 225 is now up 0.50%, while the Topix is up 0.90%, the Topix Bank Index is up 1.80%.

- South Korea’s equities are higher today with the Kospi up 1.80% erasing losses made on Wednesday. Food stocks have been the largest contributors to the move higher today, as food exports from the nation are expected to grow and helped by foreign investors who turn buyers of local equities as the won halts its drop against the dollar. The Kospi tapped the 200-day EMA on Wednesday as the 14-day RSI hit 30 before this mornings bounce.

- Taiwan equities have opened down 0.40%, although have completely reversed those moves to now trade up 0.40%, TSMC will be releasing earning later with the market eagerly waiting, it should be noted that TSMC has been responsible for about 60% of the Taiex yearly gains.

- Australian equities are higher today, miners have contributed the most to the moves as commodity prices head higher with Iron ore jumping as much as 6% on Wednesday as optimism that more Chinese steel mills would restart as demand picks up. Employment data was released earlier showing a loss of 6.6k jobs vs estimates of a 10k gain, while the employment rate fell to 3.8% in March from 3.9% in Feb. The ASX200 is up 0.46% today.

- Elsewhere in SEA, New Zealand Equities are down 0.60% after earlier testing the 100-day EMA at 11,750, Philippines equities are up 1.30%, Indonesian equities are up 0.30%, while India has returned from its break to trade up 0.20%

ASIA EQUITY FLOWS: Foreign Investors Continue To Sell Asian Equities, Taiwan Hit Worst

- China equities flows continue to show no real sign of direction, markets have stalled with the CSI300 still unable to break above the 200-day EMA level at 3600, the index has traded sideways since mid to late Feb when we broke above the 3,400. The 5-day average now -0.05b, 20-day average at -0.11b and the longer term 100-day average now 0.43B yuan.

- Taiwan equities saw another day of outflows with $640m leaving the market, equity markets largely tracking Chinese markets higher with the Taiex finishing up 0.56%. There has been little in the way of eco data this week, with Industrial Production due out Tuesday and GDP on the 30th the major focus for the month, while moves in the Philadelphia SI Semiconductor Index will also drive flows and price. The 5-day average is now -$693m, vs the 20-day at -$325m well below the longer-term trend of $123m.

- South Korea equities have now marked four straight days of net selling by foreign investors with an outflow of $141m. The Kospi is now off 7.02% from recent highs, breaking below the 20, 50 & 100-day EMA and now testing the 200-day EMA. Sellers are in control with the 14-day RSI now testing 30, at 31.7. The 5-day average is now just $16m down from $187m a week ago, the 20-day average to $289m and the 100-day average to $176m.

- Philippines equities continue to see outflows with $9m leaving the market on Wednesday, making it 9 straight days of outflows for a total of $96m, equity prices did trade higher on Wednesday ending an almost 10% drop, the PSEi is now down 8.78% from recent highs made on Apr 1st. The 5-day average is -$10m, the 20-day average is -$9.25m, while the $1.41m.

- Indonesia had a $28m outflow on Wednesday making it an 11-day streak of net selling by foreign investors for a total of $889m, the JCI is now down 4.34% from recent cycle highs, although we did bounce right off the 200-day EMA on Tuesday. The 5-day average is now -$111m, the 20-day average is -$9m, while the longer term 100-day average is still positive at $14.9m.

- Malaysian equities have now marked 6 straight days of selling by foreign investors, for a total of $319m. Equity markets are holding up better than most in the region off just 1.61% from recent highs and have bounced right off the 50-day EMA. The 5-day average is -$27, 20-day average is -$58m while the 100-day average is -$4m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | -0.2 | -0.3 | 57.9 |

| South Korea (USDmn) | -142 | 84 | 13668 |

| Taiwan (USDmn) | -640 | -3466 | 1205 |

| India (USDmn)** | 0 | 72 | 1339 |

| Indonesia (USDmn) | -29 | -558 | 921 |

| Thailand (USDmn) | -174 | 78 | -1840 |

| Malaysia (USDmn) ** | -103 | -292 | -549 |

| Philippines (USDmn) | -9 | -49.3 | 88 |

| Total (Ex China USDmn) | -1096 | -4132 | 14832 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To Apr 16th |

JAPAN DATA: Offshore Investors Continue To Buy Local Stocks, Japan Investors Sell Overseas Bonds

Offshore buying of Japan stocks was strong for the second straight week. Net inflows of ¥1740bn was just under what we saw in the prior week. This ended the run of outflows since mid-March. Over the past month net inflows have been positive at ¥711.8bn. Offshore investors also bought local bonds, but only a modest ¥50.7bn. Net flows over the past month are still negative into this space.

- Local Japan investors were large net sellers of offshore bonds (-¥1005.9bn). This came in the week where the US CPI upside surprise drove a surge in yields. Net selling of this segment has been over ¥2300bn in the past month.

- Local investors bought ¥53.9bn of overseas stocks. This only partially reverses net selling from the prior week. The trend remains for net outflows for this segment.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending Apr 12 | Prior Week |

| Foreign Buying Japan Stocks | 1740.0 | 1764.9 |

| Foreign Buying Japan Bonds | 50.7 | -348.9 |

| Japan Buying Foreign Bonds | -1005.9 | 347.9 |

| Japan Buying Foreign Stocks | 53.9 | -293.2 |

Source: MNI - Market News/Bloomberg

OIL: Crude Stabilises As Sanctions On Card For Iran & Venezuela

Oil has stabilised after falling around 3% on Wednesday on a better risk tone and weaker greenback (USD index -0.1%). Brent is up 0.3% to $87.57/bbl off the intraday low of $87.21 early in the APAC session. WTI is 0.2% higher at $82.88 after falling to $82.55.

- On the one hand US inventories rose strongly last week, but on the other the US will reinstate sanctions on Venezuelan oil unless there it changes its attitude to registering opposition candidates for the upcoming election by the end of today when the reprieve expires. New sanctions on Iranian oil are also to be tabled as part of the US foreign aid package currently struggling to pass through the House.

- There is significant uncertainty over the details of Israel’s response to Iran’s attack on the weekend. For now the situation has gone quiet but markets are wary. All of the above mean that significant risks to the energy outlook remain.

- Later the Fed’s Bowman, Williams, Bostic and Collins, ECB’s de Guindos and Schnabel, and BoE’s Greene appear. IMF meetings continue and the Eurogroup meets. US jobless claims and April Philly Fed print.

IRON ORE: Back To Late Feb Levels On China Stimulus Hopes

The active Iron ore contract in Singapore is back to late Feb levels, last near $116.25/ton (earlier highs were at $117.50). We are now around 20% above early April lows in the contract.

- The better equity tone is likely helping at the margin, although the recovery in iron ore has outperformed the rebound in property related equity indicators, which are only marginally above recent lows.

- Yesterday the NDRC stated China’s domestic demand remains insufficient with weak social expectations. It was also acknowledged that the economic foundation was not yet solid and still faced challenges (see this link). This is expected to see a speed up of ultra-long government bond issuance (see this link for more details).

- This, along with an expected restocking of iron ore inventories by China mills, have been noted as sources of support.

GOLD: Higher Today After Yesterday’s Drop

Gold is 0.6% higher in the Asia-Pacific session, after closing 0.9% lower at $2361.02 on Wednesday. This leaves the yellow metal 2.4% off its recent record high.

- Despite the prevailing risk-off sentiment in the markets yesterday, characterised by lower US Treasury yields, wider credit spreads, weaker US equities, and softer oil prices, bullion made a notable downward move.

- Technical buying, bargain hunting and an especially well-received 20-year auction also helped US Treasuries move away from YTD yield highs.

- Gold's decline yesterday likely stemmed from Federal Reserve Chair Jerome Powell's recent remarks, which indicated a potential postponement of the eagerly awaited policy shift following a string of unexpectedly high inflation readings.

- Newsflow was minimal yesterday. Today’s US calendar will see Weekly Claims, Existing Home Sales and Fed Speak.

- According to MNI’s technicals team, sights remain on $2452.5 next, a Fibonacci projection. Initial firm support is at $2286.3, the 20-day EMA.

ASIA FX: USD/Asia Pairs Lower, CNH Again Steady, PBoC Vows TO Avoid FX Overshoot

USD/Asia pairs are lower across the board, although USD/CNH has proven to be sticky. We are away from best levels for most pairs. The PBoC vowed to avoid FX overshooting in the yuan. The won has been the standout performer, up 1% at one stage before paring gains. US Treasury Secretary Yellen shared concerns from both the South Korean and Japan FinMin's on recent FX weakness. This likely aided won sentiment. Tomorrow, we have Malaysia March trade figures and Q1 GDP out. The Philippines BoP position is also due.

- USD/CNH is range bound, continuing to exhibit a low beta to overall USD moves, the pair last near 7.2475. Spot USD/CNY is down slightly though. The USD/CNY fixing was steady, which may have the market a little disappointed, given recent USD weakness. The PBoC vowed to prevent the yuan from overshooting and managing broader expectations.

- Spot USD/KRW is back to 1375, as the won rebound continues. Long USD positions are potentially being trimmed post the recent step up in verbal FX rhetoric. Local equities are also up strongly, defying the negative lead from US markets. The 1 month NDF is back close to 1373. We are away from best levels, but the won remains an outperformer over recent sessions.

- PHP is around 0.20% firmer, with USD/PHP last near 57.05/10, close to the previous resistance point near 57.00, but we haven't been able to break through. The above factors are helping, while the sharp pull back in oil prices from Wednesday is another positive.

- USD/IDR is also down by around 0.20%, the pair last near 16185. China's foreign minister is in Indonesia today, with both sides talking up economic ties. Indonesia's foreign minister stating the country expects greater access to China markets. Barclays expects BI to hike next week in response to the recent round of FX weakness.

- THB is lagging somewhat, USD/THB close to unchanged so far in Thursday trade, the pair last near 36.75/80. MYR is around 0.30% stronger, the pair back under 4.7800 backing away from the 4.8000 level.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/04/2024 | 2315/1915 |  | US | Fed Governor Michelle Bowman | |

| 18/04/2024 | 0130/1130 | *** |  | AU | Labor Force Survey |

| 18/04/2024 | 0715/0915 |  | EU | ECB's De Guindos ECB Report Presentation | |

| 18/04/2024 | 0800/1000 | ** | | EU | Current Account |

| 18/04/2024 | 0900/1100 | ** | | EU | Construction Production |

| 18/04/2024 | 1230/0830 | *** | | US | Jobless Claims |

| 18/04/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 18/04/2024 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 18/04/2024 | 1305/0905 | | US | Fed Governor Michelle Bowman | |

| 18/04/2024 | 1315/0915 | | US | New York Fed's John Williams | |

| 18/04/2024 | 1315/0915 | | US | Fed's Miki Bowman | |

| 18/04/2024 | 1400/1000 | *** | | US | NAR existing home sales |

| 18/04/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 18/04/2024 | 1500/1100 | | US | Atlanta Fed's Raphael Bostic | |

| 18/04/2024 | 1500/1600 |  | UK | BOE's Greene with Atlantic Council GeoEconomics Center | |

| 18/04/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 18/04/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 18/04/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 18/04/2024 | 1730/1930 | | EU | ECB's Schnabel Speaks At 2024 EU-US Symposium | |

| 18/04/2024 | 2145/1745 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.