Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- CHINA CONSUMPTION KEY TO GROWTH - ADVISOR - MNI INTERVIEW

- VP HARRIS URGES HAMAS TO AGREE TO AN IMMEDIATE CEASEFIRE, PUSHES ISRAEL ON AID TO GAZA - RTRS

- TRUMP WINS CONTESTS IN THREE STATES IN PUSH TO GOP NOMINATION - BBG

- OPEC+ EXTENDS OIL CUTS, WITH RUSSIA BOLSTERING ITS EFFORT - BBG

- JAPAN TO CONSIDER CALLING OFFICIAL END TO DEFLATION, KYODO SAYS - KYODO

- JAPAN Q4 CAPEX UP Q/Q; GDP SEEN REVISED HIGHER - MNI BRIEF

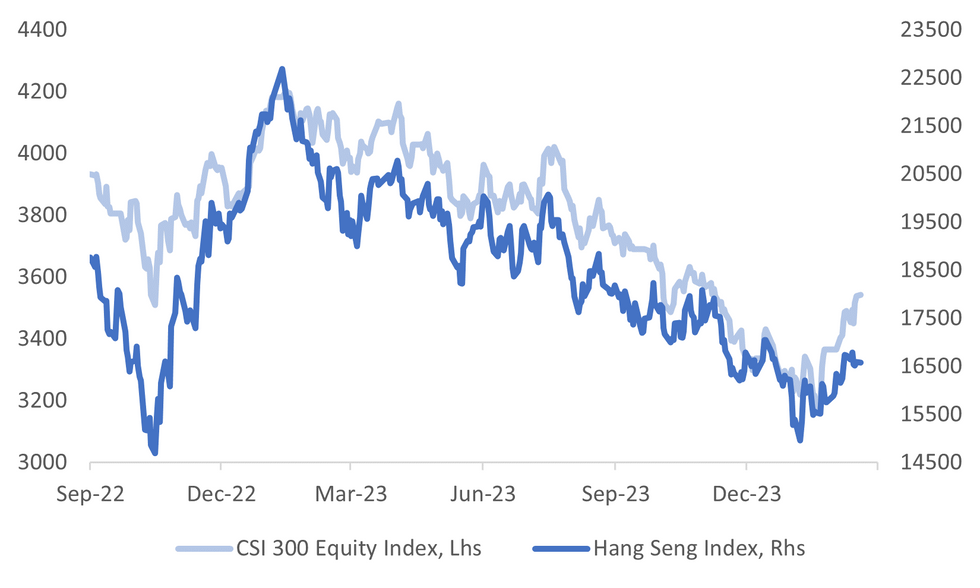

Fig. 1: China's CSI 300 Index & Hong Kong's HSI

Source: MNI - Market News/Bloomberg

U.K.

FISCAL (BBC): Chancellor Jeremy Hunt has said he wants to move towards lower taxes, but will only do so in "a responsible way". He told the BBC it would be "unconservative" to cut taxes by increasing borrowing. Mr Hunt is under pressure from some Tory MPs to reduce taxes in Wednesday's Budget, ahead of an election which must be held by the end of January.

FISCAL (BBG): Chancellor of the Exchequer Jeremy Hunt announced new funding to support the UK’s manufacturing sector, ahead of his budget Wednesday that he said would focus on long-term growth.

EUROPE

GERMANY/RUSSIA (POLITICO): Russia used the leak of a confidential call between top German military officers as part of an "information war" to destabilize the country, Germany's Defense Minister Boris Pistorius said Sunday.

FRANCE (BBG): Marine Le Pen kicked off her campaign for the European parliament elections attacking President Emmanuel Macron’s plan to reform the labor market, saying the French people would pay the price.

TURKEY (ECONOMIST): The country’s base interest rate is now 45%. But as data released on Monday are expected to reveal, government handouts have blunted the impact of the hikes. Economists polled by Reuters expect annual inflation to have reached 65.7% in February, up from 64.9% in the preceding month.

U.S.

US/MIDEAST (RTRS): U.S. Vice President Kamala Harris on Sunday demanded Palestinian militant group Hamas agree to an immediate six-week ceasefire while forcefully urging Israel to do more to boost aid deliveries into Gaza, where she said innocent people were suffering a "humanitarian catastrophe."

POLITICS (BBG): Former President Donald Trump swept three more Republican presidential nominating contests on Saturday, beating rival Nikki Haley in Missouri and Idaho and winning all of Michigan’s remaining delegates.

POLITICS (BBG): Lisa Murkowski and Susan Collins backed Nikki Haley’s bid for the White House, delivering the long-shot Republican contender her first endorsements from sitting US senators days before voters hit the polls on Super Tuesday.

FISCAL (BBG): US congressional leaders revealed a detailed agreement to keep large parts of the government operating through Sept. 30 as they sprint to avert another shutdown deadline at the end of the week.

US/CHINA (RTRS): A measure in the U.S. funding legislation unveiled by congressional leaders on Sunday would block China from buying oil from the Strategic Petroleum Reserve. The desire for a hard line on China is one of the few truly bipartisan sentiments in the deeply divided U.S. Congress, and lawmakers have introduced dozens of bills seeking to address competition with China's government.

EQUITIES (BBG): Bank of America Corp.’s Savita Subramanian is the latest equity strategist to ratchet up her target for the S&P 500 Index to among the highest on Wall Street after this year’s rally left forecasters blindsided.

FED (MNI BRIEF): Federal Reserve Governor Adriana Kugler on Friday said the recovery of the economy's supply side significantly contributed to the disinflation so far, and she remains sanguine about the prospects of a soft landing.

ECONOMY (MNI INTERVIEW): The U.S. factory sector is on firmer footing and February's ISM manufacturing report was nearly flat after ditching seasonal distortions, Institute for Supply Management chair Timothy Fiore told MNI on Friday.

OTHER

OIL (BBG): OPEC+ extended its oil supply cutbacks to the middle of the year in a bid to avert a global surplus and shore up prices. The curbs — which on paper total roughly 2 million barrels a day — will remain in place until the end of June, according to statements from members such as Saudi Arabia, which accounts for half of the pledged reduction. Russia promised to strengthen its role by focusing more on cuts to production than exports.

SHIPPING (POLITICO): Yemen's Iran-backed Houthi group said it will continue to attack British shipping in the Red Sea after sinking the MV Rubymar, which went under over the weekend.

JAPAN (KYODO): The Japanese government is discussing officially stating that the country’s economy has overcome deflation, Kyodo reported Saturday, citing several unidentified people familiar with the matter.

JAPAN (MNI BRIEF): Combined capital investment by non-financial companies excluding software rose 8.0% q/q in Q4 of 2023, accelerating from 1.0% in Q3, a quarterly survey released by the Ministry of Finance showed on Monday.

HONG KONG (BBG): Hong Kong’s property market saw the best weekend in a year after the government lifted decade-long curbs on homebuying. The financial hub’s 10 biggest estates recorded the most sales in 61 weeks with 27 transactions, 3.5 times higher than the previous weekend, according to Midland Realty, which tracks the data as a gauge of second-hand market sentiment.

CHINA

GROWTH (MNI INTERVIEW): Greater fiscal support and higher income growth will boost Chinese consumer activity in 2024, a key driver of GDP growth this year, however, retail sales will likely not match last year's levels, an advisor from a policymaking think tank told MNI in an interview.

GROWTH (BBG): China is expected to set its annual growth rate for 2024 at “around 5%” when the national legislature meets this week, a fairly ambitious target for a government grappling with severe economic challenges.

EQUITIES (SHANGHAI SECURITY NEWS): Institutional investors believe that the funding situation of A-shares has improved significantly and the liquidity crunch caused by recent position adjustment of quantitative funds has ended, Shanghai Securities News reported Monday, citing reports from domestic brokerages.

CAPITAL MARKET (SECURITIES TIMES): Authorities should strengthen top-level design to attract more medium- and long-term funds to enter the capital market, said Jia Wenqin, director of Beijing Securities Regulatory Bureau. These funds face solvency constraints and thus have a relatively conservative investment portfolio, said Jia.

CHINA MARKETS

MNI: PBOC Drains Net CNY319 Bln Via OMO Mon; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY10 billion via 7-day reverse repo on Monday, with the rates unchanged at 1.80%. The reverse repo operation has led to a net drain of CNY319 billion reverse repos after offsetting CNY329 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8040% at 09:45 am local time from the close of 1.8197% on Friday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Friday, compared with the close of 46 on Thursday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1020 on Monday, compared with 7.1059 set on Friday. The fixing was estimated at 7.1890 by Bloomberg survey today.

MARKET DATA

AUSTRALIA MI INFLATION GAUGE FEB. FELL 0.1% M/M TO 4.0% Y/Y; PRIOR 0.3% M/M & 4.6% Y/Y

AUSTRALIA 4Q INVENTORIES FALL 1.7% Q/Q; EST. 0%; PRIOR +1.2%

AUSTRALIA 4Q COMPANY PROFITS RISE 7.4% Q/Q; EST. +1.1%; PRIOR -1.6%

AUSTRALIA JAN. BUILDING APPROVALS FALL 1.0% M/M; EST. +4.0%; PRIOR -10.1%

AUSTRALIA JAN. PRIVATE-SECTOR HOME APPROVALS FALL 9.9% M/M; PRIOR -1.8%

AUSTRALIA FEB. ANZ-INDEED JOB ADVERTISEMENTS FALL 2.8% M/M; PRIOR +3.4%

NZ 4Q TERMS OF TRADE FALLS 7.8% Q/Q; EST. -0.1%; PRIOR -0.6%

NZ 4Q EXPORT VOLUMES RISE 2.6% Q/Q

NZ 4Q IMPORT VOLUMES FALL 7.0% Q/Q

JAPAN 4Q CAPITAL SPENDING RISES 16.4% Y/Y; EST. 2.8%; PRIOR +3.4%

JAPAN 4Q CAPITAL SPENDING EX-SOFTWARE +11.7% Y/Y; EST. 1.5%; PRIOR +1.7%

JAPANESE COMPANIES 4Q PROFITS RISE 13.0% Y/Y; PRIOR +20.1%

JAPANESE COMPANIES 4Q SALES RISE 4.2% Y/Y; PRIOR +5.0%

JAPAN FEB. MONETARY BASE RISES 2.4% Y/Y; PRIOR +4.8%

SOUTH KOREA JAN. INDUSTRIAL OUTPUT FALLS 1.3% M/M; EST. +0.9%; PRIOR -0.5%

SOUTH KOREA JAN. INDUSTRIAL OUTPUT RISES 12.9% Y/Y; EST. +10.0%; PRIOR +6.1%

SOUTH KOREA JAN. CYCLICAL LEADING INDEX UNCHANGED M/M; PRIOR +0.2%

SOUTH KOREA S&P GLOBAL FEB. MANUFACTURING PMI 50.7; PRIOR 51.2

MARKETS

US TSYS: Treasury Futures Off Fridays Highs, Yields 1-2bps Higher

- Jun'24 10Y futures are just off Friday highs trading at 110-29+ down - 03+ from NY closing levels, earlier we made lows of 110-28+ holding above support at 110-26+ (20-day EMA). Initial resistance hold at 111-06 (50-day EMA)

- Treasury yields are giving back some of the moves made on Friday, with yields 1-2bps higher across the curves, the 2Y yield 1.7bps higher to 4.548%, the 10y 1.6bps higher to 4.195%, while the 2y10y -0.304 at -35.456.

- VP Harris is to meet with Israeli War Cabinet Member Gantz at 3pm ET.

- Looking ahead: data resumes Tuesday with S&P Global US Services PMI, ISM Services, Factory and Durable Goods Orders.

JGBS: Futures Stronger, Mid-Range, Tokyo CPI Tomorrow

JGB futures are currently maintaining a mid-range position and are in positive territory, up by 11 points compared to settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Q4 capital spending and company profits data.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session. Newsflow has been light so far.

- The cash JGB curve has twist-steepened, pivoting at the 10s, with yields 1.2bps lower (2-year) to 1.0bp higher (20-year). The benchmark 10-year yield is unchanged at 0.717% versus the Nov-Dec rally low of 0.555%.

- Swaps are richer, with rates flat to 2bps lower. Swap spreads are generally tighter.

- (Bloomberg) -- Japan’s government bonds have cheapened relative to swaps amid expectations that an end of the negative-interest-rate policy in the nation is now just a matter of time, Koichi Sugisaki, executive director at Morgan Stanley MUFG Securities in Tokyo, writes in a note. (See link)

- Tomorrow, the local calendar sees Tokyo CPI and Jibun Bank PMI Composite & Services data, along with 10-year supply. BoJ Governor Ueda is also due to give a speech at FIN/SUM 2024.

AUSSIE BONDS: Richer, Narrow Ranges, Q4 GDP On Wednesday

ACGBs (YM +3.0 & XM +4.5) sit slightly stronger after dealing with narrow ranges. Today’s local data drop (the Melbourne Institute Inflation Gauge, Q4 Company Profits and Inventories and January Building Approvals) failed to be market-moving.

- (AFR) New house approvals have fallen to their lowest level in nearly 12 years as higher borrowing and building costs put buyers, particularly in NSW and Victoria off committing to new homes, the latest official figures show. (See link)

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session. Newsflow has been light so far.

- Cash ACGBs are 4bps richer, with the AU-US 10-year yield differential 1bp higher at -10bps.

- Swap rates are 3-4bps lower, with EFPs wider.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is flat to 3bps softer across meeting out to Dec-24. A cumulative 39bps of easing is priced by year-end.

- Tomorrow, the local calendar sees Judo Bank PMI Composite & Services, Q4 Net Exports of GDP and BoP Current Account Balance. Q4 GDP is due on Wednesday.

NZGBS: Closed Richer & At Best Levels

NZGBs concluded the session 2-4bps richer, reaching their peak levels for the day, accompanied by a steeper 2/10 curve. This movement marks a cumulative decline in benchmark yields of 15-25bps since the RBNZ decision last Wednesday. Additionally, the 2/10 curve has steepened by 10bps.

- With today’s domestic data calendar relatively light, local participants have been content to extend strength sparked by Friday’s post-ISM rally in US tsys. This came despite US tsys dealing 1-2bps heavier in today’s Asia-Pac session. News flow has been light.

- Today the NZ Government announced that it plans to spend NZ$20bn over three years on transport, including 15 new roads of national significance. It will raise the vehicle licensing fee in 2025 and 2026.

- Swap rates closed flat to 3bps lower, with the 2s10s curve and the swap box flatter.

- RBNZ dated OIS pricing is little changed. A cumulative 52bps of easing is priced by year-end.

- Tomorrow, the local calendar sees NZ Government's 7-Month Financial Statements and ANZ Commodity Prices.

FOREX: USD Recoups Early Losses, But Recent Ranges Hold

G10 FX trading has started the week in a fairly muted fashion. The BBDXY sits a touch below end Friday levels, last near 1241.85. We sit above earlier lows near 1240.8).

- In the cross asset space, US equity futures sit mixed, after posting strong cash gains in Friday trade. US yields opened higher and have generally held gains as the session has progressed. The front end has led, up nearly 2bps, but this is unwinding only a small part of Friday's fall.

- USD/JPY was weaker in the first part of trade, but dips sub 150.00 were supported. We were last near 150.25/30, which is at session highs. We had much stronger than expected Q4 capex data earlier, which should lead to positive GDP revisions for the quarter, but this didn't shift yen sentiment.

- AUD and NZD also sit lower, unable to hold earlier gains. AUD/USD was last near 0.6520. Earlier data was on balance weaker than expected, with potential downside risks for Q4's GDP print (due Wed) after an inventory drag. Iron ore prices unable to find upside traction has likely been another headwind. Still, we sit comfortably above pre US data levels from Friday around 0.6490.

- NZD/USD has tracked a similar range, last near 0.6095, off nearly 0.20% for the session. AUD/NZD touched initial resistance of 1.0700, but has been unable to break back above yet, a break here could open a further move to 1.0740 (Feb 7 highs). In the options space, US$420.5m Puts with a Strike of 1.0700 expire at the NY cut today.

- Later the Fed’s Harker speaks but there is no data of note.

ASIA STOCKS: HK & China Equities Recoup Earlier Losses, Property Underperforms

Hong Kong and China equities have opened mostly lower to start the week, although we are off lows from earlier in the day. The market is eagerly awaiting the National Peoples Congress on Tuesday to hear about further policies that could stimulate the markets. Recent policies have been seen to be supportive but there are still worries about whether or not this has just short-term fixes, as the property market still continues to struggle.

- Hong Kong Equity markets are mostly off lows from earlier today, with the HSI down 0.20% after being down 0.70%, while HSTech turned positive earlier however trades down 0.25% at the moment, while the Mainland Property Index is the worst performer down 2.80% and down 8.22% over the past week. China Mainland Equities are performing better with equities now mostly higher, the CSI 300 is up 0.10% while the CSI1000 is flat, the ChiNext is out-performing the wider market up 0.65 for the day.

- China Northbound flows were -5.333b yuan on Friday, with the 5-day average now 4.70b, while the 20-day is at 3.08b yuan.

- The Hong Kong Budget released last week was seen to be underwhelming for the most part other than for the property market after the government removed all property curbs, and over the weekend the 10 major residential estates booked 27 sales, 3.5 times the previous weekend and the highest sales number in more than a year

- Earlier, China Feb. Vehicle Inventory Alert Rises to 64.1 vs 59.9 prior.

- Looking ahead, Tuesday Premier Li Qiang will deliver the Government Work Report at the Nationals People Congress, while Caixin China PMI data is due out.

ASIA PAC EQUITIES: Asian Equities Mostly Higher, Japan's Nikkei 225 Breaks 40,000

Regional Asian Equities are mostly higher today, following on from the US on Friday. Tech names are the top performing sector in the region, Japan's Nikkei 225 break 40,000 for the first time while South Korea is back from their break on Friday.

- Japan equities continue to push higher after recently breaking all-time highs, markets are largely following the US markets move as there has been little in the way on local market headlines. The Nikkei 225 is now trading at 40,100 up 0.48% and importantly above psychological level of 40,000 level for the first time, while the TOPIX has lagged the move higher and still sits about 6% below it's all-time highs at 2,707 down 0.05%. Earlier Japan had Capital Spending data coming in at 16.4% vs 2.8% expected, while Monetary Base was 2.4% vs 4.8% prior

- South Korean equities are back from their break on Friday and are pushing higher, with the KOSPI up 1.35%. Electrical and electronic equipment stocks led the market higher after Dell surged 32% on Friday after better-than-expected results, fuelled by demand for information technology equipment. Foreign equity inflows are also picking back up, with $355m of inflows today. Earlier SK had industrial production data out coming in at 12.9% vs 10% expected, while S&P Global SK PMI was 50.7 vs 51.2 prior.

- Taiwan Equities are benefitting for higher semiconductor equity prices, after the Philadelphia Stock Exchange Semiconductor Index closed up 4.29% on Friday. the Taiex is currently up 1.93%, looking forward Taiwan has CPI on Thursday.

- Australian equities were up 0.30% during the morning session, however Building approval data at -1.0% vs 4.0% expected pushed the market lower with Mining and Health Care sectors offsetting gains in the Financial and Real Estate sectors. While earlier Melbourne Institute Inflation was out showing inflation had eased substantially to 4.00% vs 4.6% in January the lowest since April 2022. The ASX 200 finished down 0.13%.

- Elsewhere in SEA equities are mixed, with NZ closing down 0.17%, Indonesian equities down 0.16%, Singapore down 0.35% while Malaysian equities up 0.37% and Philippines equities up 1.18% are the top performers.

OIL: Crude Steady As Waits For China & Gaza Outcomes

Oil prices have held onto Friday’s gains during APAC trading with little reaction to the widely expected extension of OPEC output cuts to the end of June. WTI has been oscillating around the $80 mark and is currently at $79.94 after a high of $80.37. Brent is 0.1% higher at $83.64/bbl after rising to $83.97. The USD index is down only moderately.

- OPEC will extend its 2mbd reductions to the end of June with Russia focusing on cutting production rather than exports. The action is aimed at supporting prices and avoiding excess supply. Higher prices are also needed by many producers to shore up government finances.

- Negotiations continue for a Gaza ceasefire deal before the start of Ramadan next week but the Israelis didn’t send a delegation to yesterday’s talks after Hamas would not name the remaining hostages. The stall in progress towards a truce is providing support to oil prices.

- China’s National People’s Congress is to close on March 11 and the 2024 growth target is to be announced plus any economic policies. Crude sell offs are often driven by market concerns re demand from China, the world’s largest importer.

- Later the Fed’s Harker speaks but there is no data of note.

GOLD: Surges Friday After Weaker Than Expected ISM Data

Gold is little changed in the Asia-Pac session, after closing 1.9% higher at $2082.92 on Friday.

- According to MNI’s technicals team, gold surged beyond a key resistance at $2065.5 (Feb 1 high) and stopped marginally short of $2088.5 (Dec 28 high).

- The move in bullion was driven by lower Treasury yields and a softer USD index following the release of weaker-than-expected ISM Manufacturing data. Continued Red Sea geopolitical tension added to the bid tone.

- Balanced commentary from several Fed speakers and the preview of Chairman Powell's monetary policy report to Congress this week did little to forestall the drop in Treasury yields.

- US data resumes on Tuesday with S&P Global US Services PMI, ISM Services, Factory and Durable Goods Orders.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/03/2024 | 0700/0200 | * |  | TR | Turkey CPI |

| 04/03/2024 | 0730/0830 | *** |  | CH | CPI |

| 04/03/2024 | 1600/1100 |  | US | Philly Fed's Pat Harker | |

| 04/03/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 04/03/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 05/03/2024 | 2330/0830 | ** |  | JP | Tokyo CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.