Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

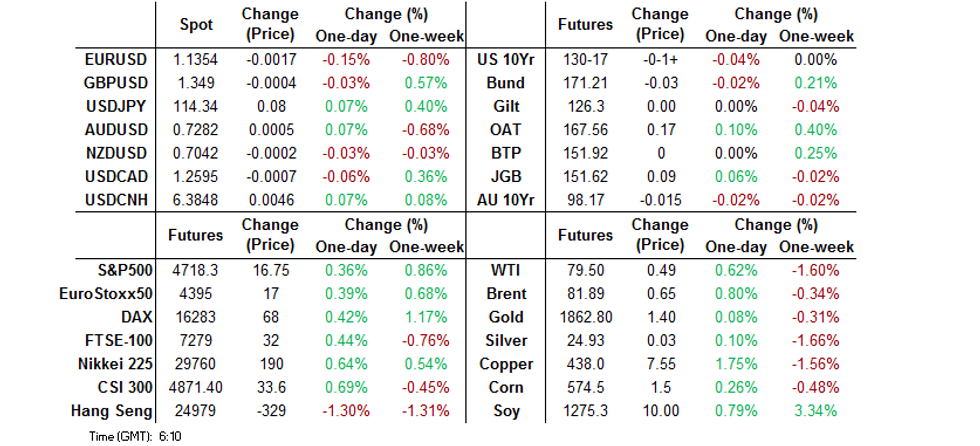

- Light macro headline flow overnight left most of the focus on the race to sit atop the Federal Reserve & the "paid for" status of U.S. President Biden's BBB plan.

- Chinese tech names struggled on the back of softer '22 guidance from Alibaba.

- Fedspeak and BoE rhetoric once again headline on Friday.

BOND SUMMARY: Core FI Mixed In Asia

Fresh record highs for both the S&P 500 & NASDAQ 100 e-mini contracts applied some very modest pressure to the Tsy space, although tight ranges were in play in the space overnight. T-Notes last -0-01+ at 130-17, sticking to a narrow 0-04 range. Cash Tsys are ~1.0-1.5bp cheaper across the curve. Macro headline flow remains very light. NY hours will be headlined by Fedspeak from Vice Chair Clarida & Governor Waller. We will also see the House vote on President Biden's BBB Bill. A note that the CBO & the White House are at loggerheads re: the "paid for" status of the BBB scheme.

- JGB futures extended their overnight uptick, +11 into the bell. Confirmation of the rumoured Y55.7tn fiscal spending package (with total support meeting the expected Y79tn watermark) via Japanese PM Kishida seemingly applied some modest pressure in the morning, with the need for swift compilation (by year end) and disbursement highlighted. A fresh bid came in during the Tokyo afternoon. Cash JGBs run flat to 1.5bp richer across the curve, with 30+-Year paper seeing some light outperformance on the lessening of issuance concerns re: the fiscal package (surplus holdings and unused funds from previous stimulus schemes may be able to do a fair chunk of the heavy lifting).

- Aussie bond futures looked through the release of next week's AOFM issuance slate, even with another A$300mn added to nominal coupon issuance (which now sits at A$2.8bn vs. this week's A$2.5bn), via ACGB Jun-51 supply on Monday. The AOFM has departed from the recent norms in terms of the number of ACGB auctions (2), with 3 rounds of coupon supply due next week. We will also see a notable uptick in Note issuance, which rises to A$5bn from the typical A$2bn. It looks like the AOFM is looking to rebuild its cash buffers. YM unch. & XM -1.5 at the close, with tight trade in play on Friday. Elsewhere, the latest round of ACGB Nov-24 supply passed smoothly, with relative and outright plays likely facilitating strong pricing as the weighted average yield printed 0.87bp through prevailing mids (per Yieldbroker). A reminder that heavy borrowing via the RBA's SLF also pointed to the potential for a strong auction. The cover ratio eased a bit vs. the prev. auction of the line, but that metric was particularly strong last time out and still printed comfortably above 4.50x this time around.

FOREX: USD Edges Higher In Quiet Asia-Pac Trade

The DXY edged higher from the off amid an uptick in U.S. Tsy yields, correlated with fresh record highs for both the S&P 500 & NASDAQ 100 e-minis.

- Firmer crude oil prices lent support to CAD and NOK. AUD followed suit but its Antipodean cousin NZD faltered.

- The kiwi slipped as BBG trader source pointed to fast money trimming longs amid lack of new catalysts after Thursday's inflation expectations data.

- All in all, major crosses held narrow ranges as broader headline flow was relatively thin.

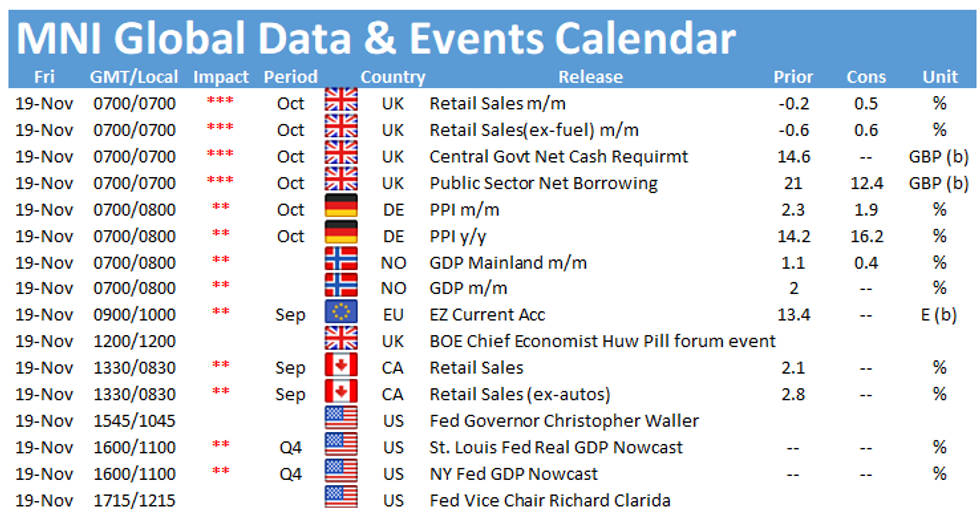

- UK & Canadian retail sales as well as Norwegian GDP take focus going forward. Comments are due from Fed's Waller & Clarida, ECB's Lagarde & Weidmann as well as BoE's Pill.

FOREX OPTIONS: Expiries for Nov19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1375-00(E1.4bln), $1.1445-50(E581mln), $1.1500(E1.6bln)

- USD/JPY: Y114.75-76($637mln)

- EUR/GBP: Gbp0.8590-00(E1.1bln)

- USD/CAD: C$1.2650($526mln), C$1.2800-20($1.1bln)

- USD/CNY: Cny6.3700($1.1bln)

ASIA FX: Greenback Outperforms Asia EM FX

The U.S. dollar caught a light bid during the final Asia-Pac session of the week, providing mild support to USD/Asia crosses.

- CNH: Offshore yuan softened. Participants digested the latest raft of PBOC rhetoric and an in-line yuan fixing.

- KRW: The won underperformed amid broader greenback strength. South Korea's PPI inflation reached a 13-year high.

- IDR: Spot USD/IDR promptly clawed back its opening losses. Indonesia said it will tighten curbs for the year-end holiday season. Bank Indonesia kept its 7-Day Reverse Repo Rate unchanged on Thursday, in line with expectations.

- MYR: Spot USD/MYR continued to test its 100-DMA, but struggled to stage a clean break above that moving average.

- PHP: The peso traded on a softer footing, after BSP kept its key policy rate on hold, as expected by virtually all analysts.

- THB: Spot USD/THB ticked away from a multi-week low printed on Thursday. The baht has been the best performer in the region this week.

EQUITIES: Hang Seng Struggles On Alibaba Guidance

Equity trade was mixed during Asia-Pac hours.

- Chinese tech names struggled in the wake of a downward revision in Alibaba's '22 outlook. This resulted in underperformance for the Hang Seng, which shed the best part of 2% vs. Thursday's closing levels.

- Elsewhere, the likes of the Nikkei 225, CSI 300 and ASX 200 posted modest gains, aided by an uptick in U.S. e-mini futures, as the S&P 500 and NASDAQ 100 contracts registered yet another round of fresh all-time highs. There wasn't a clear catalyst for the uptick in U.S. e-minis during the Asia-Pac session, with some desks pointing to spill over support from news that tech heavyweight Apple is pushing for the release of a fully autonomous car by 2025.

GOLD: As You Were

Little to really flag for gold, with spot a handful of dollars higher on the day, just shy of $1,865/oz. Our weighted U.S. real yield monitor is essentially unchanged over the last 24 hours, hovering just above the all-time low, with the DXY sitting a touch lower over the same horizon. Nothing has changed from a technical perspective, while the broader inflationary dynamic provides the fundamental focal point.

OIL: Crude Marginally Firmer Alongside E-Minis

WTI & Brent crude futures firmed during the final Asia-Pac session of the week, adding circa $0.50 vs. settlement levels, aided by an uptick in U.S. e-minis. This comes after the benchmarks printed at the lowest levels seen since early October on Thursday, with Brent showing below $80 in the process, before recovering.

- A potential coordinated stockpile release from the U.S. & China continues to dominate news flow in the space. However, Goldman Sachs note that any such move "would 1) only provide a short-term fix to a structural deficit, 2) is now fully priced-in following the $6/bbl move lower in recent weeks (pricing in a release of more than 100mn bbl into OECD stocks), and 3) would not help the slow global supply response that only higher oil prices can overcome. In fact, if such a release is confirmed and manages to keep oil prices depressed in the context of low trading activity into year-end, it would create clear upside risks to our 2022 price forecast."

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.