Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

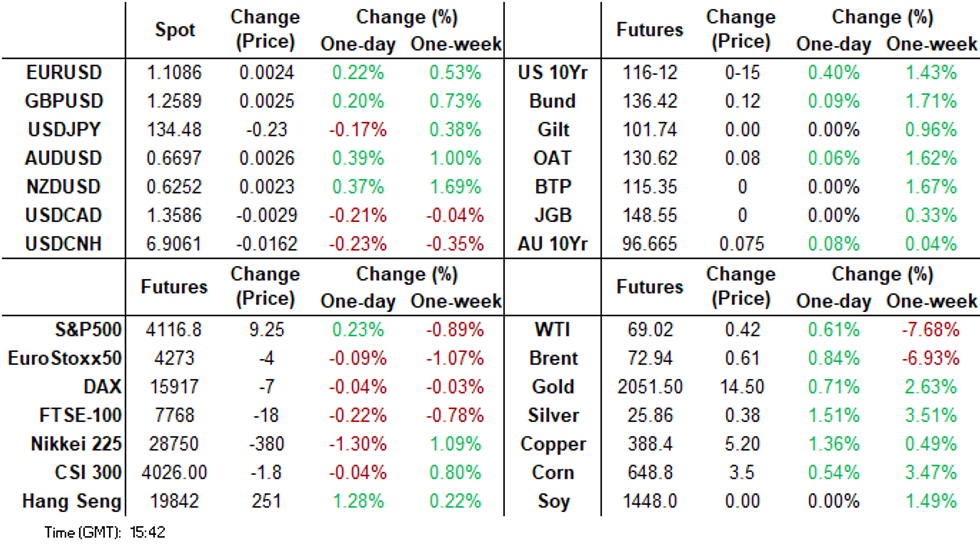

- The early Asia Pac tone was firmly risk-off post the FOMC. PacWest a US regional bank plunged as much as 60% in after hours trading, while WTI futures opened more than 7% lower. There didn't appear to be a fundamental catalyst for oil move. Commodity currencies underperformed as well, particularly against the yen, as US equity futures opened sharply lower and Tsy futures gapped higher.

- There was no follow through to these earlier moves though, tsys ticked away from session highs as WTI and e-minis erased losses to trade marginally firmer. China markets returned, with the Caixin manufacturing PMI coming in weaker than expected, which continues to suggest an uneven recovery. Still, onshore equities are up from early session lows.

- The weaker USD tone has persisted, despite the earlier risk jitters. AUD and NZD have recovered from their earlier dips, while USD/Asia pairs are lower across the board. The BBDXY has ticked through Wednesday's post FOMC lows printing its lowest level since Apr 14.

- Later the ECB meets (see MNI ECB Preview - May 2023) and is expected to hike rates 25bp. In the US, there are Q1 unit labour costs, March trade and April Challenger job cuts data.

MARKETS

US TSYS: Pares Early Gains, Cash Closed In Asia Today

TYM3 deals at 116-11, +0-14, a touch off the base of the 0-15 range on volume of ~120k.

- Cash tsys were closed in Asia today due to the observance of a national holiday in Japan. They will reopen in the London session.

- Tsy futures gapped higher in early dealing, concerns about regional US banks escalated as PacWest fell as much as 60% in post market trade following a report that it's said to weigh strategic options including a sale. Oil fell ~7%, and e-minis were pressured.

- There was no follow through on the early move higher, tsys ticked away from session highs as WTI and e-minis erased losses to trade marginally firmer.

- Further PacWest headlines have crossed this afternoon, with the bank stating it has not experienced out of the ordinary deposit flows and that its planned sale remains on track.

- President Joe Biden has picked Federal Reserve Governor Philip Jefferson for a promotion to vice chair and will nominate economist Adriana Kugler to an open board slot, reports suggested.

- In Europe today the latest monetary policy decision from the ECB provides the highlight. Further out we have Initial Jobless Claims and Trade Balance.

AUSSIE BONDS: Richer, Curve Steeper, Awaits RBA SoMP Tomorrow

ACGBs are stronger (YM +12.0 & XM +7.0) with the 3-year futures contract close to session bests. The 10-year contract tracked US tsy futures which pared early post-NY session gains in Asia-Pac trade. Cash tsys are closed until the London session due to the observance of a national holiday in Japan. Cash ACGBs are 7-12bp richer with the 3/10 curve 5bp steeper.

- Swap rates are 7-13bp lower with 3-year EFP slightly tighter.

- The bills strip bull flattened with pricing +3 to +16.

- RBA dated OIS is 6-17bp softer across meetings beyond August with early '24 leading. A 7% chance of a 25bp rate hike at the June meeting is priced with a cumulative tightening of 8bp priced by August. Terminal rate expectations sit at 3.90% with year-end easing at 24bp.

- The local calendar will release March Housing Finance data tomorrow. The highlight however will be the Statement on Monetary Policy. After the RBA’s surprise rate hike, the market will pour over the forecast update for clues about the policy outlook. Attention will also be paid to the discussion on services inflation given its emphasis in yesterday's decision statement.

- The US calendar sees the release of the March Trade balance and initial jobless claims data.

AUSSIE BONDS: AU/US 10-Year Yield Differential Too Low

The Sydney session opened today with the AU/US 10-year yield differential close to flat, which is in the middle of the range it has traded within since November of last year (+22bp to -32bp).

- In early March, the differential hit a cycle low of -32bp when the RBA shifted to a more dovish stance at its March meeting, before moving higher due to global banking concerns in mid-March.

- The current AU/US 10-year yield differential, at around flat, is the tightest it has been since late February, and 18bp wider than the levels seen before the RBA's surprise 25bp rate cut earlier this week.

- Nonetheless, a simple regression of the AU/US cash 10-year yield differential versus the AU/US 1Y3M swap differential over the current tightening cycle suggests that the 10-year yield differential is currently around 25bp too low, i.e., flat Vs. fair value at 25bp.

- This apparent mispricing is due to the recent significant decline in the US 1Y3M rate and the resulting widening of the AU/US 1Y3M differential. The US 1Y3M swap rate is currently around 30bp lower, and the AU/US differential 30bp wider, than the levels seen at the end of last week.

Figure 1: AU/US Cash 10-Year Yield Differential (%) Vs. AU/US 1Y3M Swap Differential (%)

Source: MNI – Market News / Bloomberg

NZGBS: Curve Bull Steepens, Solid Auction Demand

NZGBs closed with the 2/10 cash curve 5bp steeper with 2-year and 10-year benchmarks respectively 7bp and 1bp richer. The 2-year closed at session bests. The 10-year shifted weaker through the session in sympathy with US tsy futures in Asia-Pac trade.

- Today’s supply saw overall good demand (cover ratios 2.64x to 3.46x) consistent with last week’s auction. The May-26 bid, however, fell well short of the robust demand (cover ratio of 6.25x) displayed at the April 6th auction. Demand for short-end bonds was particularly strong, which could be attributed to concerns over potential over-tightening by the RBNZ, which had unexpectedly raised interest rates by 50bp the day before. The 2/10 cash curve nonetheless steepened around 2bp post-auction.

- Swap rates closed 4-10bp lower with implied swap spreads around 2bp tighter.

- RBNZ dated OIS closed 3-11bp softer with Apr’24 leading. 24bp of tightening is priced for the May 24 meeting with terminal OCR expectations at 5.57%.

- Building approvals rose 7% m/m in March as the impact of cyclone Gabrielle was partially unwound. ANZ commodity export prices fell 1.7% m/m in April.

- The local calendar is light tomorrow with the RBA Statement on Monetary Policy as the Antipodean highlight.

- The US calendar sees the release of the March Trade balance and initial jobless claims data.

OIL: Crude Jitters Ease During APAC Session

After declining over 4% on Wednesday to be down around 13% on the week on the back of deteriorating risk appetite and recession fears, oil prices slumped early in the APAC session with WTI reaching a low of $63.64. But with risk appetite stabilising oil prices are now off these lows with WTI up 0.5% to $68.98/bbl and Brent +0.7% to $72.85. The USD index is down 0.3% today.

- Oil prices are off of their intraday highs of $73.32 for Brent and $69.32 for WTI. Brent broke through $72.34, the March 24 low, on Wednesday which has opened up key support at $70.10, the March 20 low.

- It is unclear why WTI oil prices plunged at today’s open and there is speculation that it was due to the unwinding of speculators’ bullish positions, human error, algorithmic selling or panic selling, according to Bloomberg. Trade at that time is usually thin and Bloomberg is reporting that over 3000 June futures contracts changed hands in the fifth minute of the session. Brent didn’t follow the move when it opened a couple of hours later.

- Later the ECB meets (see MNI ECB Preview - May 2023) and is expected to hike rates 25bp. In the US, there are Q1 unit labour costs, March trade and April Challenger job cuts data.

Source: MNI - Market News/Bloomberg

GOLD: Bullion Moving Closer To $2075.47 Record High

After declining over 4% on Wednesday to be down around 13% on the week on the back of deteriorating risk appetite and recession fears, oil prices slumped early in the APAC session with WTI reaching a low of $63.64. But with risk appetite stabilising oil prices are now off these lows with WTI up 0.5% to $68.95/bbl and Brent +0.7% to $72.85. The USD index is down a further 0.3%.

- Oil prices are off of their intraday highs of $73.32 for Brent and $69.32 for WTI. Brent broke through $72.34, the March 24 low, on Wednesday which has opened up key support at $70.10, the March 20 low.

- It is unclear why WTI oil prices plunged at today’s open and there is speculation that it was due to the unwinding of speculators’ bullish positions, human error, algorithmic selling or panic selling, according to Bloomberg. Trade at that time is usually thin and Bloomberg is reporting that over 3000 June futures contracts changed hands in the fifth minute of the session. Brent didn’t follow the move when it opened a couple of hours later.

- Later the ECB meets (see MNI ECB Preview - May 2023) and is expected to hike rates 25bp. In the US, there are Q1 unit labour costs, March trade and April Challenger job cuts data.

FOREX: BBDXY Through Post Fed Lows

The greenback has been pressured in Asia, BBDXY has ticked through Wednesday's post FOMC lows printing its lowest level since Apr 14. Escalating concerns about regional banks, as PacWest fell as much as 60% in post market trade following a report that it's said to weigh strategic options including a sale, saw risk assets pressured however losses were pared through the session.

- AUD/USD is ~0.2% firmer, the pair firmed off session lows with US Equity futures. We last print at $0.6685/90 after rising ~0.7% from trough to peak. March Trade Balance printed a stronger than forecast surplus of $15.269bn.

- Kiwi is also ~0.2% firmer, NZD/USD found support at $0.62 rising ~0.6% from session lows to print $0.6240/45. March Building Permits rose 7.0% M/M, and April ANZ Commodity Prices fell 1.7%.

- Yen firmed through the session, post Fed lows were breached and JPY held its gains through the session. Support was seen at the 20-Day EMA (¥134.40).

- Elsewhere in G-10 NOK and SEK are ~0.3% firmer however Asia-Pac liquidity is generally poor. EUR and GBP are both ~0.2% firmer following the broader USD trend.

- Cross asset wise; WTI futures are ~0.5% firmer after being down 7% in early dealing. E-minis are marginally firmer erasing an early 0.5% loss. BBDXY is down ~0.3%.

- The ECBs monetary policy decision provides the highlight today, the bank is expected to raise its key policy rates 25bps. The MNI preview of the event is here.

China Data: Caixin Manufacturing PMI Slips Back Into Contractionary Territory

The Caixin manufacturing PMI came in below expectations, printing at 49.5, versus a consensus of 50.5. We are still above Jan levels near 49.0, but it signals an uneven recovery. The official manufacturing PMI also fell into contractionary territory, 49.2 from 51.9 in Mar. This is widening the divergence with better service related outcomes.

- Caixin noted that production was weighed down by faltering new orders, which fell for the first time in 3 months. Caixin stated this reflected softer than expected consumer spending, which comes after bumper retail spending figures.

- New export orders painted a better picture, but this didn't prevent staff losses. Also note Caixin said input costs and selling prices at factories slumped at the quickest rate in about seven years. No doubt falling commodity prices were a factor, but this also speaks to an uneven demand backdrop.

- Note the Caixin Services PMI will print tomorrow (not today as we posted earlier). The market expects a 57.0 reading versus 57.8 prior.

- The authorities appear mindful of the evolving nature of the recovery. Last week’s Politburo communique noted that Q1 data came in better than expected, but concluded "demand remained insufficient" while "promoting high-quality growth remained challenging.”

ASIA FX: USD/Asia Pairs Lower Post FOMC

USD/Asia pairs are lower post the FOMC, but we are away from best levels. USD/CNH couldn't sustain a move sub 6.9000, while USD/KRW found support below 1320 for the 1 month NDF. Regional equity trends have been mixed, while the Caixin manufacturing PMI in China was weaker than expected. Tomorrow, we get the Caixin services PMI for China. Taiwan inflation is out, as is the Philippines CPI. Singapore retail sales, and Indonesia Q1 GDP are also due. Malaysia markets return tomorrow, but Thailand's remain closed.

- Positive CNH sentiment was halted by the weaker than expected Caixin manufacturing PMI print (49.5, versus 50.0 expected). USD/CNH did eventually get sub 6.9000 (but only as far as 6.8960/65), we now sit back close to 6.9060. It has been an indifferent lead for China equity markets on a return from the May day holiday period.

- USD/KRW has mostly traded with a softer bias, shrugging off US recession concerns. The 1 month NDF got to a low of 1318.45, before rebounding back towards 1322, which is where we currently track. This puts us back below the 200-day MA around 1326. Onshore equities are up off earlier lows, with the Kospi close to flat at this stage.

- USD/IDR has fallen to fresh YTD lows, despite cross asset headwinds. The pair got to a low of 14575 but is now back to 14630/35, still ~0.35% firmer in IDR terms versus yesterday's close. Broad USD/Asia losses are helping the IDR rally. From a technical standpoint, not much appears in the way of a move to the low 14400 regions (lows from June last year), if we can sustain a break of 14600.

- The SGD NEER (per Goldman Sachs estimates) firmed to its highest level since the April MAS meeting yesterday before moderating gains. We currently sit ~0.9% below the top of the band. USD/SGD is under pressure today, the pair is down ~0.2% following a broader USD/Asia trend. Post FOMC lows remain intact for now, and the pair sits at $1.3270/75. Apr S&P Global PMI printed at 55.3, rising from the prior read of 52.6, to print its highest level since November 2022.

SOUTH KOREA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of South Korean Newspapers and some other major news outlets from the past day or so.

Economy: Yoon calls for Indo-Pacific solidarity to ride out economic troubles (link)

Economy: Korea to join efforts to form cooperative supply chain in Asia: Yoon (link)

Economy: Korea's GDP forecast to grow 1.1 percent in 2023: S&P (link)

Economy: Hyundai and Kia's U.S. Car Sales Increased by Almost 15% in April (link)

South Korea/Japan: Japanese PM to meet with S. Korean biz leaders during visit to Seoul (link)

Geopolitics: S. Korea pushing to resume regular talks with Japan, China: official (link)

South Korea/North Korea: N. Korea steps up criticism of S. Korea-U.S. deterrence plan (link)

Markets: Seoul advised to prepare exit plans for real estate funds: South Korean investors face a growing risk of losses from overseas real estate loans (link)

Markets: Washington signals support for South Korean chipmakers in US battle with China

Samsung and SK Hynix can expect extension to permission for sending US chipmaking tools to their Chinese plants (link)

Markets: Samsung Electronics may face 1st labor strike over wage deadlock (link)

Indonesia: Highlights From Local News Wires

Below is a collection of recent news wires reports from English versions of Indonesian Newspapers and some other major news outlets.

Politics: “Ganjar’s popularity soars among knowledgeable voters after PDI-P announcement” – Jakarta Globe (link)

- A Saiful Mujani Research poll taken at the end of April found that Presidential candidate Ganjar’s support increased 13pp to 20.8% amongst “well-informed” voters from 3 weeks ago. He would get 30.4% of the vote with Prabowo on 29.5%, Anies 19.8% and Airlangga 2.9%.

Politics: “Jokowi meets with six party leaders as things get complicated ahead of elections’ – Jakarta Globe (link)

Politics: “Golkar, PKB proclaim ‘driving’ role in grand alliance” – Jakarta Post (link)

Politics: “Megawati says people line up to become Ganjar’s running mate” – Jakarta Globe (link)

Geopolitics: “Tensions in South China Sea continue, but ASEAN successfully resolve maritime disputes” – Jakarta Post (link)

Economy: “Manufacturing PMI up in April on Eid demand: ministry” – Antara News (link)

Economy: “International arrivals in Indonesia rise by 508.87 pct in Q1” – Jakarta Globe (link)

Economy: “Investment is to spur job creation: Jokowi on May Day” – Jakarta Globe (link)

Economy: “Sandiaga Uno expects economic ‘blessing’ from ASEAN summit” – Jakarta Post (link)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/05/2023 | 0715/0915 | ** |  | ES | S&P Global Services PMI (f) |

| 04/05/2023 | 0745/0945 | ** |  | IT | S&P Global Services PMI (f) |

| 04/05/2023 | 0750/0950 | ** |  | FR | IHS Markit Services PMI (f) |

| 04/05/2023 | 0755/0955 | ** |  | DE | IHS Markit Services PMI (f) |

| 04/05/2023 | 0800/1000 | *** |  | NO | Norges Bank Rate Decision |

| 04/05/2023 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (f) |

| 04/05/2023 | 0830/0930 | ** |  | UK | BOE M4 |

| 04/05/2023 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 04/05/2023 | 0830/0930 | ** | | UK | S&P Global Services PMI (Final) |

| 04/05/2023 | 0900/1100 | ** | | EU | PPI |

| 04/05/2023 | 1215/1415 | *** | | EU | ECB Deposit Rate |

| 04/05/2023 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 04/05/2023 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 04/05/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 04/05/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 04/05/2023 | 1230/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 04/05/2023 | 1230/0830 | ** | | US | Trade Balance |

| 04/05/2023 | 1230/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 04/05/2023 | 1245/1445 | | EU | ECB Post-Meeting Press Conference | |

| 04/05/2023 | 1400/1000 | * | | CA | Ivey PMI |

| 04/05/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 04/05/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 04/05/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 04/05/2023 | 1650/1250 | | CA | BOC Governor speech/press conference. |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.