Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Source reports point to Biden & Manchin restarting BBB reports in the new year.

- That allowed e-minis and Asia-Pac equities to move higher overnight.

- Canadian retail sales data and an address from U.S. President Biden headline the docket on Tuesday.

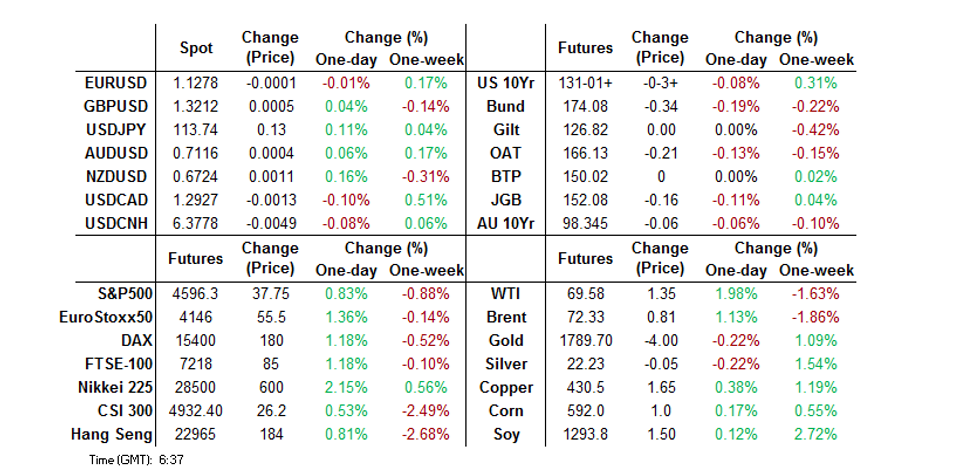

BONDS: Core FI Under Modest Pressure Overnight

An e-mini bid linked to fiscal hope re: U.S. President Biden’s BBB plan (per source reports, pointing to Biden & Senator Manchin conducting discussions on the matter in early ‘22) applied some modest pressure to Tsys overnight, with TYH2 last -0-03 at 131-02, just off the base of the contract’s 0-06 overnight range. Cash Tsys run flat to 0.5bp cheaper across the curve. 20-Year U.S. Tsy supply will provide the focal point of the U.S. docket on Tuesday. Participants also await President Biden’s Tuesday address. White House press secretary Psaki has noted that the speech is 'not about locking the country down,' but it will focus on the vaccination drive.

- A relatively lacklustre morning saw JGB futures edge away from their overnight low, before the broader impetus (which included a ~2% rally in the Nikkei 225) and the Japanese cabinet office’s first upgrade to its main economic assessment since July ’20 applied some pressure during the Tokyo afternoon. Re: the latter, this came after press reports pointed to the potential for a government upgrade re: its FY22 real GDP growth view to 3.0%+ (currently 2.2%), owing to the impact of the well-documented fiscal support package that has been outlined and in recent weeks (formally enacted on Monday). Futures finished -16. Cash JGB trade saw the major benchmarks print little changed to ~1bp cheaper on the day (the 7- to 20-Year zone led the weakness). The latest round of BoJ Rinban operations (covering 1- to 10-Year JGBs) drew offer/cover ratios of 2.7-3.0x times. This didn’t provide any notable impetus for the space

- Aussie bond futures drifted lower in the wake of the release of December’s RBA meeting minutes, with CBA now expecting for the RBA to end its bond purchase scheme in February, as they look for firmer than expected Q4 CPI and labour market data (at least when compared to RBA projections) ahead of the Bank’s February meeting. The uptick in e-minis has also helped apply some pressure to ACGBs. YM -1.0 & XM -6.0 at the bell.

FOREX: Tight Asia Session For G10 FX

The major USD crosses are essentially unchanged on the day at typing, with a lack of meaningful headline flow apparent since the Asia open. U.S. e-mini futures and crude oil ticked higher, aided by source reports pointing to U.S. President Biden & Senator Manchin restarting BBB plan discussions in the new year (these reports hit during late NY hours).

- CAD saw some marginal outperformance in the G10 FX space on the modest uptick In oil, although USD/CAD is only 15 pips lower on the day at typing.

- A weaker than expected PBoC USD/CNY mid-point fixing provided a negligible, short-lived reaction in USD/CNH, although the move was tiny in the broader scheme of things. USD/CNH sits at unchanged levels at typing.

- AUD looked through the release of the RBA’s December meeting minutes.

- The NZD blipped lower on news that omicron has resulted in a delay to the re-opening of New Zealand’s borders, but the kiwi was ultimately aided by an uptick in e-minis. NZD/USD last trades ~10 pips higher on the day. Note that NZD/USD’s YtD low ($0.6702) remained intact after a test of the level on Monday.

- Canadian retail sales data headlines the broader economic docket on Tuesday. Participants also await U.S. President Biden’s Tuesday address. White House press secretary Psaki has noted that the speech is “not about locking the country down,” but it will focus on the vaccination drive.

FX OPTIONS: Expiries for Dec21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1150(E532mln), $1.1200-20(E676mln), $1.1250-70(E889mln), $1.1275-95(E780mln), $1.1315(E527mln), $1.1350(E742mln), $1.1500(E864mln)

- USD/JPY: Y112.70($562mln)

- USD/CAD: C$1.2800-10($524mln)

- USD/CNY: Cny6.40($650mln)

EQUITIES: Equities Off To A Better Start On Tuesday

Risk appetite rebounded a little during Asia-Pac trade, with suggestion’s that President Biden’s BBB plan may not be dead and supportive Chinese policy re: property builders generating most of the attention. The Nikkei 225 led the way higher when it came to the major regional indices, adding ~2% (unwinding yesterday’s underperformance), while e-minis added 0.6-1.0%, with the NASDAQ 100 outperforming.

GOLD: Back Below $1,800/oz

Our weighted U.S. real yield monitor unwound the pressure witnessed during the early part of Monday’s session (on hope that U.S. President Biden’s BBB plan may be rekindled in the early part of ’22), which pushed spot gold back below $1,800/oz. Subsequent Asia-Pac trade has been tight, with consolidation around the $1,790/oz mark, leaving well defined technical lines in the sand in play.

OIL: Crude Edges Further Away From Monday’s Trough

E-minis have nudged higher during Asia-Pac hours, supporting crude futures. WTI & Brent have added $0.60-0.70 vs. their respective settlement levels after a volatile Monday session ultimately saw the benchmarks shed ~$2.00, but finish well off their respective session lows. A reminder that Monday saw risk appetite dented by omicron worry (centring on Europe & the UK) and U.S. Senator Manchin putting President Biden’s BBB plan in jeopardy (note that subsequent reports have suggested that Biden & Manchin will pick up discussions re: that matter in the new year, which has supported risk appetite in Asia). The broader risk dynamic dominated on Monday, with idiosyncratic news flow headlined by RTRS sources flagging an uptick in OPEC+ overcompliance when it comes to the group’s production pact, in addition to Libyan supply headaches. The usual round of weekly API crude inventory estimates will cross later on Tuesday.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/12/2021 | 0700/0700 | *** |  | UK | Public Sector Finances |

| 21/12/2021 | 1100/1100 | ** | | UK | CBI Distributive Trades |

| 21/12/2021 | 1330/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 21/12/2021 | 1330/0830 | * | | US | Current Account Balance |

| 21/12/2021 | 1330/0830 | ** |  | CA | Retail Trade |

| 21/12/2021 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 21/12/2021 | 1500/1600 | ** |  | EU | Consumer Confidence Indicator (p) |

| 21/12/2021 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 21/12/2021 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.