Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

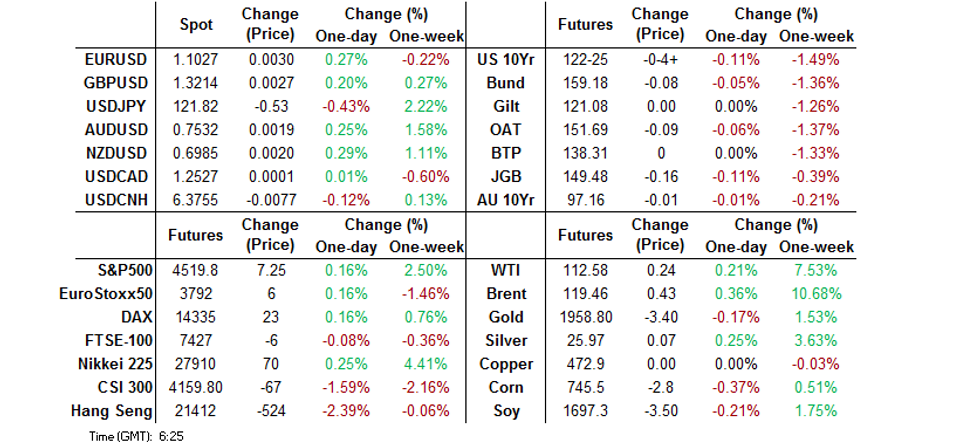

- Asia-Pac hours saw participants buy into Thursday’s U.S. Tsy dip, in the main, with a lack of overt headline flow apparent. Widespread COVID testing in the Chinese city of Shanghai and continued speculation surrounding the Russia-China situation were seen as supportive factors (in what seemed to be an exercise of finding an explainer for a modest bid after equity inspired cheapening into the NY bell), although ranges were tight.

- The yen drew support from the BoJ's inaction with regard to the move above 0.23% in the benchmark 10-Year JGB yield. A break above that level triggered BoJ fixed rate operations back in Feb as the central bank sought to defend the upper end of permitted 10-Year yield trading range (-/+0.25%). There was speculation that the level could again act as a trigger for BoJ intervention but the central bank chose to stay on the sidelines.

- Final U.S. Uni. of Mich. Sentiment, German Ifo Survey & UK retail sales take focus from here. Speeches are due from Fed's Williams, Daly, Barkin & Waller, BoC's Kozicki & Norges Bank's Bache.

BOND SUMMARY: Tsys Flatten A Touch In Asia, JGBs Soften On BoJ Inaction

Asia-Pac hours saw participants buy into Thursday’s dip, in the main, with a lack of overt headline flow apparent. Widespread COVID testing in the Chinese city of Shanghai and continued speculation surrounding the Russia-China situation were seen as supportive factors (in what seemed to be an exercise of finding an explainer for a modest bid after equity inspired cheapening into the NY bell), although ranges were tight. TYM2 sits -0-04+ at 122-05, dealing in the middle of the contract’s 0-07+ overnight range. Volume in the contract is sub-standard, at least in recent terms, running shy of 100K. 2s have cheapened by ~0.5bp, bucking the broader trend, as 30s run ~2.0bp richer on the session, with twist flattening evident. Looking ahead, pending home sales and final UoM sentiment provide the economic readings of note during NY dealing, with Fedspeak from Waller, Williams & Barkin (’24 voter) due.

- BoJ inaction, when it came to the move above 0.23% in 10-Year JGB yields, facilitated further JGB cheapening during the Tokyo morning, although afternoon trade was a little more tepid. The major cash JGB benchmarks were running little changed to ~4bp cheaper late in the day, as 40s provided the weakest point on the curve, resulting in bear steepening. Note that 10-Year JGB yields now sit at 0.24%, 1bp above the trigger point for BoJ fixed rate operations in Feb and 1bp below the top of its -/+0.25% permitted 10-Year JGB yield trading range. JGB futures were 16 ticks lower on the day, but off of worst levels, after registering fresh cycle lows. Technical support in the contract is seen at the 0.5% 10-DMA envelope (149.37), which is now within touching distance. BoJ Governor Kuroda flagged the importance of YCC when it comes to the Bank’s monetary policy operations in his latest Diet appearance, which would suggest that there are no immediate plans to alter the Bank’s permitted 10-Year JGB yield trading range (although he didn’t make direct reference to the current band settings, outside of “trading around 0%”). This seemingly makes it a case of when, not if, the BoJ will act on 10-Year JGB yields, if needs be. He also pointed to no desire to alter monetary policy settings based on cost-push inflation dynamics (a known). Elsewhere, Japanese Finance Minister Suzuki flagged an unveiling of a fiscal support package for some time next week (in line with press speculation).

- Aussie bond futures went out around the middle of their Sydney ranges, YM -1.0 & XM -2.0, with the space back from best levels after drawing support from the previously outlined firm round of ACGB Nov-24 supply and some modest regional demand for U.S. Tsys during early Asia-Pac dealing, allowing a correction from early Sydney troughs. The space looked through next week’s atypical AOFM issuance slate.

JAPAN: International Investors Shed Japanese Assets Last Week

Net international security flows on the part of Japanese investors were limited last week, with the proximity to the end of the current Japanese financial year likely limiting wider activity.

- Elsewhere, foreign investors sold decent clips of Japanese bonds and equities last week. It may have been those that didn’t hedge their FX exposure pulling out of Japanese assets given the recent JPY weakness/fears of an extension of that move.

- In terms of specifics, some may have looked to exit long equity positions after the Nikkei 225’s bounce from the recent trough (although this was the 8th consecutive week of net selling of Japanese equities by foreigners), while the net selling of Japanese bonds may have represented foreign investors looking to test the BoJ’s resolve when it comes to the enforcement of its 10-Year JGB yield trading band (although it came after 2 weeks of heavy net Japanese bond buying on the part of offshore investors).

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -111.8 | -164.4 | -968.8 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 123.5 | -194.6 | 324.7 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | -969.7 | 1337.4 | 1476.5 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -631.4 | -1050.5 | -2994.6 |

FOREX: BoJ Inaction, Demand For Save Havens Throw Lifeline To Embattled Yen

Defensive feel took hold in G10 FX space, even as latest headline flow failed to add much to the familiar picture. Growth proxies such as AUD, NZD and CAD lost ground, with JPY and CHF lodging gains. Demand for safe havens allowed the yen to snap its recent rout, which earlier this week drove USD/JPY through several round figures to fresh multi-year highs.

- The yen drew additional support from the BoJ's inaction with regard to the move above 0.23% in benchmark 10-Year JGB yield. A break above that level triggered BoJ fixed rate operations back in Feb as the central bank sought to defend the upper end of permitted 10-Year yield trading range (-/+0.25%). There was speculation that the level could again act as a trigger for BoJ intervention but the central bank chose to stay on the sidelines.

- Spot USD/JPY pulled back below the Y122.00 mark to a session low of Y121.51 from yesterday's Y122.44 cycle peak. Implied volatilities remained elevated, even as those further out the curve posted marginal downticks.

- Aiding the retreat in USD/JPY was broader greenback weakness. The USD remains among the weakest G10 performers in the lead-up to the London session as lower U.S. Tsy yields bite.

- BoJ's Kuroda said that yen depreciation doesn't mean that the Japanese currency has lost credibility and (together with FinMin Suzuki) underscored the importance of stable FX rates.

- Final U.S. Uni. of Mich. Sentiment, German Ifo Survey & UK retail sales take focus from here. Speeches are due from Fed's Williams, Daly, Barkin & Waller, BoC's Kozicki & Norges Bank's Bache.

FOREX OPTIONS: Expiries for Mar25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1000(E1.6bln)

- USD/JPY: Y119.25($1.0bln)

- AUD/USD: $0.7370-80(A$507mln)

- USD/CAD: C$1.2610-15($517mln)

ASIA FX: Most Asia EM Currencies Edge Higher In Quiet Session

The U.S. dollar showed some weakness towards the end of the trading week in Asia, which resulted in pressure to most USD/Asia crosses.

- CNH: Spot USD/CNH ground lower as broader greenback strength eroded. The PBOC set the yuan reference rate 13 pips above average sell-side estimate, offering no meaningful impetus to the yuan.

- KRW: South Korean won was rangebound, happy to look through confirmation of North Korea's first ICBM test since 2017.

- IDR: Spot USD/IDR traded slightly shy of neutral levels, holding a tight range.

- MYR: Spot USD/MYR retreated, extending its pullback from yesterday's three-month high. Malaysia's CPI unexpectedly slowed to +2.2% Y/Y in February from +2.3% prior, missing median estimate of +2.4%.

- PHP: Spot USD/PHP lost some altitude after the BSP kept benchmark interest rate unchanged Thursday but raised its inflation outlook and said it saw a path toward normalisation.

- THB: Spot USD/THB slipped and moved away from a multi-week high printed Thursday. Softer oil prices, above-forecast customs trade data and potential for further relaxation of Thailand's border rules lent support to the baht.

EQUITIES: Mixed As Chinese Equities Struggle

The major Asia-Pac equity indices are mixed at typing, bucking a positive lead from Wall St. Still, equity indices across the region remain on track to record gains for at least a second week with the exception of the CSI300, as persistent weakness has been observed in Chinese high-beta large caps after the PBoC’s monthly LPR fixings were conducted at unchanged levels on Monday.

- Australia’s ASX200 shrugged off the broader trend of losses, sitting 0.3% better off at the close on outperformance in its materials and energy sub-indices.

- The Nikkei 225 sits virtually unchanged at typing after opening sharply higher, trading on either side of neutral levels, leaving a 7-day streak of gains in the balance. The earlier move lower came as USD/JPY retreated below the Y122.00 mark, with that dynamic weighing after the recent yen weakness boosted hopes re: corporate earnings for Japanese companies. Understandably, outperformance in commodity-related sub-indices was countered by weakness in export-oriented names.

- The Hang Seng underperformed, sitting 2.2% worse off at typing. China-based tech names led losses, with the Hang Seng Tech Index dealing ~4.1% softer after index heavyweight JD.com slipped on the issuance of new shares at a relatively steep discount. Large cap peers such as Tencent and Alibaba struggled for a second day, while Meituan (~-7.0% at writing) has fallen ahead of its earnings beat later on Friday.

- U.S. e-mini equity index futures are flat to 0.2% firmer at typing.

GOLD: Higher As West Expands Sanctions On Russia

Gold is ~$3/oz higher, printing $1,961/oz at typing. The precious metal operates near the top of Thursday’s range as relations (and rhetoric) continues to worsen between Russia and the western powers. Focus now turns to details surrounding an incoming fifth round of EU sanctions on Russia, after the U.S. and UK outlined their latest measures on Thursday.

- To recap, the precious metal closed ~$15/oz higher on Thursday for a second straight day of gains, although an uptick in U.S. real yields helped bullion move away from best levels late in NY dealing.

- On the Russia-Ukraine conflict, NATO has agreed to increase military deployments in the east, while a mobilisation of the alliance’s “chemical, biological, radiological and nuclear defence elements” was also announced, underscoring fears re: potential Russian weapon choices. NATO leaders have so far refused to specify what their response to a Russian chemical/biological attack on Ukraine would be, with U.S. President Biden stating that such an attack would “trigger a response in kind”.

- Looking to technical levels, gold has broken initial resistance at $1,954.7/oz (Mar 15 high), exposing further resistance at $2,009.2 (Mar 10 high).

OIL: Flat As EU Embargo Worry Further Recedes

WTI and Brent are virtually unchanged at typing, struggling to make headway above neutral levels in Asia-Pac dealing. Both benchmarks operate off Thursday’s best levels as expectations for imminent EU sanctions on Russian crude have faded, but remain on track to close higher for the week (after two straight weeks of declines).

- To elaborate, deliberations between EU leaders on Thursday saw familiar opposition re: sanctions on Russian energy. On a related issue, while source reports have highlighted a potential U.S.-EU deal to boost LNG supplies to the latter via the former, near-term measures appear insufficient (RTRS and FT sources say that the agreement is for 15bn cubic metres more LNG from the U.S., against the EU’s current 50bn cubic metres target re: replacement of Russian natural gas imports).

- Elsewhere, RTRS source reports have pointed to a partial resumption in oil loadings from the CPC pipeline (reported on Thursday as having completely halted exports), with a source estimating that exports for CPC Blend crude would be reduced to 800K bpd from 1.4mn bpd.

- Looking to the Middle East, progress towards an Iranian nuclear deal appears to have halted, with Iran’s Foreign Minister saying on Thursday that the U.S. was “wasting time”. On the other hand, U.S. officials have not budged from earlier statements that it is up to Iran to make “difficult decisions”, while emphasising that the U.S. has begun exploring alternatives to the deal.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/03/2022 | 0700/0700 | *** |  | UK | Retail Sales |

| 25/03/2022 | 0800/0900 | *** |  | ES | GDP (f) |

| 25/03/2022 | 0800/0900 | ** | | ES | PPI |

| 25/03/2022 | 0900/1000 | ** |  | IT | ISTAT Consumer Confidence |

| 25/03/2022 | 0900/1000 | *** |  | DE | IFO Business Climate Index |

| 25/03/2022 | 0900/1000 | ** |  | EU | M3 |

| 25/03/2022 | 0900/1000 | ** | | IT | ISTAT Business Confidence |

| 25/03/2022 | 1400/1000 | ** |  | US | NAR pending home sales |

| 25/03/2022 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 25/03/2022 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 25/03/2022 | 1400/1000 | | US | New York Fed's John Williams | |

| 25/03/2022 | 1500/1100 | | US | San Francisco Fed's Mary Daly | |

| 25/03/2022 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 25/03/2022 | 1530/1130 | | US | Richmond Fed's Tom Barkin | |

| 25/03/2022 | 1600/1200 | | US | Fed Governor Christopher Waller | |

| 25/03/2022 | 1645/1245 | | CA | BOC Deputy Kozicki speaks at SF Fed conference on "A world of difference: households, the pandemic and monetary policy" |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.