Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Oil prices are higher today driven by increased uncertainty in the Middle East after the Jordan leg of US President Biden’s trip was cancelled due to a large blast at a Gaza hospital. Stronger domestic data in China also supported prices but we are now off earlier highs.

- Regional equity sentiment has mostly been weaker, with continued focus on China property concerns a headwind. This has taken some of the shine off China related assets, but AUD and NZD are still higher in the G10 FX space.

- Elsewhere, US cash tsys sit 2bps richer to 1bp cheaper, the curve has twist steepened pivoting on 10s. In Tokyo afternoon dealings, JGB futures remain weaker, -38 compared to settlement levels.

- Later there are numerous Fed speakers including Waller, Williams, Bowman, Barkin, Harker and Cook plus the release of the Beige Book. In terms of data, there are US housing starts/permits and UK CPI. ECB’s Lagarde is also scheduled to speak.

MARKETS

US TSYS: Narrow Ranges In Asia

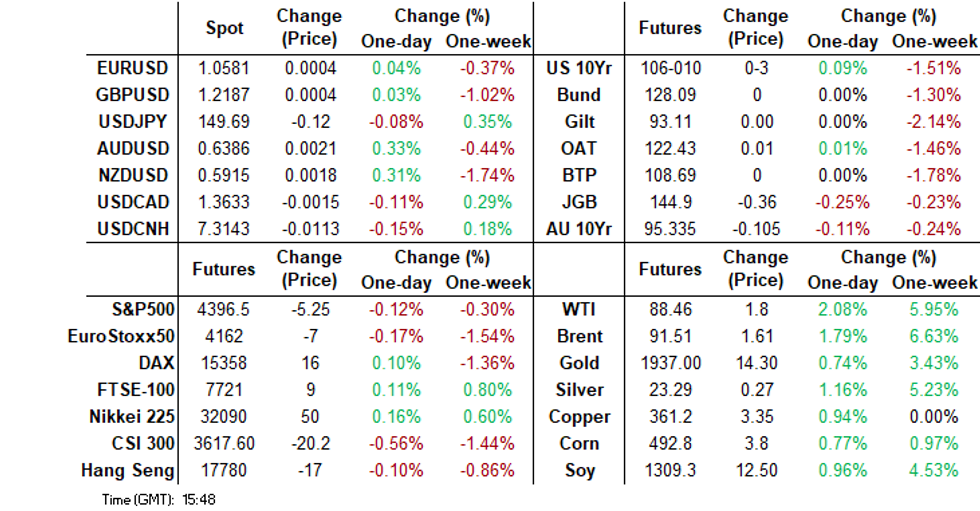

TYZ3 deals at 106-10, +0-03, a 0-04+ range has been observed on volume of ~99k.

- Cash tsys sit 2bps richer to 1bp cheaper, the curve has twist steepened pivoting on 10s.

- Tsys have observed narrow ranges in Asia with little follow through on moves, light risk off flows as President Biden's meeting with Arab leaders was cancelled saw tsys tick away from session lows.

- There was little follow through and tsys remained in narrow ranges for the majority of the session. The space looked through a strong Chinese Q3 GDP print.

- In Europe today the September CPI print from the UK crosses. Further out we have House Starts, Fed Beige Books and a number of Fed speakers including Philadelphia Fed President Patrick Harker and New York Fed President John Williams.

JGBS: Futures Cheaper, BOJ Inflation Projection Fears & US Tsys Weigh

In Tokyo afternoon dealings, JGB futures remain weaker, -38 compared to settlement levels.

- With the local data calendar light today (Tokyo Condominiums for Sale data the only release), JGBs weakness over the past 24 hours has reflected the combination of BOJ-induced selling and fresh cycle highs for US tsys.

- JGB futures pushed lower in the overnight session as BBG sources reported that “the BOJ is likely to discuss raising its inflation projection for fiscal year 2023 and 2024 at its policy meeting later this month, extending the period in which it sees prices hitting or exceeding its 2% goal.”

- JGB futures weakness then extended overnight, with US tsys finishing the NY session 8-15bps cheaper after another batch of firm data. However, US tsys are flat to 2bps richer in today’s Asia-Pac session.

- The cash JGB curve has bear-steepened, with yields 0.4bps to 5.1bps higher. The benchmark 10-year yield is 2.6bps higher at 0.807% versus the cycle high of 0.82% set today.

- Mid-session unscheduled bond purchases by the BOJ of Y300bn of 5-to-10-year and Y100bn of 10-to-25-year notes at market yields appeared to, at least momentarily, arrest the push higher in yields.

- Swap rate movements are mixed and bounded by 0.9bp lower and 1.3bps higher. Swap spreads are tighter beyond the 2-year.

- Tomorrow the local calendar sees Trade Balance and International Investment data.

AUSSIE BONDS: Sharply Cheaper, Global Bonds Weigh, Employment Report Tomorrow

ACGBs (YM -11.0 & XM -11.0) are sharply lower and close to Sydney session lows. Today’s move brings the sell-off over the past 24 hours to around 15-20bps.

- The local calendar has been light today.

- Accordingly, today’s move has been a continuation of the firming of RBA tightening expectations following yesterday’s RBA Minutes.

- The push to cycle highs for US tsy and JGB yields have also impacted. So far in Asia-Pac trade today, cash US tsys are flat to 2bps richer.

- Following news that the BOJ may raise its inflation projections, the JGB curve has bear-steepened, with yields 0.9bps to 5.2bps higher.

- Cash ACGBs are 9-11bps cheaper, with the AU-US 10-year yield differential 3bps higher at -18bps.

- Swap rates are 10-11bps higher.

- The bills strip has bear-steepened, with pricing -4 to -13.

- RBA-dated OIS pricing is 4-13bps firmer for ’24 meetings.

- Tomorrow, the local calendar sees the Employment Report for September, along with the release of NAB Business Confidence.

- Bloomberg consensus has 20k new jobs with the unemployment rate stable at 3.7%.

- QTC has announced the launch of a new 5.25% 21 July 2036 bond. Initial price guidance is a range of 80-84bps over the 10-year futures contract. This transaction is expected to price tomorrow, subject to market conditions.

AUSTRALIAN DATA: Westpac Lead Indicator Suggests Growth Stabilising Below Trend

The Westpac leading index for September rose 0.07% after falling -0.04% resulting in the 6-month annualised growth rate improving to -0.3% from -0.5%, the best result since August 2022 when the series turned negative. It continues to indicate that growth will be below trend through the first half of 2024.

- Activity is stabilising but weaker equities and lower hours worked weighed on the index. US IP, widening of bond yields and steadying of building approvals have driven the improvement in the 6-month rate. Westpac also observes that the contribution from commodity prices has stabilised.

- Westpac is forecasting GDP growth of 1.2% y/y in 2023 and 2024 after 3.7% in 2022, compared with population growth of 2.3%.

Source: MNI - Market News/Refinitiv

NZGBS: Cheaper But Off Worst Levels, Outperformance In $-Bloc Continued

NZGBs closed 1-5bps cheaper but near the best levels of the local session. With no significant domestic events until the release of trade balance data on Friday, it's probable that local participants have been closely following global bond market trends. This attention has been driven by the overnight uptick in US tsy yields to new cycle highs and the current surge in longer-dated JGBs to fresh cycle peaks.

- Nevertheless, NZGBs have managed to add to yesterday’s post-CPI-induced outperformance in the $-bloc. The NZ-US and NZ-AU 10-year yield differentials have narrowed another 4-6bps today, bringing the cumulative outperformance from pre-CPI levels to 8-9bps.

- Swap rates are flat to 3bps higher, with the 2s10s curve steeper and implied swap spreads tighter.

- RBNZ dated OIS pricing is flat to 3bps firmer across meetings, unwinding some of yesterday’s post-CPI softening. Nevertheless, pricing remains 5-7bps softer than pre-CPI levels. Terminal OCR expectations sit a 5.65% versus the pre-CPI level of 5.72%.

- Tomorrow, the NZ Treasury plans to sell NZ$200mn of the May-26 bond, NZ$200mn of the May-34 bond and NZ$100mn of the May-41 bond.

- Later today, the US calendar sees House Starts and the Fed’s Beige Book. There is also a number of Fed speakers.

EQUITIES: Tracking Weaker, US Futures Lower, Oil Prices Up On Middle East Tension

Regional equity markets are mostly tracking lower in the first part of Wednesday trade. For the most part losses are modest, but sentiment has struggled amid a further rise in oil prices and on-going China property market concerns. US futures are down, Eminis last off by 0.10%, with higher oil prices weighing as a Middle East summit meant to held in Jordan was cancelled. We are off session lows though, the active contract last near 4397 (against earlier lows of 4386).

- In China, the CSI 300 sits 0.57% weaker at the break. Northbound stock connect outflows continue. This comes despite a better Q3 GDP print and higher y/y retail sales for September. Still, IP and retail sales slowed in m/m terms for September, and property sales/investment remained weak.

- A potential dollar bond default from Country Garden is also weighing on broader property sentiment. The CSI 300 real estate index is off a further 0.83%. The index has fallen in 7 out of the last 8 sessions.

- The HSI is off by 0.10% at the break, which is comfortably above earlier session lows.

- In Taiwan, the Taiex is one of the weaker performers in the region, off by over 1%. Weakness in the semiconductor sector is the main drag. South Korean shares are doing better, holding close to flat at this stage. The ASX 200 sits slightly higher in Australia.

- In SEA, most markets are down, although Thailand is outperforming, up 0.50% at this stage.

FOREX: Greenback Reverses Gains After Chinese Data

The USD reversed an early uptick which was seen alongside higher Oil prices after China's Q3 GDP, September Industrial Production and Retail Sales were firmer than forecast. Ranges remain narrow in today's Asian session and there has been little follow through on moves. WTI has held it's early gains and is up ~2%. US Tsy Yields are little changed across the curve. E-minis have pared losses and sit ~0.2% lower.

- The AUD is the strongest performer in the G-10 space, early losses were reversed after the Chinese data and AUD/USD sits up ~0.2%. Technically AUD/USD is bearish, the pair is supported at $0.6286 low from Oct 3. Resistance is at $0.6445, high from Oct 11.

- Kiwi was also pressured before reversing losses and NZD/USD now sits above the $0.59 handle.

- Yen is a touch firmer however there has been little follow through on moves. Resistance in USD/JPY remains at ¥150.16, Oct 3 high and bull trigger. Support is at the 20-Day EMA (¥148.74).

- Elsewhere in G-10 EUR and GBP are little changed from opening levels. BBDXY is marginally softer.

- CPI data from the UK provides the highlight in Europe today.

OIL: Crude Stronger On Better China Data And Heightened Middle East Risks

Oil prices are higher today driven by increased uncertainty in the Middle East after the Jordan leg of US President Biden’s trip was cancelled due to an explosion at a Gaza hospital. Stronger domestic data in China also supported prices but they are now off the high reached directly after the data was released. The USD index is flat.

- Brent is currently 1.8% higher during APAC trading at $91.54/bbl. Earlier it broke through $92 briefly following China data, which showed apparent oil demand up 17% last month. WTI is up 2.1% to $88.45 and reached a high of $89.09.

- Uncertainties in the Middle East continue to cause jitters in energy markets. There are concerns that the conflict will spread particularly to Iran, who also controls the strategic Strait of Hormuz, at a time of tight supplies. On a more positive note, Venezuela’s government and opposition have agreed on terms for a fair election, which would result in an easing of oil sanctions.

- Bloomberg reported that US crude inventories fell a more-than-expected 4.38mn barrels after rising 12.9mn in the previous week according to API data. Later official EIA data print and a drawdown of just over 1mn barrels is expected.

- Later there are numerous Fed speakers including Waller, Williams, Bowman, Barkin, Harker and Cook plus the release of the Beige Book. In terms of data, there are US housing starts/permits and UK CPI. ECB’s Lagarde is also scheduled to speak.

GOLD: Highest in Four Weeks As Hopes Of A Diplomatic Resolution To Middle East Conflict Fade

Gold is 0.7% higher in the Asia-Pac session, the highest level in four weeks, as the intensifying conflict in the Middle East bolstered haven demand. Hopes for a diplomatic resolution deteriorated after a deadly explosion at Gaza hospital left hundreds dead and Arab leaders pulled out of a meeting planned with US President Joe Biden on his scheduled visit to Israel and Jordan.

- Bullion closed +0.2% at $1924.06 on Tuesday as geopolitical concerns and a softer USD offset a strong push higher in Treasury yields.

- US Treasury yields were pushed to or close to cycle highs after another batch of hot data. Retail sales were strong, with the ex-auto and gas measure rising by 0.6% m/m in September, above the 0.1% expected. The strength of domestic data was later reinforced by an upward revision to the Atlanta Fed’s GDPNow to 5.4% annualised for Q3.

- By the NY session close, US Treasury yields had lifted chunky 8-15bps, with the belly underperforming. The 5-year yield printed a high of 4.89%, its highest level since 2007

- According to MNI’s technical team, the high of $1931.58 came close to a key resistance at $1932.9 (Oct 13 high).

SOUTH KOREA: MNI BoK Preview - October 2023: On Hold, Policy Bias Likely To Stay Restrictive

- The BoK is widely expected to hold rates steady at 3.50%. Focus is likely to be on the BoK's policy bias, which should stay restrictive/open to another hike, given still elevated inflation pressures. Market pricing is roughly around a full +25bps within the next 6 months.

- Financial stability concerns are also likely to feature, although macroprudential policies may be the preferred path to deal with higher household debt levels.

- The BoK is likely to be encouraged by some signs of improving external demand, but elevated uncertainty is still likely to feature in terms of how the central bank describes the outlook.

- See the full preview here:

INDONESIA: MNI Bank Indonesia Preview - October 2023: Extended Pause, Focus On IDR

- Bank Indonesia (BI) is expected to leave rates unchanged at 5.75% at its October 19 meeting with the policy focus on IDR stabilisation as it has depreciated further versus the greenback and on a trade-weighted basis since the last meeting. The weaker IDR doesn’t mean that there needs to be another hike when the economy doesn’t need it, BI has other tools it can use to strengthen the currency.

- Inflation remains contained and at the bottom of BI's target band. While there may be little downside left for headline inflation due to less favourable base effects, and higher oil & food prices, BI looks at second-round effects and so core developments will be its focus. Core CPI moderated 0.2pp to 2% in September.

- BI's pause is likely to be extended well into 2024 as it shores up the rupiah while it remains unclear when the Fed will be finished tightening. A prerequisite for the start of an easing cycle is likely to be IDR stabilisation.

- See full preview here.

INDONESIA: Q3 Growth Solid But May Be Slowing

In September Bank Indonesia (BI) said that “economic growth in Indonesia remains solid, supported by domestic demand”. While consumer confidence and the S&P Global manufacturing PMI both eased in September they continue to point to “solid” growth but possibly slower. BI’s own measure of business activity has been trending higher over the year and is almost 2 points higher than Q3 last year. Domestic demand is unlikely to be as strong as it was in Q2 as the large rise in public spending is probably won’t be repeated, but private sector activity is still looking robust. However, annual real export growth fell in Q2 and is also looking weak in Q3. BI meet again on Thursday (see MNI BI Preview here).

Indonesia private consumption vs consumer confidence

Source: MNI - Market News/Refinitiv

Indonesia GDP growth vs BI business activity index

Source: MNI - Market News/Refinitiv

ASIA FX: USD/Asia Pairs Lower, But Regional Equity Weakness Curbs Dollar Losses

Most USD/Asia pairs are lower for the session, but we are away from session bests, as regional equity sentiment has been weighed by on-going China property market concerns. This took the shine off earlier Q3 GDP/September activity beats in China. MYR and IDR have lagged the rest of the region, with both currencies modestly weaker. Tomorrow the focus is on the BI and BOK decisions. Both central banks are expected to hold steady.

- USD/CNH has climbed off session lows in recent dealings. After getting just under 7.3050, we last tracked just above 7.3160. We are still off earlier highs near 7.3275 and still +0.10% higher in CNH terms for the session. Spot USD/CNY still sits lower, the pair last near 7.3070. The better than expected Q3 GDP print was welcomed by the market, likewise in terms of the better retail sales y/y outcome and steady IP growth. Still, BBG notes that growth in both IP and retail sales slowed in the month of September versus August. The property side also remains weak, with investment off -9.1% ytd y/y, with new construction and funds for property development remaining weak. Local equities are around session lows, with the CSI 300 off nearly 0.60%. The property sub-index making fresh cyclical lows. The above data prints not helping, while a potential Country Garden dollar bond default is also a drag.

- 1 month USD/KRW sits below recent highs, the pair last near 1348. Onshore equities are around flat, modestly outperforming weaker trends elsewhere. Tomorrow the BOK decision is no due. no change is expected at this stage.

- The bias in spot USD/IDR remains a buy on dips strategy. Equally though, we aren't seeing a break higher in the pair. Latest spot levels deal at 15730, little changed versus Tuesday closing levels. Highs from last week around 15740 remain intact. Beyond that lies end Dec 2022 highs of 15763. Recent dips towards the 15680 level have been supported. The 20-day EMA continues to trend higher, last near 15600. The near term macro focus rests with tomorrow's BI policy meeting. No change is expected but IDR weakness may be in renewed focus. The weaker IDR doesn’t mean that there needs to be another hike when the economy doesn’t need it, BI has other tools it can use to strengthen the currency.

- Spot USD/HKD tracks near 7.8240 in recent dealings. This is close to unchanged for the session. Earlier lows in the week sub 7.8200 were support. Back to late September, the 7.8150/60 region has seen dollar support emerge. On the topside, offers have emerged on moves above 7.8250, so not too far from current spot levels. These shifts in USD/HKD broadly match short rate US-HK interest rate differentials. The 3 month spread was last at +20bps, above late September lows, but not showing a strong trend in October to date. HKMA Chief Eddie Yue reiterated yesterday that Hong Kong has no intention to change the HKD peg system

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing on Tuesday and remains well within recent ranges. The measure sits ~0.6% below the top of the band. USD/SGD is holding in a narrow range above the 20-Day EMA ($1.3667) as of yet the pair has been unable to sustain a rally above the $1.37 handle. We sit at $1.3685/90. Looking ahead, a reminder that the local docket is empty for the remainder of the week.

- The Ringgit has been pressured in early dealing as participants digest Tuesday's rise in US Tsy Yields. USD/MYR printed at fresh YTD high at 4.7478 before marginally paring gains to sit at 4.7400/20. Palm Oil firmed to its highest level since mid-September yesterday rising as much as 0.7% as supply concerns and a rally in Soybean Oil in the US added a layer of support.

- The Rupee has opened a touch below Tuesday's closing levels, USD/INR remains well within the recent range as narrow ranges continue to persist. USD/INR sits at 83.2250/2350, the pair has been dealing in a narrow range between the 20-Day EMA (83.18) and 83.28 handle. A reminder that the local data docket is empty until 31 October when September Fiscal Deficit and Sep Eight Infrastructure Industries cross.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/10/2023 | 0030/1130 | *** |  | AU | RBA board meeting minutes |

| 17/10/2023 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 17/10/2023 | 0900/1100 | *** |  | DE | ZEW Current Conditions Index |

| 17/10/2023 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 17/10/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 17/10/2023 | 1200/0800 |  | US | New York Fed's John Williams | |

| 17/10/2023 | - |  | EU | ECB's de Guindos attends Luxembourg Ecofin meeting | |

| 17/10/2023 | 1230/0830 | * |  | CA | International Canadian Transaction in Securities |

| 17/10/2023 | 1230/0830 | *** | | CA | CPI |

| 17/10/2023 | 1230/0830 | *** | | US | Retail Sales |

| 17/10/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 17/10/2023 | 1315/0915 | *** | | US | Industrial Production |

| 17/10/2023 | 1320/0920 | | US | Fed Governor Michelle Bowman | |

| 17/10/2023 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 17/10/2023 | 1400/1000 | * | | US | Business Inventories |

| 17/10/2023 | 1445/1045 | | US | Richmond Fed's Tom Barkin | |

| 17/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 17/10/2023 | 1700/1900 | | EU | ECB's De Guindos Speech at Conference | |

| 17/10/2023 | 2000/1600 | ** | | US | TICS |

| 17/10/2023 | 2100/1700 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.