Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Most regional stock indices & U.S. e-mini futures creep higher as participants assess recovery outlook.

- U.S. Tsy yield curve steepens, unwinding overnight move; ACGBs move away from session lows after local jobs data release.

- Yen goes offered across the board, yuan softens after a weaker than expected PBOC fix.

- Turkish lira prints record lows after Erdogan ousts three CBRT policymakers.

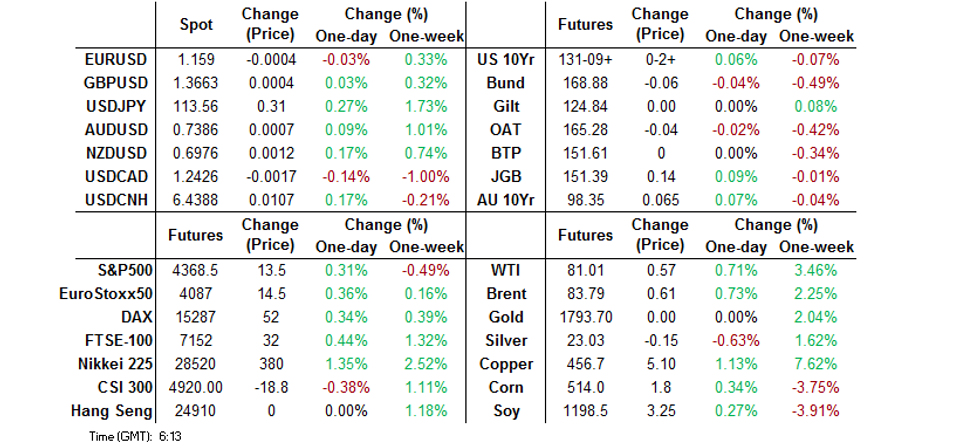

BOND SUMMARY: U.S. Tsy Yield Curve Steepens, ACGBs Bid After Aussie Jobs Report

The initial impetus from Wednesday's eventful NY session gradually dissipated, while further acceleration in China's PPI growth poured fuel on global inflation worries. Australia's labour market report and Japan's 5-Year debt auction provided remaining regional highlights.

- T-Notes meandered within a 0-04 range, struggling for a clear direction. The contract last trades +0-01+ at 131-08+. Cash Tsy curve runs steeper as we type, unwinding some of yesterday's move, with yields sitting -0.5bp to +3.2bp. 30-Year Tsys underperform, despite yesterday's solid offering of that tenor. Eurodollar futures last seen unch. to +2.5 ticks through the reds. U.S. factory-gate inflation and weekly jobless claims take focus on the data front, while there is plenty of Fedspeak coming up today.

- JGB futures edged higher into the Tokyo lunch break but trimmed gains thereafter. The contract changes hands at 151.36, 11 ticks above last settlement. Cash JGB yield curve bull flattened. The MoF auctioned 5-Year JGBs, drawing bid/cover ratio of 3.86x (prev. 4.42x), with low price matching dealer expectations. PM Kishida dissolved parliament, setting the scene for the Oct 31 general election.

- Cash ACGB curve was paring its initial bull flattening, but the release of a net negative Australian jobs market report reversed that trend, inspiring fresh demand for Aussie bonds. The curve still runs flatter, with yields sitting +1.0bp to -7.7bp. Aussie bond futures moved away from lows, YM trades -1.0 & XM +5.5 at typing. Bills run 1-2 ticks through the reds. Australia's employment shrank more than forecast, which was driven exclusively by part-time positions. Unemployment edged higher, but not as much as expected, while participation dipped. Comments from RBA Dep Gov Debelle offered little of note, while the Reserve Bank offered to buy A$1.6bn of ACGBs with maturities of Apr '29 to Nov '32, but excluding ACGB May '32.

FOREX: Yen Resumes Losses, Commodity-Tied FX Outperform

Yen sales resumed after the currency took a breather yesterday. The Nikkei 225 advanced, while upticks in all three main U.S. e-mini futures inspired hope for a continued pick-up in risk appetite. BoJ's Noguchi pointed to a continued need for an aggressive fiscal and monetary stimulus, in another reminder of the Bank's divergence with its major peers. His comments came after FOMC minutes suggested that tapering is in sight.

- The redback went offered after a weaker than expected PBOC fix. China's central bank set their central USD/CNY mid-point at CNY6.4414, 44 pips above sell-side estimate (the largest weak bias since May 10).

- China's factory-gate inflation accelerated to the fastest pace in almost 26 years, overshooting consensus estimate. The report came after U.S. CPI topped expectations, reinforcing broader inflation concerns.

- AUD showed a limited reaction to domestic labour market report, which showed a smaller than expected uptick in the unemployment rate coupled with an above-forecast dip in participation. Employment shrank more than projected, exclusively on the back of losses in part-time jobs.

- Broader commodity-tied FX space was generally firmer, with NZD leading gains. RBNZ Dep Gov Bascand noted that New Zealand's economy recovered strongly from 2020 but the Delta outbreak weighs on outlook. NZD/USD re-tested its monthly highs, while NZD/JPY rose to its best levels since early Jun.

- U.S. weekly jobless claims & PPI take focus on the data front going forward. The global central bank speaker slate is tightly packed with Fed, ECB & BoE members.

FOREX OPTIONS: Expiries for Oct14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1485-00(E691mln), $1.1550-65(E904mln), $1.1600(E1.4bln), $1.1700-20(E999mln)

- EUR/GBP: Gbp0.8510-25(E1.2bln)

- USD/JPY: Y113.00($835mln), Y113.75-90($700mln)

- USD/CAD: C$1.2495($520mln), C$1.2550-60($578mln)

- USD/CNY: Cny6.4500($1.3bln)

ASIA FX: Most EM Currencies Stronger, Yuan Weaker After Fix

- CNH: Offshore yuan weakened, USD/CNH reversing some of the previous day's decline. The PBOC fix was 44 pips above sellside estimates indicating a preference for a weaker yuan, the biggest divergence since May 10 when the delta was 55 pips.

- SGD: Singapore dollar strengthened sharply after the MAS unexpectedly tightened policy, raising the slope of the currency band, the central bank cited risks to financial stability and highlighted inflationary risks.

- TWD: Taiwan dollar is stronger but off session highs. Geopolitics remains a concern, while TSMC earnings are due later today.

- KRW: Won strengthened again for a second day, USD/KRW retreating from the psychological 1200 level. FinMin Hong said late on Wednesday that the government will take market-stabilization steps should there be increased volatility in the foreign exchange market caused by abnormal factors.

- MYR: Ringgit gained, Health Min Khairy said that Malaysia will start distributing Covid-19 booster shots to senior citizens and frontline health workers.

- IDR: Rupiah rose, Indonesia confirmed its readiness to reopen the Bali airport to visitors from 19 selected low-risk countries today, but it is unclear if many travellers will head to the island as long as strict safety measures remain in place.

- PHP: Peso is higher, the Presidential Palace announced that the Philippines is relaxing some restrictions on activity. The national Covid-19 task force authorised lowering the Alert Level in Metro Manila by one notch to Level 3 from Oct 16

- THB: Baht gained, officials are expected to approve further relaxations of existing curbs at the COVID-19 panel today. The BoT said it was ready to use additional policy tools if needed in the latest minutes release.

ASIA RATES: China Futures Rally For Second Day

- INDIA: Yields higher in early trade, building on yesterday's gains. Yields finished higher for the second day yesterday amid constructive risk tone in India where the equity markets finished at record highs and the rupee rose for the first day in four. Inflows into equity markets helped support the rupee, with a lower CPI print earlier in the week assuaging fears of premature tightening from the RBI. Markets look ahead to WPI data today to confirm inflationary pressures receding, wholesale prices are expected to rise 11.15% in September from 11.39% previously. Elsewhere the RBI will auction INR 240bn of government bonds, the auction bought forward a day due to market holiday for Dussehra being observed tomorrow.

- SOUTH KOREA: Futures higher in South Korea, even as equity markets rise and KRW goes bid. The move in the 10-Year takes the contract to with touching distance of the Sep 7/8 high of 123.16. UST's rose on Wednesday, even as the FOMC minutes showed the board considering a taper as early as November, while CPI rose above expectations. In the cash space yields are lower, the 10-Year dropping 1.5bps to 2.387% and reversing its post-BoK rise.

- CHINA: The PBOC drained CNY 90bn of liquidity today, continuing to drain the pre-Golden Week liquidity injection. Repo rates are within recent ranges, the overnight rate down 6.19bps at 2.0881%, 7-day repo rate up 1.27bps at 2.1627%. Futures have risen again higher for a second day after sliding in October. Speculation is abound that an RRR cut could come as soon as October, as does chatter of an MLF injection, both theories have gathered weight by the latest USD/CNH fixing today where the PBOC indicated a preference for a weaker yuan. Futures have ignored PPI data that showed factory places rose at the fastest pace since 1995, and instead are supported by slightly slower CPI and an overnight move higher in US treasuries.

- INDONESIA: Yields lower across the curve, Indonesia confirmed its readiness to reopen the Bali airport to visitors from 19 selected low-risk countries today, but it is unclear if many travellers will head to the island as long as strict safety measures remain in place. Markets look ahead to trade balance data tomorrow, before the BI rate announcement next week.

EQUITIES: Mostly Higher, China Fluctuates

Most equity markets in the region higher, taking a positive lead from the US where equity markets eked out small gains. Hong Kong markets were shut in observance of Chung Yeung Festival. Bourses in Japan lead the way higher with gains of over 1%, in Japan a survey showed that corporates support PM Kishida's additional fiscal stimulus plan with hopes it will be worth at least JPY 10tn. Kishida is expected to formally sign off on dissolution of the House of Representatives today and schedule a general election for Oct 31. Markets in China are slightly lower but off worst levels of the session, data showed CPI slowed slightly while PPI picked up and rose at the fastest pace since 1995. In Australia equity indices gained over 1%, supported by higher commodity prices. E-minis rose, S&P futures broke out of the previous two day's range, markets look ahead to PPI data and speeches from Fed's Bullard and Bostic.

GOLD: Softens

The yellow metal slipped in Asia-Pac trade on Thursday after jumping in the wake of US CPI data. Gold rose from intraday lows of $1758.03 before jumping to highs of $1796.25, last trading down $3.11 at $1789.84. Support now seen at $1781.4/87.4 - High Oct 8 / High Sep 22 and key resistance while next resistance is at $1808.7 - High Sep 14. Markets look ahead to speeches from Fed's Bullard and Bostic after the FOMC minutes yesterday showed that tapering could be on the table as soon as November.

OIL: Stockpile Build Doesn't Concern Crude

Crude futures broadly flat, holding near Wednesday's highs after managing a positive close. Price action has been more reminiscent of consolidation and profit-taking rather than any sea change in sentiment as both oil contracts remain in a bullish trend. Monday's gains confirmed an extension of the current bullish price sequence of higher highs and higher lows, reinforcing the uptrend. Note that the $80.00 psychological hurdle has also been cleared. The focus is on $82.89, a Fibonacci projection. Concerns among global policy markets over the current high price of oil and energy continues to be reflected in headline newsflow, with an MNI report showing the Bank of Japan's concerns over both high energy prices and high import costs as working against corporate profits. This sentiment was reflected in Reuters reports citing sources as saying the White House is conversing with US oil and gas producers on how the industry can help bring down prices.

- Further evidence of the global shortage of energy supplies arose just after the London close, as the Moldovan Deputy PM formally issued a state of emergency in the domestic energy sector thanks to the natural gas shortage in the country. Elsewhere API inventory data showed US crude stocks rose 5.21m bbls, while Cushing hub saw stocks fall 2.28m bbls and downstream products also saw draws. Markets look ahead to the delayed US DOE inventory figures.

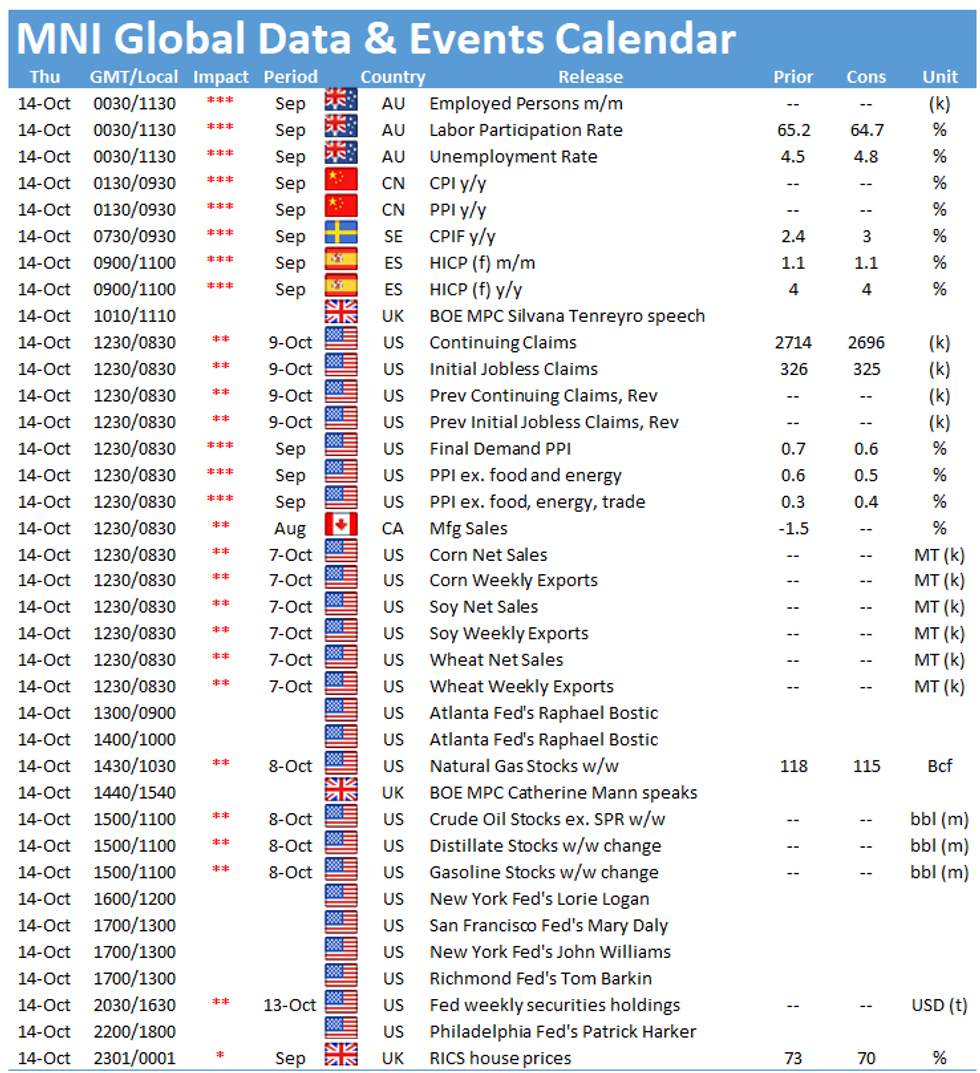

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.