Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED’S DALY SEES HALF-POINT SEPTEMBER HIKE; NO INFLATION VICTORY (BBG)

- XI SOUGHT TO SEND MESSAGE TO BIDEN ON TAIWAN: NOW IS NO TIME FOR A CRISIS (WSJ)

- SHANGHAI FINDS FIRST COVID CASES IN WEEK; HAINAN STAYS ELEVATED (BBG)

- EU PROPOSES SIGNIFICANT CONCESSION TO IRAN TO REVIVE NUCLEAR DEAL (WSJ)

- UKRAINE RESUMES RUSSIAN OIL FLOWS TO HUNGARY, SLOVAKIA AS BILLS SETTLE (RTRS)

- OIL LEAK CONTAINED AT THREE U.S. GULF PLATFORMS ON PIPELINE OUTAGE, SHELL SAYS (RTRS)

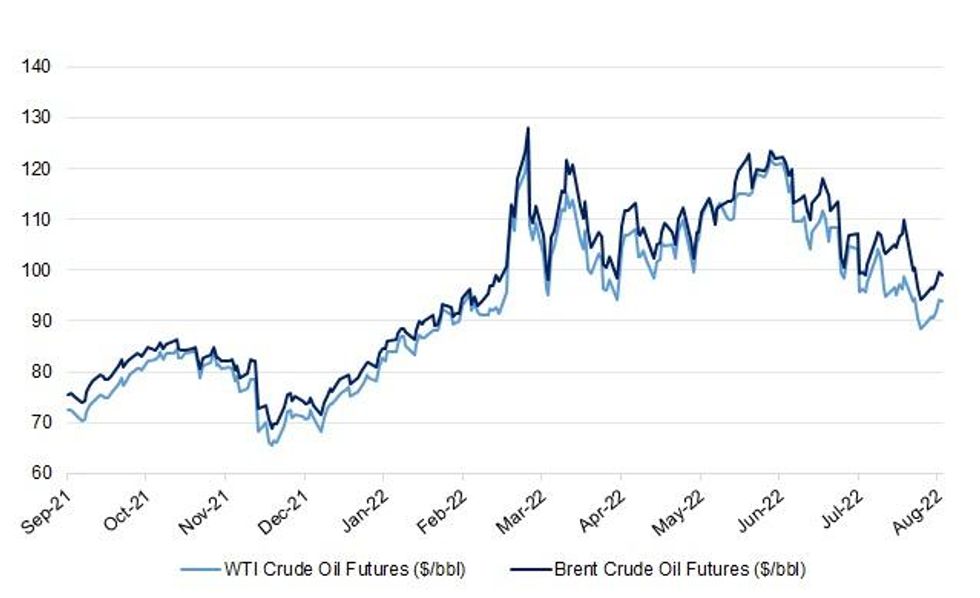

Fig. 1: WTI & Brent Crude Oil Futures

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

POLITICS/FISCAL: Conservative leadership front-runner Liz Truss ruled out fresh windfall tax on energy companies if she becomes prime minister, while her opponent Rishi Sunak vowed to find up to another £10 billion to help Britons pay for soaring power bills. (BBG)

POLITICS: Boris Johnson is taking legal advice over a privileges committee investigation as those close to him accept it is a “foregone conclusion” that he will be found in contempt of parliament. (The Times)

EUROPE

RATINGS: Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Moody’s on Germany (current rating: Aaa; Outlook Stable)

- S&P on Switzerland (current rating AAA; Outlook Stable) and Hungary (current rating: BBB; Outlook Stable)

- DBRS Morningstar on Belgium (current rating AA (high); Negative Trend)

U.S.

FED: The cooler inflation reading for July is welcome news and may mean it’s appropriate for the Federal Reserve to slow its interest-rate increase to 50 basis points at its September meeting, but the fight against fast price growth is far from over, San Francisco Fed President Mary Daly said. (BBG)

POLITICS: In his first public statement since federal agents searched former President Donald Trump's home at Mar-a-Lago earlier this week, Attorney General Merrick Garland on Thursday said that the Justice Department had filed in court a request that the search warrant and property receipt from the search be unsealed. Garland also said he "personally approved the decision to seek a search warrant in this matter." (CNN)

POLITICS: Classified documents relating to nuclear weapons were among the items FBI agents sought in a search of former president Donald Trump's Florida residence on Monday, according to people familiar with the Investigation. (Washington Post)

EQUITIES: Apple Inc. has asked suppliers to build at least as many of its next-generation iPhones this year as in 2021, counting on an affluent clientele and dwindling competition to weather a global electronics downturn. (BBG)

OTHER

U.S./CHINA/TAIWAN: Four days before U.S. House Speaker Nancy Pelosi’s visit to Taiwan, Chinese leader Xi Jinping got on the phone with President Biden and delivered a message: Now isn’t the time for a full-blown crisis. Mr. Xi—who views bringing Taiwan under Beijing’s control as central to his vision of Chinese national revival—was frustrated that months of diplomatic efforts had failed to stop Mrs. Pelosi’s planned trip, according to people close to China’s decision-making process. (WSJ)

JAPAN: Japanese Prime Minister Fumio Kishida said on Friday he will instruct his government to come up with additional measures to cushion the economic blow from rising energy and food prices. (RTRS)

JAPAN: Japanese Prime Minister Kishida's administration continues to haemorrhage support despite this week's reshuffle of Cabinet and the ruling party's executive line-up, opinion polls from Yomiuri Shimbun and Nikkei/TV Tokyo showed. (MNI)

RBNZ: The Reserve Bank of New Zealand (RBNZ) will stick to its hawkish stance and deliver a fourth straight half-point rate hike on Wednesday in its most aggressive tightening in over two decades to try to rein in stubbornly-high inflation, a Reuters poll found. (RTRS)

RBNZ: The RBNZ's quarterly survey of household inflation expectations showed that consumers were no longer anticipating quicker price growth across the forecast horizon. Median perceptions of current inflation as well as 1-year and 2-year out inflation expectations stayed unchanged in the third quarter, while respective means slipped. Both median and mean values of inflation expectations for 5 years ahead fell. (MNI)

MEXICO: Mexico’s central bank boosted its key interest rate to an all-time high after inflation hit the fastest pace in over 21 years, but dispensed with hawkish forward guidance that it had given in its previous decision. (BBG)

BRAZIL: Brazilian state-run oil company Petrobras said on Thursday it will lower refinery gate diesel prices by 4% starting Friday, the second cut in a week, which drew praise from President Jair Bolsonaro. (RTRS)

RUSSIA: United Nations Secretary-General Antonio Guterres said he was “gravely concerned” about the situation unfolding at the Russian-seized Zaporizhzhia nuclear plant in Ukraine, Europe’s largest. (BBG)

IRAN: European Union diplomats trying to break a deadlock in talks over an Iran nuclear accord have proposed a significant new concession to Tehran aimed at speedily ending a U.N. investigation into the Islamic Republic’s past atomic activities. A key sticking point in 16-month-old talks to revive the 2015 deal, which put limits on Iran’s nuclear programs in exchange for sanctions relief, has been a probe by the International Atomic Energy Agency into undeclared nuclear material found in Iran in 2019. (WSJ)

ARGENTINA: Argentina’s central bank raised its benchmark Leliq rate to 69.5%, representing the largest hike in almost three years and signaling a more aggressive stance against surging inflation. (BBG)

PERU: Peru's central bank raised the country's benchmark interest rate by 50 basis points to 6.5% on Thursday, its 13th consecutive hike as the copper-rich nation, along with much of the world, battles persistently high inflation. (RTRS)

OIL: Oil flows have resumed from Russia to Hungary and Slovakia via the Ukrainian section of the Druzhba oil pipeline, Ukraine's Naftogaz said on Thursday, days after being suspended over payment issues. (RTRS)

OIL: The United States on Thursday said nine companies will buy 20 million barrels of oil in the latest sale from the Strategic Petroleum Reserve as part of the Biden administration's efforts to ease petroleum prices elevated by Russia's invasion of Ukraine and thin global spare capacity to boost output. The administration said in March it would release a record 1 million barrels of crude per day from May to October, or about 180 million barrels, from the SPR, which holds oil in caverns on the coasts of Louisiana and Texas. (RTRS)

OIL: Top U.S. Gulf of Mexico oil producer Shell said on Thursday it halted production at three U.S. Gulf of Mexico deepwater platforms after a leak shut two pipelines connecting the platforms, adding it expected pipeline service to resume on Friday. (RTRS)

CHINA

PBOC: The PBOC’s move to deploy small injections via open market operations is a result of less demand from primary dealers amid ample liquidity conditions, not a sign of tightening, the China Securities Journal reported, citing analysts. The PBOC has been injecting just CNY2 billion in seven-day reverse repos on a daily basis since July 27, because the bids submitted by primary dealers have continued to decrease, the newspaper said. Increased fiscal spending, tax rebates and profits turned over by the central bank drove up liquidity supply in the money market in Q2, which left the average DR007 rate at 1.72%. Liquidity will remain loose in August, with a large amount of local government special bonds being allocated by the end of the month, the newspaper said, citing analysts. (MNI)

CREDIT: The interest rates applied to China’s corporate loans may continue to fall as the PBOC is keen to expand credit, while the weakness of the real economy has limited demand for such loans, the 21st Century Business Herald reported, citing analysts. The weighted average interest rate of newly issued corporate loans in June was 4.16%, a record low, the newspaper said, citing Wang Yifeng, analyst at Everbright Securities. For the household sector, the weighted average mortgage rate sat at 4.62% in June, hitting the lowest level observed since 2017, as unfinished housing projects dampened buyers’ confidence, the newspaper said, citing Dai Zhifeng, director at Zhongtai Securities Research Institute. The central bank may guide mortgage rates lower to help boost housing demand, the newspaper said, citing Wang. (MNI)

CORONAVIRUS: Shanghai found its first Covid-19 cases in a week as outbreaks continue to flare around the country, while the resort island of Hainan fell short in its effort to stop transmission by Friday as it disclosed more than 1,000 new infections. The financial hub reported 7 cases for Thursday, the most since July 28, snapping a seven-day streak of zero cases. Hainan recorded 1,209 cases, with most of those in the beachside city of Sanya. (BBG)

CHINA MARKETS

PBOC INJECTS CNY2 BILLION VIA OMOS, LIQUIDITY UNCHANGED

The People's Bank of China (PBOC) injected CNY2 billion via 7-day reverse repos with the rate unchanged at 2.1% on Friday. This keeps the liquidity unchanged after offsetting the maturity of CNY2 billion repos today, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.5723% at 9:36 am local time from the close of 1.3315% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 40 on Thursday vs 43 on Wednesday.

PBOC SETS YUAN CENTRAL PARITY AT 6.7413 FRI VS 6.7324

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 6.7413 on Friday, compared with 6.7324 set on Thursday.

OVERNIGHT DATA

NEW ZEALAND JUL FOOD PRICES +2.1% M/M; JUN +1.2%

NEW ZEALAND JUL BUSINESSNZ M’FING PMI 52.7; JUN 50.0

The key sub index values of Production (49.0) and New Orders (50.5) both improved from June, although the former was still in contraction. While Employment (52.6) rose 1.3 points from June, both Finished Stocks (49.4) and Deliveries (49.4) were in contraction. Also, manufacturers have continued to have a more negative mindset, with the July result showing 62.1% providing negative comments. Although this was down from 68.5% recorded in June, staff retention/shortages and supply chain issues continue to show a strong presence. (BusinessNZ)

SOUTH KOREA JUL EXPORT PRICE INDEX -2.1% M/M; JUN +1.0%

SOUTH KOREA JUL EXPORT PRICE INDEX +16.3% Y/Y; JUN +23.5%

SOUTH KOREA JUL IMPORT PRICE INDEX -0.9% Y/Y; JUN +0.6%

SOUTH KOREA JUL IMPORT PRICE +27.9% Y/Y; JUN +33.6%

MARKETS

SNAPSHOT: Searching For A Definitive Catalyst Into The Weekend

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 up 655.63 points at 28474.96

- ASX 200 down 48.351 points at 7022.60

- Shanghai Comp. down 5.133 points at 3276.532

- JGB 10-Yr future down 5 ticks at 150.28, yield up 0.1bp at 0.191%

- Aussie 10-Yr future down 12 ticks at 96.57, yield up 11.5bp at 3.404%

- U.S. 10-Yr future +0-05+ at 119-08+, yield down 2.73bp at 2.860%

- WTI crude down $0.45 at $93.89, Gold up $1.43 at $1791.16

- USD/JPY up 21 pips at Y133.23

- FED’S DALY SEES HALF-POINT SEPTEMBER HIKE; NO INFLATION VICTORY (BBG)

- XI SOUGHT TO SEND MESSAGE TO BIDEN ON TAIWAN: NOW IS NO TIME FOR A CRISIS (WSJ)

- SHANGHAI FINDS FIRST COVID CASES IN WEEK; HAINAN STAYS ELEVATED (BBG)

- EU PROPOSES SIGNIFICANT CONCESSION TO IRAN TO REVIVE NUCLEAR DEAL (WSJ)

- UKRAINE RESUMES RUSSIAN OIL FLOWS TO HUNGARY, SLOVAKIA AS BILLS SETTLE (RTRS)

- OIL LEAK CONTAINED AT THREE U.S. GULF PLATFORMS ON PIPELINE OUTAGE, SHELL SAYS (RTRS)

US TSYS: A Little Richer In Asia

Tsys richened overnight, with desks flagging an apparent regional interest in fading Thursday’s cheapening & steepening given the lack of overt game changing drivers evident yesterday (with position squaring and block flow-driven moves evident in NY hours, as well 30-Year auction concession/reaction).

- Upside options expressions in the form of FVU2 113.00 & TYU2 119.50 calls aided the direction of travel, as did a couple of rounds of screen lifts in TY futures.

- That leaves TYU2 printing +0-05 at 119-08 ahead of London hours, 0-03 off the peak of its 0-12 Asia-Pac range, although volume isn’t particularly firm, running at ~80K lots.

- Cash Tsys sit 1.5-3.5bp richer across the curve, with 20s leading the rally.

- San Francisco Fed President Daly (’24 voter) reiterated her baseline view of a 50bp hike at the September FOMC, although she once again failed to rule out the idea of a 75bp rate hike, stressing the data-dependent nature of monetary policy alongside a need to assess the inflation and labour market data that will cross between now and then.

- Looking ahead, NY hours will see the latest round of UoM sentiment data (with the inflation expectation components eyed) and Fedspeak from Richmond Fed President Barkin (’24 voter).

JGBS: Twisting Flatter As Tokyo Returns

JGB futures generally tracked the broader impetus in core global FI markets during the morning session as Tokyo participants found their feet after yesterday’s holiday. That was before a slowing of activity in the afternoon session, with liquidity diminished owing to the summer holiday period in Japan.

- That leaves the contract off of its session extremes as we work towards the weekend, -6 vs. Wednesday’s settlement. Wider cash JGB trade has seen the curve twist flatten with the major benchmarks running 1bp cheaper to 2bp richer, pivoting around 10s, after the long end more than reversed its modest, early losses.

- The only real domestic headline flow of note saw Japanese PM Kishida revealing that he plans to hold a meeting to discuss ways to curb inflation, with the gathering set to take place this Monday. Rising food prices and wages will seemingly form the focal points of those discussions.

- As we noted elsewhere, the latest round of Japanese weekly international security flow data revealed that last week saw foreign investors buy more than Y1tn of Japanese bonds in net terms for the fourth time in five weeks, with the latest round of purchases likely representing short covering of existing JGB positions, foreign investors looking to take advantage of FX-hedge-related yield pickups, or a mixture of the two.

- Looking ahead, preliminary Q2 GDP data headlines the domestic docket on Monday, with final industrial production data for June also due.

JGBS AUCTION: Japanese MOF sells Y4.54004tn 3-Month Bills:

The Japanese Ministry of Finance (MOF) sells Y4.54004tn 3-Month Bills:

- Average Yield: -0.1126% (prev. -0.1299%)

- Average Price: 100.0281 (prev. 100.0324)

- High Yield: -0.1042% (prev. -0.1202%)

- Low Price: 100.0260 (prev. 100.0300)

- % Allotted At High Yield: 38.4144% (prev. 46.6848%)

- Bid/Cover: 3.955x (prev. 2.703x)

AUSSIE BONDS: Cheaper, But Off Lows

Aussie bonds are off of session cheaps, as a light bid in U.S. Tsys has helped to pull the space back from session lows. The overnight cheapening in futures that stemmed from Thursday’s bear steepening in the Tsy space gained further momentum as YM & XM registered multi-week lows in early Sydney trade, before the aforementioned move away from worst levels. Cash ACGBs run 7.0-13.5bp cheaper across the curve, bear steepening. YM and XM are -8.5 and -12.0, respectively. Bills run flat to 9 ticks cheaper through the reds.

- The latest round of ACGB Sep-26 supply saw firm pricing, aided by the stabilisation away from cycle cheaps in Aussie bonds, with the weighted average yield printing 1.83bp through prevailing mids (per Yieldbroker). On the other hand, the cover ratio moderated to 2.66x from the previous auction’s 3.40x, coming in far below the six-auction average of 4.03x, with international investors still seemingly sidelined amidst lingering uncertainty re: the degree of tightening that will be executed by the RBA in the current cycle. The slightly higher DV01 on offer from the AOFM this week and the marginal richness of the line in micro-RV terms also provided headwinds, limiting demand at the auction.

- The release of the AOFM’s weekly issuance slate provoked little by way of meaningful reaction in Aussie bonds, seeing a smaller A$1.5bn of ACGBs (with a slight step down in the DV01 from this week’s supply) and A$2.5bn of note supply on offer next week.

- The domestic data docket is virtually empty on Monday, with minutes of the RBA’s Aug policy meeting and CBA household spending data expected to provide the first points of interest on Tuesday.

AUSSIE BONDS: AOFM sells A$700mn of the 0.50% 21 September 2026 Bond, issue #TB164:

The Australian Office of Financial Management (AOFM) sells A$700mn of the 0.50% 21 September 2026 Bond, issue #TB164:

- Average Yield: 3.1722% (prev. 3.2120%)

- High Yield: 3.1750% (prev. 3.2150%)

- Bid/Cover: 2.6643x (prev. 3.4029x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield: 41.5% (prev 42.8%)

- Bidders 37 (prev. 48), successful 13 (prev. 19), allocated in full 8 (prev. 11)

AUSSIE BONDS: AOFM Weekly Issuance Slate

The AOFM has released its weekly issuance slate:

- On Wednesday 17 August it plans to sell A$800mn of the 1.25% 21 May 2032 Bond.

- On Thursday 18 August it plans to sell A$1.0bn of the 21 October 2022 Note, A$1.0bn of the 25 November 2022 Note & A$500mn of the 27 January 2023 Note.

- On Friday 19 August it plans to sell A$700mn of the 2.75% 21 November 2027 Bond.

EQUITIES: Mixed In Asia; Japan Plays Catch-Up

Major Asia-Pac equity indices are mixed at writing on a similar showing from Wall St. on Thursday.

- Suppliers of Apple Inc across Asia were bid as BBG sources have pointed to the U.S. tech giant asking suppliers to produce at least as many next-gen iPhones in ‘22 (~90mn) as in ‘21, with some participants likely watching for similar bids in Europe and U.S. listed suppliers later on Friday.

- Japanese stocks outperformed on their first day back from the holiday on Thursday, experiencing a lift as Japanese participants played catch-up to the recent rally in equities on Wednesday’s better-than-expected U.S. CPI print. Large-caps lead the way higher, with the Nikkei 225 dealing 2.4% firmer at typing, ahead of the broader TOPIX index (+1.8%).

- The CSI300 is 0.2% worse off at typing after a brief show above neutral levels, turning the benchmark away from fresh one-week highs made earlier in the session. Relatively shallow gains across most sectors was countered by losses in consumer discretionary and tech stocks, with the ChiNext index trading 0.9% lower at typing.

- The ASX200 sits 0.7% worse off, backing away from nine-week highs made on Thursday amidst weakness across virtually every sub-index, with healthcare and tech contributing the most to losses (S&P/ASX All Tech Index: -1.5%).

- E-minis deal 0.1-0.3% firmer at typing, operating adrift of their respective multi-month highs made on Thursday.

OIL: A Little Below One-Week Highs

WTI and Brent are ~-$0.50 softer apiece at writing, operating a little below their respective one-week highs made on Thursday. Both benchmarks are on track for a higher weekly close amidst a moderation in demand destruction worry in recent sessions, but remain well short of unwinding last week’s steep selloff, with concern re: tightness in global crude supplies continuing to pull away from recent extremes (Brent’s prompt spread sits at ~$1.27 vs. the ~$2.80 peak witnessed at the beginning of August).

- WTI and Brent closed ~$2 higher apiece on Thursday despite diverging demand forecasts from the International Energy Agency (IEA) and OPEC, with the former highlighting that OPEC+ is unlikely to raise output in the near-term due to severely limited spare capacity, while flagging the potential for further disruptions to Russian crude exports as another risk to supply.

- Turning to the forecasts, the IEA boosted its ‘22 global demand growth projections by 380K bpd while OPEC cut its own ‘22 demand growth forecasts by ~260K bpd later in the session, with the latter also predicting that global oil markets will experience a surplus in Q3 ‘22 on simultaneous supply increases from non-OPEC+ members.

- Elsewhere, crude has also drawn support from news of pipeline and oil & gas field closures in the Gulf of Mexico due to leaks, with Shell expecting the affected pipelines (capacity ~500K bpd of crude) to return to service on Friday, with no timeline given re: restarting production at the fields at writing.

GOLD: Little Changed In Asia; On Track For Higher Weekly Close

Gold sits ~$1/oz weaker, printing ~$1,788/oz at writing. The precious metal operates around the bottom of Thursday’s range at typing, backing away from recently-made five-week highs, but remaining on course to close higher for a fourth consecutive week, drawing support from a continued pullback in the USD (DXY) from cycle highs observed in mid-July.

- While comments from San Fran Fed Pres Daly (‘24 voter) earlier in the session provoked little reaction in gold (with her delivered remarks providing little fresh insight after her FT interview on Thursday), Daly emphasised the need to not get “head-faked” by the recent better-than-expected CPI print, pointing to further employment and inflation data due before the next FOMC due in September.

- Sep FOMC dated OIS now price in ~60bp of tightening, pointing to greater odds of a 50bp hike at that meeting (vs. odds for a 75bp hike), little changed from levels observed a week ago prior to the hot NFP print on Friday.

- From a technical perspective, gold’s recent breach of trendline resistance (~$1,794.6/oz) has signalled a firmer tone for the yellow metal. Initial resistance is located at $1,807.9/oz (Aug 10 high and the bull trigger), while support is seen at $1,754.4 (Aug 3 low, key short-term support).

FOREX: Better Sentiment Keeps Lid On Yen, Supports Antipodeans

The risk switch flicked to on, lending support to the Antipodeans and sapping strength from the yen as the working week in Asia was drawing to an end. Both U.S. Tsys and e-mini contracts found poise amid continued assessment of the outlook for Fed tightening campaign.

- USD/JPY ran as high as to Y133.50 before giving back the bulk of its earlier gains as U.S. Tsy yields lost altitude. Risk reversals crept higher, with one-year skews returning above par. The yen remains the worst G10 performer as risk-on impetus seemingly outweighed slight tightening in U.S./Japan yield gap. Note that there is a notable $1.7bn option expiry with strikes at Y133.98-00 due at the NY cut.

- The kiwi dollar paced gains, setting the tone for the outperformance of commodity-tied FX bloc. The kiwi looked past a quarterly survey which showed that inflation expectations of New Zealand households have stabilised.

- AUD/NZD went offered in line with a move in Australia/New Zealand 2-year swap spread. The spot rate fell to its lowest point in 10 days, with its 100-DMA now within sight. That moving average has remained intact since Dec 2021.

- The sterling traded on a softer footing ahead of the release of UK data which is expected to show that domestic economy slipped into contraction in the second quarter.

- Flash UK GDP & industrial output, Swedish CPI will take focus in European hours, while the American docket is headline by flash U.S. Uni. of Michigan Survey (inflation expectations gauges from that survey will be closely watched). Fed's Barkin will make a TV appearance.

FX OPTIONS: Expiries for Aug12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0185-00(E812mln), $1.0225-30(E639mln), $1.0300(E1.8bln), $1.0325(E800mln), $1.0350(E766mln), $1.0435-40(E521mln)

- USD/JPY: Y132.00($810mln), Y132.45-50($575mln), Y133.98-00($1.7bln)

- GBP/USD: $1.2300(Gbp576mln)

- AUD/USD: $0.7100(A$593mln)

- USD/CAD: C$1.2700($1.3bln), C$1.2800($880mln), C$1.3135-55($1.5bln), C$1.3200($1.1bln)

- USD/CNY: Cny6.80($899mln), Cny6.85($500mln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/08/2022 | 0600/0700 | ** |  | UK | Index of Services |

| 12/08/2022 | 0600/0700 | *** | | UK | Index of Production |

| 12/08/2022 | 0600/0700 | ** | | UK | UK Monthly GDP |

| 12/08/2022 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 12/08/2022 | 0600/0700 | ** | | UK | Trade Balance |

| 12/08/2022 | 0600/0700 | *** | | UK | GDP First Estimate |

| 12/08/2022 | 0600/0800 | *** |  | SE | Inflation report |

| 12/08/2022 | 0645/0845 | *** |  | FR | HICP (f) |

| 12/08/2022 | 0700/0900 | *** |  | ES | HICP (f) |

| 12/08/2022 | 0900/1100 | ** |  | EU | industrial production |

| 12/08/2022 | 1230/0830 | ** |  | US | Import/Export Price Index |

| 12/08/2022 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 12/08/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.