Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

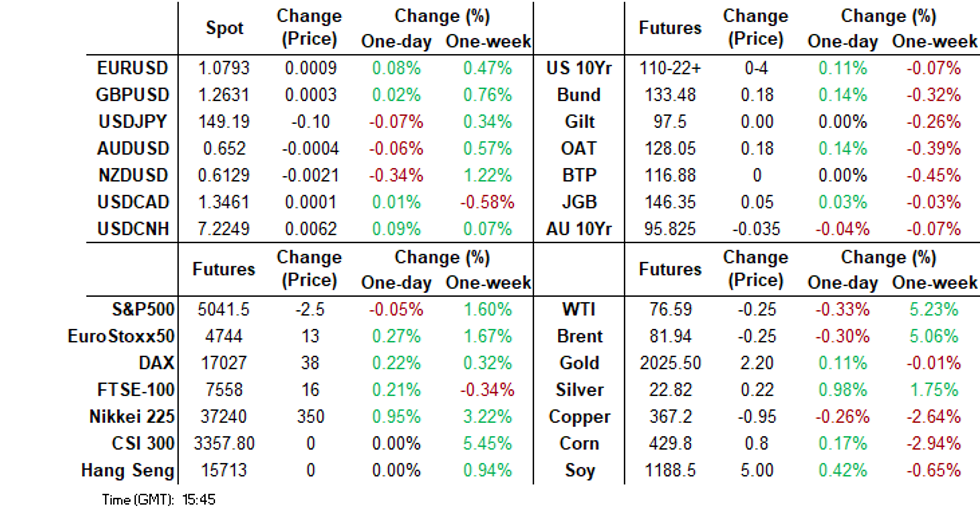

- It has been a relatively muted start to trading for the week in Asia Pac markets. Much of the region is out for LNY holidays, while Japan has also been out today.

- NZD/USD has given back some of Friday's outperformance but remains within recent ranges. Some comments by RBNZ Governor Orr may have weighed at the margin, although NZGBs closed 2-4bps cheaper across benchmarks (albeit off the local session’s worst levels). US Tsy futures have drifted higher on light volumes, but there has been no cash trading with Japan markets out.

- Elsewhere, our recession probability estimate signals that there is still a risk of recession in the euro area in H1 2024 with growth positive again in the second half, see below for more details.

- Looking ahead, the Fed’s Bowman, Barkin and Kashkari make appearances, BoE’s Bailey and the ECB’s Lane, Cipollone and Buch speak. In terms of data there are January NY Fed 1-yr inflation expectations and US budget statement. US CPI on Tuesday will be watched closely.

MARKETS

US TSYS: Tsys Slightly Stronger On Low Volume, Holding Above Support Levels

TYH4 is currently trading at 110-23, + 04+ from New York closing levels.

As expected a slow start to the week for markets, treasuries largely unchanged in Asia trading.

- The past month has seen downside pressure on US Tsys, testing the 110-22+ area multiple times, the first support zone and the bear trigger, closing the past week below support at 110-18+ solidifying the break, next support zone remains at 110-16 Dec 13th low, and a level we touched during the Friday session, however only very briefly a break here would open up a move to the Dec 11th lows, of 109-31+.

- To the upside, initial key resistance has been defined at 113-06+, Feb 1 high, where a breach would reinstate a bullish theme. First resistance is 111-11, the 20-day EMA.

- Cash yields have range bound over the past few months, the 10yr has been trading within the 3.80%/4.20% area, closely Friday at 4.175% a break above the 4.20% level would open up a move to the Dec 12 highs of 4.28%.

- Key event risk this week is with the US CPI on Wednesday Est of 0.2% vs 0.3% previously, while retail sales and Claims are expected on Friday.

- Look ahead: Monday data calendar includes NY Fed Inflation Expectations, and more Fed commentary from Fed Gov Bowman, Richmond Fed Barkin MN Fed Kashkar and MN Fed Kashkari.

Fig 1: US 10yr Futures

Source: MNI - Market News/Bloomberg

ECB: March ECB Forecasts Key To Timing Of First Rate Cut

In January euro area headline inflation eased to 2.7% from 2.9% in line with the ECB’s December forecast for Q2 2024. Core is stickier easing to 3.2% from 3.4% and above the ECB’s 3.2% Q1 2024 projection. The forecasts will be updated for the March meeting on March 7, and with recent CPI data moderating faster than expected there is a chance that achieving the inflation target could be brought forward. The market expects a rate cut by June.

- On the weekend Spain’s Governing Council member de Cos said that the March “projections will be key” in helping the ECB decide if it is confident that it will meet its 2% target and can thus start easing. Confidence that inflation targets will be met is something central banks globally are trying to establish.

- De Cos believes that disinflation is “advanced” and will continue over “coming quarters”.

- The dovish Bank of Italy Governor Panetta also thinks the move towards the ECB’s target is “advanced” and that the moderation towards 2% is “rapid” and that core hasn’t proven sticky. Current ECB forecasts don’t have headline inflation back around target until H2 2025 and core at the end 2025 but this may be brought forward given the moderate start to 2024 since Panetta sees downside risks to inflation. As a result he said that the “time for reversal of the monetary policy stance is fast approaching”.

- Bank of Portugal Governor Centeno is also positive about the inflation outlook but warned that easing should be gradual and that if it is rapid it signals that “something isn’t going well”. He also said that rates won’t return to the very low levels seen before this cycle as they are “perverse for economic growth and financial stability” and “ideally” rates will stabilise around neutral of “close to 2%”.

EUROZONE: Risk Of Recession In H1 2024 But Stagnation Likely

Q4 euro area GDP was flat after declining 0.1% in the previous quarter. Despite energy prices remaining low through the winter, the chance of recession remains real and is being monitored closely. With inflation falling further below 3% in January, there are growing calls for the ECB to cut rates. Our recession probability estimate signals that there is still a risk of recession in the euro area in H1 2024 with growth positive again in the second half.

- Our probit model starting in 1998 estimated the risk of recession 6-months ahead at above the key 50% level for the five months from July 2023 with the peak in September at 68% but it fell below 50% in December and further in January to 28%. Since it didn’t rise close to 100%, which usually happens when a recession occurs, then persistent stagnating growth is likely rather than a contraction.

- The downward move in recession probability over the last two months has been driven by the 6-month change in the economic sentiment indicator turning positive, rising real equity prices, lower real oil prices in euros and low unemployment.

- Our calculation starting in 1985 has signalled little chance of a euro area recession 6-months ahead since Q3 2022.

- It is worth noting that econometric calculations are only estimates and not predictions. Also, euro area recessions are dated by a committee rather than defined as two consecutive quarters of negative growth.

Source: MNI - Market News/Refinitiv

AUSSIE BONDS: Cheaper, Narrow Ranges, Subdued Session With No Cash Tsys

ACGBs (YM -6.0 & XM -2.5) are holding cheaper after dealing in relatively narrow ranges in today’s Sydney session. With the domestic calendar light, local participants have likely been on headlines and US tsys watch.

- However, today’s news flow has been light, with US tsy futures dealing slightly stronger. Cash Us tsys have not been trading in today’s Asia session due to a Japanese holiday.

- Key event risk this week is US CPI on Wednesday, and US Retail Sales and Claims data on Thursday.

- Cash ACGBs are 2-5bps cheaper, with the AU-US 10-year yield differential 1bp tighter at -3bps. The 3/10 curve is flatter.

- Swap rates are 3-4bps higher.

- The bills strip has bear-steepened, with pricing -2 to -6.

- RBA-dated OIS pricing is 3-6bps firmer across meetings beyond August. A cumulative 39bps of easing is priced by year-end compared to 67bps at the start of February.

- Tomorrow, the local calendar sees Westpac Consumer and NAB Business Confidence, along with remarks by Marion Kohler, RBA’s Head of Economic Analysis, at the Australian Business Economists Annual Forecasting Conference in Sydney.

AUSSIE BONDS: AU-NZ 10Y Yield Differential Breaks Out Of Its 3M Range

Today, the NZ-US 10-year yield differential remains relatively stable, standing at +66bps, which is approximately 10bps wider than Friday's opening level. However, this places it close to the midpoint of the range observed over the last 12 months, which has fluctuated between +40 and +85bps.

- In contrast, the AU-NZ 10-year yield differential has reached its widest level since October, currently sitting at -68bps.

- Before Friday, this particular differential had fluctuated within a range of -30 to -60bps over the past three months.

- It's noteworthy that the 12-month high for this differential is approximately -100bps.

Figure 1: AU-NZ 10-Year Yield Differential

Source: MNI – Market News / Bloomberg

NZGBS: Cheaper But Off The Session’s Worst Levels, Subdued Session

NZGBs closed 2-4bps cheaper across benchmarks but off the local session’s worst levels. Nevertheless, with the domestic calendar light, local participants have extended Friday’s sell-off, prompted by ANZ Bank's hawkish OCR forecast change. ANZ Bank now anticipates that the RBNZ will raise the official cash rate (OCR) by a cumulative 50bps (this month and in April) to 6.0%.

- The 2-year yield currently sits 30-35bps higher than last week's start. The 10-year yield is 20bps higher, with its yield differential with ACGBs 15bps wider.

- Swap rates are 3-5bps higher.

- RBNZ dated OIS pricing is 3-6bps softer across meetings out to August. That said, the cumulative easing priced by year-end has been pared to 51bps from a peak of 5.68% versus around 100bps of easing off 5.53% at the end of January.

- RBNZ Chief Economist Paul Conway will speak to the ANZ Investor Tour in Wellington tomorrow. There will be no new economic information or insights presented in this engagement.

- The NZ Government will deliver the Budget on May 30.

- Tomorrow, the local calendar sees Inflation Expectations, ahead of REINZ House Sales, Card Spending and Food Prices on Wednesday. The RBNZ Policy Decision is on 28 February.

NZ STIR: RBNZ Dated OIS Continue To Pare Friday’s Post-ANZ Forecasts Firming

RBNZ dated OIS pricing has further pared Friday’s significant firming, prompted by ANZ Bank's 'OCR to 6.0%' forecast.

- Speaking to a parliamentary committee today, RBNZ Governor Orr stated that “Inflation at 4.7% annualised is still too high, we’re aiming for 2%. That’s why we’ve retained a restrictive monetary policy stance with the Official Cash Rate at 5.5%, and we’ll be back at the end of this month again with our updated views on the wisdom of that stance and the length which we have to be there.”

Figure 1: RBNZ Dated OIS Pricing (%)

Source: MNI – Market News / Bloomberg

FOREX: NZD Gives Back Some Of Friday's Outperformance, Steady Trends Elsewhere

Outside of some NZD weakness, G10 markets have started this week in a muted fashion. The BBDXY sits little changed, last near 1241.6. Most EM Asia markets are closed, including China, Hong Kong and Singapore for LNY, while Japan markets are also out.

- Cross asset moves have been quiet as well, US equity futures sit close to flat, while US Tsy futures have drifted a touch higher.

- NZD/USD is close to session lows in recent dealings, last near 0.6130, around 0.3% lower than NY closing levels from Friday. this puts us back sub the 20 and 50-day EMAs, albeit just.

- Comments from RBNZ Governor Orr may have weighed at the margin. He stated that higher inflation is why policy rates are staying restrictive. Orr is appearing before parliament today. He also noted that "we’ll be back at the end of this month again with our updated views on the wisdom of that stance and the length which we have to be there" (per BBG).

- At face value this doesn't suggest a further tightening in rates is being considered, although tomorrow we get inflation expectations and Orr speaks early on Friday morning local time. It seems that if the data warrants it, that policy will stay "restrictive" for longer rather than hiking again at this juncture. In November, the RBNZ projections didn't imply an easing until H1 2025.

- Elsewhere, AUD/USD has been dragged down by NZD, a touch, last near 0.6520, but the AUD/NZD cross has firmed. We were last near 1.0635, but off session highs of 1.0640. Lows from last week came in at 1.0586.

- USD/JPY sits in the 149.20/25 in recent dealings little changed for the session.

- Looking ahead, the Fed’s Bowman, Barkin and Kashkari make appearances, BoE’s Bailey and the ECB’s Lane, Cipollone and Buch speak. In terms of data there are January NY Fed 1-yr inflation expectations and US budget statement. US CPI on Tuesday will be watched closely.

ASIA PAC EQUITIES: Equities Lower As Asia Enjoys LNY

It's a slow day for equities, especially with most of Asia observing Lunar New Year. US Equity Futures remain largely unchanged as the market anticipates the US CPI release on Wednesday.

- In Australia, equities are trending lower today, currently down by 0.20%. Health stocks, particularly CSL due to disappointing Phase 3 AEGIS-II trial results, causing their equity of 5.10%. Miners are also contributing to the downturn, with the ASX Metals and Mining Index 0.66% lower at 5880. A crucial level to watch is 5800, and a break below could signal further weakness, possibly moving towards the year lows of 5600. WBC Consumer Confidence and NAB Business Confidence/Conditions are on the agenda for tomorrow, with Employment data due on Thursday.

- New Zealand equities have dipped after remarks from the RBNZ Governor and Deputy Governor, emphasizing persistently high inflation and the system's capacity to handle elevated interest rates. The NZX50 is down 0.72%. Looking ahead, 2yr Inflation expectations are due tomorrow, followed by House Sales and Food prices on Wednesday.

- Indonesia equities are trending higher today, up by 0.40%, driven by financials, especially Bank Mandiri, higher by 2.20% continuing it's strong performance following a positive earnings outlook announcement last week. Note that Indonesia's Presidential elections are held on Wednesday, which will be a public holiday.

- Philippines equities show a slight decline today off 0.20%, lacking significant earnings or market headlines. Investors might be looking to secure profits after the PSEi hit 1-year highs on Thursday. The PSEi has witnessed 130m of inflows this year, with 42m of that coming in the past week.

OIL: Crude Consolidates In Thin Holiday Trading Ahead Of Monthly Reports

Oil prices have given up some of their gains from late last week with trading thin due to much of Asia closed for holidays. WTI is down 0.6% to $76.41/bbl off the intraday low of $76.18 and Brent is down 0.5% to $81.78/bbl and has been moving in a narrow range. The USD index is slightly lower.

- Oil has sold off today on news that Iran has been talking with Hamas in Beirut to find a “diplomatic solution”. Iran commented that progress is being made on the situation in Gaza including the release of Israeli hostages, according to Bloomberg. Later today US President Biden and King Abdullah of Jordan will speak.

- Geopolitical developments continue to support crude but concerns over excess supply persist given scepticism that OPEC members will stick to quotas and Plains All American Pipeline saying that output from the US Permian Basin of West Texas and New Mexico is expected to rise almost 5% before year-end. Revised forecasts will be included in the OPEC and IEA monthly reports due this week.

- Later the Fed’s Bowman, Barkin and Kashkari make appearances, BoE’s Bailey and the ECB’s Lane, Cipollone and Buch speak. In terms of data there are January NY Fed 1-yr inflation expectations and US budget statement. US CPI on Tuesday will be watched closely.

GOLD: Steady After Friday’s Drop

Gold is little changed in the Asia-Pac session, after closing 0.5% lower at $2024.26 on Friday.

- Friday’s move locked in a weekly decline for bullion, as traders weighed the outlook for interest rates ahead of crucial US CPI data on Wednesday and Retail Sales on Thursday.

- With limited economic data on Friday, the market focused on revisions to US CPI data after Fed Waller highlighted the importance of the adjustments to confirm the downward trend for inflation in a recent speech. Overall, CPI revisions provided only minor and offsetting adjustments that did little to change the outlook that the Fed will be pivoting to rate cuts in the coming months.

- US Treasuries finished Friday moderately weaker, with yields 2-3bps higher. US Treasury futures are dealing slightly stronger in today's Asia-Pac session, with cash bonds not trading due to a Japanese holiday.

INDONESIAN POLITICS: Prabowo Increases Lead Ahead Of Wednesday’s Vote

Indonesian elections are held on Wednesday, which will also be a public holiday. The latest polls all show defence minister Prabowo not only ahead of the other two presidential candidates but likely to receive over 50% of the vote making a runoff in June unlikely. But with 53.5% the highest level of support, there is still a chance he won’t reach 50% given standard error bands around surveys. In this case the risk is that the other two candidates join forces and outpoll Prabowo in the June runoff.

- The LSI Denny JA poll taken between January 26 and February 6 covered responses following the fifth presidential debate. It showed support for Prabowo increasing 2.8pp from the January 16-26 survey to 53.5% with Anies still in second but falling 0.3pp to 21.7% and the incumbent PDI-P’s Ganjar down 0.5pp to 19.2%. So the ‘undecideds’ seem to be moving towards Prabowo.

- The polls taken since January 21’s fourth debate have Prabowo on an average 52.1%, Anies 22.7% and Ganjar 18.9%.

- There is concern that a Prabowo presidency would be a risk to Indonesia’s democracy given his past and the continuation of current President Joko Widodo’s dynasty with his son as VP, who received a constitutional dispensation from the age requirement. Jokowi remains very popular and this was seen as his endorsement of Prabowo who is not representing Jokowi’s PDI-P. This has caused tensions in his cabinet. According to The Economist, Anies and Ganjar have said their campaign events have been disrupted.

- As defence minister Prabowo proposed a Ukrainian peace plan in 2023 which was pro-Russian but also against Indonesia’s official policy on the conflict and he hadn’t consulted the government beforehand. This is driving fear that his presidency may be unpredictable, especially given many of his proposals are unrealistic or very expensive.

ASIA FX: Muted Start For Asian FX, With Many Markets Closed For LNY

It has been a very muted start to the week for Asian FX, with only a small number of markets open. China, Hong Kong, South Korea and Singapore have been closed today. Singapore and South Korea return tomorrow, but China remains closed for the week, Hong Kong returns on Wednesday. Note still to come later on is India CPI and IP data. Most focus will rest on the CPI print given last week's hawkish hold.

- USD/PHP has gravitated higher after Friday's break. The pair was last 56.14, around 0.40% weaker versus end Thursday levels. Recent lows in the 1 month NDF (55.80) coincided with the 50-day MA, which now is back to 55.83. All key EMAs are near by to current NDF and spot levels. The main macro focus this week will be Thursday's BSP decision. None of the economists surveyed by BBG look for a shift in the policy rate, which currently sits at 6.50%. The tone from the BSP will be watched, although recent rhetoric has pushed back against the idea of a near term dovish shift.

- USD/IDR is a little lower versus end Wednesday levels from last week, as markets return from the Thur/Fri break. The pair was last near 15620 after closing last Wednesday at 15635. The 1 month NDF is little changed from end Friday levels in NY, last near 15635. We are now back to mid Jan levels for the pair. The clear focus this week will be on Indonesia's election, with a clear victory for current favorite Prabowo likely to be the most market outcome, in terms reducing uncertainty that might come with an election run off.

- USD/INR spot sits little changed, last near 83.00, comfortably within recent ranges.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/02/2024 | 0945/1045 |  | EU | ECB's Lane keynote speech at conference | |

| 12/02/2024 | 1315/1415 | | EU | ECB's Lane participates in 'post-pandemic' roundtable | |

| 12/02/2024 | 1420/0920 |  | US | Fed Governor Michelle Bowman | |

| 12/02/2024 | 1550/1650 | | EU | ECB's Cipollone participates in panel on Euro@25 | |

| 12/02/2024 | 1600/1100 | ** | | US | NY Fed Survey of Consumer Expectations |

| 12/02/2024 | 1800/1300 | | US | Minneapolis Fed's Neel Kashkari | |

| 12/02/2024 | 1800/1800 |  | UK | BOE's Bailey lecture at Loughborough University | |

| 12/02/2024 | 1900/1400 | ** | | US | Treasury Budget |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.