Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

OVERNIGHT NEWS AND PRESS

EXECUTIVE SUMMARY

* RBA CUTS RATES, ANNOUNCES A$100 BILLION BOND-BUYING PROGRAM (BBG)

* CHINA BAN ON US$400 MILLION AUSTRALIAN WHEAT IMPORTS LOOMS (SCMP)

* BATTLE AT ARM CHINA THREATENS $40BN NVIDIA DEAL (FT)

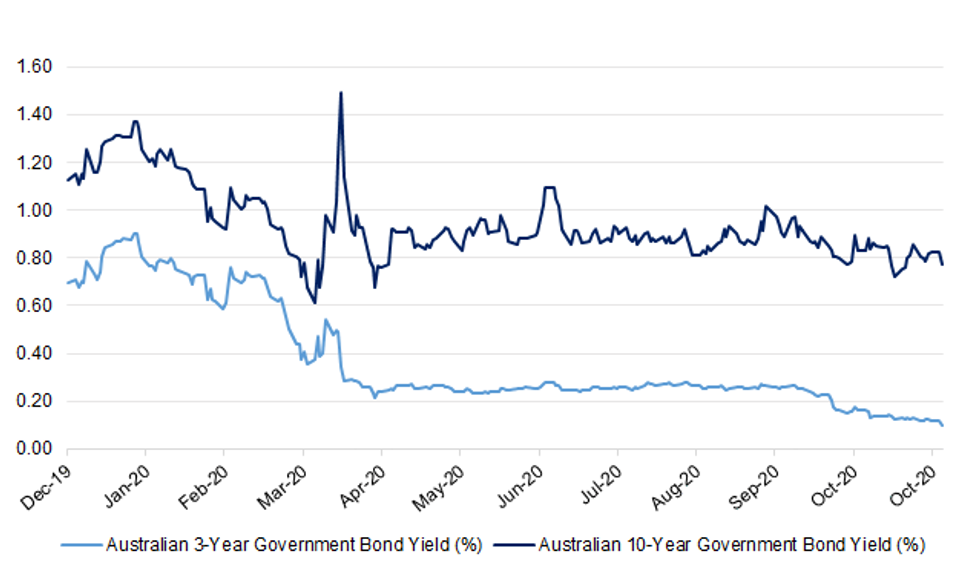

Fig 1: Australian 3- & 10-Year Government Bond Yields

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

CORONAVIRUS: The population of Liverpool will be offered regular Covid-19 tests in the first pilot of whole city testing in England. Everyone living or working in the city will be offered them - whether they have symptoms or not. The aim is to limit spread of the virus by identifying as many infected people as possible, and taking action to break chains of transmission. (BBC)

BREXIT: European Union negotiators have conceded a major British demand on fishing rights after Brexit, it was reported on Monday. Brussels was said to have caved on a long-standing UK demand that future fishing opportunities be calculated on the basis of zonal attachment, although that was denied by some EU sources. (Telegraph)

FISCAL: Self-employed workers will be able to claim government support worth 80% of trading profits as England prepares to enter a new lockdown, Boris Johnson has announced. Ahead of the new national measures coming into force on Thursday, the prime minister used a House of Commons statement to warn of an "existential threat" to the NHS due to the "remorseless advance" of the second wave of coronavirus infections. "It's now clear we must do more together," he told MPs. (Sky)

ECONOMY: British companies face the prospect of a "bleak mid-winter" according to the boss of the UK's biggest lobby group, after high-street retailers, pub chains and airlines warned of the impact a second lockdown in England will have on their businesses. Carolyn Fairbairn, the director general of the Confederation of British Industry (CBI), said the latest English lockdown was in some ways worse than the first one, which started in March. (Guardian)

EUROPE

FRANCE: France reported record daily coronavirus cases on Monday after a slowdown over the weekend, with 52,518 confirmed new infections. Deaths increased by 416 to 37,435, with the seven- day average of fatalities climbing to the highest since April. (BBG)

AUSTRIA: Gunmen opened fire on people enjoying a last night out at Vienna's cafes and restaurants before a coronavirus lockdown Monday in what authorities said was a terrorist attack that left at least two dead — including one of the assailants — and 15 wounded. (Associated Press)

U.S.

ECONOMY: MNI INTERVIEW: US Factory ISM Surges But Faces 2nd Wave Risk

- The U.S. factory recovery is poised for growth through year-end but remains jeopardized by rising coronavirus cases and the failure of Congress to deliver fiscal relief, Institute for Supply Management chair Tim Fiore told MNI Monday - on MNI Policy Main Wire and email now - for more details please contact sales@marketnews.com.

ECONOMY: MNI INTERVIEW: US October Job Openings Up Despite Virus Surge

- Employment isn't likely to drop to the record lows seen when the U.S. was battling its first wave of Covid-19 even as caseloads surged to fresh highs across the country in October, Julia Pollak, a labor economist at online job marketplace ZipRecruiter, told MNI, citing steadily rising job postings over the past weeks - on MNI Policy Main Wire and email now - for more details please contact sales@marketnews.com.

FISCAL: MNI POLICY: U.S. Cuts Q4 Borrowing Plans in Half to USD617B

- The U.S. Treasury on Monday said it plans to borrow USD617 billion in the fourth quarter, half what officials predicted in August because the absence of a second fiscal package left the government with more cash on hand. The borrowing estimate in Q4 is USD599 billion lower than expected in August 2020, and assumes a cash balance of USD800 billion at the end of December. During the first quarter of 2021, Treasury expects to borrow USD1.127 trillion in privately-held net marketable debt, assuming an end-of-March cash balance of USD800billion - on MNI Policy Main Wire and email now - for more details please contact sales@marketnews.com.

CORONAVIRUS: The US reported one of its biggest single-day jumps in coronavirus infections since the start of the pandemic, adding nearly 83,000 new cases on Monday and another rise in hospitalisations. (FT)

CORONAVIRUS: Massachusetts Gov. Charlie Baker announced curfews for businesses and a stay-at-home advisory as the number of coronavirus cases continues to climb. Baker also issued an updated face covering order, mandating that everyone in public wear a mask, even when maintaining a social distance of six feet. (Boston Business Journal)

POLITICS: MNI POLITICAL RISK ANALYSIS – US Election – Viewers Guide

- In this article we provide an estimated timetable of events for the US general election taking place on Tuesday 3 November as ballots are counted. As well as a guide of what times various states may call their results, we also provide analysis on key counties to watch in swing states that are likely to give the best indication as to the direction the presidency is heading in. All timings in this article are subject to change and given the major shift to mail-in and early voting, the tabulation process may take longer or be more prone to challenges than in previous election cycles. As such, there is the possibility that at the end of the counting of ballots it is still not clear which candidate has won the presidency or which party is in control of the Congress - for more details please contact sales@marketnews.com.

POLITICS: Early voting in the 2020 election across the U.S. on Monday had already reached 71% of 2016's total turnout, according to state data compiled by the U.S. Elections Project. (Axios)

POLITICS: Democratic presidential nominee Joe Biden holds narrow leads over President Donald Trump in six states the president aims to defend Tuesday in his bid for a second term, according to a new CNBC/Change Research poll. The survey released Monday finds the former vice president holding at least a slim edge in all of Arizona, Florida, Michigan, North Carolina, Pennsylvania and Wisconsin, all of which Trump won in 2016. Even so, it shows a race within striking distance for the president in most of those electoral college prizes.

- All six swing states: Biden 50%, Trump 46%

- Arizona: Biden 50%, Trump 47%

- Florida: Biden 51%, Trump 48%

- Michigan: Biden 51%, Trump 44%

- North Carolina: Biden 49%, Trump 47%

- Pennsylvania: Biden 50%, Trump 46%

- Wisconsin: Biden 53%, Trump 45% (CNBC)

POLITICS: Democrat Joe Biden holds a narrow lead over President Donald Trump in the all-important battleground state of Pennsylvania, while the two candidates are tied in Arizona, according to the final NBC News/Marist state polls of the 2020 presidential election. (NBC)

POLITICS: Democratic candidate Joe Biden has a narrow lead in the key states of Florida and Ohio, according to a Quinnipiac poll published just before Election Day. In Florida, 47 percent of likely voters support Biden, while 42 percent support President Donald Trump, according to the poll released Monday. In Ohio, 47 percent support Biden and 43 support Trump. Nationally, Biden has a wide lead with 50 percent of likely voters supporting him to only 39 percent for Trump. (Politico)

POLITICS: Democrat Joe Biden appeared to take a narrow lead over President Donald Trump in Florida in the final days of the 2020 U.S. election campaign, with the two candidates locked in a dead heat in North Carolina and Arizona, according to Reuters/Ipsos opinion polls released on Monday. A week earlier, Reuters/Ipsos polls showed Trump and Biden in a statistical tie across the three states. (RTRS)

POLITICS: The Biden campaign is preparing for a long election night and is warning the country — and the media — to ignore any victory declaration from President Trump before all the ballots are counted.

POLITICS: A federal judge on Monday rejected a Republican request to invalidate 127,000 ballots that had already been cast via drive-through voting stations across Harris County, Texas. (Axios)

POLITICS: A Nevada judge rejected a GOP lawsuit seeking to halt early vote counting in Clark County, which includes Las Vegas, over stringency of signature-matching computer software and how closely observers can watch votes being counted. (CNN)

EQUITIES: Apple announced on Monday an event for Nov. 10 where it's expected to announce new Macs. (CNBC)

OTHER

GLOBAL TRADE: Nvidia's $40bn deal for the UK-based chip designer Arm is facing fresh problems in China, after it emerged that the disaffected head of Arm's local joint venture controls almost 17 per cent of the unit. Company registration documents reviewed by the Financial Times show that Allen Wu, the chief executive of Arm China, assumed control of a key investment firm in November last year, and now controls four out of six of Arm China's shareholders.

GLOBAL TRADE: MNI EXCLUSIVE: Boeing An Early Test For EU Ties If Biden Wins

- The EU's dispute with the U.S. over subsidies for Boeing and Airbus will provide an early test of the bloc's willingness to work with any Joe Biden administration, a former senior U.S. diplomat told MNI, adding that substantive differences on trade would persist whoever wins Tuesday's elections - on MNI Policy Main Wire and email now - for more details please contact sales@marketnews.com.

HONG KONG: Hong Kong will extend all social distancing rules by another week, Chief Executive Carrie Lam says at briefing. Hong Kong will offer free virus test for kindergarten, primary and high school staff next week in phases. Government clinics will distribute testing and specimen bottles during the weekend and offer free testing kits at vending machines. The four community testing centers operated by private labs will provide virus check for HK$240 ($31) per test. (BBG)

HONG KONG: Hong Kong Chief Executive Carrie Lam aims to deliver her policy address Nov. 25, she says at briefing. Her visit to Beijing, Guangzhou and Shenzhen this week would focus on how the Chinese government can give the city more support in reviving the economy, including measures on further integration with the mainland, financial services, aviation and technology innovation. (BBG)

RBA: Australia's central bank cut interest rates and announced a new bond-buying program as it seeks to ensure a rapid recovery across an economy now free of lockdowns. The Reserve Bank of Australia lowered its key interest rate, yield-curve target and bank lending facility rate to 0.10% from 0.25%, as forecast by an overwhelming majority of economists. The board also said it would buy A$100 billion ($70.4 billion) of government bonds with maturities of around 5-10 years over the next six months. These will comprises securities issued by the federal government and the states and territories at an expected 80:20 split. The RBA also cut the rate paid to commercial lenders for their deposits at the central bank to zero. (BBG)

AUSTRALIA/CHINA: China is expected to ban imports of Australian wheat, putting a A$560 million (US$394 million) trade in doubt, with the grain the latest to join a list of new blocks on Australian products, according to industry sources. From Friday, barley, sugar, red wine, timber, coal, lobster, copper ore and copper concentrates from Australia, are expected to be barred from China even if the goods have been paid for and have arrived at ports. The ban on wheat is likely to follow, although a date has not yet been set, sources said. It is understood that Beijing will communicate the bans to all Chinese state-owned and private traders by Tuesday. Traders who have already been notified said no formal document was issued nor were reasons provided. (SCMP)

RBNZ: Finance Minister Grant Robertson comments in interview with Radio New Zealand. Says decisions on LVR loan restrictions are the responsibility of the RBNZ "but it's something we've got significant interest in". Says anything that threatens financial stability is something the government and the RBNZ take seriously. Will meet RBNZ Governor Adrian Orr early next week to talk through where his thinking is. (BBG)

TAIWAN: Eight Chinese aircraft entered Taiwan's southwest Air Defense Identification Zone on Nov. 2, according to Taiwan's Ministry of National Defense. Taiwan's air force issued radio warnings, deployed patrolling aircraft and air defense missile systems to monitor the activities. (BBG)

MARKETS: The world's top asset manager BlackRock downgraded European equities to neutral on Monday on a surge in COVID cases and renewed restrictions, though raised exposure to emerging stocks on a rising probability of a Democratic sweep in the U.S. vote. "Polls are suggesting a greater likelihood of a Democratic sweep in this week's U.S. election," Mike Pyle, global chief investment strategist at the BlackRock Investment Institute, said in a note to clients. "We are starting to incorporate themes we believe would outperform in that event, moving toward a more pro-risk stance overall despite last week's market pullback." BlackRock upgraded emerging market equities to overweight, citing the rising probability of a Democratic sweep outcome, with larger fiscal spending, more stable foreign policy, a weaker dollar and negative real rates poised to benefit developing market assets. The asset manager also upgraded Asia fixed income to overweight, saying China and other Asian countries had done better in containing the virus and are further ahead on economic recovery. However, BlackRock downgraded Japan equities to underweight, adding that a weaker dollar and stronger yen could weigh on the country's exporters. (RTRS)

OIL: Russian oil company sources tell Energy Intelligence that the companies may be willing to go along with an extension of Opec-plus production cuts at their current levels into next year, if current unsupportive market conditions persist. (Energy Intelligence)

CHINA

POLICY: China will focus on improving and opening its markets and promote the efficient allocation of resources to expand domestic demand, Xinhua News Agency reported late Monday. The report, which came from the16th meeting on deepening reform chaired by President Xi Jinping, said China would also increase the competitiveness of SOEs, improve their roles in safeguarding strategic security and industry leadership, while at the same time preventing the loss of state assets. (MNI)

LAND: China's top leaders have urged local authorities to give 30-year extensions to rural land leases after they expire, so as to maintain stable collective ownership and rural contract-farming systems, the People's Daily reported. The registration and certification processes for rural contracted lands is critical in improving rural governance, and the 30-year lease extension project will help safeguard the legitimate rights and interests of millions of farmers, the Daily said citing Premier Li Keqiang. (MNI)

FINTECH: Chinese regulators have increased measures to supervise fin-tech companies in an effort to prevent risks, the Securities Times reported in its WeChat social media account. The PBOC and three other financial regulators on Monday summoned Jack Ma and two other executives of Ant Group for talks over regulations. After the meeting, the company said it would accept supervision, the Times said. Online micro loan lenders would also begin to face stricter supervision and must now seek approvals to conduct lending business across provinces, the Times report said. (MNI)

OVERNIGHT DATA

AUSTRALIA ANZ ROY MORGAN WEEKLY CONSUMER CONFIDENCE

Confidence gained for the ninth straight week and is now close to neutral, its highest level since the pandemic induced collapse in confidence in mid-March. The details suggest some caution about the result, however. 'Current financial conditions' fell by more than 6% – its biggest weekly decline since the extreme weakness seen in March. This may be a sign that the cutbacks in the JobKeeper and JobSeeker payments are starting to be felt. The sub-indices can be volatile from week-to-week, as evidenced by the jump in inflation expectations after the plunge the week before, so we need to be cautious about reading too much into the drop. And consumers are quite confident about their future financial outlook. Still, we will be looking at other data (such as ANZ observed card spending) for any confirmation that household financial conditions are tightening. (ANZ)

SOUTH KOREA OCT CPI +0.1% Y/Y; MEDIAN +0.8%; SEP +1.0%

SOUTH KOREA OCT CPI -0.6% M/M; MEDIAN 0.0%; SEP +0.7%

SOUTH KOREA OCT CORE CPI +0.1% Y/Y; MEDIAN +0.7%; SEP +0.9%

CHINA MARKETS

PBOC NET INJECTS CNY20BN VIA OMOS

The People's Bank of China (PBOC) injected CNY120 billion via 7-day reverse repos with the rate unchanged on Tuesday. This resulted in a net injection of CNY20 billion after the maturity of CNY100 billion of reverse repos, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) fell to 2.1522% at 09:35 am local time from the close of 2.4630% on Monday: Wind Information.

- The CFETS-NEX money-market sentiment index closed at 36 on Monday vs 69 on Friday. A lower index indicates decreased market expectations for tighter liquidity.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 6.6957 on Tuesday, compared with the 6.7050 set on Monday.

MARKETS

SNAPSHOT: RBA Moves To ELB In Rates, Adopts Purer Form Of QE

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 is closed

- ASX 200 up 115.102 points at 6066.4

- Shanghai Comp. up 35.836 points at 3260.779

- JGBs are closed

- Aussie 10-Yr future up 5 ticks at 99.225, yield down 5bp at 0.773%

- U.S. 10-Yr future -0-00+ at 138-09, cash Tsys are closed

- WTI crude down $0.04 at $36.77, Gold down $2.4 at $1893.06

- USD/JPY up 1 pip at Y104.73

- RBA CUTS RATES, ANNOUNCES A$100 BILLION BOND-BUYING PROGRAM (BBG)

- CHINA BAN ON US$400 MILLION AUSTRALIAN WHEAT IMPORTS LOOMS (SCMP)

- BATTLE AT ARM CHINA THREATENS $40BN NVIDIA DEAL (FT)

BOND SUMMARY: Tsys Tight With Japan Out, ACGBs Steal Limelight As RBA Eases

T-Notes +0-00+ at 138-10, with the contract happy to stick to a 0-02+ range in Asia-Pac hours, ahead of the well-documented round of local event risk, with the lower liquidity backdrop owing to the Japanese holiday and ensuing cash Tsy market closure (until London hours) also limiting activity.

- Aussie swaps have widened vs. the ACGB space on the back of the RBA decision, with the more aggressive than consensus 5-10 Year bond purchase horizon (6 months vs. 12), alongside an in line with consensus purchase war chest of A$100bn, forward guidance tweak pointing to lower for longer settings at the RBA (after the expected 15bp cuts to the cash rate target, 3-Year ACGB yield target and rate applied to the TFF facility) and openness to doing more, if required, at the fore (Governor Lowe's press conference highlighted that any further easing would likely focus on the bond side of the equation, as opposed to interest rates, with the Bank still against the idea of -ve rates). YM +2.0 and XM +6.0 at typing, as the latter sits shy of the reaction highs, curve flatter vs. pre-decision levels. Bills have also firmed and now sit 2-3 ticks higher through the reds. The IRH1 contract printed as high as 100.01, i.e. in negative BBSW territory. This was aided by the interest rate being paid on E/S surplus balances lodged at the RBA being set at 0.00% (given the recent relationship between this rate and BBSW fixings), which only a few pointed to as their base case ahead of the decision (most looked for 0.01% or 0.05%). A reminder that RBA Assistant Governor Kent recently noted that it wouldn't be surprising to sit the BBSW fixing slip into negative territory.

EQUITIES: Bid Pre-Election

Asia-Pacific equities rallied hard, taking their lead from Wall St. and Monday's recovery in crude prices, even as the Japanese holiday sapped liquidity from the region.

- E-minis had a look through their respective Monday highs, before fading back from best levels, as caution remained evident ahead of the Presidential election, making the moves a little indecisive on net. A reminder that Joe Biden Remains the favourite to take the White House (per polls and betting markets), while a 'Blue Wave' scenario is priced, roughly, as a 50/50 scenario, per the latest betting market odds.

- Ant Financial & pipeline IPO matters continued to dominate in China & Hong Kong.

- Nikkei 255 closed, Hang Seng +2.0%, CSI 300 +1.0%, ASX 200 +2.1%

- S&P 500 futures +13, DJIA futures +160, NASDAQ 100 +15.

OIL: Choppy Prices To Start The Week

WTI & Brent gave back their post-settlement gains in Asia-Pac hours and last sit virtually unchanged, with e-minis off highs.

- A reminder that crude saw a sharp recovery from the European lockdown/Libyan supply inspired Asia-Pac lows on Monday, aided by a RTRS source report suggesting that "top managers of Russian oil companies and Russian Energy Minister Alexander Novak on Monday discussed a possible extension of oil output restrictions into the first quarter of 2021." The piece went on to note that "Russian oil companies and Energy Minister Novak discussed three options on Monday... One of the options was to extend the current output curbs into the first quarter of 2021, the source said. The two other options were to increase oil output in January, as planned, or to cut output even further." Elsewhere, Russian Deputy Energy Minister Sorokin declined to comment on future decisions surrounding OPEC+ matters, stressing that broader oil market conditions would be dependent on how the world contains COVID-19.

- Elsewhere, U.S. Gulf of Mexico facilities continue to come back online, with 28% of offshore facilities shut in, per yesterday's BSEE count.

GOLD: U.S. Real Yields Support Bullion Ahead Of Event Risk

Monday's fall in U.S. real yields & some pre-U.S. election caution supported bullion in the early exchanges this week, with spot testing $1,900/oz to the upside in Tuesday's Asia-Pac session as a result. The risk-heavy U.S. docket is set to dominate matters this week, while technical parameters remain little changed.

FOREX: RBA Decision Knocks AUD, USD/CNH 1-Week Implied Vol At Record High As U.S. Election Looms Large

AUD established itself as the worst performer in G10 FX space, following the monetary policy decision from the RBA. The in-line decision to cut the cash rate, 3-Year yield target & TFF rate to 0.1% was coupled with the reduction of the rate applied to ES balances to zero and the announcement of an intention to buy A$100bn worth of ACGBs from the 5-10 Year sector over the next six months (i.e. more aggressive horizon than expected). Furthermore, the Bank tweaked its forward guidance, forecasting no cash rate hikes for at least three years.

- Apart from the RBA decision, news & data flow was light and activity was limited by a market holiday in Japan. Most G10 pairs were happy to hold relatively tight ranges.

- The U.S. election steals the spotlight today, with market jitters reflected in spikes in implied volatilities across multiple USD crosses. Offshore yuan grabbed attention as one-week tenor for USD/CNH surged to the highest level since BBG started running the data series in 2011.

- Spot USD/CNH hugged a fairly narrow range overnight, recouping its initial losses after a softer than expected PBoC fix.

- Elsewhere, focus turns to U.S. factory orders & final durable goods orders, as well as comments from ECB's Knot and Riksbank's Ingves & Breman.

FOREX OPTIONS: Expiries for Nov3 NY cut 1000ET (Source DTCC):

- EUR/USD: $1.1435-50(E529mln), $1.1590-00(E620mln-EUR puts), $1.1650(E622mln), $1.1725(E585mln-EUR puts), $1.1895-1.1905(E1.5bln)

- USD/JPY: Y104.50-55($540mln), Y105.45-50($1.4bln)

- GBP/USD: $1.2850(Gbp684mln-GBP puts), $1.3000(Gbp456mln), $1.3100(Gbp631mln-GBP calls)

- EUR/GBP: Gbp0.9000(E720mln-EUR puts)

- USD/CHF: Chf0.9200($675mln-USD calls)

- AUD/USD: $0.7000(A$706mln), $0.7035-55(A$847mln)

- USD/CAD: C$1.2995-1.3005($550mln)

- USD/CNY: Cny6.5334($1.2bln), Cny6.72($500mln)

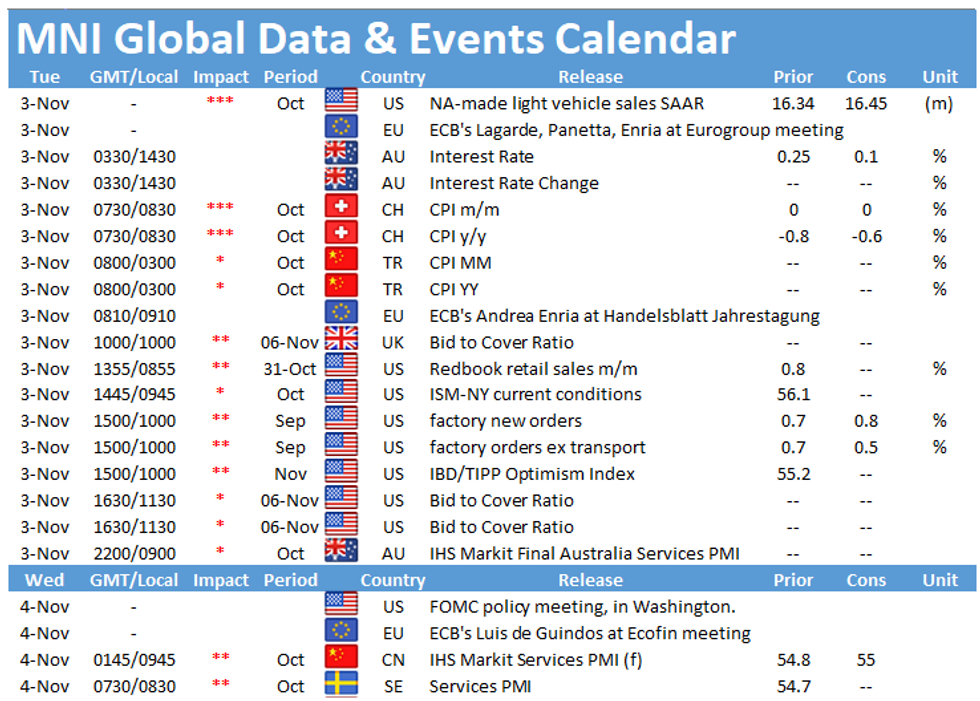

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.