Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

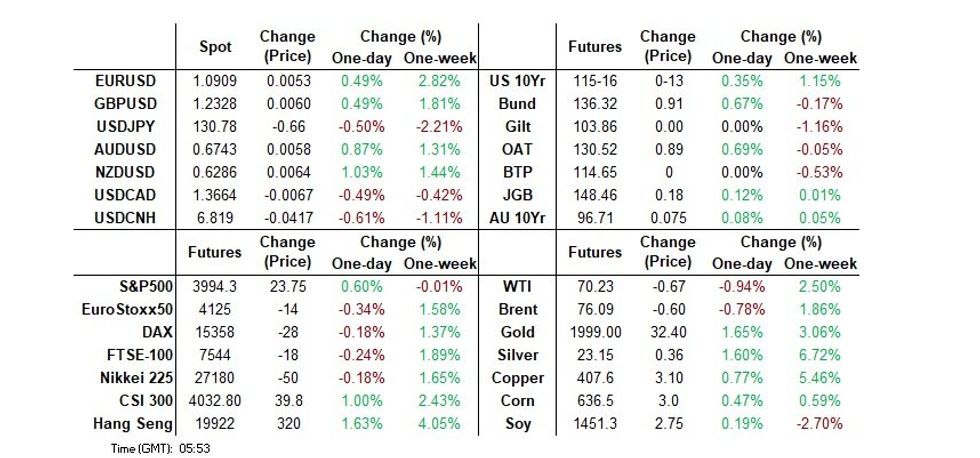

- The greenback is pressured in Asia, as Asia-Pac participants looked to the dovish elements of Wednesday’s post-FOMC statement and Chair Powell’s communique. BBDXY breached lows seen in the aftermath of the FOMC rate decision, and now sits a touch off its lowest level since 14 Feb.

- 2-Year Tsy yields moved through their post-FOMC trough, along with a similar move in year-end FOMC-dated OIS, which triggered a fresh flurry of demand for Tsys.

- In Europe today we have SNB, Norges Bank and BOE monetary policy decisions. Further out U.S. New Home Sales, Initial Jobless Claims and Fedspeak from St Louis Fed President Bullard will cross.

MNI BOE Preview - Mar 2023: Feb CPI to Determine Hike or Hold

- The MNI Markets team expects 3 members of the MPC to vote for unchanged rates, 3 members to vote for a 25bp hike and 3 members to determine their vote based on the outcome of the February inflation data (which the MPC received on Friday morning). In our view, it is not necessarily the headline data but services inflation that will determine the votes of Bailey, Broadbent and Pill.

- If services inflation was to show another notable deceleration in the February data, we would expect to see rates left on hold this week. However, if the January slowdown in services inflation was to be reversed, the MNI Markets team thinks these members would vote for a 25bp hike. This will tip the balance of the MPC into either a hold or a hike.

- For the full document, including summaries of over 20 sell-side previews see:MNI BoE Preview - Mar23.pdf

MNI SNB Preview - March 2023: Bank Liquidity Provision Should Clear Path for More Hikes

EXECUTIVE SUMMARY

- Bank seen raising rates by 50bps, reinstating the Eurozone-Swiss rate differential

- Sluggish return to inflation target seen persisting, justifying extra tightening

- Global banking turmoil should curtail impulse to hike 75bps, despite high CPI

- Full preview, including summary of sell-side views here: MNISNBPrevMar23.pdf

MNI Norges Bank Preview - March 2023: 25bps Base Case, Further Tightening Hints Likely

EXECUTIVE SUMMARY

- Bank expected to raise rates by 25bps, inline with the guidance handed down in January

- Fresh path projections likely to point to higher peak rate in Q3

- Global banking turmoil should curtail impulse to hike 50bps, despite high CPI

- Full preview including summary of sell-side views here: MNINBPrevMar23.pdf

Fig. 1: Q1 inflation topped the Bank’s Dec forecast

US TSYS: Curve Steepens In Asia

TYM3 deals at 115-17, +0-14, 0-01 off the top of the contract’s 0-11 range on volume of ~112K.

- Cash Tsys sit 6bps richer to 2bps cheaper across the major benchmarks. The curve has twist steepened, pivoting around 10s.

- Asia-Pac participants initially faded the move seen in the aftermath of the latest Fed decision, perhaps using the opportunity to close out long positions.

- A bid in e-minis and pressure on the USD saw Tsys recover off session lows, before a break in 2-Year yields, through their post-FOMC trough, along with a similar move in year-end FOMC-dated OIS, triggered a fresh flurry of demand.

- Asia-Pac participants generally looked to the dovish elements of Wednesday’s post-FOMC statement and Chair Powell’s communique.

- Flow was headlined by a TU/UXY block steepener (DV01 ~$150K).

- Fed-dated OIS now prices ~10bps of tightening at the May FOMC meeting, with a terminal rate of ~4.90% observed. There are ~80bps of cuts priced for 2023.

- In Europe today we have SNB, Norges Bank and BOE monetary policy decisions. Further out New Home Sales, Initial Jobless Claims and Fedspeak from St Louis Fed President Bullard will cross, as will 10-Year TIPS supply.

JGBS: Futures Give Back Chunk Of Overnight Gains, Curve Twist Steepens

The early afternoon session impulse from the bid in U.S. Tsys subsided as U.S. fixed income consolidated a little off richest levels of the day, allowing JGB futures to drift lower, printing fresh Tokyo session lows in the process, before regaining some poise into the bell.

- That left the contract +20 ahead of the close, paring around half of the FOMC-inspired overnight session gains. The wider JGB curve has twist steepened, with the 7- to 10-Year zone outperforming on the move in futures since yesterday’s settlement, while 40s are the only major benchmark to sit cheaper on the day, as the major cash JGBs run 3bp richer to 1bp cheaper.

- Swap rates have also ticked away from session lows, in sympathy with the moves in JGB yields. Swap spreads are mixed across the curve.

- Local headline flow was essentially non-existent.

- The latest liquidity enhancement auction covering off-the-run 5- to 15.5-Year JGBs saw spreads print comfortably through prevailing market levels, although the cover ratio moderated a touch. This suggests that those that needed access to the line (maybe with short covering requirements) were willing to “pay up” to guarantee their access, while the recent richening left other prospective bidders on the sidelines.

- Looking ahead, national CPI and flash Jibun Bank PMI data will cross on Friday.

AUSSIE BONDS: Stronger But Well Off Post-FOMC Bests

ACGBs closed richer (YM +8.0 & XM +7.5) but off session extremes as the U.S. Tsy curve twist steepened in Asia-Pac trade following the FOMC policy decision. At the Sydney close, the 2-year U.S. Tsy yield was 6bp lower and the 10-year 1bp higher. Cash ACGBs closed 8bp richer on the day with the 3/10 curve unchanged and the AU/US 10-year yield differential is +7bp at -15bp.

- Swaps closed 9-10bp stronger but similarly off Asia-Pac session extremes with the 3s10s curve unchanged and EFPs 1-2bp tighter.

- Bills strip flattened with pricing flat to +14.

- RBA dated OIS closed flat to 2bp firmer for meetings out to September and 3-7bp softer beyond. April meeting pricing firmed to an 11% chance of a 25bp hike. Year-end easing expectations closed at 26bp versus 34bp earlier in the session.

- The local calendar is light until next week when February retail sales (Tue) and monthly CPI (Wed) are scheduled for release. These two releases were highlighted in the RBA Minutes as important inputs to the April policy decision.

- Until then, the market will continue to track U.S. Tsys in the wake of yesterday's FOMC decision. The U.S. calendar is light today with U.S. Home Sales and Claims data as the highlights.

NZGBS: 10-Year NZGB Off Bests As U.S. Tsys Twist Steepen In Asia-Pac

NZGBs closed 4-11bp stronger on the day but well off bests as U.S. Tsys twist steepen in Asia-Pac trade. 2/10 cash curve bull steepened 6bp with the 10-year benchmark closing 5bp off best levels. The 2-year benchmark closed at yield lows. NZGBS underperformed U.S Tsys with the 10-year yield differential closing +8bp. NZ/AU 10-year yield differential closed unchanged suggesting ACGB weakness contributed to NZGBs underperformance versus U.S. Tsys today.

- Swaps richen 3-10bp, implying wider swap spreads, with the 2s10s curve 7bp steeper.

- In a speech today RBNZ Chief Economist Conway sounded the usual hawkish rhetoric but acknowledged that the OCR was near the peak and comfortably above neutral with the full contractionary effects yet to be felt.

- Little response from RBNZ dated OIS however which softened 2-7bp for meetings beyond April with terminal OCR expectations at 5.19%. April meeting pricing closed with 23bp of tightening.

- The Antipodean calendar is light until next week. The next major release in NZ is not until ANZ Business Confidence and Building consents on Thursday.

- Accordingly, the market will continue to track U.S. Tsys in the wake of yesterday's FOMC decision. U.S. calendar is light with U.S. Home Sales and Claims data the highlights.

STIR: NZ Still An Outlier But For How Long?

Yesterday we highlighted NZ STIR as an outlier in the $-Bloc with regard to its relatively modest reduction in terminal rate expectations since early March. In terms of explanations, we believed the RBNZ’s reputation as an overshooter of OIS expectationsthis cycle was a key contributor.

- With the Fed delivering a dovishly perceived 25bp hike yesterday, post-FOMC pricing appears to have strengthened NZ STIR’s status as a $-Bloc outlier.

- RBNZ dated OIS has 43bp of tightening over meetings to July priced versus 9bp, 31bp and 35bp of easing respectively priced for the RBA, the BoC and the Fed over the same period.

- Interestingly, with RBNZ Chief Economist Conway (in a speech today) stating that the OCR is near the peak and comfortably above neutral with the full contractionary effects yet to be felt, one must wonder when the NZ STIR will play catch-up with its $-Bloc peers in terms of terminal rate pricing as well as year-end easing.

- A pause in April is possible, but the May MPS would appear more logical for a policy guidance re-set on the back of a new set of forecasts encompassing both local growth setbacks and global growth developments.

Fig. 1: $-Bloc STIR

Source: MNI – Market News / Bloomberg

FOREX: USD Pressured In Asia

The greenback is pressured in Asia, Asia-Pac participants looked to the dovish elements of Wednesday’s post-FOMC statement and Chair Powell’s communique. BBDXY breached lows seen in the aftermath of the FOMC rate decision, and now sits a touch off its lowest level since 14 Feb.

- Kiwi is the strongest performer in the G-10 space at the margins. NZD/USD sits above the 200-Day EMA ($0.6272). Earlier in the session RBNZ Chief Economist Conway spoke this morning, he noted that damaging effects of high inflation and that inflation remains too high in NZ. He also said the RBNZ will need to hike more to return inflation to target.

- AUD/USD prints at $0.6740/45, up ~0.8% today. The next resistance in AUD/USD is seen at the 50-Day EMA ($0.6771).

- Yen is also firmer, benefiting from a fall in 2 Year US Treasury Yields. USD/JPY prints at ¥130.60/70 and has breached yesterday's post FOMC lows. The pair found support below ¥130.54, low from March 20, and marginally pared losses.

- Elsewhere in G-10 broad based USD weakness has seen EUR rise ~0.4%. EUR/USD is within touching distance of yesterday's €1.0912 peak, a break through there would expose key resistance at €1.1033 Feb 2 high.

- Cross asset wise; 2 Year US Treasury yields are ~6bps lower at 3.87% having peaked in early trade at 3.97%. E-minis are ~0.5% firmer, and the Hang Seng is ~0.8% firmer.

- In Europe today we have SNB, Norges Bank and BOE rate decisions. Further out New Home Sales, Initial Jobless Claims and Fedspeak from St Louis Fed Bullard will also cross.

FX OPTIONS: Expiries for Mar23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0580-00(E1.8bln), $1.0650-52(E848mln), $1.0800(E874mln), $1.0890-05(E553mln), $1.0920-25(E541mln)

- USD/JPY: Y130.00($574mln), Y130.37-55($1.3bln), Y131.00($631mln), Y131.50($1.5bln), Y132.00($827mln)

- EUR/GBP: Gbp0.8900(E1.1bln)

- AUD/USD: $0.6640-50(A$643mln)

- USD/CNY: Cny6.7500($1.3bln), Cny6.9500($576mln)

ASIA FX: Broad Base Gains, USD/CNH Back Sub 50-Day MA

USD/Asia pairs are lower across the board. USD weakness against the majors, has spilled over to the region, and while CNH initially struggled to rally, it has caught up this afternoon. Lower US yields (2yr off ~10bps from early session highs) as the market continues to digest yesterday's FOMC, and a resilient equity market backdrop have been other positives. Still to comes is the BSP, with +25bps expected, as well as the CBC in Taiwan, with no change the consensus expectation. Tomorrow the data calendar has Singapore IP and Malaysian CPI.

- USD/CNH currently tracks just above session lows, currently around 6.8200 (we touched 6.8140/45 earlier). This is lows back to the first part of Feb. Gains have accelerated after the pair broke down through the 50 day MA (6.8431). CNH is up around 0.60% for the session, after lagging the USD sell-off to begin with. HK equity related equity strength, related to better technology earnings, is also likely helping at the margins.

- 1 month USD/KRW is close to its 50-day MA as well (near 1275), with the pair last around 1277/78. This puts the pair 1.5% sub NY closing levels. The recovery in local equities form early lows has helped, although this looks to be more a broad USD move, with the won showing its high beta characteristics.

- USD/TWD sits just under 30.40, fresh lows in the pair back to late Feb. We are below all key EMAs, except for the 200 day, which comes in at 30.375, so very close to current spot levels. The simple 50-day MA is also nearby at 30.405. A break below these levels could open up the low 30.00 region/high 29.00 region, which the pair bottomed out in early Feb. Taiwan equities have improved as the session progressed, +0.45% for the Taiex and note yesterday saw over $900mn in offshore inflows to local equities.

- USD/PHP sits below session highs, last around 54.40/45. This is still only 0.15% firmer in PHP terms versus yesterday's closing levels, so the peso is underperforming gains elsewhere in the region. The BSP is expected to hike rates by 25bps later.

- USD/INR is softer this morning, falling ~0.6% in the first part of dealing. The pair last printed at 82.15/20. The Rupee is tracking Asia FX gains seen in the wake of yesterday's dovish +25bps FOMC rate hike.US Treasury Yields are off session highs this morning further pressing the USD. From a technical perspective we have broken the 20-day EMA (82.44), bears now target the 200-Day EMA at 80.87. Bulls look to test the 83 handle.

- USD/SGD is sub Wednesday session lows, last near 1.3240/45. The NEER is elevated but slightly down off recent fresh highs. Feb inflation data was a touch below expectations, but core pressures remain elevated (5.5% y/y).

SGD: Feb Inflation Below Expectations, Core Flat M/M, But Still Elevated Y/Y

Singapore Feb inflation picked up in m/m terms to 0.6% from 0.2% in Jan. This wasn't enough to see y/y momentum accelerate though. The headline y/y eased to 6.3%, from 6.6%, with the market consensus at 6.4%. The core was steady at 5.5% y/y, although this was also sub market expectations at 5.8%.

- Headline inflation is slowly moving off 2022 peaks (7.5% y/y Sep last year). Core is proving to be much more stubborn, holding around at recent highs, although the MAS may take some comfort we aren't accelerating further. Indeed, the core measure was flat in m/m terms.

- Still, outside of declining transport costs, which moved to 9.7% y/y from 11.9%, most other sub-categories stayed around their recent y/y pace. So, it may be too early to expect a meaningful pull back in core inflation pressures.

- Around mid April should be the timing of the next MAS policy meeting. The central bank has to grapple with expectations around the inflation outlook but also recent volatility in global markets and paring back of terminal rate expectations.

- The SGD NEER is just off fresh highs, although this may reflect Singapore's safe haven characteristics attracting capital inflows as opposed to fresh tightening expectations.

EQUITIES: Tech Names & Higher US Futures Help Regional Sentiment

Regional equities are mixed, although those markets that are weaker, aren't down as much as implied by the US fall from Wednesday's session. Higher US futures through the course of today, with eminis and Nasdaq futures tracking around ~0.45% higher has helped. Cross asset wise, lower US yields, and a weaker USD have helped from a risk sentiment standpoint as well.

- The HSI is tracking close to 0.8% higher at this stage. The underlying tech index is +1.6%, the third straight session of gains. This came after Tencent earnings were better than expected. Alibaba shares were also higher. The HS China enterprise index is up 0.92% so far.

- Mainland shares are also firmer, the CSI 300 +0.36%, while the Shanghai Composite is flat. Northbound flows remain modestly positive so far today (+1.45bn yuan).

- The Topix is around 0.4% weaker at the stage, with bank sub-index down around 1.5%. The Taiex is faring better, up around 0.45%, with semiconductor stocks leading the move. The Kospi is around flat, but is comfortably up off session lows.

- The ASX 200 is down near 0.70%, with weakness in materials and financial stocks the main drags.

GOLD: Gold Moves Higher Again But Struggling To Break $2000

Gold is higher again today following its rally post the Fed decision on Wednesday. It reached a high of $1978.86/oz but couldn’t break through $2000 again. Bullion is 0.3% higher to $1975.78 today following +1.6%. It is close to its intraday high of $1977.68. The USD index is down a further 0.4% and US yields are lower, which are supportive of gold.

- The Fed hiked rates 25bp as expected, but considered pausing given recent banking troubles, which was dovish but it was made clear that a cut isn’t imminent, which limited the upside in gold. Inflation still needs to come down but the Fed is close to its terminal rate.

- Bullion is down slightly on the week. Resistance remains at $2009.70, the March 20 high.

- Goldman Sachs revised up its target for gold to $2050 over the next year. It believes that risks are skewed to the upside given that it sees a recession as more likely than a soft landing in the US.

- A number of European central banks meet later and are all expected to increase rates despite recent banking turmoil. The BoE is forecast to hike by 25bp, the SNB 50bp and the Norges bank 25bp. In the US jobless claims, new home sales and Kansas & Chicago activity indices print.

OIL: Oil Prices Pull Back As US Recession Fears Resurface

Oil prices are lower today after rising moderately on Wednesday. Brent is down 0.9% to $76.03 and WTI is down 1% to $70.16, down around $10 from end-2022. Both are off of their intraday lows but are facing whole number support levels. The USD index is 0.4% lower.

- Oil is struggling after the Fed said that there wouldn’t be any rate cuts this year and that it will hike further if needed to bring inflation down. Also, Treasury Secretary Yellen said there’s unlikely to be a “blanket” deposit insurance scheme. Crude markets have been nervous about a tightening-induced US recession which has been exacerbated by recent banking turmoil.

- In addition to demand worries, there is concern on the supply side too. US stocks continue to rise and there is uncertainty over Russian output cuts. However, Goldman Sachs remains bullish oil.

- A number of European central banks meet later and are all expected to increase rates despite recent banking turmoil. The BoE is forecast to hike by 25bp, the SNB 50bp and the Norges bank 25bp. In the US jobless claims, new home sales and Kansas & Chicago activity indices print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/03/2023 | 0830/0930 |  | CH | SNB interest rate decision | |

| 23/03/2023 | 0900/1000 | *** |  | NO | Norges Bank Rate Decision |

| 23/03/2023 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 23/03/2023 | 1200/1200 | *** |  | UK | Bank Of England Interest Rate |

| 23/03/2023 | 1200/1200 | *** | | UK | Bank Of England Interest Rate |

| 23/03/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 23/03/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 23/03/2023 | 1230/0830 | * | | US | Current Account Balance |

| 23/03/2023 | 1400/1000 | *** | | US | New Home Sales |

| 23/03/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 23/03/2023 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 23/03/2023 | 1500/1600 | ** |  | EU | Consumer Confidence Indicator (p) |

| 23/03/2023 | 1500/1600 | | EU | ECB Lane Panels Peterson Institute Conference | |

| 23/03/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 23/03/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 23/03/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 24/03/2023 | 2200/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.