Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Weakness in Hong Kong & Chinese equities (with some starting to question the scope for meaningful easing from the PBoC after stickier than expected Chinese PPI data given the prospect of notably higher commodity prices starting to feed into the dataset imminently) provided some counter to early core fixed income weakness that came on the back of the U.S. putting the coolers of any talk of Polish airforce planes being stationed at one of its German bases (although talks between the two are ongoing, perhaps linked to the stationing of patriot missiles in Poland).

- There isn’t much in the way of notable risk events slated for Wednesday, with U.S. JOLTS job openings perhaps providing the highlight. It will be a case of headline watching, with focus already moving to Thursday’s ECB meeting & U.S. CPI data.

- Headline risk surrounding the Ukraine-Russia meeting in Turkey will be evident.

BONDS: Hong Kong & Chinese Equity Weakness Allows Core FI To Move Off Lows

Weakness in Hong Kong & Chinese equities (with some starting to question the scope for meaningful easing from the PBoC after stickier than expected Chinese PPI data given the prospect of notably higher commodity prices starting to feed into the dataset imminently) provided some counter to early core fixed income weakness that came on the back of the U.S. putting the coolers of any talk of Polish airforce planes being stationed at one of its German bases (although talks between the two are ongoing, perhaps linked to the stationing of patriot missiles in Poland).

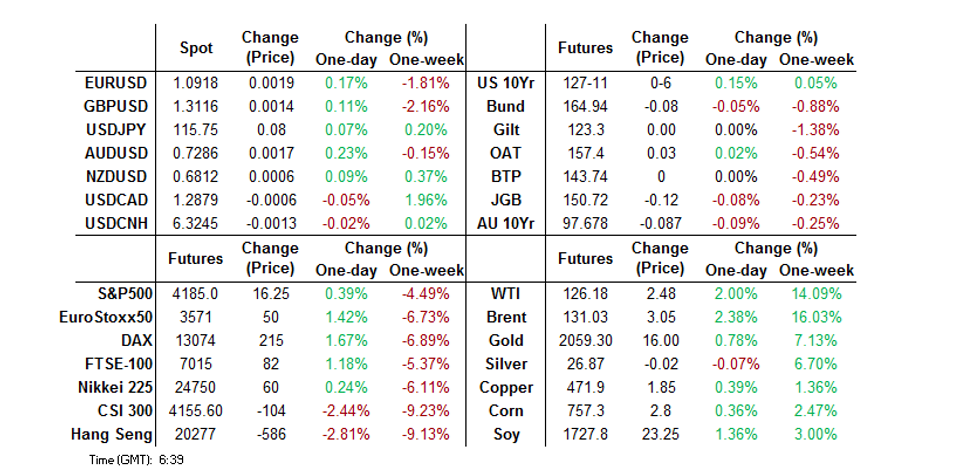

- TYM2 +0-05 at 127-10, while cash Tsys run little changed across the curve. There wasn’t much in the way of wider headline flow to observe in Asia, with a fairly contained 0-08+ range in play in TYM2 on volume of ~85K (paltry by recent Asia-Pac session standards).

- JGB futures consolidated the bulk of their overnight losses but rebounded off of worst levels to close -15. The rebound in futures came alongside a rally in the longer end of the JGB curve, which reversed the early steepening theme (we didn’t see a clear catalyst for this move). Cash JGBs sit little changed to 1.5bp cheaper out to 10s, with 7s underperforming, linked to the weakness in futures. Further out, 20+-Year paper was 1.5-2.5bp richer, with 40s leading.

- Aussie bonds looked through RBA Governor Lowe’s embedding of further optionality in lift off deliberations, with some of the phrasing deployed by Lowe pointing to upside risks in inflation, in addition to no plan when it comes to the timing of the first hike (when questioned on potential inflation scenarios). YM was -7.8 at the bell, ticking lower into the close, while XM was -8.7. IRH2 was marginally higher, while the remainder of the IR strip softened.

FOREX: JPY Brings Up The Rear

The greenback trades a touch lower against the majority of its G10 FX peers. Asia-Pac hours saw the U.S. effectively note that Polish airforce planes would not be welcome at one its German army bases after Poland made an offer to bolster the Ukrainian armory on Tuesday, although talks between the U.S. & Poland are ongoing (perhaps in relation to the potential deployment of patriot missiles to Poland, which was sketched out by U.S. officials on Tuesday).

- The exception to the broader rule was the JPY, which finds itself at the foot of the G10 FX table. A combination of softer than expected final Japanese GDP data, Japan’s susceptibility to higher crude prices, a light uptick in e-minis/local Japanese stocks and talk of importer-related flows in USD/JPY weighed on the JPY. USD/JPY is ~15 pips higher, printing just above Y115.80. The rate showed above initial technical resistance before backing off. Bulls ultimately look to key resistance in the form of the Feb 10 high/Jan 4 high & bull trigger (Y116.34/35).

- EUR/USD managed to add ~25 pips but sticks within the range observed during the first half of the week, printing $1.1925.

- AUD/USD nudged higher on the USD downtick, with nothing in the way of immediate reaction to the latest round of RBA communique. Governor Lowe seemed to embed further optionality into the timing of the Bank’s cash rate lift off, although he continued to point to the RBA’s ability to be patient.

- Chinese inflation data failed to impact the wider G10 FX space, while USD/CNH stuck to a narrow range.

- There isn’t much in the way of notable risk events slated for Wednesday, with U.S. JOLTS job openings perhaps providing the highlight. It will be a case of headline watching, with focus already moving to Thursday’s ECB meeting & U.S. CPI data.

FOREX OPTIONS: Expiries for Mar09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0965(E650mln), $1.1100(E561mln), $1.1300(E1.0bln)

- GBP/USD: $1.3280-00(Gbp603mln)

- AUD/USD: $0.7250-65(A$672mln)

EQUITIES: Mixed As Commodities Push Higher

Major Asia-Pac equity indices are mixed following a negative lead from Wall St., with Hong Kong and Chinese stocks notably under pressure. Most energy and materials stocks across the region have again caught a bid amidst a continued rally in commodities, while high-beta equities fell amidst elevated inflation worry arising from the well-documented U.S. and UK embargoes of Russian crude.

- The ASX200 outperformed, snapping a three-day streak of losses to finish 1.0% higher, although the wider trend was bucked here, with energy names little changed on net, while the tech sector led the rally..

- The Hang Seng sits 2.2% weaker at typing, taking the index to levels not witnessed since Jul ‘16. An address by Hong Kong Chief Executive Carrie Lam mainly re: the city’s worsening COVID-19 outbreak has done seemingly little to sooth investor nerves, with steep declines seen in the Hang Seng’s Commerce & Industry sub-index. China-based tech companies struggled as well, with the Hang Seng Tech Index plunging to another all-time low.

- The CSI300 is 1.3% worse off at writing, with inflation-sensitive healthcare and consumer discretionary stocks leading losses in the index. Chinese PPI slowed in Y/Y terms during Feb (although still topped wider expectations), while the CPI print held steady, below 1.0% Y/Y. Discussions re: the scope for further easing from the PBoC have done the rounds, with the well-documented commodity price surge widely tipped to impact Chinese inflation readings as early as March.

- U.S. e-mini equity index futures deal 0.3% to 0.5% firmer at typing.

GOLD: Slightly Higher In Asia

Gold trades ~$5/oz firmer, printing $2,055.7/oz at typing. The precious metal has backed away from fresh cycle highs made on Tuesday ($2,070.44/oz), although a continued downtick in broader U.S. real yields provides continued support. The real yield dynamic has ultimately pushed bullion higher in recent weeks, with inflationary spillovers from the Russia-Ukraine conflict remaining front and centre.

- To recap, gold closed ~$50/oz firmer on Tuesday, with the move higher facilitated by the U.S. and the UK announcing embargoes on Russian crude imports, heightening concern re: inflationary spillovers. Elsewhere, Europe and Japan continue to debate their own energy sanctions on Russia (although Germany continues to lead opposition against any such measures, given the European reliance on Russian energy flows).

- From a technical perspective, price action over the previous day has seen the precious metal again break several levels of resistance, confirming the bullish underlying trend. Initial resistance is now located at $2,075.47/oz (Aug ’20 all-time high and major resistance), while support sits some distance away at $1,961.2 (Mar 7 low).

OIL: Higher In Asia In Wake Of U.S. & UK Embargoes Of Russian Oil

WTI is +$2.80 and Brent is +$3.60, with both benchmarks operating ~$2 to $3 below Tuesday’s highs at writing. Crude remains strongly bid as worry re: tightness in global supply continues to mix with well-documented aversion of Russian oil amongst traders, while some focus has shifted to progress in the G7’s partially enacted embargo of Russian energy imports.

- To elaborate, the U.S. is banning Russian oil, gas, and coal imports immediately, while the UK will “phase out” Russian crude imports by end-’22, with further measures re: reduction of Russian natural gas imports expected to come later this week. The announcements have come independent of Japan and Europe, with the latter still facing firm, German-led opposition to proposed sanctions on Russian energy products.

- Elsewhere, the latest round of weekly U.S. API inventory estimates crossed late on Tuesday. Reports pointed to a surprise build in U.S. crude stockpiles, while there was a drawdown in gasoline, distillate, as well as hub inventories.

- Looking ahead, U.S. EIA data is due later Wednesday (1530 GMT), with WSJ median estimates calling for a decline in crude, gasoline, and distillate stocks.

- Looking to technical levels, resistance for WTI and Brent is situated at their Mar 7 highs of $130.50 and $139.13 respectively, while support is seen at $105.18 (Mar 2 low) for WTI, and $106.83 (Mar 2 low) for Brent.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/03/2022 | 0900/1000 | * |  | IT | Industrial Production |

| 09/03/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 09/03/2022 | 1500/1000 | ** | | US | JOLTS jobs opening level |

| 09/03/2022 | 1500/1000 | ** | | US | JOLTS quits Rate |

| 09/03/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 09/03/2022 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 09/03/2022 | 1700/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 09/03/2022 | 1800/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.