Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

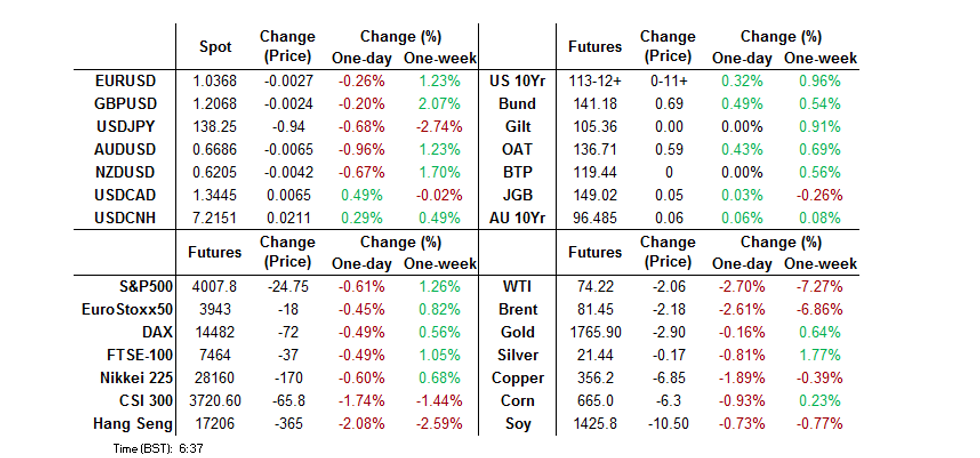

- Tsys were pretty much bid from the off in Asia-Pac dealing, with reports of pockets of COVID-related social unrest across some of the major Chinese cities and a continued uptick in new daily COVID cases in China dominating news flow. That weighed on e-minis, as well & HK & Chinese equities, providing a further leg of support for Tsys, via cross-market flows.

- JPY outperformed amongst G10 FX against this backdrop, while the Antipodeans found themselves at the other end of the perfromance table.

- Looking ahead, headline flow surrounding the proposed price cap on Russian crude oil will garner attention. Meanwhile, the Dallas Fed m’fing index headlines a limited global economic docket on Monday, with comments from a raft of ECB speakers, headlined by President Lagarde, as well as Fedspeak from Williams & Bullard, also slated.

US TSYS: On The Front Foot In Asia

Tsys were pretty much bid from the off in Asia-Pac dealing, with reports of pockets of COVID-related social unrest across some of the major Chinese cities and a continued uptick in new daily COVID cases in China dominating news flow. That weighed on e-minis, as well & HK & Chinese equities, providing a further leg of support for Tsys, via cross-market flows. Weakness in crude oil futures further built on the cross-market support for Tsys.

- TYZ2 deals just off the top of its 0-13+ range into London hours, +0-14 at 113-15, on volume of ~157K (although 63K of that is roll related), while cash Tsys run 3-4bp richer across the curve.

- Overnight flow was headlined by a block seller of TU futures (-4,850).

- Looking ahead, news surrounding the ongoing EU negotiations re: the proposed Russian oil price cap will generate attention on Monday, while the NY docket is headlined by the Dallas Fed m’fing activity index and Fedspeak from NY Fed President Williams & St. Louis Fed President Bullard.

JGBS: Cash Little Changed, Futures Unwind Overnight Losses

JGBs stuck to narrow ranges in Monday trade, essentially operating at near enough unchanged levels for most of the session, as the broader risk-off impulse and press reports surrounding initial government spending proposals for its defence plans offset.

- That allowed JGB futures to unwind their overnight losses and a little bit more, with the contract +4 into the bell. Elsewhere, cash JGBs deal either side of unchanged, and sit within 1bp of Friday’s closing levels.

- Note that the offer/cover ratios for the BoJ Rinban operations spanning 3- to 25+-Year JGBs were average to below average, which may have provided a source of incremental support in the afternoon.

- Comments from Japanese PM Kishida & BoJ Governor Kuroda failed to move the needle.

- Looking ahead, Tuesday’s local docket is headlined by the latest monthly labour market report and 2-Year JGB supply.

AUSSIE BONDS: Early Losses More Than Unwound On Soft Data & Chinese COVID Matters

The overnight cheapening in Aussie Bond futures more than reversed as the session wore on, with the previously covered COVID situation in China (another round of record daily news cases and pockets of social unrest showing up across some of the major Chinese cities) coupling with soft local data (a surprise fall in retail sales) to provide the bid in the space.

- That left YM +7.0 & XM +6.0 at the bell, with 3-7bp of richening witnessed across the major cash ACGB benchmarks, as the curve bull steepened.

- Parliamentary comments from RBA Governor Lowe failed to move the needle, with familiar lines of questioning and answers provided.

- Elsewhere, we note that Anna Hughes, the Deputy Under Treasury for South Australia, was appointed as the new head of the Australian Office of Financial Management (AOFM).

- Bills were 4-9bp richer through the reds, bull flattening, more once again more than reversing early losses. RBA dated OIS eased a touch on the session, but the major metrics stuck within the recently observed ranges.

- Tomorrow’s thin local docket will be headlined by the weekly ANZ-Roy Morgan consumer confidence index.

NZGBS: Flatter To Start The Week, China COVID Matters Headline

The COVID situation in China, including the pockets of unrest related to COVID restrictions witnessed over the weekend, provided a bid for NZGBs on Monday, leaving the major cash NGZB benchmarks 7-10bp richer come the bell, with some bull flattening in play.

- Swap rates generally tracked the move across the curve, resulting in little net movement in swap spreads on the session.

- RBNZ dated OIS eased a touch on the session, owing to the above dynamics. That leaves RBNZ dated OIS pricing just under 70bp of tightening for the Feb ’23 meeting, with a terminal OCR of just over 5.40% priced.

- RBNZ Assistant Governor Silk gave a couple of interviews, as she reiterated the Bank’s surprise at persistently strong inflation, while highlighting the lagged impact of monetary policy, alongside the benefits that a stronger NZD would bring in the current inflationary backdrop. The remainder of her comments largely went over the Bank’s latest round of economic projections.

- The local economic docket is empty on Tuesday.

FOREX: JPY Outperforms On China COVID Dynamic, Antipodeans Struggle

A continued uptick in the daily count of new Chinese COVID cases, which hit another record high, as well as pockets of social unrest related to COVID restriction across some of the major Chinese cities dominated Asia-Pac dealing, with equities trading lower and U.S. Tsys bid.

- This left the JPY atop the G10 FX pile, with USD/JPY operating 80 pips or so lower on the day as we move towards London hours. USD/JPY sits at Y138.40, with bears focused on the bear trigger located at the Nov 15 low (Y137.68).

- The USD outperformed the remainder of its G10 FX peers, with the Antipodeans struggling owing to links to China and their high beta status, while the softer than expected AUD retail sales data added a local source of pressure for the Aussie.

- Elsewhere, USD/CNH gapped higher, but staged a pretty impressive pullback from session highs of circa CNH7.2600, even as Chinese & HK equities struggled, as the previously flagged COVID-related matters in China dominated news flow. The rate last deals a touch above CNH7.2200, with the major HK & Chinese equities also operating off of lows.

- Looking ahead, headline flow surrounding the proposed price cap on Russian crude oil will garner attention. Meanwhile, the Dallas Fed m’fing index headlines a limited global economic docket on Monday, with comments from a raft of ECB speakers, headlined by President Lagarde, as well as Fedspeak from Williams & Bullard, also slated.

FOREX OPTIONS: Expiries for Nov28 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9990-00(E1.1bln), $1.0075-80(E1.1bln), $1.0250(E1.9bln), $1.0300(E737mln), $1.0390-10(E1.2bln), $1.0425-50(E1.4bln), $1.0800(E1.4bln)

- USD/JPY: Y135.80-00($1.8bln), Y138.30-50($1.2bln)

- EUR/JPY: Y145.95(E628mln)

- GBP/USD: $1.1700(Gbp873mln), $1.2100(Gbp971mln)

- AUD/USD: $0.6700-15(A$1.0bln)

- USD/CNY: Cny7.1500($755mln), Cny7.2000($863mln), Cny7.2500($624mln), Cny7.3000($1.5bln)

EQUITIES: On The Defensive

The previously alluded to uptick in new daily Chinese COVID cases, as well as reports pointing to pockets of social unrest re: COVID restrictions across some of the major Chinese cities, weighed on risk sentiment in Asia-Pac hours. There was little to really counter the move, with the Hang Seng leading the major regional equity indices lower, trading just over 2% softer on the session, albeit off of session lows. E-minis are also off of worst levels, but the 3 major contracts are still 0.5-0.9% lower on the day, with the S&P 500 future making a brief showing below 4,000.

GOLD: Prices Down As USD Strengthens On China Unrest

Gold prices are down about 0.3% to around $1750/oz as the USD has risen 0.4% on the back of Covid-related unrest in China. They are off the day’s low of $1746.13. Bullion reached a high early in today’s session at $1754.11.

- Gold prices continue to range trade within its support level of $1726.40, the 20-day EMA, and resistance level of $1768.50, the November 15 high and bull trigger. It has been trading between $1700 and $1800 since November 10.

- There is very little scheduled for later. NY Fed’s Williams speaks, which will be important for gold, especially if his comments are on the dovish side. Developments in China will continue to be important for their impact on the dollar. The main focus of the week will be US payrolls on Friday, where further labour market slowing would support bullion.

OIL: Prices Continue To Move Lower On Uncertain Global Outlook

Oil prices ended last week down and they are lower again in today’s trading as the USD strengthened as protests in China over harsh Covid restrictions dampened the global growth outlook.

- WTI is trading down 2.9% close to its intraday low at $74.05/bbl and has broken through its medium-term key support of $74.96. It reached a high of $76.50 early in the session. It is now well below its 10-, 20- and 50-day moving averages. Brent is 2.8% lower at around $81.25/bbl after an earlier high of $83.93.

- Oil demand has been hit significantly by restrictions in China limiting the movement of people, which may be broadened. Given this backdrop, OPEC+ may cut output even more at its next meeting on December 4 or early in 2023.

- Asia continues to buy Russian oil and at a significant discount of over $33/bbl to Brent. (ANZ)

- There is very little scheduled for later. NY Fed’s Williams speaks, which will be important for the USD, especially if his comments are on the dovish side. Developments in China will continue to be important for their impact on the dollar. The main focus of the week will be US payrolls on Friday.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/11/2022 | 0900/1000 | ** |  | EU | M3 |

| 28/11/2022 | 1100/1100 | ** |  | UK | CBI Distributive Trades |

| 28/11/2022 | 1330/0830 | * |  | CA | Current account |

| 28/11/2022 | 1400/1500 | | EU | ECB Lagarde Intro at ECON Hearing | |

| 28/11/2022 | 1530/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 28/11/2022 | 1530/1530 | | UK | DMO Q1 Consultation Meetings | |

| 28/11/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 28/11/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 28/11/2022 | 1700/1200 | | US | New York Fed's John Williams | |

| 29/11/2022 | 2350/0850 | * |  | JP | Retail sales (p) |

| 29/11/2022 | 2350/0850 | * | | JP | labor force survey |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.