Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED’S BOSTIC WANTS RATES ON HOLD UNTIL END 2024 - MNI

- US CURVE INVERSION DEEPENS TO ONE PERCENTAGE POINT AFTER POWELL - BBG

- WATCH TRADE-OFF ON POLICY CHANGES - BOJ NOGUCHI- MNI BRIEF

- TREASURER TO NAME NEXT RBA GOVERNOR IN JULY - MNI BRIEF

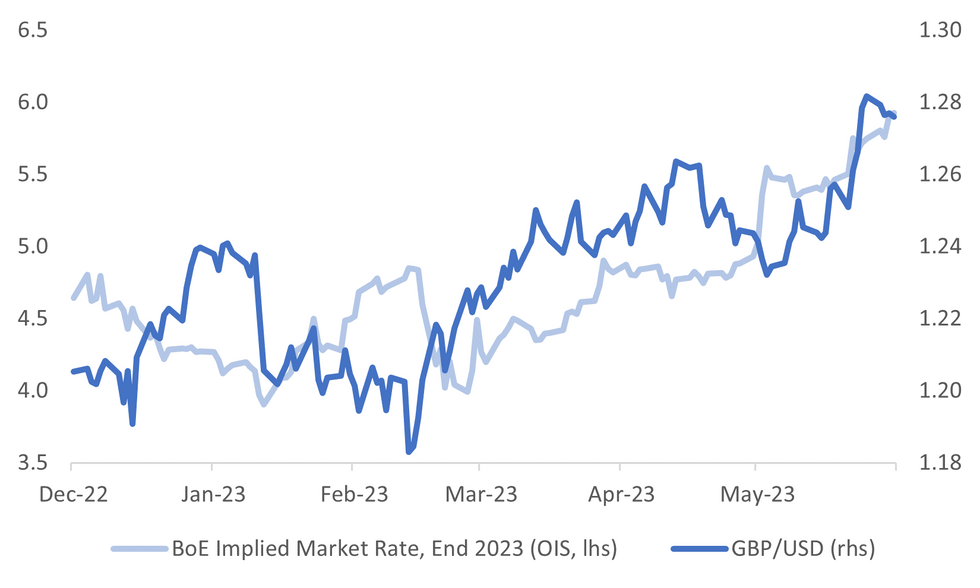

Fig. 1: GBP/USD & End Year BoE Market Implied Rate (OIS)

Source: MNI - Market News/Bloomberg

U.K.

HOUSING: Prime Minister Rishi Sunak faces mounting pressure from members of his Conservative Party to help Britons struggling with surging mortgage costs, amid fears that the UK’s sticky inflation and skyrocketing interest rates will cost them their seats in the next general election. (BBG)

EUROPE

UKRAINE: Ukraine has recruited the help of a top White House adviser to meet with officials from nations that have stayed on the sidelines of the war in Ukraine, the Financial Times reported on Wednesday. National Security Advisor Jake Sullivan is expected to join Ukraine’s effort to sway various countries, according to the FT. The newspaper said the meeting will take place in Denmark over the weekend and participants may include representatives from countries such as India, Brazil, South Africa and Turkey. (FT)

UKRAINE: President Volodymyr Zelenskiy was quoted on Wednesday as saying progress in Ukraine's counteroffensive against Russian forces was "slower than desired", but Kyiv would not be pressured into speeding it up. (RTRS)

SNB: Swiss National Bank in its Financial Stability Report says there are three observations from Credit Suisse crisis that are particularly relevant from its perspective: (BBG)

U.S.

FED: (MNI) WASHINGTON - Federal Reserve Bank of Atlanta President Raphael Bostic told MNI Wednesday he's prepared to hold interest rates at current 15-year highs through the end of 2024, but would be willing to support additional monetary tightening if inflation proves more stubborn than he expects. "I have our fed funds rate at the level it is right now to the end of the year and then staying at that level for all 2024 as well," he said about his contribution to the June Summary of Economic Projections released last week. (MNI)

FED: Bond investors’ concern over a potential US recession deepened after Federal Reserve Chair Jerome Powell signaled policymakers may keep pushing interest rates higher. Yields on two-year Treasuries exceeded those on 10-year notes by as much as one percentage point on Wednesday after short-term rates climbed following Powell’s testimony in Congress. The two-10 segment of the yield curve — which has inverted before each of the past five US recessions — is now the most inverted since March. (BBG)

OTHER

JAPAN: (MNI) TOKYO - Asahi Noguchi, Bank of Japan board member, said Thursday the BOJ should consider the trade-off between easy-policy effects and restoring market function when changing the range of the long-term policy interest rate. Noguchi, a dovish board member, maintained a cautious price view, saying the possibility is high that the y/y rise in core CPI will fall below 2% after temporary cost-push factors wane. “The BOJ must carefully ascertain whether the norm [prices and wages do not rise and inflation remains low] will change or not for the time being,” Noguchi told business leaders in Naha City. (MNI)

JAPAN: Goldman Sachs Group Inc. lifted its targets for Japanese stocks after the market soared this year amid expectations for corporate reforms and solid fundamentals relative to overseas markets. The Topix may reach 2,500 in 12 months, analysts including Kazunori Tatebe wrote in a June 21 report, raising their forecast from 2,200. That implies an 8.9% upside from Wednesday’s close. (BBG)

AUSTRALIA: (MNI) Sydney - Australian Treasurer Jim Chalmers will name the future Reserve Bank of Australia Governor in July. Speaking to local media, Chalmers said he was consulting with cabinet colleagues and wanted to finalise a decision in the coming weeks. The treasurer would not confirm whether he would reappoint Governor Philip Lowe, whose term ends September. (MNI)

AUSTRALIA: Australian Treasurer Jim Chalmers is expected to announce a decision in July on the governor of the Reserve Bank, with incumbent Philip Lowe’s current seven-year term due to expire in less than three months. “This is a big job and it’s a big call,” Chalmers told Australian Broadcasting Corp. radio on Thursday. “I’m in the process right now of consulting with my cabinet colleagues and with others as well. I’m aiming to make an announcement in July but certainly by the time the parliament returns.” (BBG)

NZ: New Zealand house sales rose from a year earlier for the first time in two years, adding to signs the nation’s property market is finding a floor. Sales rose 7.5% in May from a year earlier to 5,959, CoreLogic New Zealand said Thursday in Wellington. That arrested a series of double-digit slumps extending back into 2021. (BBG)

INDIA: The Biden administration will make it easier for Indians to live and work in the United States, using this week's state visit by Prime Minister Narendra Modi to help some skilled workers enter or remain in the country, according to three people familiar with the matter. (RTRS)

INDONESIA: Most Indonesians will get to enjoy a five-day weekend at the end of the month after the government announced extra holidays in a bid to boost travel and consumption. President Joko Widodo declared June 28 and 30 as collective leave days around the Eid al-Adha holiday on June 29, effectively giving Indonesians an extended break. The leave days apply to all civil servants, with companies usually following suit by giving their employees time off. The stock exchange will be shut on those days. (BBG)

CHINA

YUAN: Society for Worldwide Interbank Financial Telecommunication says in an emailed statement. The renminbi ranked as fifth most widely used currency for global transactions, the same as last year. (BBG)

YUAN: There is no basis for the Chinese currency to depreciate significantly and the yuan will be supported as the government implements policies to bolster an economic recovery, according to a commentary in the official Economic Daily on Thursday. (BBG)

US/CHINA: A U.S. Coast Guard ship sailed through the Taiwan Strait on Tuesday , the U.S. Navy's 7th Fleet said on Thursday, transiting the sensitive waterway a day after U.S. Secretary of State Antony Blinken completed a rare visit to Beijing. (RTRS)

OVERNIGHT DATA

NZ MAY EXPORTS NZD 6.99bn; PRIOR 6.61bn

NZ MAY IMPORTS NZD 6.95bn; PRIOR 6.37bn

NZ MAY TRADE BALANCE NZD 46mn; PRIOR 236mn

NZ MAY TRADE BALANCE 12Mth YTD NZD -17119mn; PRIOR -17017mn

CHINA MAY SWIFT GLOBAL PAYMENTS CNY 2.54%; PRIOR 2.29%

MARKETS

US TSYS: Little Changed, Narrow Range, Awaits BoE Decision & Chair Powell 2.0

TYU3 is currently trading at 113-08+, -1+ versus NY closing levels, after trading in a narrow range in Asia-Pac trade.

- Cash US tsys are little changed across major benchmarks.

- With the Asian calendar light, local participants are likely on headlines watch ahead of the BoE policy decision and Fed Chair Powell’s reappearance at Senate Banking Committee later today.

- According to Bloomberg Economics, A string of hotter-than-expected pay and inflation data has raised the chances that the BoE delivers a 50bp hike at its June meeting. The baseline view is that the central bank will err on the side of gradualism, given the ground covered to date, and opt for a smaller move with a hawkish message in the minutes of the meeting. (See link)

JGBS: Richer After Smooth Digestion Of 5-Year Supply, CPI Tomorrow

JGB futures are trading on a high note in Tokyo afternoon trading, +11 compared to settlement levels, after 5-year supply goes well with the auction low price aligning with dealer expectations, the tail decreasing and the cover ratio improving to 3.850x compared to 3.703x in the previous month's auction.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined weekly investment flow data and speech by BoJ Board Member Asahi Noguchi. (See link, ICYMI)

- With the local calendar thin today, local participants have likely been on headlines and US tsys watch.

- Cash US tsys are flat to 1bp cheaper across benchmarks in Asia-Pac trade with TYU3 dealing at 113-07+, -2+ versus NY closing levels.

- Cash JGBs are richer in afternoon trading with a twist flattening of the curve, pivoting at the 2-year zone. The benchmark 10-year yield is 0.8bp lower at 0.374%, below the BoJ's YCC limit of 0.50%.

- The 5-year JGB remains unchanged after the auction, hovering near the lower end of the morning's range at 0.072%, a decrease of 0.3bp for the day.

- Swap spreads are generally wider beyond the 1-year zone.

- The local calendar tomorrow sees the release of May CPI along with the Jibun Bank PMI data.

- Tomorrow will also see BoJ Rinban operations covering 1- to 25-Year JGBs.

AUSSIE BONDS: Twist Flattening, Off Bests, Focus On BoE & Chair Powell’s Testimony

ACGB futures curve has twist flattened (YM -3.0 & XM +2.0) with pricing notably below the highs observed earlier in Sydney trading. Given the relatively light local calendar, it appears that the trading activity has been influenced by the weakening observed in US tsys during the Asia-Pac trading session.

- Cash ACGBs are 2bp cheaper to 2bp richer with the 3/10 curve flatter and the AU-US 10-year yield differential 1bp wider at +23bp.

- The 3s10s swap curve twist flattens with EFPs little changed.

- The bills strip bear flattens with pricing -6 to -1.

- RBA-dated OIS pricing is 4-6bp firmer for meetings beyond September. Terminal cash rate expectations sit at 4.57%.

- The local calendar is light tomorrow with Judo Bank PMI Preliminary data as the highlight. The next major data is the release of the CPI Monthly for May next Wednesday.

- Ahead of that, market participants are likely to be watching global bond yields as they navigate the BoE policy decision and Fed Chair Powell’s reappearance at Senate Banking Committee later today.

- The US is also slated to release weekly Jobless Claims, May Chicago Fed Activity Index and June Kansas City Fed Index.

NZGBS: Weaker But Off Cheaps After Solid Digestion Of Weekly Supply

NZGBs closed 4-5bp cheaper but off session cheaps after today’s weekly auction covering the May-30, Apr-33 and Apr-37 NZGB lines shows solid demand with the respective cover ratios printing 4.10x, 4.93x and 3.98x. In post-auction trading, these cash lines closed 2-3bp lower in yield.

- Nonetheless, NZGBs have underperformed the $-bloc with NZ/US and NZ/AU 10-year yield differentials both 5bp wider.

- Swap rates are 2-4bp higher with implied swap spreads tighter.

- RBNZ dated OIS pricing is flat to 4bp firmer across meetings with Feb’24 leading.

- The May trade surplus narrowed to NZ$46mn from a downwardly revised NZ$236mn. This left the YTD deficit slightly wider at NZ$17.12bn from NZ$17.02bn. Good exports rose 2.8% y/y and imports +4.4% y/y.

- The RBNZ released research on the importance of inflation expectations when forecasting the CPI. It finds that its headline inflation projections are more accurate when expectations are included and that the 1-year mean household inflation expectations have the best forecasting power. (See link)

- The local calendar is light tomorrow.

- Later today sees the BoE policy decision, with a 25bp hike expected, ahead of Fed Chair Powell’s reappearance at Senate Banking Committee.

FOREX: USD Index Back To Session Highs, AUD/JPY Dips

The BBDXY sits a touch above NY closing levels from Wednesday, last at 1222.80, with dips today under 1222 supported. Commodity was firmer in early trade, but has given up gains, particularly on crosses like AUD/JPY. Cross asset signals have been muted, with US yields little changed, while US equity futures are down a touch. Regional equities are mixed in holiday impacted markets, with China and Hong Kong both out today.

- AUD/USD couldn't sustain earlier gains above 0.6800. The pair last tracks 0.6770/75, around 0.35% weaker versus NY closing levels from Wednesday. Local equities are underperformers (the ASX 200 off 1.6%), although we have seen iron ore firm by around 1%. AUD/JPY is down around 0.50%, last back under 96.00, after earlier highs above 96.50.

- NZD/USD couldn't get above 0.6220 and now sits back at 0.6200, slightly down for the session. Earlier May trade figures showed a small surplus as exports to China continued to recover.

- USD/JPY is tracking slightly lower, last around session lows at 141.65/70. Slight risk off in the commodity FX space likely helping at the margins. BoJ board member Noguchi struck a familiar tone in a speech today, saying the bank is showing a strong commitment to easing and that 2% inflation expectations are not anchored yet.

- EUR/USD is steady around 1.0990, while GBP/USD is down a touch to 1.2760.

- Later, the BoE, Norgesbank and SNB decisions are announced. All three are expected to hike rates by 25bp. Also Fed Chair Powell appears before the Senate Banking Committee and the Fed’s Waller, Bowman, Mester and Barkin speak. There is US Chicago & Kansas indices, jobless claims and existing home sales.

EQUITIES: Mixed Trends In Holiday Impacted Markets

Regional equity markets are mixed today. China and Hong Kong markets are out, which has no doubt reduced liquidity and broader regional participation. Japan shares are mixed, although Goldman's upgraded its Topix target. US futures are a touch lower, with Eminis back closer to 4407, while EU futures are tracking lower.

- Goldman's raised the Topix target to potentially reach 2500 in the next 12 months. That compares with current levels around 2307. The bank cited expectations of corporate reforms and better fundamentals to offshore markets. IT services and electrical machinery are the preferred sub-index overweights.

- The Topix is a little over +0.60% firmer at this stage, while the Nikkei 225 is -0.50%.

- The Kospi is tracking higher in South Korea, last +0.50% higher, despite negative tech leads in US trade on Wednesday.

- The ASX 200 is down sharply, off 1.56%, as material stocks underperform. Bank stocks are also weaker.

- Most bourses in SEA are weaker, with PSEi down 0.55% and 10% off Jan highs. The Philippines has been weighed by planned tax changes to the food and beverages sector.

- Indian shares are a touch higher in early trade, looking to continue he recent run of outperformance, as Modi's visit to the US spurs hope of fresh investment flows.

OIL: Crude Down Slightly Ahead Of More Fed Speakers

Oil prices are down slightly during APAC trading after rising around 1.5% on Wednesday. WTI is 0.3% lower at $72.30/bbl, close to the intraday low of $72.26. Brent is also down 0.3% to $76.88 after a low of $76.83. The USD index has moved sideways.

- Official EIA data is published later today. Bloomberg is reporting API measured US crude stocks fell 1.2mn barrels in the latest week according to sources familiar with the data. Gasoline rose 2.9mn but distillate fell 0.3mn. Prices eased slightly following the data.

- The market remains nervous about the demand outlook but has become tentatively more optimistic following some Chinese stimulus and the June Fed pause. FOMC chair Powell noted that some tightening will probably be needed but other members sounded more dovish.

- Later the BoE, Norgesbank and SNB decisions are announced. All three are expected to hike rates by 25bp. Also Fed Chair Powell appears before the Senate Banking Committee and the Fed’s Waller, Bowman, Mester and Barkin speak. There is US Chicago & Kansas indices, jobless claims and existing home sales.

GOLD: Fed Chair Powell's Testimony Weighs On Bullion

Gold is little changed in the Asia-Pac session. In the previous session, it experienced a slight decline of 0.2% and closed at 1932.55 following Fed Chairman Powell's semi-annual testimony to Congress.

- During his testimony, Powell reiterated the key points discussed in last week's hawkish hold. He emphasised that the decision to maintain interest rates at their current level, which marked the first time since March 2022, was a reflection of the significant progress made in a relatively short period. Powell further stated that future decisions regarding interest rates will be approached on a meeting-by-meeting basis.

- Gold has been negatively affected by the expectation of further monetary tightening from both the US Federal Reserve and the ECB, following their recent meetings.

- Additionally, the recent strengthening of the US dollar has dampened demand for gold, further impacting its performance.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/06/2023 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 22/06/2023 | 0730/0930 | *** |  | CH | SNB PolicyRate |

| 22/06/2023 | 0800/1000 | *** |  | NO | Norges Bank Rate Decision |

| 22/06/2023 | 0800/0400 |  | US | Fed Governor Chris Waller | |

| 22/06/2023 | 0915/1115 |  | EU | ECB Panetta Speech at Buba/ECB/Chicago Fed Conference | |

| 22/06/2023 | 1100/1200 | *** |  | UK | Bank Of England Interest Rate |

| 22/06/2023 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 22/06/2023 | 1100/1200 | *** | | UK | Bank Of England Interest Rate |

| 22/06/2023 | 1230/0830 | ** | | US | Jobless Claims |

| 22/06/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 22/06/2023 | 1230/0830 | * | | US | Current Account Balance |

| 22/06/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 22/06/2023 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 22/06/2023 | 1400/1000 | | US | Fed's Michelle Bowman, Loretta Mester | |

| 22/06/2023 | 1400/1000 | | US | Fed Chair Jerome Powell | |

| 22/06/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 22/06/2023 | 1430/1630 | | EU | ECB de Guindos at Financial Journalists' Roundtable | |

| 22/06/2023 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 22/06/2023 | 1500/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 22/06/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 22/06/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 22/06/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 22/06/2023 | 1900/1500 | | US | Atlanta Fed's Raphael Bostic | |

| 22/06/2023 | 2030/1630 | | US | Richmond Fed's Tom Barkin | |

| 23/06/2023 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.