Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

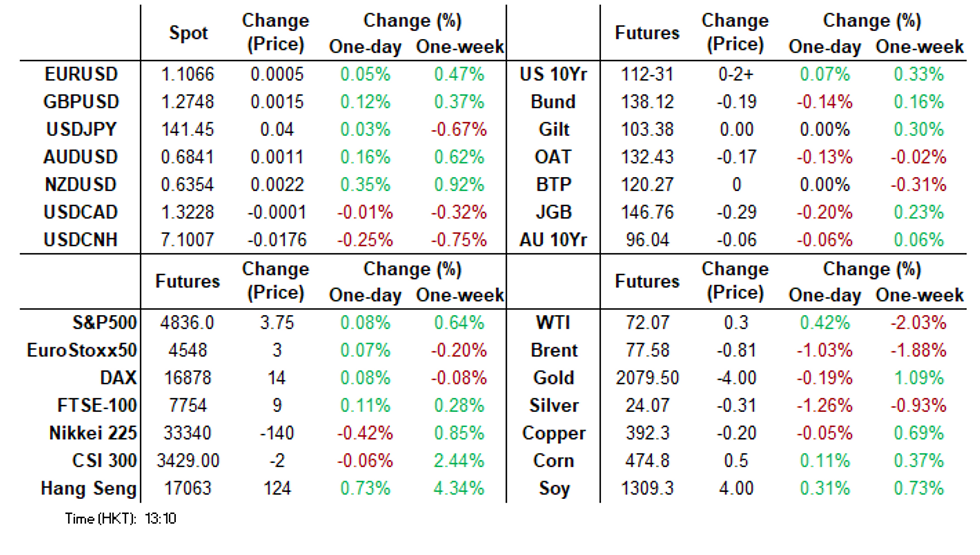

- There has been a muted session in Asia to finish 2023, across assets there were little moves of note and activity was limited.

MARKETS

US TSYS: Muted Session To Wrap 2023 In Asia

TYH4 deals at 112-31, +0-02+, a 0-04+ range has been observed on volume of ~30k.

- Cash tsys sit ~1bp richer across the major benchmarks.

- Tsys have observed very narrow ranges with little follow through on moves in a muted last Asian session of 2023.

- The docket in Europe is thin today, further out we have MNI Chicago PMI.

JGBs: Bear-Steepening To End The Year, Market Closed Mon, Tue & Wed Next Week

JGB futures are holding cheaper, -29 compared to settlement levels, after trading in a narrow range throughout the Tokyo session.

- In the absence of domestic data catalysts, the local market has experienced a drift towards cheaper valuations, particularly driven by the long end. Nevertheless, the 20-40-year zone is currently positioned above the session's cheapest points. A slight improvement in US tsys during today's Asia-Pac session may have contributed to the rebound from the session's nadir levels.

- Nevertheless, the cash JGB curve continues to hold a bear-steepening, with yields flat to 6bps higher. The benchmark 10-year yield is 2.3bps higher at 0.618% versus the recent rally low of 0.555% set on 20 Dec.

- (Bloomberg) JGB futures have consistently produced a sell signal soon after rising above the 200-day moving average, and it looks set to run into next year as speculation rises over an exit from negative rates. (See link)

- The swaps curve has also bear-steepened, with swap spreads wider to the 4-year and tighter beyond.

- A reminder that Japanese markets are closed Monday, Tuesday, and Wednesday next week.

ACGBs: Holding Cheaper Into Year-End, Light Calendar Again Next Week

ACGBs (YM -4.0 & XM -6.5) are holding cheaper on the final trading session of 2023 after dealing in relatively narrow ranges. With the local calendar empty, local participants have likely been eyeing US tsys in today’s Asia-Pac session as the year of trading comes to an end.

- US tsys are currently dealing flat to 1 bp richer across benchmarks versus NY closing levels.

- Cash ACGBs are 4-6 bps cheaper, with the 3/10 curve steeper and the AU-US 10-year yield differential 2 bps wider at +12 bps.

- Swap rates are 3-5 bps higher, with EFPs little changed.

- The bill strip is cheaper, with pricing from -1 to -4. Mid-reds are the weakest.

- RBA-dated OIS pricing is dealing mixed, but the moves remain small across meetings.

- (AFR) Global fund managers have slashed their cash holdings to a two-year low and are betting that technology stocks and bonds will be the biggest winners when the Federal Reserve pivots to rate cuts. (See link)

- Next week, the local calendar is relatively light with CoreLogic House Prices and Judo Bank PMI Mfg on Tuesday and Judo Bank PMI Composite & Services on Thursday.

NZGBS: Drifted Cheaper Into Year-End

NZGBs concluded the session 1-3 bps cheaper across benchmarks, after dealing in relatively narrow trading ranges throughout the local session. In the absence of local calendar events, today's market dynamics have primarily reflected a drift towards year-end.

- US tsys currently dealing 1-2 bps richer than NY's close in today’s Asia-Pac session. The CME Group trading floor closes at 1300ET Friday for the New Year's Holiday, while Globex closes at its normal time of 1600ET (re-open at 1600ET next Monday instead of the normal Sunday opening).

- The NZ-US 10-year yield differential, currently at +48 bps, is approaching its lowest level since mid-November when it was +45 bps. To provide context, this differential was hovering around +75 bps in early December.

- Notably, the recent outperformance of the NZ 10-year yield has been particularly pronounced compared to its ACGB counterpart. The NZ-AU 10-year yield differential is presently at +36 bps, a significant shift from its +99 bps position in early October.

- Swap rates closed 1-2bps higher.

- RBNZ dated OIS pricing closed little changed across meetings.

- Next week, the local calendar is empty apart from CoreLogic House Prices on Thursday.

- The focus for the remainder of Friday will be the December reading of the Chicago Purchasing Managers Index, the final data point for 2023.

GOLD: Weaker On Thursday But Still Looking At A Weekly Gain

Gold is slightly stronger in the Asia-Pac session, after closing 0.6% lower at $2065.61 on Thursday.

- Bullion’s slide yesterday was driven by a rise in bond yields, some unwinding of haven flows and a firmer dollar. US Treasuries finished 3-5 bps cheaper across the major benchmarks following a poor 7-year US Treasury auction.

- Despite Thursday’s decline, gold is headed for a weekly gain as investors continue to bet aggressively that the Federal Reserve will start to unwind its restrictive stance on monetary policy in 2024.

- According to MNI’s technicals team, the Dec 13 reversal in bullion and the subsequent move higher points to the end of the Dec 4 - 13 corrective pullback. This week’s move highlights a bullish theme. Moving average studies are also in a bull-mode position, reflecting an uptrend. A continuation higher has opened $2097.1, 76.4% of the Dec 4 - 13 bear leg. Initial support is at $2031.3, the 20-day EMA.

FOREX: Steady Session In Asia

There has been steady session across G-10 FX on Friday in Asia, ranges are narrow and moves have had little follow through. The docket is light in Asia and little meaningful macros newsflow has crossed.

- Yen is flat, unchanged from opening levels. USD/JPY traded lower Thursday and the pair remains below ¥144.96, the Dec 9 high. The recent recovery from ¥140.97, the Dec 14 low, has been a correction and the trend condition remains bearish. Support at ¥140.97, the Dec 14 low, has been cleared, confirming a resumption of the downtrend that started Nov 13. This opens ¥140.23, a Fibonacci projection point.

- AUD/USD is a touch firmer however narrow ranges are persisting thus far. Bullish trend conditions in AUDUSD remain intact and this week's continuation higher reinforces current conditions. The climb maintains the bullish price sequence of higher highs and higher lows. Sights are on $0.6900, the Jun 16 high and the next key key resistance. On the downside, key short-term support is unchanged at $0.6526, the Dec 7 low. Initial firm support is at $0.6702, the 20-day EMA. Short-term weakness is considered corrective.

- Kiwi is up ~ 0.2% however NZD/USD remains well within recent ranges. Technically the uptrend remains intact; bulls target $0.6412, the high from 14 Jul. A break through here opens $0.6563, a Fibonacci projection. Bears focus on the 20-Day EMA ($0.6227).

- CHF is ~0.2% firmer however liquidity is generally poor in Asia.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.