Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- USD/CNH gradually lost altitude overnight and USD/CNY slid under the CNY6.90 mark. The PBOC continued to lean against depreciation impetus via its USD/CNY mid-point fixing, which was set 177 pips below the average sell-side estimate today. This comes on the heels of Tuesday's 249-pip miss, the second-strongest pushback on record.

- U.S. Tsys were tight ahead of the latest round of domestic labour market data.

- Flash Eurozone CPI, the German unemployment rate, U.S. ADP employment report & MNI Chicago PMI, as well as Canadian GDP are set to take focus on the data front. The central bank speaker slate includes Fed's Mester & Bostic and Riksbank's Breman. Finally, the Dallas Fed will hold an event to introduce its new President, Logan.

US TSYS: Marginally Cheaper Overnight, Labour Market Data Eyed

Tsys are little changed into London hours, with a very modest cheapening bias observed during most of the overnight session, while e-minis were bid and the broader USD traded on the defensive. TYZ2 +0-00+ at 117-03, operating in a 0-05+ range on ~60K lots. Cash Tsys print flat to 1bp cheaper across the curve.

- A slightly stronger-than-expected round of official PMI data out of China was seen, although the m’fing reading remained in contractionary territory.

- Rates traders were willing to stay on the sidelines awaiting the latest inputs to gauge the likely size of the Fed’s September rate step.

- A block buyer of TYZ2 futures (+10K, DV01 ~$703K) helped the space away from cheaps during the latter rounds of Asia dealing.

- Looking ahead, the refreshed ADP employment data and the latest MNI Chicago PMI print will hit in NY hours, with Fedspeak from Cleveland Fed President Mester (’22 voter), Atlanta Fed President Bostic (’24 voter) and perhaps new Dallas Fed President Logan (’23 voter) all eyed.

- Ultimately, this week’s broader focus is on Friday’s NFP print, with the Fed stressing its central message ahead of its Sep meeting (debate open re: 50-75bp hike, data-contingent, with ~67bp currently priced by OIS). Tuesday’s JOLTS job opening print presents an upside risk to Friday’s headline NFP reading, but the ADP employment print and ISM m’fing employment component may change perceptions between now and then.

JGBS: Futures Stick To Narrow Range, Curve Comes Under Light Flattening Pressure

JGB futures were confined to the range established during the overnight session during the Tokyo session, after blipping higher at the re-open, dealing at unchanged levels ahead of the bell. Cash JGBs run little changed to 2bp richer on the day, with the curve flattening as 20s lead the bid.

- Firmer than expected domestic data and modest upside surprises in the Chinese official PMI prints likely capped, and then pressured, the space during the Tokyo morning (all at the margins given the narrow ranges).

- The presence of BoJ Rinban operations then provided some offset, with no fresh impetus evident on the back of the movement in the cover ratios observed across the 3- to 25+-Year buckets.

- BoJ board member Nakagawa reaffirmed the Bank’s central stance in her latest address i.e. stressing the need for sustained monetary easing as the Bank looks to facilitate meaningful wage growth to underpin inflation.

- News that Japan will be more than doubling the amount of permitted international travellers from 7 Sep met wider expectations on the back of press reports and had little, if any, impact on JGBs.

- Domestically, Q2 CapEx and the final manufacturing PMI reading are due tomorrow, as is 10-Year JGB supply. The latest round of weekly international security flow data will also receive the usual scrutiny.

AUSSIE BONDS: Early Bid Moderates

Aussie bonds have backed away from their early highs as we have worked our way through the Sydney day, nudging lower after a mix of domestic and international data releases (below-expectations Q2 completed construction, largely in-line private sector credit, and marginal beats in Chinese PMIs), tracking a limited downtick in U.S. Tsys.

- Cash ACGBs run flat to 2.0bp richer across the curve, with 30s leading the way higher.

- YM is +2.5 and XM is +1.0. EFPs have narrowed a little, with the 3-/10-Year box steepening, while Bills run flat to 6 ticks richer across the reds, bull flattening

- The latest round of ACGB Nov-32 supply was absorbed smoothly, with fairly nondescript internal metrics observed.

- CoreLogic house prices for Aug are due ahead of tomorrow’s Sydney session, while Thursday’s data docket will be headlined by Aug final m’fing PMI, Jul housing loan data, and Aug commodity prices.

FOREX: PBOC Continues To Push Back Against Yuan Depreciation, Greenback Loses Ground

The FX space showed a limited initial reaction to China's official PMI figures which printed marginally above the expected levels. Still, e-mini contracts extended their earlier gains and U.S. Tsy yields crept higher as the session progressed, suggesting that the data may have supported market confidence to a degree, even if broader volatility remained subdued.

- USD/CNH gradually lost altitude and USD/CNY slid under the CNY6.90 mark. The PBOC continued to lean against depreciation impetus via its USD/CNY mid-point fixing, which was set 177 pips below the average sell-side estimate today. This comes on the heels of Tuesday's 249-pip miss, the second-strongest pushback on record.

- Yuan strength spilled over into the Antipodeans, pushing the Aussie dollar to the top of the G10 scoreboard. This allowed AUD/USD to claw back some of its Tuesday's losses, when the AUD was the worst performer among major currencies.

- The greenback went offered across the board despite slightly firmer U.S. Tsy yields. The BBDXY held the prior day's range amid the absence of any wide price swings across G10 currency pairs.

- Flash EZ CPI & German jobless rate, U.S. ADP employment report & MNI Chicago PMI, as well as Canadian GDP are set to take focus on the data front.

- The central bank speaker slate includes Fed's Mester & Bostic and Riksbank's Breman. Dallas Fed will hold an event to introduce its new President.

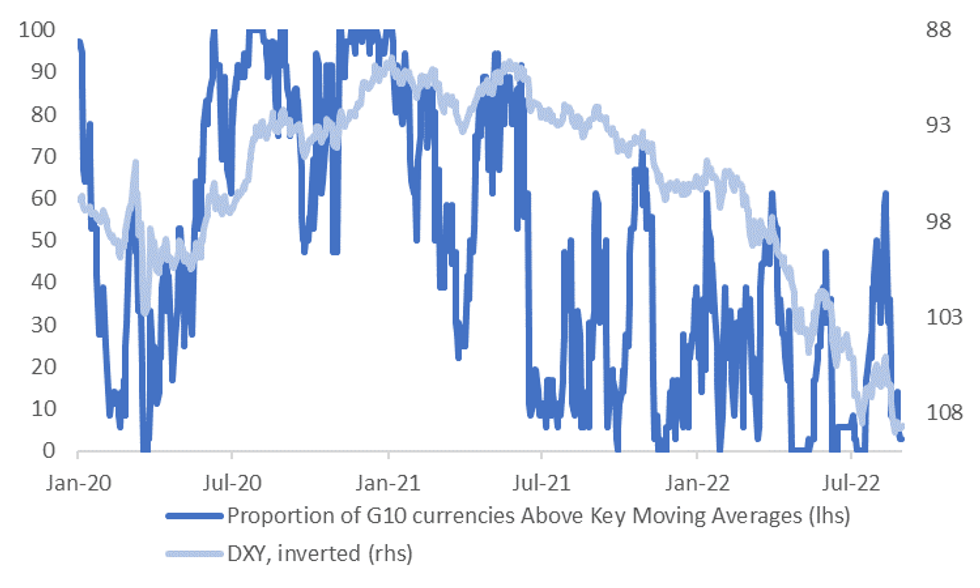

USD: Market Insight: USD Momentum Very Elevated, EUR Likely Key To Any Turnaround

USD momentum remains very strong, at least relative to key moving averages (MA). The first chart below plots the DXY index, which is inverted on chart, against the proportion of G10 currencies which are above key MAs against the USD. This metric looks at whether each G10 currency is above or below its 20, 50, 100 and 200 MA against the USD (see this link for more details on this metric).

- Presently, the G10 currencies only have 1 out of a possible 36 MAs firmer against the USD. This is NOK, which is on the strong side of its 50 day MA.

- Obviously, we are close to the zero bound on this metric, which we have hit on a number of occasions in 2022.

- Interestingly, the DXY has peaked not long after we have hit this zero bound on a number several times this year. This may reflect upside USD momentum running out of steam, or profit-taking flows on long USD positions.

- The exception though was back in late April/early May when the index kept moving higher, although we were at lower levels in the DXY back then compared to now.

- Ultimately shifts lower in the DXY from these peaks have proven to be short lived, before the uptrend resumes once again.

Fig 1: G10 FX Moving Average Momentum & DXY Trend

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

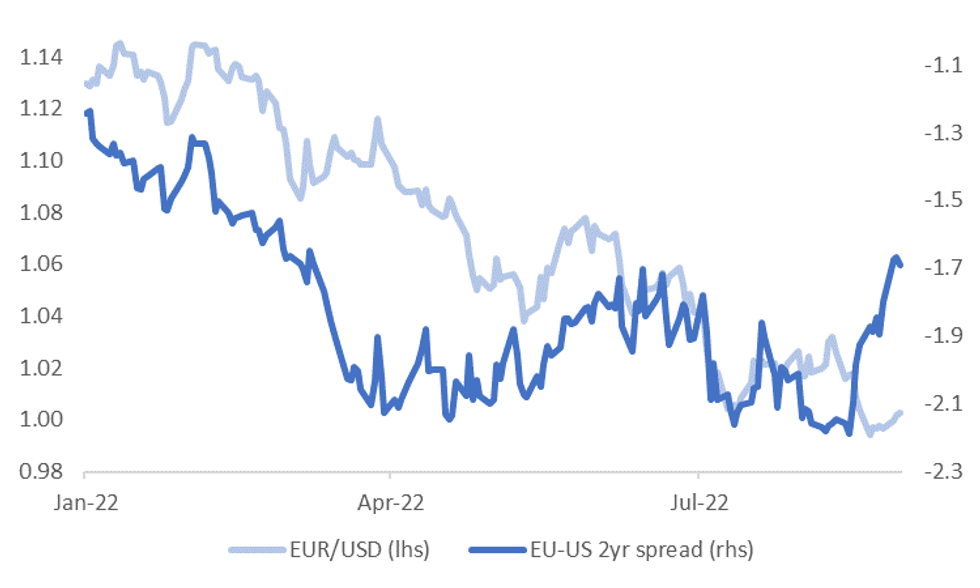

- In the current context, any turnaround in USD momentum is likely to be quite EUR dependent. The euro's weight in USD indices is quite high and correlates well with the rest of the G10 bloc.

- Some macro drivers have turned less bearish for the EUR, at least in a relative sense. The second chart below plots EUR/USD against the 2yr swap spread with the US.

- Outright spreads are still heavily in favor of the USD (-170bps), but momentum has tilted the other way (+50bps from recent lows). It's a similar backdrop for the relative terms of trade, given recent falls in EU gas prices.

- The 20-day MA for EUR/USD comes in at 1.0111 (versus current spot at 1.0040). Also note we have key event risk later today, with the EU CPI due.

Fig 2: EUR/USD & EU-US 2yr Swap Spread

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

AUSTRALIA DATA: Q2 Construction Weakness To Be Slight Drag On GDP

Q2 completed construction work fell sharply, -3.8% Q/Q, sharply undershooting the BBG median estimate of +0.8%.

- This data feeds into the national accounts and is likely to provide a small drag on quarterly GDP growth.

- The weakness was broad-based across residential and non-residential construction.

- Residential building was the weakest component, falling 6.8% Q/Q and 7.6% Y/Y. This was the sharpest quarterly fall since 2000. The sector has been facing bottlenecks via supply-chain issues for materials and a shortage of workers.

- All states saw contractions when it came to completed construction work, particularly WA & Victoria, but both territories still posted strong rises in construction activity.

Source: MNI - Market News, ABS

FX OPTIONS: Expiries for Aug31 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9925(E1.2bln), $1.0000(E1.6bln), $1.0100(E1.8bln), $1.0150-62(E1.2bln)

- USD/JPY: Y136.00($1.5bln), Y137.50($695mln), Y138.00($753mln), Y139.90-00($1.3bln)

- AUD/USD: $0.6785(A$719mln). $0.7089-00(A$1.1bln)

- NZD/USD: $0.6400(N$706mln)

- USD/CNY: Cny6.70($1.2bln), Cny6.80-81($1.1bln), Cny6.90($1.5bln), Cny6.9250($920mln)

ASIA FX: CNH & KRW Rebound

CNH and KRW have rebounded today, which has helped the rest of the region, although THB and IDR have been laggards.

- CNH: USD/CNH is back sub the 6.9000 level. We had another stronger CNY fixing today, relative to market consensus, while official PMI prints came in a touch firmer than expected, although they still suggest economic momentum eased in August. Equities have bucked the broader recovery trend today. Nevertheless, CNH is around +0.40% firmer versus NY closing levels.

- KRW: USD/KRW pushed higher initially but couldn't make much headway above 1350. Domestic data for July was weaker, but didn't impact sentiment a great deal. Onshore equities rebounded from earlier losses, tracking the improved tone in US futures. The Kospi was last at +0.50%. 1 month USD/KRW is back to the 1340 level.

- IDR: IDR has underperformed softer USD sentiment elsewhere. USD/IDR was last at 14848, around +5 figs for the session. Bank Indonesia lowered its GDP outlook for 2023 to +4.5%-5.3% Y/Y from +4.7%-5.5% and warned that inflation may breach the +2.0%-4.0% Y/Y target range. The central bank said it now sees USD/IDR average at IDR14,800-15,200 next year rather than at IDR14,400-14,800.

- THB: The baht is also underperforming. USD/THB was last at 36.40, although we are away from session highs at just under 36.60. Latest comments from Thai officials signalled optimism re: tourism recovery. The government's spokesman said foreign arrivals are expected to be 7.5mn in the second half of the year, generating about THB400bn in revenue. Thai manufacturing production was a little weaker than expected at +6.37%, versus the +8.4% forecast.

- PHP: Spot USD/PHP is slightly lower at 56.145 (-0.08 figs for the session). Factory-gate price growth kept accelerating in July. The latest data from the local statistics authority showed that PPI inflation quickened to +7.9% Y/Y from +7.5% prior. Onshore equities are underperforming, down 1.30% so far today.

EQUITIES: Off Worst Levels; Travel Stocks Rebound

Major Asia-Pac equity indices are mostly off worst levels and sit between 0.1-1.0% softer at writing, with a negative lead from Wall St. waning throughout the session alongside an uptick in e-minis.

- The Hang Seng is 0.4% worse off at writing, back from as much as 1.9% lower earlier, with a sharp reversal in China-based tech (HSTECH: +0.8% from -2.5% earlier) contributing the most to the paring of losses.

- The Chinese CSI300 (-0.6%) was weaker as well, with industrials leading the way lower as official m’fing PMIs pointed to a second straight month of contraction (despite marginally beating expectations).

- The ASX200 is 0.2% softer at writing, with commodity-related sectors providing the most drag in the wake of Tuesday’s fall in commodity prices, offsetting a strong showing from high-beta tech and healthcare equities (S&P/ASX All Tech Index: +1.4%).

- The Nikkei 225 trades 0.4% lower on losses in virtually every sector, with transport-related stocks (airlines and trains) catching a bid on Japanese PM Kishida’s earlier announcement re: the easing of travel restrictions.

- The Taiex (+0.5%) and Kospi (+0.3%) bucked the broader trend of declines, with Korean travel-related stocks leading the way higher as the country announced their own plans to ease COVID measures for travellers, adding to continued outperformance in major exporters.

- E-minis are 0.6-0.7% firmer apiece, working away from their respective, fresh one-month lows made on Tuesday.

GOLD: Little Changed In Asia; $1,720/oz Eyed

Gold is ~$2/oz worse off to print ~$1,722/oz, operating a shade above Monday’s one-month lows at writing. The precious metal has maintained a tight ~$4/oz range in fairly limited Asia-Pac dealing, with no meaningful follow-through from a blip lower on marginal beats in official Chinese PMIs.

- To recap, gold closed ~$13/oz lower on Tuesday, pressured by above-estimate U.S. consumer confidence and JOLTs job openings, adding to worry re: Fed rate hikes amidst hawkish remarks from NY Fed Vice Chair Williams (voter) and Richmond Fed Pres Barkin (‘24 voter).

- Gold is on track for a fifth straight monthly decline, its longest such losing streak in four years with Fed hawkishness in focus, while the Dollar operates at historically elevated levels.

- Sep FOMC dated OIS now price in ~69bp of tightening at that meeting, with the measure returning to the highest levels observed in Aug since the decline in rate hike expectations from the below-expectations U.S. CPI print on Aug 10.

- From a technical perspective, gold remains in a short-term downtrend. Initial support is seen at $1,711.0/oz (76.4% retracement of the Jul21-Aug10 upleg), with further support situated at $1,700.0/oz (round number support). On the other hand, initial resistance is located at ~$1,765.5/oz (Aug 25 high).

OIL: Off Tuesday’s Lows; U.S. Inventories In Focus

WTI and Brent are ~$0.90 firmer apiece, working away from their respective one-week lows observed on Tuesday, but ultimately coming nowhere near to unwinding yesterday’s losses at writing.

- To recap, both benchmarks closed >$5 lower apiece on Tuesday, falling by the most in a month amidst an easing in supply-related worry from their extremes, with hawkish language from Fed and ECB officials fuelling concerns re: economic slowdowns on tighter central bank policy.

- To elaborate on the former, worry surrounding a disruption to Iraqi oil supplies (OPEC’s second largest producer) has eased, with officials stating on Tuesday that operations have been unaffected. Elsewhere, fresh unrest in Libya has also seen no impact on crude production so far.

- U.S. API inventory estimates on Tuesday saw reports point to a relatively small, surprise build in crude stockpiles (coming after large drawdowns were reported over past two weeks), with declines observed in gasoline, distillate, and Cushing Hub stocks.

- Looking ahead, EIA inventory estimates are due, with BBG median estimates calling for a modest decline in crude stockpiles. A note that average diesel prices in the U.S. have returned to above $5/gallon, pointing to possible further tightness in already-low distillate inventories.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 31/08/2022 | 0645/0845 | *** |  | FR | HICP (p) |

| 31/08/2022 | 0645/0845 | ** | | FR | PPI |

| 31/08/2022 | 0645/0845 | *** | | FR | GDP (f) |

| 31/08/2022 | 0645/0845 | ** | | FR | Consumer Spending |

| 31/08/2022 | 0755/0955 | ** |  | DE | Unemployment |

| 31/08/2022 | 0900/1100 | *** |  | IT | HICP (p) |

| 31/08/2022 | 0900/1100 | *** |  | EU | HICP (p) |

| 31/08/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 31/08/2022 | 1200/0800 | | US | Cleveland Fed's Loretta Mester | |

| 31/08/2022 | 1215/0815 | *** | | US | ADP Employment Report |

| 31/08/2022 | 1230/0830 | *** |  | CA | CA GDP by Industry and GDP Canadian Economic Accounts Combined |

| 31/08/2022 | 1345/0945 | ** | | US | MNI Chicago PMI |

| 31/08/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 31/08/2022 | 2200/1800 | | US | Dallas Fed's Lorie Logan | |

| 31/08/2022 | 2230/1830 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.