Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

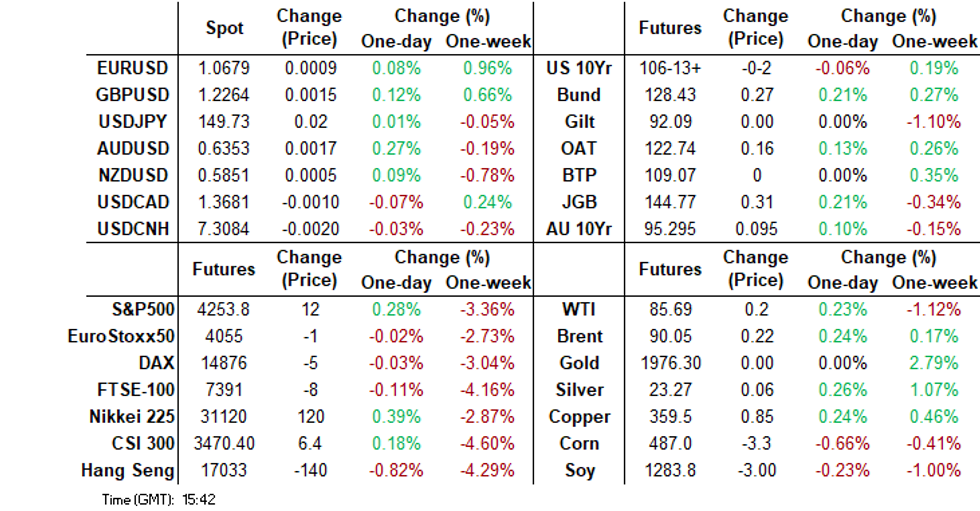

- US Tsys firmed off session lows alongside regional equities firming and pressure on the USD as risk sentiment improved through the Asian session. The BBDXY sits around 0.15% lower, while most USD/Asia pairs are lower.

- The BOJ announced an unscheduled bond purchase of ¥300bn worth of 5-to-10-year bonds and ¥100bn of 10-to-25-year JGBs at market prices. After some initial volatility, benchmark yields have moved lower by around 1-2bps across benchmarks.

- In Australia, RBA Governor Bullock’s speaks tonight at CBA’s annual conference (1900 AEDT) and then Q3 CPI tomorrow is out tomorrow.

- In Europe, ECB President Lagarde speaks, UK labour market data and European preliminary PMIs are out. In the US, preliminary October PMIs, Philly Fed non-manufacturing and Richmond Fed indices are released.

MARKETS

US TSYS: Narrow Ranges In Asia

TYZ3 deals at 106-13+, -0-02, a 0-06 range has been observed on volume of ~91k.

- Cash tsys sit 1bp cheaper to 1bp richer across the major benchmarks, the curve has twist flattened pivoting on 5s.

- Tsys firmed off session lows alongside regional equities firming and pressure on the USD as risk sentiment improved through the Asian session. However ranges remain narrow with little follow through on moves thus far.

- The recovery came after an early move lower as participants faded yesterday's richening, perhaps using the opportunity to close long positions/add fresh shorts. Several block sellers of TY, 2 clips of 3k, also weighed.

- Flash PMIs from Europe and the UK headline the European session. Further out we have flash S&P Global PMIs, Philly Fed Non-Mfg Index and Richmond Fed Mfg Index. The latest 2-Year Supply is also due.

JGBS: Futures At Session Highs, Curve Twist Flattens

In the Tokyo afternoon session, JGB futures have rebounded to a new intraday high, +27 compared to the settlement levels. The strengthening through to session appeared to reflect both domestic and offshore factors.

- Locally, the BOJ announced an unscheduled bond purchase of ¥300bn worth of 5-to-10-year bonds and ¥100bn of 10-to-25-year JGBs at market prices. After some initial volatility, benchmark yields have moved lower by around 1-2bps across benchmarks.

- There hasn’t been much in the way of domestic data to flag outside of the previously outlined Jibun Bank PMI data. September Department store sales are due later today.

- Assisting the afternoon strengthening in JGBs has been firming in US tsys from session lows. Cash US tsys are 1.5bp cheaper to 1bp richer, with the curve twist-flattening, pivoting on 5s.

- The cash JGB curve has also twist-flattened, pivoting at the 3s, with yields 0.7bp higher to 3.5bps lower. The benchmark 10-year yield is 2.2bps lower at 0.855% versus the cycle high of 0.882% set yesterday.

- The swaps curve has bull-flattened, with rates flat to 2.2bps lower. Swap spreads are wider beyond the 3-year.

- Tomorrow, the local calendar sees Leading and Coincident Indices for August (Final) alongside a Liquidity Enhancement Auction for 15.5-39-year JGBs at 1700 JT.

JAPAN DATA: Services PMI Momentum Cools, Composite PMI Back Under 50.0

Japan's October preliminary PMIs saw softer momentum relative to September. The Jibun Bank manufacturing PMI was unchanged at 48.5. The services print fell back to 51.1 from 53.8 prior. This dragged the composite index back into contractionary territory at 49.9, from 52.1 prior. Note there are no consensus estimates for these prints.

- The detail on the manufacturing side showed output falling to 47.6 from 48.7 prior. New orders rose. For the headline manufacturing PMI, we remain above earlier 2023 lows, but only modestly.

- On the services side, the headline index is back to December 2022 levels. We did see the employment sub-index rise to 52.8 (from 49.1), but the prices sub-index slipped.

AUSSIE BONDS: Richer Ahead Of RBA Gov Bullock’s Speech & Q3 CPI Tomorrow

ACGBs (YM +6.0 & XM +9.5) are richer and at Sydney session highs after US tsys pare early Asia-Pac weakness. With the data docket light today, the direction of the local market has been linked to US tsys dealings in today’s Asia-Pac session ahead of RBA Governor Bullock’s speech tonight at CBA’s annual conference (1900 AEDT) and Q3 CPI tomorrow.

- In the wake of yesterday's abrupt turnaround, which pushed down US tsy yields following the 10-year's surge to a fresh cycle high above the 5% threshold, US tsys have exhibited a twist-flattening in today's Asia-Pacific session. Cash US tsys are dealing 1.5bps cheaper to 1bp richer.

- Cash ACGBs are 6-9bps richer, with the AU-US 10-year yield differential 3bps higher at -16bps.

- Swap rates are 5-9bps lower, with the 3s10s curve flatter.

- The bills strip has bull-flattened, with pricing +1 to +7.

- RBA-dated OIS pricing is 2-5bps softer across ’24 meetings, with terminal rate expectations at 4.32% versus 4.36% yesterday. The market has attached a 38% chance of a 25bp hike at the RBA’s November meeting.

- Tomorrow, the local calendar sees Q3 CPI data, with Bloomberg consensus expecting a cooling in the headline and core CPI measures. The Trimmed Mean measure is forecast to fall to 5.0% y/y from 5.9% in Q2.

AUSTRALIAN DATA: PMI Shows Weak Start To Q4, Selling Price Rises Moderating

The preliminary composite Judo Bank PMI for October returned into contractionary territory falling to 47.3 from 51.5, the lowest since January 2022. The weakness was driven by a cut in output driven by lower new orders and more pessimism re the outlook but employment continued to grow albeit more slowly. Services activity contracted with the index at 47.6 down from 51.8 and manufacturing shrank at a faster pace as the PMI deteriorated to 48 from 48.7.

- Survey respondents noted that higher rates, lower demand and price pressures drove the decline in new domestic business. Export orders also continued to decline.

- Input cost pressures rose to a 3-month high due to fuel and higher wages. While selling price inflation continued to rise, lower pricing power meant that it was at its lowest rate since March 2021.

- Both services and manufacturing sectors increased their work forces but more moderately than seen for most of 2023.

- Businesses remain positive regarding the outlook but less so than they have been with confidence falling to its lowest since the start of the pandemic and is below the series average.

- See Judo Bank PMI report here.

Source: MNI - Market News/Bloomberg

AUSTRALIAN DATA: Q3 CPI Should Moderate Further But Quarterly Rise Still High

Q3 and September CPI data are released on Wednesday and will be a key input into the November RBA decision. Headline is forecast to have eased to 5.3% y/y from 6% in Q2, helped by base effects, but September may have risen slightly to 5.3% (fc: 5-5.8%). The Q3 trimmed mean is also expected to be lower at 5%. RBA watcher McCrann wrote in The Australian that he believes an increase above 1.5% q/q would be needed to get the RBA to hike again.

- A consensus outcome may result in a slight overshoot of the RBA’s implied Q3 expectations but not by enough to mean a revision to Q4 2023. It only projects Q2 and Q4.

- All forecasters surveyed by Bloomberg expect annual CPI inflation eased in Q3 but almost all expect the quarterly rate to be higher than Q2 due to fuel prices. Consensus is at 1.1% q/q and 5.3% after 0.8% and 6% in Q2 with expectations between 0.7% and 1.2% q/q and 5% and 5.7% y/y. ANZ, NAB and Westpac are all at consensus but Westpac is below forecasting 0.9% and 5.1%.

- The trimmed mean should also see a stronger quarterly rise but the annual rate ease further with consensus at 1.0% q/q and 5% y/y with forecasts 0.8-1.3% and 4.7-5.3% after 0.9% and 5.9% in Q2. CBA is in line with consensus but NAB & Westpac expect 1.1% q/q and ANZ +1.2%.

- Sticky core services inflation remains a key RBA concern. Helpful base effects should mean the annual rate moderates for the first time in Q3, as Q3 2022 rose 1.8% q/q. It increased 1.2% q/q and 6.8% y/y in Q2.

- The weight for international travel and accommodation will be increased in Q3 by around 1pp to 2.84%. A full re-weighting will follow in January.

NZGBS: Closed Richer & At Session Bests After Trade Resumed Following Yesterday’s Holiday

NZGBs closed at the session’s best levels, 2-9bps richer, after yesterday’s holiday. With the domestic calendar empty until Friday’s release of ANZ Consumer Confidence data, local participants have been guided by US tsys.

- In the wake of yesterday's abrupt turnaround, which pushed down US tsy yields following the 10-year's surge to a fresh cycle high above the 5% threshold, US tsys have exhibited a twist-flattening in today's Asia-Pacific session. Cash US tsys are dealing 1.5bps cheaper to 1bp richer.

- The NZGB 10-year closed with a mixed performance versus its $-bloc counterparts. The NZ-US and NZ-AU 10-year yields differentials closed 1bp wider and 4bps narrower respectively.

- Swap rates closed 6-9bps lower, with the 2s10s curve flatter and implied swap spreads slightly narrower.

- RBNZ dated OIS pricing closed flat to 2bps softer across meetings, with terminal OCR expectations at 5.61% versus 5.63% yesterday.

- While the local calendar is empty tomorrow, Australia sees Q3 CPI data.

FOREX: USD Pressured In Asia

The greenback has extended Monday's fall in Asia, BBDXY is down ~0.2% and has fallen below its 20-Day EMA. The move lower in the USD was seen alongside US Tsys and regional equities firming from session lows. Bitcoin dealt at the $35k handle for the first time since Sep 2022 which weighed on the USD at the margins.

- The Aussie is the strongest performer in the G-10 space at the margins. AUD/USD is up ~0.4% last printing at $0.6355/60 and is at its highest level since 18 Oct. Resistance is at $0.6393, high from Oct 18. Tomorrow Australia's Q3 CPI is due.

- Kiwi is ~0.2% higher, last printing at $0.5860/65, bulls look to move through the $0.59 handle to target the 20-Day EMA ($0.5907).

- Yen is a touch firmer, USD/JPY is down ~0.1% and has observed narrow ranges thus far today. Technically bulls remain in the drivers seat, resistance is at ¥150.16, high from Oct 3 and bull trigger. Support comes in at ¥149.16, 20-Day EMA.

- Elsewhere in G-10, EUR and GBP are following the broader USD move and are ~0.1% firmer.

- Flash PMIs from the Eurozone and the UK provide the highlight in todays European session.

EQUITIES: Japan Markets Weighed By Earnings, Mixed Trends Elsewhere

Regional equity markets have been mixed in Asia Pac trade so far for Tuesday. Japan markets have been the weakest performers, but there have been pockets of strength elsewhere. US equity futures have been in positive territory, but gains haven't pushed beyond 0.30%. Eminis were last near 4250.50, +0.20% higher for the session. We remain sub the simple 200-day MA (4258) at this stage.

- Japan's Topix is weaker, but sits above session lows. The index last down around 0.65%, with the Nikkei 225 off by a similar amount. Shares in EV supplier Nidec have fallen sharply, after earnings were weaker than expected.

- Hong Kong markets have returned, and hold in negative territory at the break. The HSI is off around 0.65%. We are away from session lows though (near -1.7% loss at one stage). The properties sub index is down nearly 1%. Evergrande fell sharply in early trade, while there remains concern around a Country Garden default.

- The CSI 300 is around flat at the break. The index is up from earlier lows, with property headwinds being offset to some extent by reports of the country's sovereign wealth fund buying ETFs yesterday. SOEs are also reportedly looking at further share buy backs (see this BBG link).

- Elsewhere, the Kospi and Taiex are only down modestly. The ASX 200 is around flat.

- Indonesian stocks have curbed some recent losses, the JCI up 0.80% so far today. Singapore shares are also higher, but other parts of SEA are weaker.

OIL: Crude Moves Higher Watching Middle East & US Economy

Oil prices are off their intraday highs but are still about 0.7% higher during the APAC session after falling around 2% on Monday. Brent has traded above $90 and made a high of $90.60/bbl earlier after prices fell to $90.18. It is currently $90.44. WTI has spent much of the session above $86 rising to a high of $86.30 before falling to $85.82. It is now around $86.04. The USD index is 0.2% lower.

- Developments in the Middle East remain the main driver of oil markets but US economic news also remains important. This week the data focus is on US preliminary October PMIs and core consumption for September.

- Prices are currently in a holding pattern while the prospects of an Israeli ground offensive seem to be in doubt, especially while negotiations to release hostages continue. War risk has been priced into crude but some of that was taken out yesterday as the conflict hasn’t spread outside Israel/Gaza. Iran is the main risk to global oil shipments.

- API data on US crude/product inventories are published later. Last week saw a drawdown of over 4mn barrels.

- In the US, preliminary October PMIs, Philly Fed non-manufacturing and Richmond Fed indices are released. Also ECB President Lagarde speaks, UK labour market data and European preliminary PMIs are out.

GOLD: Slightly Higher In Asia-Pac After Sliding On Monday Despite Lower Yields & USD

Gold is 0.2% higher in the Asia-Pac session, after closing -0.4% at $1972.85 on Monday.

- There was no discernible boost for bullion from a slide in the USD index in the second half of the session and the large intraday rally in US Treasuries. The US 10-year yield traded in a 19bp range, breaching the 5% mark (5.019%) for the first time since 2007, before finishing 6bps lower at 4.85%. The 2-year finished 3bps richer at 5.05%.

- Bloomberg reported Bill Gross had covered short positions, while Pershing Square fund manager/CEO Bill Ackman tweeted he had covered shorts in US tsys in light of "too much risk in the world to remain short." Additionally, Reuters reported asset manager Vanguard is bullish on longer-dated US tsys after this year’s brutal selloff, betting that the Federal Reserve is at the end of its rate hiking cycle and that the economy will slow next year.

- The decline in yields provided support for equities, while oil declined with gold and the USD.

- Geopolitics remained a focus, but the delay to a much-feared Israel ground assault on Gaza provided some stability to the markets as diplomats tried to prevent a wider regional conflict.

- According to MNI’s technicals team, Friday’s high of $1997.2 marks resistance whilst it remains off support at $1945.3 (Oct 19 low).

US-CHINA: US-China Economic Working Group Holds Virtual Meeting, China FM To Travel To US This Week

Headlines have crossed that the US-China Economic Working Group held their first meeting virtually (see this BBG link). The meeting reportedly went for two hours. Both global and domestic economic issues were reportedly discussed. Both sides also reportedly raised issues of concern, although exactly what those areas were wasn't divulged.

- The discussions were described as 'productive and substantive'.

- This meeting comes ahead of China Foreign Minister Wang's trip to the US later this week (Oct 26-28th). This trip is expected to lay the groundwork for a trip to the US in November by China President Xi Jinping.

THAILAND DATA: China Drives Positive Export Growth, Weak To Other Key Markets

The customs trade surplus for September widened significantly more than expected to $2090mn from $360mn due to better-than-predicted export growth and weaker imports. Exports rose 2.1% y/y down from 2.6%, a contraction had been expected, and the Ministry of Commerce expects growth through to year end. Imports fell 8.3% y/y after -12.8% in August.

- Thai annual export growth turned positive in August. September’s second consecutive month of growth was driven by increased demand from China and also food shipments. The Ministry of Commerce said that drought in a number of other countries had increased orders for food grown in Thailand.

- Exports to China rose 14.4% y/y due to fruit, jewellery and computers & parts. China accounts for around 12% of total merchandise shipments, one of the lower shares in Asia, but they were worth a significant 6.9% of GDP in 2022. So, the improving export growth to China is good news for the Thai economy.

- Exports to the US fell 10% y/y, to the EU -9.3% and Japan -5%; they are all top 5 destinations for Thai goods.

Source: MNI - Market News/Refinitiv

ASIA FX: USD/Asia Pairs Down, Amidst Broader USD Pull Back

Most USD/Asia pairs are lower in line with a softer USD against the majors and US yields, which couldn't sustain an earlier bounce. THB and KRW have outperformed. CNH has lagged though. Tomorrow on the data front we just have South Korean consumer confidence early. Note Hong Kong Chief Executive John Lee will also give his annual policy address.

- USD/CNH sits slightly lower in recent dealings, last near 7.3080. Earlier dips to 7.3015/20 found support, while moves above 7.3100 have seen selling interest emerge. Local equities are trying to push higher, amid various supports from SOEs and the country's sovereign wealth fund. However, gains are still modest for the CSI 300. The US-China Economic Working Group held discussions, which comes ahead of the foreign minister's trip to the US later this week.

- Spot USD/HKD has drifted lower through the first part of Tuesday trade. Hong Kong markets have returned, but spot USD/HKD remains well within recent ranges. We last tracked near 7.8215, with the pair sub all key EMAs, with the 200-day back near 7.8300. Still, dips sub 7.8200 haven't proven sustainable in recent weeks. US-HK short term rate differentials have drifted lower, but the 3 mth spread at +18bps is still above late September lows. Note tomorrow Hong Kong Chief Executive John Lee delivers his annual policy address.

- USD/IDR sits comfortably off Monday session highs, but has crept higher as the session has progressed today. The pair was last near 15885/90. Session lows today came in at 15855. Highs in the pair yesterday were at 15962, before BI intervention curbed USD gains. Earlier President Jokowi stated that the impact of the weaker IDR trend is manageable from an inflation standpoint. He added higher US rates and capital outflows are additional risks (per BBG).

- USD/PHP sits slightly lower for the session, last near 56.75, around 0.15% stronger in PHP terms. This is underperforming higher beta plays in the region amid fresh USD softness, but we continue to track recent ranges. Earlier comments from Deputy BSP Governor Dakila struck a familiar tone. The central bank is watching CPI trends, it remains hawkish and won't cut rates until it is confident inflation is back in target (per BBG).

- The baht is sharply stronger in the first part of trade today. The currency is up over 1% against the USD. This puts us back near 36.15, slightly up from session lows for the pair. Whilst part of this reflects catch up to USD weakness (as onshore markets were shut yesterday), trade data has given the currency another lift, via a stronger than expected surplus due to higher export growth. Current USD/THB levels put us back close to October lows in the pair. We are back sub the 20-day EMA (near 36.39), while the 50-day is just under 36.00.

- Markets in India are closed today for the observance of a national holiday. On Monday USD/INR firmed ~0.1% to finish a touch above the 20-Day EMA (83.1871) as higher US Tsy Yields weighed on the Rupee. The data calendar in India is empty this week.

- USD/MYR is pressured today as the greenback is broadly weaker in Asia. The pair has ticked away from yesterday's cycle high of 4.7958 through this morning's session. We sit down ~0.4% at 4.7755/95. Bank Negara Malaysia Governor Ghaffour noted yesterday that the bank intends to ensure that Ringgit moves stay orderly and recent weakening of the currency do not reflect economic fundamentals.

- The SGD NEER (per Goldman Sachs estimates) has ticked higher in early dealing on Tuesday after firming yesterday to its highest level since 12 Oct. The measure sits ~0.5% below the top of the band. USD/SGD has fallen below the 20-Day EMA (1.3678) today as broad based greenback weakness weighs. The pair is ~1% below last weeks highs and last prints at $1.3650/55. Yesterday's September CPI report was mixed, headline CPI was a touch firmer than estimated at 4.1% Y/Y ticking higher from the prior 4.0%. Core CPI nudged lower to 3.0% Y/Y from 3.4%.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/10/2023 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 24/10/2023 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 24/10/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 24/10/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 24/10/2023 | 0730/0930 | ** | | DE | S&P Global Services PMI (p) |

| 24/10/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 24/10/2023 | 0800/1000 |  | EU | ECB Bank Lending Survey (Q3 2023) | |

| 24/10/2023 | 0800/1000 | ** | | EU | S&P Global Services PMI (p) |

| 24/10/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 24/10/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 24/10/2023 | 0830/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 24/10/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 24/10/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 24/10/2023 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 24/10/2023 | 0900/0500 | * |  | US | Business Inventories |

| 24/10/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 24/10/2023 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 24/10/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 24/10/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 24/10/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 24/10/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 24/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 24/10/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.