Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

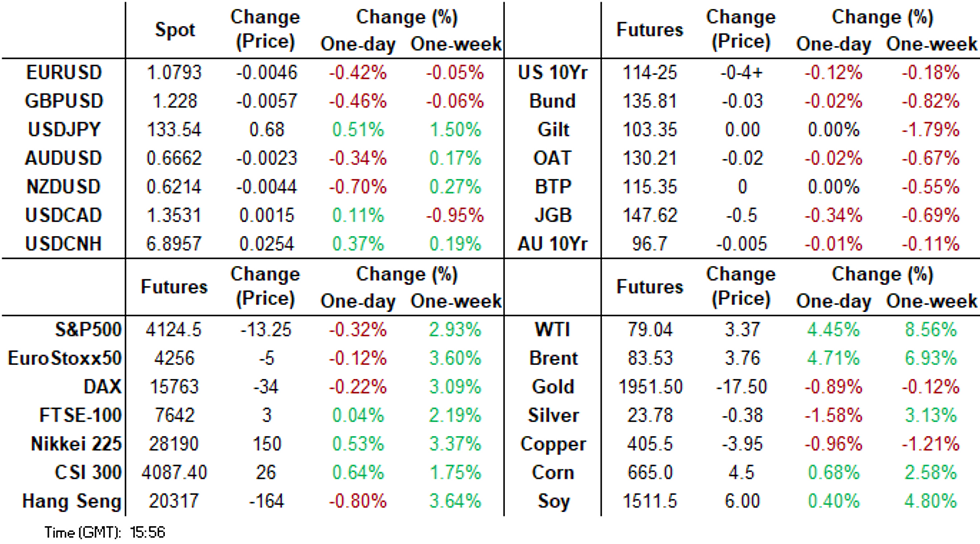

- The start of the week has been dominated by fallout from the weekend news of OPEC’s surprise announcement that it will cut output by 1.1mbd from May. Oil prices surged at the open but both Brent and WTI are off intra-day highs, albeit still close to +4.5% higher.

- The spillover to other asset classes was evident in terms of a firmer US yield backdrop, with the 2yr back to 4.10% (+7bps), while US equity futures have stayed in the red, led by tech. The USD was also higher across the board. Even oil sensitive plays like NOK and CAD are weaker versus opening levels, albeit outperforming the rest of the G10. Similar trends were evident in USD/Asia pairs, with USD/CNH back close to 6.9000. A weaker than expected Caixin manufacturing PMI also weighed, although China equities outperformed amid broader Q2 growth optimism from onshore.

- Looking ahead, in Europe we have Swiss CPI, further out the ISM Manufacturing Survey and the final print of the Manufacturing PMI headline. Fedspeak from Governor Cook will also cross.

US TSYS: Cheaper In Asia, OPEC+ Cuts Oil Production

TYM3 deals at 114-23, -0-06+, with an observed range of 0-13 on volume of ~56k.

- Cash tsys sit 4-8bps cheaper across the major benchmarks, the curve has bear flattened.

- Tsys were pressured in early trade as OPEC+ announced a surprise oil production cut of more than 1 million barrels a day abandoning previous assurances it would hold supply steady linkhere.

- In the wake of the weaker than expected Caixin Mfg PMI print tsys were marginally pressured, however daily ranges remained intact in TU and TY.

- Fed dated OIS price a ~16bp hike into the May meeting with the terminal rate at 4.98%, there are ~55bps of cuts priced for 2023.

- On the wires today in Europe we have Swiss CPI, further out the ISM Manufacturing Survey and the final print of Manufacturing PMI headline. Fedspeak from Governor Cook will cross.

AUSSIE BONDS: Slightly weaker, Pressured by U.S. Tsys

ACGBs sit near session cheaps (YM -3.0 & XM -1.0) ahead of the bell with U.S Tsys pressured in Asia-Pac trade by news of a surprise oil production cut of more than a 1milllion barrels a day by OPEC+. The local data drop today had failed to provide a domestic catalyst for a market that has shifted its focus to tomorrow’s RBA rates decision.

- Cash ACGBs are 1-2bp cheaper with the 3/10c curve 1bp flatter with the AU-US 10-year yield differential +4bp at -21bp.

- Swaps are flat to 1bp richer with the 3s10s curve flatter and EFPs 2bp narrower.

- Bills pricing is 2-3bp weaker across the strip.

- Ahead of the RBA policy decision tomorrow, RBA dated OIS is 1-4bp firmer for meetings beyond April with a 15% chance of a 25bp hike priced for tomorrow.

- On the local data front, the Inflation Gauge eased to 5.7% in March from 6.3%, indicating that it likely peaked at 6.4% in January. Building Approvals showed a weaker-than-expected increase of 4.0% M/M (+10.0% expected) in February, while Home Loan data for February surprised on the upside with a fall of 0.9% M/M versus expectations of -1.8%.

- Further afield, today’s calendar is scheduled to deliver final prints for March Manufacturing PMIs globally along with the ISM Manufacturing Survey.

NZGBS: Late Session Bull Flattening

The NZGB 10-year benchmark closed at session bests despite weaker U.S Tsys in Asia-Pac trade. Without an obvious catalyst, late session strength in the long end appeared to be driven by the local market playing catch-up to U.S. Tsy strength ahead of the weekend. At the bell benchmark yields were 2-9bp lower with the 2/10 curve 7bp flatter and the NZ/US 10-year yield differential 4bp narrower at +60bp.

- 2s10s swaps curve bull steepened sharply into the close with rates flat to 10bp richer. The implied swap spread box curve flattened.

- RBNZ dated OIS closed little changed today with 28bp of tightening priced for Wednesday’s meeting and terminal OCR expectations at 5.28% (28bp of additional tightening assuming a 25bp hike this week).

- The RBNZ released a Debt-to-Income (DTI) framework that set the specifications that banks need to comply with if a DTI tool is activated. The publication does not immediately activate DTI restrictions.

- The local calendar is light ahead of the RBNZ decision on Wednesday with the NZIER Quarterly Business Opinion Survey tomorrow as the highlight.

- In Australia, the RBA policy is slated for tomorrow with a no-change outcome expected.

- Further afield, today’s calendar is scheduled to deliver final prints for March Manufacturing PMIs globally along with the ISM Manufacturing Survey.

EQUITIES: China Shares Outperform, Mixed Trends Elsewhere As Oil Price Spike Assessed

Much of the focus today has been on the fallout from the oil price spike post the weekend news of OPEC+ cutting production. Sentiment around the region is mixed, with still some positive carry over from last week's gains in US and EU bourses helping at the margin. Still, futures for both these markets are lower today, led by the Nasdaq (-0.57%).

- This backdrop has seen some modest underperformance of tech related plays, but only at the margins. The HSI is off by 0.59%, with the tech sub index off by -1.2% at this stage. The Kospi, in South Korea is also weaker, down 0.15%.

- China shares have fared better. The CSI up nearly 0.90%, the Shanghai Composite +0.56%. Optimism around the Q2 recovery from onshore equities, along with positive housing market data likely positive catalysts. This has offset the weaker than expected Caixin manufacturing PMI for March (50.0 versus 51.4).

- Japan stocks are outperforming modestly, up close to 0.60% for the Topix index at this stage.

- Elsewhere there has been some divergence around commodity exposure. The ASX 200 up around 0.60%, while the JCI in Indonesia has risen 0.20% and Malaysia's bourse 0.34%. These markets have outperformed Thai and Indian equities, but the divergences haven't been large.

GOLD: Threatening Downside Break Of $1950, Amid Broad USD Gains

Gold has spent the first part of the Monday session mostly on the back foot. The precious found some support under $1950, but hasn't been able to rebound far, last near $1951.50. This leaves us still around 0.9% lower from closing levels at the end of last week (above $1969). Gold weakness has predominantly been driven by the firmer dollar backdrop. The DXY is up 0.50%, last above 103.00.

- The spill over from the oil price surge (following the weekend OPEC+ supply cut) is evident in terms of higher US yields, which has aided the USD and weighed on equity futures.

- Still, there hasn't been any safe haven demand for gold at this stage.

- On the downside, March 27 lows came in close to $1943, below that is 22nd lows near $1934.

OIL: Crude Surges On OPEC+ Output Cut News, But Off Intraday Highs

Oil prices have jumped during APAC trading today following OPEC’s surprise announcement on Sunday that it will cut output by 1.1mbd from May following October’s 2mbd reduction. Prices are off their peaks but are still up over 5.5%. WTI is around $79.67/bbl and Brent $84.00 following intraday highs of $81.69 and $86.44 respectively. The USD index is 0.5% higher.

- Today’s rally has seen Brent break through both the 50- and 100-day simple moving averages and it is now heading towards the 200-day at $84.77.

- Saudi Arabia will account for 500kbd of the output reduction with UAE, Kuwait and Algeria making up the rest. Russia also announced that its production cuts will be extended to year end from June. Goldman Sachs has increased its forecast for end-2023 Brent to $95 and end-2024 to $100. There is a chance now that Q2 will post a deficit when a crude surplus had been expected.

- The announcement is likely to weigh on already strained US-Saudi relations and make it harder for central banks to bring inflation down.

- Later today March manufacturing PMIs print in the US and Europe and the US ISM is also released.

FOREX: USD Firmer In Asia as OPEC+ Cuts Oil Production

The greenback is firmer in the Asian session on Monday. Over the weekend OPEC+ announced a surprise oil production cut of more than 1 million barrels a day abandoning previous assurances it would hold supply steady linkhere.

- Kiwi is pressured, NZD/USD is down ~0.6%. The pair is dealing a touch below its 20-Day EMA ($0.6227). NZ Residential Property listings in March were the lowest since 2007 falling 18% Y/Y. Fonterra has lowered FY23 forecast farmgate milk prices to NZ$8.00-8.60/kg down from NZ$8.20-8.80/kg, as Chinese demand has not returned to expected levels and supply is increasing as the Northern Hemisphere entered spring.

- AUD/USD prints at $0.6660/70, ~0.3% softer. Judo Bank Manufacturing PMI printed its lowest level since May 2020 at 49.1.

- Yen is pressured as rising US Treasury Yields weigh, USD/JPY is up ~0.3% last printing at ¥133.35/45. Resistance comes in at ¥133.59, the high from 31 March.

- Elsewhere in G10 NOK was ~0.4% firmer in early dealing, however gains have been pared and USD/NOK is flat. EUR and GBP are both ~0.4% softer.

- Cross asset wise; WTI futures are ~5.5% firmer, they were however ~7% firmer in early dealing. BBDXY is ~0.4% higher, 10 Year US Treasury Yields are up ~5bps.

- On the wires today in Europe we have Swiss CPI, further out the ISM Manufacturing Survey and the final print of US Manufacturing PMI headline.

FX OPTIONS: Expiries for Apr03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0850-55(E672mln), $1.0900(E1.1bln), $1.1000-10(E1.1bln)

- USD/JPY: Y128.00($1.5bln)

ASIA FX: USD/Asia Pairs Rally, Some Outperformance From IDR & MYR

USD/Asia pairs are higher across the board, with fallout from the oil price spike felt around the region. There has been some modest outperformance from currencies with some commodity exposure, like MYR and IDR, while KRW and THB have been underperformers. Tomorrow, South Korean CPI is on tap, which is the main event risk for the session.

- USD/CNH tested back above 6.9000, amid broad USD gains and a weaker than expected Caixin manufacturing PMI print. We are now back close to 6.8950, still around 0.35% weaker versus closing levels at the end of last week. The onshore equity backdrop is better, with the CSI 300 up 0.87% at this stage, which has likely helped the currency at the margins.

- 1 month USD/KRW got above 1318 before selling interest capped the move. This is still multi week highs. The simple 200-day MA comes in near 1324. Over the weekend exports remained around recent lows for Mar, although the trade deficit was better than expected. The 1 month last sat at 1314/15.

- USD/IDR edged back above 15000 in the first part of trading, but has seen very little follow through dollar demand. This leaves the pair little changed for the session, which is outperforming the firmer USD backdrop elsewhere in the Asian FX space. The better commodity backdrop evident today from a palm oil standpoint is helping. On the data front today we have already had the Mar PMI, coming in better than the prior read (51.9 from 51.2). Mar CPI came in lower than forecast, headline at 4.97%, versus 5.12% expected.

- The Ringgit is marginally outperforming USD/Asia this morning as it benefits from OPEC+ unexpected production cuts which were announced over the weekend. WTI futures are up ~5.5% having been as much as 7% firmer in early trade. Palm Oil futures are also firmer currently up ~2.5% having risen over 3% in early dealing. Bears target the March lows at 4.3857, bulls look to break the 20-Day EMA to turn the tide (4.4406).

- USD/SGD is ~0.3% firmer today, dealing a touch below the 20-Day EMA ($1.3354), as SGD follows the broader USD/Asia trend after a softer than expected Caixin MFg PMI print from China. Bulls first look to break the 20-Day EMA ($1.3354) from here they can target the March high at $1.3576. The next downside target for bears is the 2023 low at $1.3032. The SGD NEER is slightly higher, albeit within recent ranges.

- USD/THB is back above 34.40, close to +0.60% firmer versus Friday closing levels. This is close by to the 100-day MA, with rallies beyond this level not sustained in late March, early February.

ASIA PMIs: ASEAN Manufacturing PMI Eases As Orders Slow, Price Pressures Moderate

The March Global S&P manufacturing PMI for the ASEAN region eased to 51 from 51.5, below average, but importantly confidence ticked up. The results were mixed at a country level with 4 out of 7 seeing improving conditions. The result was driven by slower output and order growth. Employment and stocks of purchases contracted. Price pressures eased with output inflation reaching a 16-month low. (See press release here.)

- Indonesia’ PMI rose to 51.9 from 51.2 driven by faster new orders and output, which resulted in stronger employment and purchasing. The improvement in business confidence and expected future sales performance is positive for the outlook. While input costs rose, the trend remains one of easing inflation pressures. Producers were still able to pass on these higher costs but it was at a slower rate.

- Thailand’s PMI eased to 53.1 from 54.8 but remained the second strongest in the region. The decline was driven by declining new orders (including foreign orders) but output remained strong as the backlog of orders was worked through. Business confidence improved, implying the order weakness may be temporary, but optimism wasn’t reflected in hiring. Supply constraints continued and price pressures worsened signalling further BoT tightening ahead.

- The PMI in the Philippines eased slightly to 52.5 (Feb 52.7) and reported a welcome easing in price pressures. Malaysia and Singapore saw contractions in manufacturing at 48.8 (Feb 48.4) and 48.9 (50) respectively.

Source: MNI - Market News/Global S&P

AUSTRALIAN HOUSING: Home Lending Decline Eases, Approvals Signal Worsening Shortages

Today’s housing-related data for February and March is not what would be expected after over 300bp of tightening. Not only did CoreLogic report a 0.6% m/m rise in March home prices, but consistent with this home loan values fell at their lowest rate since May 2022 and previous months were revised up. Building approvals were less than expected but January was revised up. They are notoriously volatile due to the apartment component. Immigration is supporting the housing sector and talk of the RBA being close to a peak may also be injecting a bit of confidence.

- Home loan values for February fell 0.9% m/m after an upwardly revised -2.4% the previous month. They are now down 30.9% y/y off the January 2023 trough of -32.6% but still over 18% above February 2020. Owner-occupied loans fell 1.2% m/m and -30% y/y after -2.1% and -32.6%. Investor loans fell 0.5% m/m, the highest since March 2022, and -32.6% y/y but the level of lending remains strong at 47% above pre-pandemic levels.

- The value of first time homebuyer loans rose 0.9% m/m, the first increase since August 2022, they are still down 26.8% y/y, but off the December 2022 trough of -35.6%. The number of new loans though fell 3.5% m/m after -4.6%.

- The ABS reported that refis rose 3.5% to a record high, as mortgage holders come off fixed rates and look for better deals.

- Building approvals rose 4% m/m with private houses rising a robust 11.3% but not fully unwinding the seasonal January drop of 13.5%. Total approvals are now 21.6% below pre-Covid levels with houses -1.9% but multi-dwelling units 45.9% below - this trend is exacerbating Australia’s housing shortage and is also likely to support prices and rents going forward.

Source: MNI - Market News/ABS

Australia number of dwellings approved - private sector houses

Source: MNI - Market News/ABS

AUSTRALIAN INFLATION: Inflation Gauge Confirms Inflation Peak Behind Us

The Melbourne Institute’s inflation gauge eased to 5.7% in March from 6.3%, indicating that it likely peaked in January at 6.4%. It rose 0.3% m/m after 0.4% in February and 0.9% in January. The trimmed mean measure rose 0.4% m/m and 5.2% y/y, which rose 4.9% the previous month. The MI inflation gauge is signalling that price pressures persist but are easing. Analysts are divided over the outcome of Tuesday’s RBA meeting. Q1 CPI data is released on April 26, which should give a clearer picture on domestically-driven inflation.

Australia CPI vs MI inflation gauge y/y%

Source: MNI - Market News/Refinitiv/ABS

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/04/2023 | 0630/0830 | *** |  | CH | CPI |

| 03/04/2023 | 0700/0300 | * |  | TR | Turkey CPI |

| 03/04/2023 | 0715/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 03/04/2023 | 0745/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 03/04/2023 | 0750/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 03/04/2023 | 0755/0955 | ** |  | DE | IHS Markit Manufacturing PMI (f) |

| 03/04/2023 | 0800/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 03/04/2023 | 0830/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 03/04/2023 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 03/04/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 03/04/2023 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 03/04/2023 | 1400/1000 | * | | US | Construction Spending |

| 03/04/2023 | 1430/1030 | ** |  | CA | BOC Business Outlook Survey |

| 03/04/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 03/04/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 03/04/2023 | 2015/1615 | | US | Fed Governor Lisa Cook |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.