Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

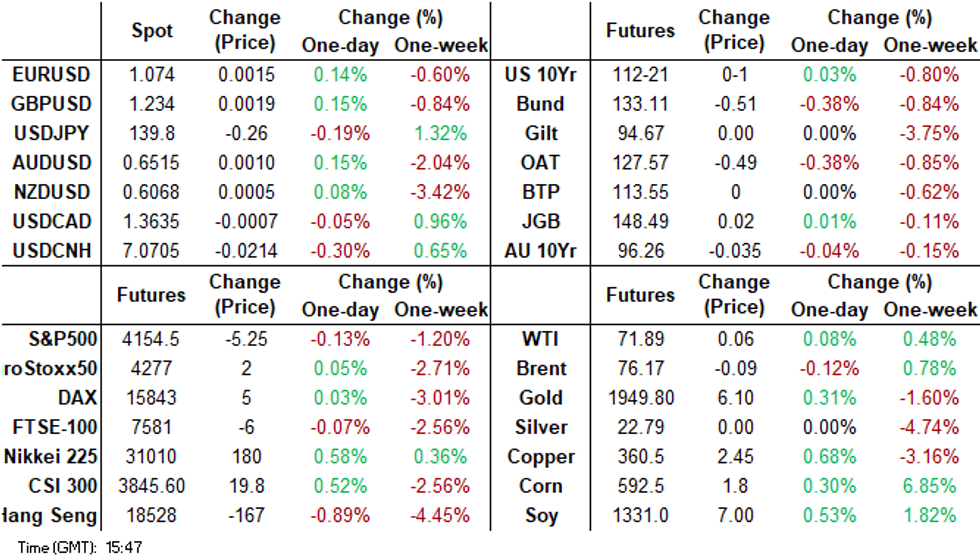

- Tsys were pressured in early dealing as concerns over the US Debt Ceiling impasse weighed. House Speaker McCarthy noted that this is no agreement on the US Debt Ceiling. TY dealt below Thursdays lows, however the move did not follow through.

- $-Bloc markets are signaling that further tightening measures are on the horizon, a stark deviation from the message conveyed on May 8 when it was widely believed that the tightening cycle was nearing its conclusion.

- The USD is a touch lower in Asia on Friday, the Antipodeans were pressured in early dealing however losses were pared. AUD and NZD sit a touch firmer. USD/JPY is back sub 140.00, last 139.75. Tokyo Apr CPI was mixed, but Finmin Suzuki stated FX levels were being watched closely. USD/CNH hit fresh highs near 7.1000, but reported USD sales onshore helped curb gains.

- In Europe today we have UK Retail Sales, further out US PCE deflator, Consumer income, Wholesale Inventories, Durable Goods and UofMich Consumer Sentiment crosses.

MARKETS

US TSYS: Marginally Richer In Asia

TYM3 deals at 112-21, +0-01, a 0-05+ range has been observed on volume of ~76k.

- Cash tsys sit 1-2bps richer across the major benchmarks, the curve has bull steepened.

- Tsys were pressured in early dealing as concerns over the US Debt Ceiling impasse weighed. House Speaker McCarthy noted that this is no agreement on the US Debt Ceiling. TY dealt below Thursdays lows, however the move did not follow through.

- A recovery off session lows was seen as the USD retreated off best levels and e-minis pared early losses.

- Tsys held richer for the remainder of the Asian session however ranges remained narrow and moves had little follow through..

- In Europe today we have UK Retail Sales, further out US Consumer income, Wholesale Inventories, Durable Goods and UofMich Consumer Sentiment crosses.

STIR: Tightening Cycle Isn’t Over In The $-Bloc

$-Bloc markets are signaling that further tightening measures are on the horizon, a stark deviation from the message conveyed on May 8 when it was widely believed that the tightening cycle was nearing its conclusion.

- This week has seen a significant firming across meetings as hawkish Fedspeak and the release of FOMC minutes for May, which revealed a division among officials regarding their support for further interest rate hikes, pressure pricing. A cumulative 25bp of tightening is now priced by July, with year-end easing scaled back to 37bp from 51bp on Monday and 80bp on May 11.

- CA STIR has also moved to price in more than one cumulative 25bp hike by October. At the end of last week, only 11bp of further was priced.

- Terminal rate expectations have pushed to a post-May RBA hike high of 4.01% this week ahead of retail sales data for April today.

- In sharp contrast to the other $-Bloc markets, NZ STIR has shunted softer following the dovish hike from the RBNZ. RBNZ dated OIS pricing is 26-29bp softer across meetings with the terminal rate dropping from 5.93% pre-RBNZ to 5.66% currently.

Figure 1: $-Bloc STIR: Terminal Rate Expectations & Year-End Pricing

Source: MNI – Market News / Bloomberg

JGBS: Futures Reverse Morning Weakness in Afternoon Trade, 40-Year Outperforms

JGB futures strengthen in the afternoon session, unwinding morning weakness, to be -5 compared to the settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Tokyo CPI and PPI Services data.

- Local market participants seemed content to track US tsys in anticipation of the release of April US PCE deflator data later in the day. US tsys were 1-2bp richer in Asia-Pac trade.

- Cash JGBs are little changed out to the 10-year zone, but richer beyond. The benchmark 10-year yield is 0.1bp higher at 0.427%, below the morning session high of 0.454%. The 40-year has reversed morning underperformance to be the star performer in the afternoon session. The yield is 2.2bp lower at 1.450% after hitting a morning high of 1.509%.

- Swap rates are trading mixed with the curve exhibiting a flattening bias. Swap spreads are generally narrower out to the 30-year zone and wider beyond.

- The local calendar next week sees Leading and Coincident Indicators (Mar F) on Monday, Jobless Rate (Apr) on Tuesday, Retail Sales (Apr), IP (Apr P) and Housing Starts (Apr) on Wednesday, and Capital Spending (Q1) and Company Profits (Q1) on Thursday.

- The next week also has slated BoJ Rinban operation covering 3-25-year+ JGBs (Mon) along with 2-year (Tue) and 10-year (Thu) supply.

JAPAN DATA: Tokyo CPI Headline Misses, But Core-Core Fresh Y/Y Highs

Tokyo CPI prints for May were mixed. The headline y/y coming in weaker at 3.2%, versus 3.4% forecast and 3.5% prior. Headline CPI is now some distance below Jan highs of 4.40%. We saw the exact same outcomes for the measure which excludes fresh-food (3.2% y/y, versus 3.4% expected). The core measure which excludes both fresh-food and energy was in line with expectations though, +3.9%, versus 3.8% prior.

- This is a fresh high for the core measure in y/y terms since 1982. Looking at the sub-categories, we saw 6 out of 10 record faster y/y momentum compared to Apr. Utilities, down -7.3% y/y, was a big drag on the softer headline result (down -4.1% m/m).

- All categories saw m/m increases except for household goods and utilities, (while housing was flat).

- Overall goods inflation was -0.2% m/m, while services rose 0.1%, slightly down from the recent pace of 0.2-0.3%.

- Market reaction has been limited, USD/JPY drifting up from session lows to 140.00 (earlier lows were at 139.87, as US equity futures softened).

AUSSIE BONDS: Cheaper, Narrow Range, Awaits US PCE Deflator

ACGBs are weaker (YM -5.0 & XM -4.0) although holding above session lows. ACGBs traded within a relatively narrow range in the Sydney session with no significant domestic catalysts.

- Local market participants seemed content to adopt a wait-and-see approach in anticipation of the release of April US PCE deflator data later in the day. According to BBG consensus, the core PCE deflator is expected to show a monthly increase of 0.3% and a year-on-year figure of 4.6%, remaining unchanged from March.

- US tsys were 1-2bp richer in Asia-Pac trade.

- Cash ACGBs are 4bp cheaper with the AU-US 10-year yield differential -1bp at -6bp.

- Swap rates are 3-4bp higher with EFPs slightly tighter.

- The bills strip is steeper with pricing flat to -7.

- RBA dated OIS is little changed across meetings.

- The RBA has reiterated that it will consider later this year whether there is a case for selling Commonwealth government bonds off its balance sheet once banks have repaid the first tranche of the circa A$190bn they borrowed from RBA during the pandemic (AFR).

- The local calendar next week sees Building Approvals (Apr) on Tuesday, Construction Work Done (Q1), Private Sector Credit (Apr) and CPI Monthly (Apr) on Wednesday, Capex (Q1) on Thursday and Home Loan data (Apr) on Friday.

NZGBS: Continue To Outperform in the $-Bloc

NZGBs closed 3-4bp cheaper after trading in a relatively narrow range. Without domestic drivers, local participants appear to have been happy to sit on the sidelines ahead of April US PCE deflator data later today. BBG consensus expects the core PCE deflator to print 0.3% m/m 4.6% y/y unchanged from March.

- NZGBs have continued their outperformance in the $-Bloc since the RBZ decision with NZ/US and NZ/AU 10-year yield differentials 3bp and 2bp respectively lower.

- Swap rates are 2-4bp higher with the implied long-end swap spread wider.

- RBNZ dated OIS closed with pricing 1-4bp firmer for meetings beyond August.

- RBNZ Silk said the impact of cyclone Gabrielle has been less inflationary than first feared. The Reserve Bank had initially estimated that Cyclone Gabrielle would add 0.3ppt to inflation in both the first and second quarters but has since downgraded that impact to just 0.1ppt. (link)

- ANZ consumer confidence index fell to 79.2 in May from 79.3 in April. Inflation expectations eased to 4.8% from 5.2%.

- The local calendar next week sees Building Permits (Apr) on Monday, ANZ Business Confidence (May) and CoreLogic House Prices (May) on Wednesday and Terms of Trade (Q1) on Friday.

FOREX: Greenback Marginally Pressured In Asia

The USD is a touch lower in Asia on Friday, the Antipodeans were pressured in early dealing however losses were pared. AUD and NZD sit a touch firmer. Early in the session House Speaker McCarthy noted that this is no agreement on the US Debt Ceiling. He also said he will stay at the Capitol and continue working until a deal is done.

- Yen is ~0.2% firmer, USD/JPY deals below the ¥140 handle however we remain well within recent ranges. Tokyo Headline and Core CPI were a touch below estimates.

- Kiwi is marginally firmer, NZD/USD was down as much as ~0.3% in early trade as e-minis extended losses and RBNZ's Silk noted that rates need to stay on hold for an extended period and that the bank is wary of over tightening. Support was seen ahead of year to date lows and losses were pared.

- AUD/USD is ~0.1% firmer, the pair dealt below the $0.65 printing a low of $0.6491 before paring losses to sit a touch firmer at $0.6510/15.

- Elsewhere in G-10 SEK is ~0.2% firmer, however liquidity is generally poor in Asia. EUR and GBP are both up 0.1%.

- Cross asset wise; e-minis are 0.1% softer however they were down as much as 0.3% in early trade. BBDXY is down ~0.2% and US Treasury Yields are softer across the curve.

- In Europe today we have UK Retail Sales, further out US Consumer income, Wholesale Inventories, Durable Goods and UofMich Consumer Sentiment crosses.

FX VOL: Implied Volatility Subdued Despite US Debt Ceiling Impasse

1 Month Implied volatility in FX markets, measured using the JP Morgan G-10 Volatility Index, have ticked away from year to date lows but remain subuded.

- The index prints at 8.60%, having printed its lowest level since March 2022 in mid-May at 7.78%.

- Option markets remain calm with vol well below elevated levels seen in the wake of the SVB crisis despite the impasse over the US debt ceiling and sticky inflation across G-10 markets.

Fig 1: JP Morgan G-10 Volatility Index

Source: JP Morgan/MNI/Bloomberg

EQUITIES: Tech Still Outperforming, Mixed Trends Elsewhere

Regional equity sentiment is mixed in Asia Pac for the final trading session of the week. Hong Kong markets have been closed today, which has lightened liquidity for the region. Tech related plays are outperforming modestly, while China and parts of SEA remain weaker.

- US futures are in the red, albeit with losses not extending beyond -0.30% for Eminis. The index was last at 4152, down by -0.2%, with Nasdaq futures off by a similar amount. Headlines from US House Majority Leader McCarthy that there is no agreement on the debt ceiling weighed at the margins in early trade. Negotiations are likely to continue into the weekend.

- In Taiwan, the Taiex is the outperformer, up over 1%, with positive Chip/Tech sentiment from Thursday trade in the US aiding moves. This is fresh highs for the index back to early June last year.

- The Kospi is also up but a more modest 0.15%, although offshore investors have bought another $487.7mn in local locals, brining week to date inflows to $881.6mn.

- China markets are weaker to the break, the CSI 300 off a further 0.40%. We are up from fresh lows though.

- In SEA, Philippines stocks are down around 0.80%, while Thai stocks are -0.40% at this stage, unwinding gains from earlier in the week.

OIL: Brent Close To Flat For The Week On Mixed OPEC Views

Brent crude is modestly lower versus NY closing levels from Thursday. We were last close to $76/bbl. This is well below highs for the week above $78.50/bbl, but we haven't tested Thursday session lows near $75/bbl so far today. WTI was last under $72/bbl, following a similar trajectory.

- Brent is barely in positive territory for the week, as the market continues to digest conflicting signals from OPEC+ members. Russia's Deputy Premier stating the group was unlikely to adjust production targets in June (next meeting is next weekend June 3-4). This contrasted with earlier comments from the Saudi Arabia Energy Minister, which stated speculators should 'watch out'.

- Speculation around the meeting outcome is likely to dominate market sentiment over the coming week.

- For Brent, a break sub $75/bbl would open up a move to the May 15 low around $73.50/bbl. On the topside, the 20-day simple MA comes in close to $79/bbl.

GOLD: Touched Two-Month Low, 6% From Peak

Gold is firmer at 1948.74 (+0.4%) in the Asia-Pacific session, after closing 0.8% lower on Thursday at 1941.41, a two-month low.

- Gold is on track for its largest weekly decline, currently standing at 1.5%, in nearly four months. This decline comes as indications of resilience in the US economy raise the likelihood of the Federal Reserve continuing its rate hikes. The US GDP saw a slight upward revision for Q1, reaching an annualized rate of 1.3%. Additionally, the core PCE deflator was revised upward by 0.1% to a 5.0% annual rate for Q1.

- Traders have now fully factored in another 25bp hike by July. Higher interest rates traditionally having a negative impact on gold, which does not offer interest-bearing returns. As a result, the metal has experienced a decline of approximately 6% since its peak in early May, largely driven by speculation surrounding interest rates.

- However, the ongoing impasse concerning the US debt-ceiling is providing some support to the haven asset.

ASIA FX: Onshore USD Sales Aids CNH, KRW & TWD Higher On Tech Optimism

Most USD/Asia pairs are lower today. CNH has been aided by reported state owned banks dollar sales onshore. KRW and TWD have also rallied on continued tech optimism. THB remains a laggard though with little progress around the election result.

- Headlines have crossed from Reuters that large state owned banks are reportedly selling USD/CNY onshore spot. The report notes the selling started on Thursday and has carried over to today. Offers emerged this morning when USD/CNH got close to 7.1000 (the high was 7.0986 per Bloomberg). Onshore spot USD/CNY is tracking lower last at 7.0600, -0.30% so far for the session. Earlier highs were close to 7.0800. USD/CNH is being dragged lower, last under the 7.0700 level. A recovery in onshore equities is also helping, the CSI erasing an earlier -0.9% loss.

- Won has outperformed in Asia FX over the past week. In spot terms the currency (last 1323/24) is the only one within the region to record a gain against the USD over this period (albeit a modest one at +0.2%). The 1 month USD/KRW NDF is back to 1321/22, around -0.55% sub NY closing levels from Thursday. Onshore equities are up modestly so far today, +0.20%, with tech sentiment remaining positive post Nvidia's results. We have seen chunky inflows from offshore investors in Korean shares, +487.7mn so far today, bringing weekly inflows to $881.6mn. For May we have seen $2054.5mn in inflows.

- TWD is also firmer, the USD/TWD 1 month NDF is back to 64.64, -0.40% so far for Friday's session. The Taiex is +1.20%, outperforming the rest of the region, as tech optimism continues.

- USD/INR is ~0.1% lower this morning, however narrow ranges are persisting after the pair printed its highest level since late February on Wednesday. The pair prints at 82.60/80, broader USD/Asia trends have dominated in May. The rupee has lost ~1% in May. Equity Inflows in May remain strong, with a further $374mn in Indian Equities bought by foreign investors this week to Wednesday. Looking ahead on the wires next week Q1 GDP headlines the data calendar, an increase of 5.1% is expected, ticking higher from 4.4% in Q4 2022.

- USD/THB sits just below recent highs, last around 34.65. We are around 0.15% weaker in baht terms versus yesterday's close. The currency is underperforming other USD/Asia pairs, which are seeing more downside so far today. This may reflect some carry over from USD strength post yesterday's onshore spot close. Election negotiations look set to continue into a third week, with no clear signs of a near term resolution.

- In Malaysia, April CPI printed at 3.3% Y/Y in line with expectations ticking lower from the 3.4% observed in March. The Ringgit pared early losses in recent dealing. USD/MYR is ~0.2% firmer today last printing at 4.6260/90. The pair has printed a fresh high for 2023 and is at its highest level since 11 Nov. MYR has lost ~4% so far in May.

- The SGD NEER (per Goldman Sachs estimates) is little changed this morning, we remain well within recent ranges. We now sit ~0.9% below the upper end of the band. USD/SGD is a touch softer this morning, the pair is down ~0.1% from opening levels. Broader USD trends are dominating flows in early dealing on Friday. April Industrial Production was weaker than forecast printing at -1.9 M/M vs 0.1% exp.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/05/2023 | 0600/0700 | *** |  | UK | Retail Sales |

| 26/05/2023 | 0600/0800 | ** |  | SE | Retail Sales |

| 26/05/2023 | 0600/0800 | ** | | SE | PPI |

| 26/05/2023 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 26/05/2023 | 0740/0940 |  | EU | ECB Lane Panels Dubrovnik Econ Conference | |

| 26/05/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 26/05/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 26/05/2023 | 1230/0830 | ** |  | US | Durable Goods New Orders |

| 26/05/2023 | 1230/0830 | ** | | US | Personal Income and Consumption |

| 26/05/2023 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 26/05/2023 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 26/05/2023 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.