Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

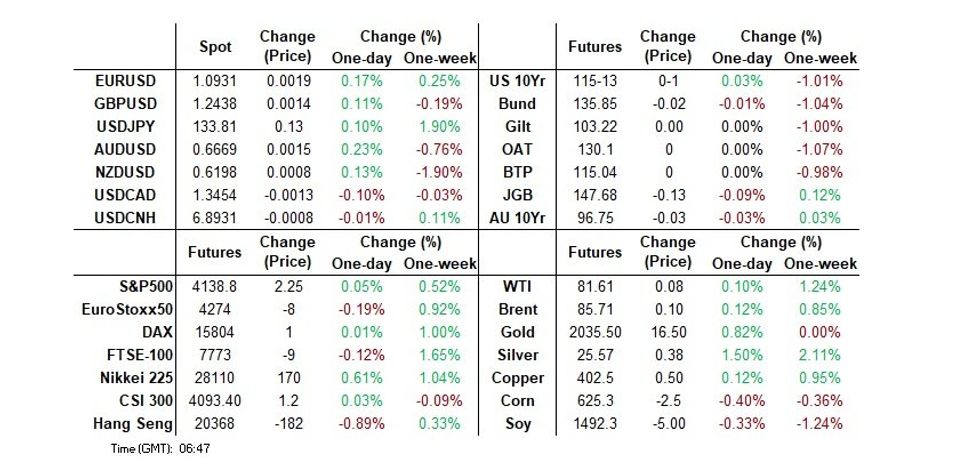

- Cash Tsys sit flat to 1bp cheaper across the major benchmarks after holding narrow ranges overnight.

- USD/JPY briefly dealt above ¥134, printing at the highest level since mid-March. Elsewhere in G10 FX, ranges have been narrow.

- The U.S. CPI print is the highlight of today's session. We also have the minutes from the March FOMC meeting, as well as the latest monetary policy decision from the Bank of Canada.

MNI US CPI Preview: Core CPI Seen Holding Stubbornly High

EXECUTIVE SUMMARY

- Core CPI inflation is widely seen printing its fourth consecutive 0.4% handle after February’s 0.45% M/M.

- Monthly core CPI should be lifted by a large decline for used car prices dropping out whilst there is broader uncertainty for airfares after prior surprising strength.

- Core goods prices beyond used cars could offer some renewed disinflationary pressure after a recent improvement in supply chain pressures, but we suspect any continued stickiness in non-housing core services will dictate the market reaction ahead of the May FOMC, with an 18bp hike currently priced.

- PLEASE FIND THE FULL REPORT HERE:USCPIPrevApr2023.pdf

Prior Inflation Developments

US TSYS: Marginally Cheaper In Asia, CPI In View

TYM3 deals at 115-13+, +0-01+, a narrow 0-03 range has been observed in Asia on volume of ~41k.

- Cash tsys sit flat to 1bp cheaper across the major benchmarks.

- Tsys have dealt in narrow ranges with little follow through on moves in the Asian session as Asia-Pac participants remain focused on today's CPI print.

- Some light cheapening was observed as the USD came off session lows, which held through the latter half of the session.

- Fedspeak from Philadelphia Fed President Harker crossed early in the session, he noted that he is watching data to see if more action is needed on inflation.

- Minneapolis Fed President Kashkari also crossed in Asia, he noted that he does not see the build up of the kind of risks that took down SVB building up across the wider banking sector. He also noted that he sees inflation at middle 3% by the end of this year and closer to 2% next year.

- Today's CPI print, our preview is here, is the highlight of today's session. We also have the minutes from the March FOMC meeting, matters north of the border will be in focus as the Bank of Canada delivers their latest monetary policy decision.

- Fedspeak from Richmond Fed President Barkin and SF Fed President Daly will cross. We also have the latest 10-Year Supply.

EUROZONE: Recession Risk Remains Highest For H1 2023, Unlikely In H2

Despite the banking turmoil in March, which also reached Europe through Credit Suisse, the probability of a recession in 6-months time remained low and well below the benchmark 50%. Given that the estimates were above 50% through H2 2022, the biggest risk of a euro area recession remains in H1 of this year. The IMF doesn’t expect in its April projections that the euro area as a whole will fall into recession but is forecasting negative growth in Germany.

- Our March estimate assumes that annual M3 growth in March remained steady at February’s 2.9% and that the number of unemployed continued to ease at -2.2% y/y.

- The equation from 1985 indicates a 27.5% probability of a recession in September, which was up slightly from February’s 18.7%. This is down from our preliminary estimate at the time of the CS troubles, as markets stabilised following central bank intervention and the announcement that UBS would buy CS.

- The 1998-estimation shows a 30.6% recession probability, down from February’s 43.8%. The downward trend in the 6-month change in the number of unemployed has been putting downward pressure on the recession estimate.

- Econometric estimates are only estimates and not projections.

Source: MNI - Market News/Refinitiv

JGBS: Weakness In Futures Results In Humped Yield Move

JGB futures show just below late morning levels as we head towards the bell, last -20, after recovering from their early Tokyo base and then meandering through the session (initial cheapening was largely driven by spill over from weakness in wider core global FI on Tuesday).

- The wider cash JGB pattern observed in morning trade continues to hold (light cheapening in 7s & 10s owing to futures vs. some richening elsewhere, with super-long paper outperforming).

- Swap rates are flat to ~1.5bp higher, with the 7- to 10-Year zone seeing the biggest move, while super-long swap rates pulled back from early highs on the aforementioned richening in the corresponding JGBs. Swap spreads are wider across the curve and have been all day.

- A Nikkei interview with an MUFG executive revealed a downtick in the average duration of the firm’s JGB holdings, while he suggested that he would only have any real willingness to add to longs in the 10-Year zone of the curve when 10s reached 0.8% or above in yield terms.

- Money stock & weekly international security flow data headline the domestic data docket tomorrow, with the latest liquidity enhancement auction covering off-the-rum 15.5- to 39-Year JGBs also due.

MACRO: Sticky Core Inflation Could Result In Rates Higher For Longer

The IMF revised up its global inflation forecasts in its April report to 7% in 2023 and 4.9% in 2024 from 6.6% and 4.3% respectively. The upward revision was predominantly driven by the developing world. The IMF warned that drivers of inflation could persist until 2025 with core inflation particularly sticky, thus resulting in rates being held higher for longer.

- G20 CPI inflation eased to 8% in February from 8.4%. The Federal Reserve of NY’s global supply chain pressure index fell in March to -1.06, the lowest since the end of 2008, indicating that there is likely to be a further moderation in inflation over the coming months. Despite this, there is concern regarding core price pressures.

- While OECD inflation eased to 8.8% in February from 9.2%, core was steady at around 7.25%, signalling sticky underlying inflation pressures. Thus, further monetary tightening is expected in many economies and talk of easing is premature. US March CPI is released later today and while headline is expected to ease to 5.1% from 6%, core is forecast to rise 0.1pp to 5.6% (see U.S. CPI Preview: April 2023).

- Most of Asia have reported CPI data for March and while inflation in non-Japan Asia including and excluding China has seen a moderation of around 0.3pp to 2.8% and 5.3% respectively, underlying inflation is looking more stubborn at 1.6% and 3.9%. But Asian inflation remains well below that of the OECD and so less monetary tightening has been required. (See Headline CPI Easing But Core Looks Sticky In Some Countries.)

Source: MNI - Market News/Refinitiv

Fig.2 : G20 CPI y/y% vs NY Fed global supply chain pressures 3mma

Source: MNI - Market News/Refinitiv

AUSSIE BONDS: At Session Cheaps, Narrow Range for US Tsys

ACGBs sit at session cheaps (YM -4.0 & XM -4.0) with US Tsys little changed in a narrow range ahead of US CPI data and FOMC Minutes later today. There has been little meaningful macro news flow in today’s Asian session.

- With the local calendar light today, the highlight is likely to be RBA Deputy Governor Bullock's appearance on the WEAI Monetary Panel, which has just commenced. So far across the wires, Bullock has stated that the RBA doesn’t use rates to dial up or down financial stability and that the RBA had underestimated fiscal-monetary power during the pandemic. There hadn't been any market reaction to her comments at the time of writing.

- Cash ACGBs are 3-4bp cheaper with the curve 1bp flatter and the AU-US 10-year yield differential +1bp at -17bp.

- Swap rates are 6bp higher with EFPs 2bp wider.

- Bills strip pricing is -6 to -10 with early whites the weakest.

- RBA dated OIS pricing firms 4-8bp for meetings beyond June. A 25% chance of a 25bp hike in May is priced with year-end easing expectations at 17bp versus 29bp ahead of the Easter holiday.

- The market’s focus now shifts to the release of US CPI and FOMC Minutes later today.

NZGBS: Twist Steepen Ahead of NZGB Supply Tomorrow

NZGB cash curve twist steepens, with the 2-year benchmark 1bp richer and the 10-year benchmark 4bp cheaper at the close. This movement was linked to the weekly supply announcement from the NZ Treasury. Implied long-end swap spread narrowed with swap rates 1-2bp lower at the close.

- The NZ Treasury plans to sell NZ$200mn of the May-28 bond, NZ$150mn of the Apr-33 bond and NZ$50mn of the May-51 bond tomorrow.

- The NZGB auctions on April 6th also resulted in a steepening of the curve, with stronger demand seen for short-end supply, likely due to concerns of over-tightening by the RBNZ.

- Today's price action may also have been influenced by RBNZ's recent decision statement, which expressed concerns about the inflation risks associated with fiscal spending financed through borrowing, as opposed to re-prioritisation or spending deferrals.

- RBNZ dated OIS pricing is flat to 4bp firmer across meetings with 20bp of tightening priced for May.

- With Total Card Spending in March (+3.1% M/M, 16.1% Y/Y) suggesting very little deceleration in retail sales values in Q1, the RBNZ is unlikely to find any comfort in today’s data.

- The market’s focus now shifts to the release of US CPI and FOMC Minutes later today.

NZ SWAPS: 1y Vs. 1y1y Flattens To GFC Levels

Last week's surprise 50bp rate hike by the RBNZ has resulted in a flattening of the 1-year swap Vs. 1-year swap rate 1 year forward (1y1y) to levels not seen since the Global Financial Crisis (GFC).

- As noted previously with respect to AU swaps, 1y Vs. 1y1y typically flattens until the last rate hike of the cycle. Soft economic data reinforces the flattening trend, as investors become concerned about the risk of overtightening and the potential for a recession.

- The market seems to be taking last week’s hawkish message from the RBNZ seriously, given the central bank's track record of overshooting OIS forward pricing.

- With the market attaching an 80% chance of a 25bp hike at the May meeting, there are few signs that investors are considering fading post-RBNZ pricing.

Fig. 1: RBNZ OCR (%) Vs. 1y Vs. 1y1y (%)

Source: Bloomberg / MNI - Market News

FOREX: USD/JPY Briefly Tops ¥134 In Otherwise Muted Asian Session

USD/JPY briefly dealt above ¥134 in the Asian session, printing the pairs highest level since mid March. Elsewhere in G-10 ranges have been narrow with little follow through on moves.

- Yesterday's uptick in Oil prices and modest pro-USD gyrations in the U.S./Japan 2- & 10-Year yield spreads have also supported the cross. The breach of Monday's high in USD/JPY has opened ¥134.75, 61.8% retracement of the Mar 8-24 bear leg, for bulls. March PPI printed in line with expectations at 0.0% M/M whilst the Y/Y measure was a touch above estimates at 7.2%.

- AUD is the strongest performer in the G10 space at the margins. AUD/USD is up ~0.2% last printing at $0.6665/70. The next target for bulls is $0.6697, the 20-Day EMA.

- Kiwi is a touch firmer however NZD/USD has observed narrow ranges with $0.62 capping rallies and support seen below $0.6180.

- Cross asset wise; BBDXY is little changed as are e-minis. 2 Year US Treasury Yields are ~1bp firmer.

- Today's US CPI print, our preview is here, is the highlight of today's session. We also have the minutes from the March FOMC meeting, as well as the latest monetary policy decision from the Bank of Canada.

MNI BOC Preview, Apr'23: No Need To Change Guidance Yet

EXECUTIVE SUMMARY

- The BoC is unanimously expected to keep rates on hold at 4.5% on Wednesday and for the most part echo March’s continued guidance of a conditional pause whilst leaving the door open to further hikes to prevent an excessively large easing in financial conditions.

- The macro backdrop isn’t sufficiently different to warrant a change in guidance, although new forecasts could be used as a hawkish nuance if wanted, especially on the growth side. It’s not a base case but we don’t rule out a tweak higher in the annual neutral rate revision.

- Governor Macklem will follow the day’s proceedings with a fire side chat at the IMF on Apr 13, 0900ET.

- PLEASE FIND THE FULL REPORT HERE: BOCPreviewApr2023.pdf

FX OPTIONS: Expiries for Apr12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0900-10(E2.7bln), $1.0940-50(E640mln)

- USD/JPY: Y132.00($732mln), Y132.15-25($863mln), Y134.10-15($1.1bln)

- GBP/USD: $1.2300(Gbp692mln)

- EUR/GBP: Gbp0.8755-70(E480mln), Gbp0.8795-10(E595mln)

- AUD/USD: $0.6700(A$545mln), $0.6750(A$1.2bln)

- USD/CAD: C$1.3800($582mln)

GOLD: Bullion Stronger Again Today, Waiting For US CPI & FOMC Minutes

Gold prices are higher again during the APAC session today ahead of US CPI data. Bullion is 0.7% higher to around $2017.65/oz after rising 0.6% on Tuesday on the back of a weaker dollar. The USD index has been range trading on Wednesday.

- Gold has been trending higher since the banking turmoil in the US began. It is currently trading close to its intraday high of $2019.42 and is heading towards resistance at $2032.10, the April 5 high, but is still some way off it. On Tuesday the high was $2009.52.

- The focus later today is on US CPI data for March, as markets look for direction on the Fed. While the headline is expected to ease to 5.1% from 6%, core is forecast to rise 0.1pp to 5.6% (see U.S. CPI Preview: April 2023). In terms of the Fed, the FOMC minutes for March 22 are published and there are also a number of speakers including Kashkari, Barkin and Daly.

OIL: Crude Close To Tuesday’s Highs Ahead of US CPI Data

During APAC trading today crude is holding onto Tuesday’s gains ahead of the release of the US CPI later, but it is in a narrow range. Both Brent and WTI have been moving sideways after rising around 2% and are currently around $85.62/bbl and $81.51 respectively. They are close to intraday highs, which are slightly above Tuesday’s highs.

- Bloomberg tanker tracking data showed that Russian output is finally softening with shipments below 3mbd. Also on the supply-side, pipeline flows from Iraqi Kurdistan remain stalled.

- Futures contract spreads are showing that the oil market is tightening following OPEC’s output cut decision.

- The EIA releases official US inventory data on Wednesday. On Tuesday the API reported a 400k build in crude stocks in the latest week and 500k in gasoline but a 2mn drawdown in distillate, according to Bloomberg from people familiar with the data.

- The focus later today is on US CPI data for March, as markets look for direction on the Fed. While the headline is expected to ease to 5.1% from 6%, core is forecast to rise 0.1pp to 5.6% (see U.S. CPI Preview: April 2023). In terms of the Fed, the FOMC minutes for March 22 are published and there are also a number of speakers including Kashkari, Barkin and Daly. The BoC also meets.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/04/2023 | 0600/0800 | ** |  | NO | Norway GDP |

| 12/04/2023 | 0900/1000 | * |  | UK | Index Linked Gilt Outright Auction Result |

| 12/04/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 12/04/2023 | - |  | EU | ECB Lagarde and Panetta in IMF/World Bank, G20 Finance Ministers' Meetings | |

| 12/04/2023 | 1230/0830 | *** | | US | CPI |

| 12/04/2023 | 1230/1430 | | EU | ECB de Guindos at Asociacion para el Progreso de Direccion Event | |

| 12/04/2023 | 1300/1400 | | UK | BOE Bailey Remarks at Institute of International Finance | |

| 12/04/2023 | 1300/0900 | | US | Richmond Fed's Tom Barkin | |

| 12/04/2023 | 1400/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 12/04/2023 | 1400/1000 | | CA | Bank of Canada Monetary Policy Report | |

| 12/04/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 12/04/2023 | 1500/1100 | | CA | Bank of Canada Governor press conference | |

| 12/04/2023 | 1600/1200 | | US | San Francisco Fed's Mary Daly | |

| 12/04/2023 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 12/04/2023 | 1800/1400 | ** | | US | Treasury Budget |

| 12/04/2023 | 1800/1400 | * | | US | FOMC Statement |

| 12/04/2023 | 1915/2015 | | UK | BOE Bailey Speaks at IMF Governor Talks |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.